Answers and Solutions: 5 – 1

Chapter 5

Bond Valuation

ANSWERS TO END-OF-CHAPTER QUESTIONS

5-1 a. A bond is a promissory note issued by a business or a governmental unit. Treasury

bonds, sometimes referred to as government bonds, are issued by the Federal

government and are not exposed to default risk. Corporate bonds are issued by

corporations and are exposed to default risk. Different corporate bonds have different

levels of default risk, depending on the issuing company’s characteristics and on the

Maturity dates generally range from 10 to 40 years from the time of issue. A call

provision may be written into a bond contract, giving the issuer the right to redeem the

bonds under specific conditions prior to the normal maturity date. A bond’s coupon, or

coupon payment, is the dollar amount of interest paid to each bondholder on the interest

payment dates. The coupon is so named because bonds used to have dated coupons

attached to them which investors could tear off and redeem on the interest payment

dates. The coupon interest rate is the stated rate of interest on a bond.

Answers and Solutions: 5 – 2

d. Most bonds contain a call provision, which gives the issuing corporation the right to

call the bonds for redemption. The call provision generally states that if the bonds are

called, the company must pay the bondholders an amount greater than the par value, a

market.

e. Convertible bonds are securities that are convertible into shares of common stock, at a

fixed price, at the option of the bondholder. Bonds issued with warrants are similar to

convertibles. Warrants are options which permit the holder to buy stock for a stated

price, thereby providing a capital gain if the stock price rises. Income bonds pay

interest only if the interest is earned. These securities cannot bankrupt a company, but

from an investor’s standpoint they are riskier than “regular” bonds. The interest rate of

an indexed, or purchasing power, bond is based on an inflation index such as the

consumer price index (CPI), so the interest paid rises automatically when the inflation

rate rises, thus protecting the bondholders against inflation.

h. Corporations can influence the default risk of their bonds by changing the type of bonds

they issue. Under a mortgage bond, the corporation pledges certain assets as security

i. A development bond is a tax-exempt bond sold by state and local governments whose

proceeds are made available to corporations for specific uses deemed (by Congress) to

be in the public interest. Municipalities can insure their bonds, in which an insurance

company guarantees to pay the coupon and principal payments should the issuer

default. This reduces the risk to investors who are willing to accept a lower coupon

rate for an insured bond issue vis-a-vis an uninsured issue. Bond issues are normally

assigned quality ratings by major rating agencies, such as Moody’s Investors Service

j. The real risk-free rate is the rate that a hypothetical riskless security pays each moment

if zero inflation were expected. The real risk-free rate is not constant—r* changes over

time depending on economic conditions. The real risk-free rate could also be called the

pure rate of interest since it is the rate of interest that would exist on very short-term,

default-free U.S. Treasury securities if the expected rate of inflation were zero. It has

k. The inflation premium is the premium added to the real risk-free rate of interest to

compensate for the expected loss of purchasing power. The inflation premium is the

average rate of inflation expected over the life of the security. Default risk is the risk

that a borrower will not pay the interest and/or principal on a loan as they become due.

l. Interest rate risk arises from the fact that bond prices decline when interest rates rise.

Under these circumstances, selling a bond prior to maturity will result in a capital loss,

and the longer the term to maturity, the larger the loss. Thus, a maturity risk premium

m. The term structure of interest rates is the relationship between yield to maturity and

term to maturity for bonds of a single risk class. The yield curve is the curve that results

when yield to maturity is plotted on the Y-axis with term to maturity on the X-axis.

5-2 False. Short-term bond prices are less sensitive than long-term bond prices to interest rate

changes because funds invested in short-term bonds can be reinvested at the new interest

rate sooner than funds tied up in long-term bonds.

5-3 The price of the bond will fall and its YTM will rise if interest rates rise. If the bond still

has a long term to maturity, its YTM will reflect long-term rates. Of course, the bond’s

5-4 If interest rates decline significantly, the values of callable bonds will not rise by as much

as those of bonds without the call provision. It is likely that the bonds would be called by

the issuer before maturity, so that the issuer can take advantage of the new, lower rates.

5-5 From the corporation’s viewpoint, one important factor in establishing a sinking fund is

that its own bonds generally have a higher yield than do government bonds; hence, the

company saves more interest by retiring its own bonds than it could earn by buying

government bonds. This factor causes firms to favor the second procedure. Investors also

Answers and Solutions: 5 – 6

SOLUTIONS TO END–OF-CHAPTER PROBLEMS

5-1 With your financial calculator, enter the following:

N = 12; I/YR = YTM = 9%; PMT = 0.08 1,000 = 80; FV = 1000; PV = VB = ?

5-2 With your financial calculator, enter the following:

5-3 With your financial calculator, enter the following to find the current value of the bonds,

so you can then calculate their current yield:

N = 7; I/YR = YTM = 8; PMT = 0.09 1,000 = 90; FV = 1000; PV = VB = ?

Answers and Solutions: 5 – 7

5-4 r* = 4%; I1 = 2%; I2 = 4%; I3 = 4%; MRP = 0; rT-2 = ?; rT-3 = ?

r = r* + IP + DRP + LP + MRP.

5-5 rT-10 = 6%; rC-10 = 9%; LP = 0.5%; DRP = ?

r = r* + IP + DRP + LP + MRP.

5-6 r* = 3%; IP = 3%; rT-2 = 6.3%; MRP2 = ?

Answers and Solutions: 5 – 8

5-7 The problem asks you to find the price of a bond, given the following facts:

5-8 With your financial calculator, enter the following to find YTM:

N = 10 2 = 20; PV = -1100; PMT = 0.08/2 1,000 = 40; FV = 1000; I/YR = YTM = ?

YTM = 3.31% 2 = 6.62%.

5-9 a.

1. 5%: Bond L: Input N = 15, I/YR = 5, PMT = 100, FV = 1000, PV = ?, PV =

$1,518.98.

Bond S: Change N = 1, PV = ? PV = $1,047.62.

b. Think about a bond that matures in one month. Its present value is influenced primarily

by the maturity value, which will be received in only one month. Even if interest rates

double, the price of the bond will still be close to $1,000. A one-year bond’s value

would fluctuate more than the one-month bond’s value because of the difference in the

Answers and Solutions: 5 – 9

5-10 a. Calculator solution:

1. Input N = 5, PV = -829, PMT = 90, FV = 1000, I/YR = ? I/YR = 13.98%.

2. Change PV = -1104, I/YR = ? I/YR = 6.50%.

5-11 N = 7; PV = −1000; PMT = 14%(1,000) =140; FV = (1 + 0.09)(1,000) = 1090; I/YR = ?

Solve for I/YR = 14.82%.

5-12 a. Using a financial calculator, input the following:

N = 20, PV = -1100, PMT = 60, FV = 1000, and solve for I/YR = 5.1849%.

Answers and Solutions: 5 – 10

5-13 The problem asks you to solve for the YTM, given the following facts:

N = 5, PMT = 80, and FV = 1000. In order to solve for I/YR we need PV.

However, you are also given that the current yield is equal to 8.21%. Given this

information, we can find PV.

5-14 The problem asks you to solve for the current yield, given the following facts: N = 14,

I/YR = 10.5883/2 = 5.2942, PV = −1020, and FV = 1000. In order to solve for the current

5-15 The bond is selling at a large premium, which means that its coupon rate is much higher

than the going rate of interest. Therefore, the bond is likely to be called—it is more likely

5-16 The price of a perpetuity is: Price = (Annual payment)/(Interest rate). For example, the

price of a $100 perpetuity at an 8% interest rate is: $100/0.08 = $1,250.

The prices for the other cases are found with a financial calculator. For example, the price

of a 10-year, 10% bond is found using these inputs: N = 10, I/YR = 10, PV = ?, PMT =

−(0.10 x 1000) = −100, FV = −1000; solve for PV = 1,134.20. The same approach can be

Answers and Solutions: 5 – 11

used for the zero coupon bonds by substituting zero for the payment.

Price at 8%

Price at 7%

Pctge. change

10-year zero

5-year zero

30-year zero

$100 perpetuity

5-17 Using a financial calculator, the price of Bond C is found using these inputs: N = 4 − Yeart,

I/YR = 9.6, PV = ?, PMT = −(0.10 x 1000) = −100, FV = −1000; solve for PV. For example, the

price of Bond C at Year0 is: N = 4, I/YR = 9.6, PV = ?, PMT = −(0.10 x 1000) = −100, FV =

Price of Bond C

Price of Bond Z

5-18 r = r* + IP + MRP + DRP + LP.

r* = 0.02.

IP = [0.03 + 0.04 + (5)(0.035)]/7 = 0.035.

MRP = 0.0005(6) = 0.003.

Answers and Solutions: 5 – 12

5-19 First, note that we will use the equation rt = 3% + IPt + MRPt. We have the data needed to

find the IPs:

Answers and Solutions: 5 – 13

5-20 Basic relevant equations:

rt = r* + IPt + DRPt + MRPt + LPt.

But here IP is the only premium, so rt = r* + IPt.

IPt = Avg. inflation = (I1 + I2 + …)/N.

We can set up this table:

r* I Avg. I = IPt r = r* + IPt

1 2 3 3%/1 = 3% 5%

2 2 I (3% + I)/2 = IP2

3 2 I (3% + I + I)/3 = IP3 r3 = 7%, so IP3 = 7% – 2% = 5%.

5-21 a. The bonds now have an 8-year, or a 16-semiannual period, maturity, and their value is

calculated as follows:

Calculator solution: Input N = 16, I/YR = 3, PMT = 50, FV = 1000,

PV = ? PV = $1,251.22.

Answers and Solutions: 5 – 14

5-22 a. Find the YTM as follows:

N = 10, PV = -1200, PMT = 110, FV = 1000

I/YR = YTM = 8.02%.

d. Similarly from above, YTC can be found, if called in each subsequent year.

If called in Year 6:

N = 6, PV = –1200, PMT = 110, FV = 1080

I/YR = YTC = 7.80%.

If called in Year 7:

N = 7, PV = –1200, PMT = 110, FV = 1070

I/YR = YTC = 7.95%.

Answers and Solutions: 5 – 15

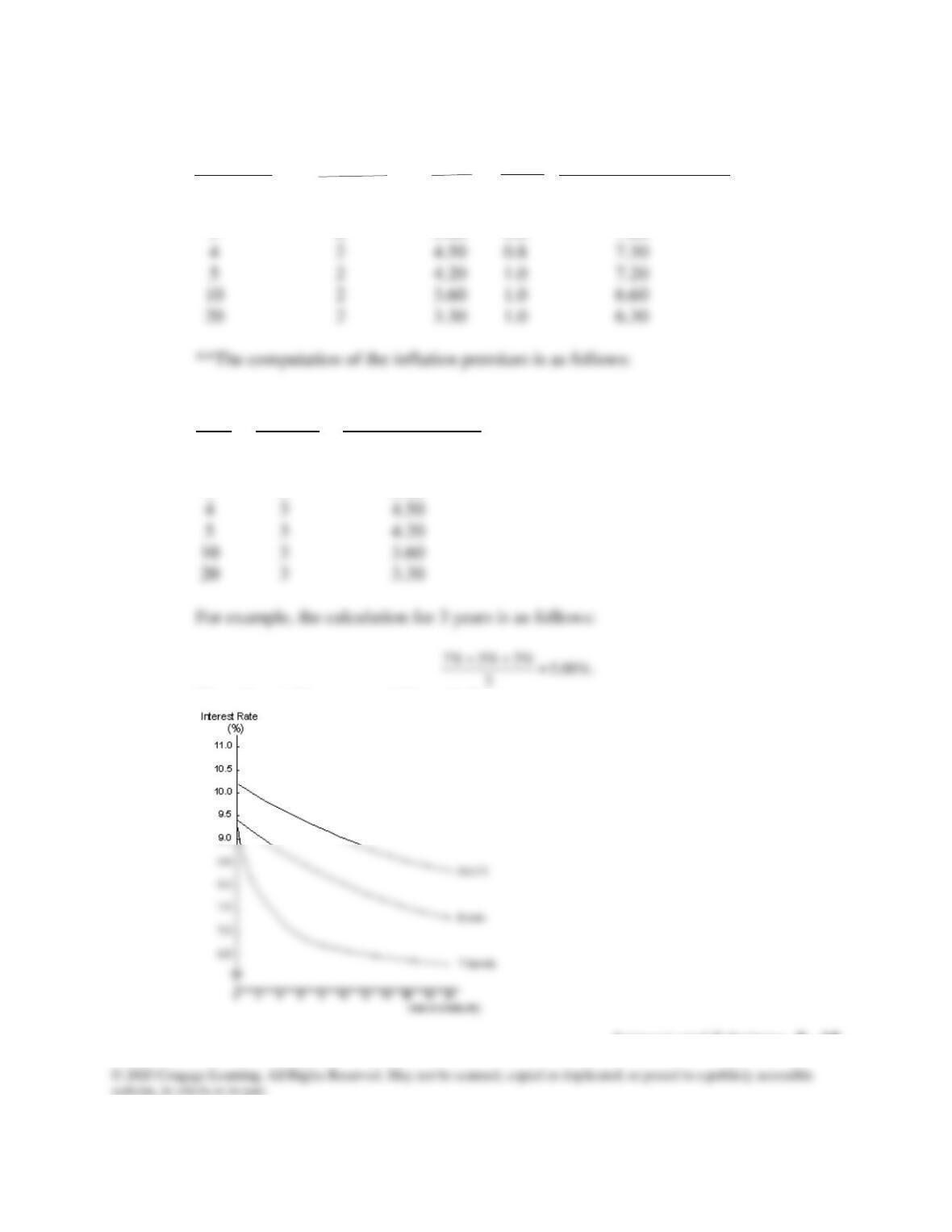

5-23 a. Real

Years to Risk-Free

Maturity Rate (r*) IP** MRP rT = r* + IP + MRP

1 2% 7.00% 0.2% 9.20%

2 2 6.00 0.4 8.40

3 2 5.00 0.6 7.60

Expected Average

Year Inflation Expected Inflation

1 7% 7.00%

2 5 6.00

3 3 5.00

Thus, the yield curve would be as follows:

Answers and Solutions: 5 – 16

b. The interest rate on the ExxonMobil bonds has the same components as the Treasury

securities, except that the ExxonMobil bonds have default risk, so a default risk

premium must be included. Therefore,

c. LILCO bonds would have significantly more default risk than either Treasury securities

or Exxon bonds, and the risk of default would increase over time due to possible

financial deterioration. In this example, the default risk premium was assumed to be

Answers and Solutions: 5 – 17

SOLUTION TO SPREADSHEET PROBLEM

5-24 The detailed solution for the problem is in the file Ch05 P24 Build a Model Solution.xlsx

and is available on the instructor’s side of the textbook’s web site.

Mini Case: 5 – 18

MINI CASE

Sam Strother and Shawna Tibbs are vice-presidents of Mutual of Seattle Insurance

Company and co-directors of the company’s pension fund management division. A major

new client, the Northwestern Municipal Alliance, has requested that Mutual of Seattle

present an investment seminar to the mayors of the represented cities, and Strother and

Tibbs, who will make the actual presentation, have asked you to help them by answering the

following questions. Because the Boeing Company operates in one of the league’s cities, you

are to work Boeing into the presentation.

a. What are the key features of a bond?

Answer:

1. Par or face value. We generally assume a $1,000 par value, but par can be anything,

and often $5,000 or more is used. With registered bonds, which is what are issued

today, if you bought $50,000 worth, that amount would appear on the certificate.

Mini Case: 5 – 19

b. What are call provisions and sinking fund provisions? Do these provisions make

bonds more or less risky?

Answer: A call provision is a provision in a bond contract that gives the issuing corporation the

right to redeem the bonds under specified terms prior to the normal maturity date. The

call provision generally states that the company must pay the bondholders an amount

Mini Case: 5 – 20

c. How is the value of any asset whose value is based on expected future cash flows

determined?

Answer: 0 1 2 3 n

| | | | • • • |

CF1 CF2 CF3 CFN

PV CF1

PV CF2