Answers and Solutions: 4 -21

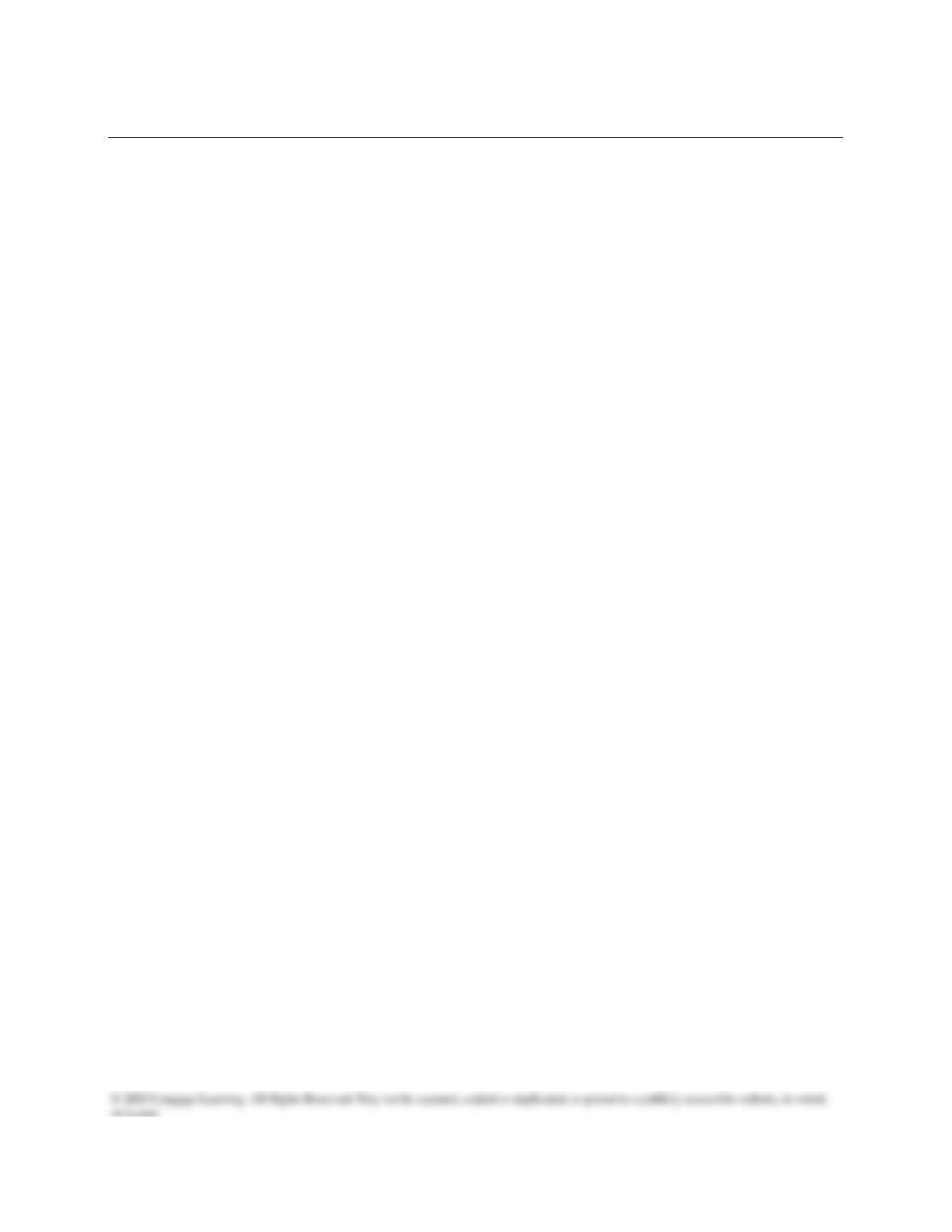

4-34 Information given:

The nominal time line is shown below, with a different payment each period and a FV of

a nominal $1 millon:

$1,000,000 / (1 + Inflation)N = $1,000,000 / (1 + 0.03)25 = $477,605.57.

This is a growing annuity, with a nominal rate of 8% and an inflation rate of 3%. You

should use the real rate in the calculator: rr = [(1 + rNOM)/(1 + Inflation)] – 1.0 =

[1.08/1.03] – 1.0 = .0485437 = 4.85437%.

So the “real” time line in expressed in today’s purchasing power is:

Answers and Solutions: 4 – 22

SOLUTION TO SPREADSHEET PROBLEM

4-35 The detailed solution for the spreadsheet problem, Ch04 P35 Build a Model Solution.xlsx,

is available on the textbook’s Web site.

Mini Case: 4 -23

MINI CASE

Assume that you are nearing graduation and have applied for a job with a local bank. As

part of the bank’s evaluation process, you have been asked to take an examination that covers

several financial analysis techniques. The first section of the test addresses discounted cash

flow analysis. See how you would do by answering the following questions.

a. Draw time lines for (a) a $100 lump sum cash flow at the end of year 2, (b) an

ordinary annuity of $100 per year for 3 years, and (c) an uneven cash flow stream

of -$50, $100, $75, and $50 at the end of years 0 through 3.

Answer: (Begin by discussing basic discounted cash flow concepts, terminology, and solution

methods.) A time line is a graphical representation which is used to show the timing

of cash flows. The tick marks represent end of periods (often years), so time 0 is today;

time 1 is the end of the first year, or 1 year from today; and so on.

Mini Case: 4 – 24

b. 1. What is the future value of an initial $100 after 3 years if it is invested in an

account paying 10% annual interest?

Answer: Show dollars corresponding to question mark, calculated as follows:

0 1 2 3

| | | |

100 FV = ?

After 1 year:

FV1 = PV + I1 = PV + PV(I) = PV(1 + I) = $100(1.10) = $110.00.

10%

Mini Case: 4 -25

b. 2. What is the present value of $100 to be received in 3 years if the appropriate

interest rate is 10%?

Answer: Finding present values, or discounting (moving to the left along the time line), is the

reverse of compounding, and the basic present value equation is the reciprocal of the

compounding equation:

Mini Case: 4 – 26

c. We sometimes need to find out how long it will take a sum of money (or anything

else) to grow to some specified amount. For example, if a company’s sales are

growing at a rate of 20% per year, how long will it take sales to double?

Answer: We have this situation in time line format:

0 1 2 3 3.8 4

| | | | | |

-1 2

20%

Mini Case: 4 -27

d. If you want an investment to double in 3 years, what interest rate must it earn?

Answer: 0 1 2 3

| | | |

-1 2

1(1 + I) 1(1 + I)2 1(1 + I)3

FV = $1(1 + I)3 = $2.

e. What is the difference between an ordinary annuity and an annuity due? What

type of annuity is shown below? How would you change it to the other type of

annuity?

0 1 2 3

| | | |

100 100 100

Answer: This is an ordinary annuity—it has its payments at the end of each period; that is, the

first payment is made 1 period from today. Conversely, an annuity due has its first

Mini Case: 4 – 28

f. 1. What is the future value of a 3-year ordinary annuity of $100 if the appropriate

interest rate is 10%?

Answer: 0 1 2 3

| | | |

100 100 100

110

121

$331

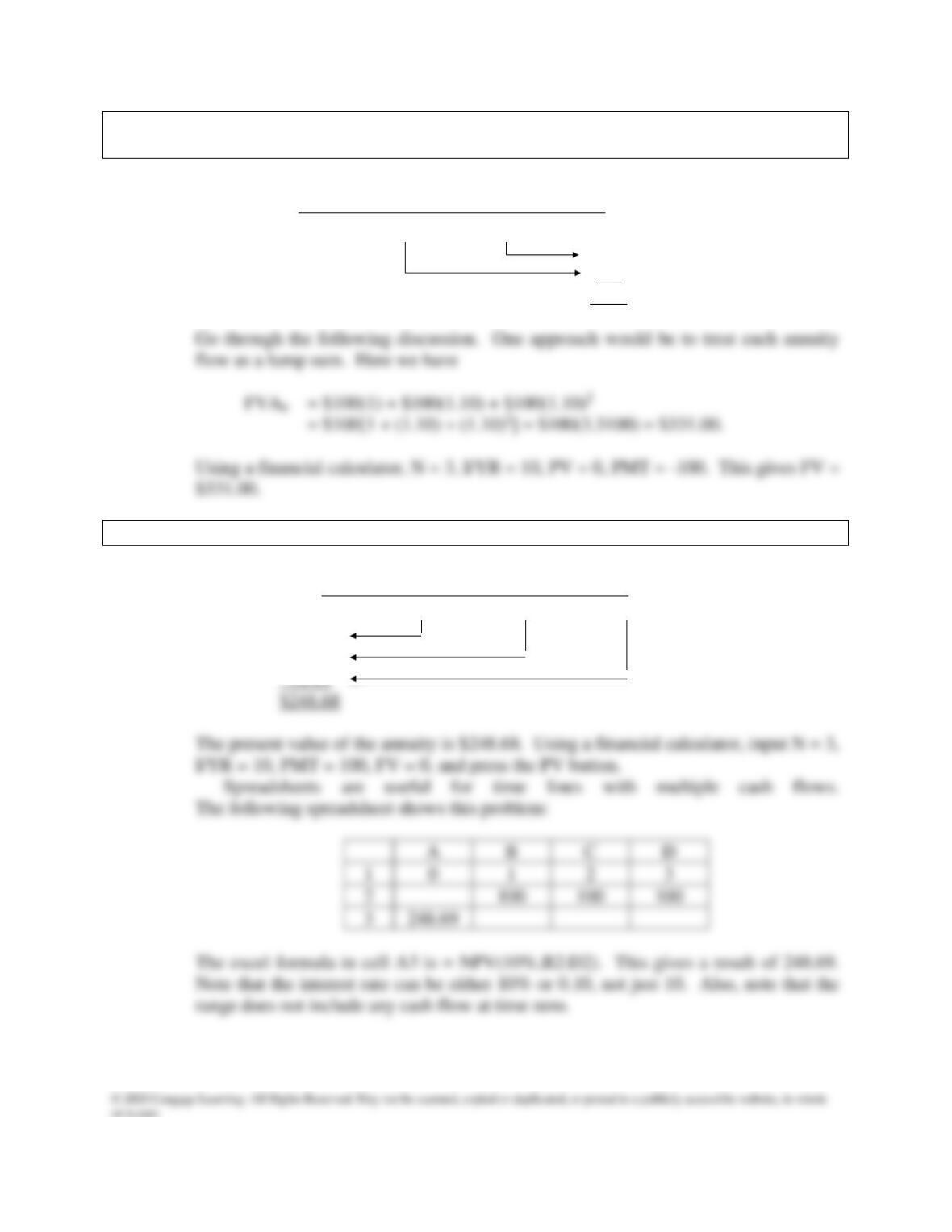

f. 2. What is the present value of the annuity?

Answer: 0 1 2 3

| | | |

100 100 100

90.91

82.64

10%

10%

Mini Case: 4 -29

f. 3. What would the future and present values be if the annuity were an annuity due?

Answer: If the annuity were an annuity due, each payment would be shifted to the left, so each

payment is compounded over an additional period or discounted back over one less

period.

To find the future value of an annuity due use the following formula:

Mini Case: 4 – 30

g. What is the present value of the following uneven cash flow stream? The

appropriate interest rate is 10%, compounded annually.

0 1 2 3 4 years

| | | | |

0 100 300 300 -50

Answer: Here we have an uneven cash flow stream. The most straightforward approach is to

find the PVs of each cash flow and then sum them as shown below:

h. 1. Define (a) the stated, or quoted, or nominal rate, (iNom), and (b) the periodic rate

(iPer).

ANSWER: The quoted, or nominal, rate is merely the quoted percentage rate of return. The

Mini Case: 4 -31

h. 2. Will the future value be larger or smaller if we compound an initial amount more

often than annually, for example, every 6 months, or semiannually, holding the

stated interest rate constant? Why?

Answer: Accounts that pay interest more frequently than once a year, for example, semiannually,

h. 3. What is the future value of $100 after 5 years under 12% annual compounding?

Semiannual compounding? Quarterly compounding? Monthly compounding?

Daily compounding

Answer: Under annual compounding, the $100 is compounded over 5 annual periods at a 12.0

percent periodic rate:

INOM = 12%.