Chapter 4 CFIN6

Chapter 4 Solutions

(Most solutions are rounded in the final answers, not in the intermediate computations.)

0 1 2 3 4

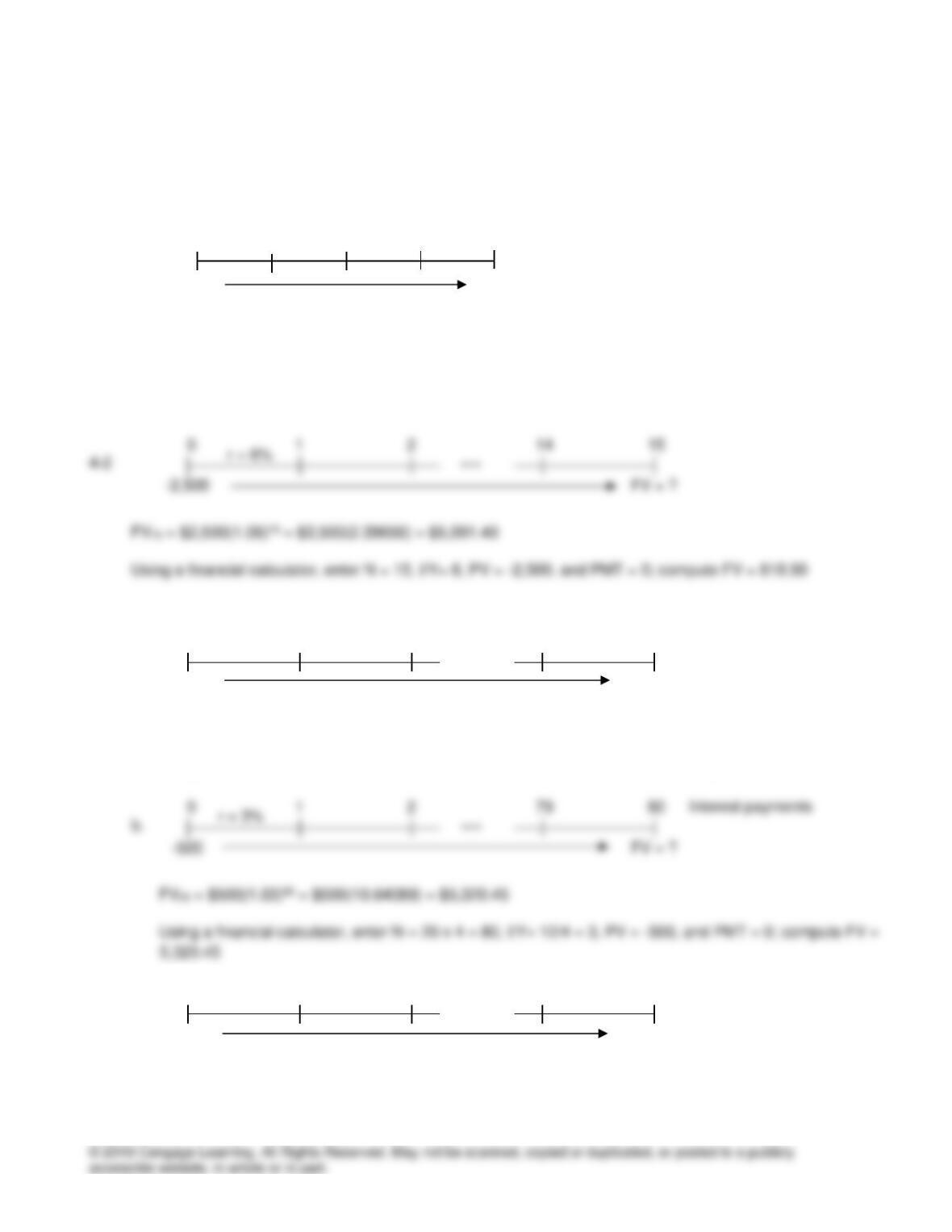

4-1

-700 FV = ?

FV4 = $700(1.04)4 = $700(1.16986) = $818.90

Using a financial calculator, enter N = 4, I/Y= 4, PV = -700, and PMT = 0; compute FV = 818.90

r = 6%

…

0 1 2 14 20

4-3 a.

–500 FV = ?

FV20 = $500(1.12)20 = $500(9.64629) = $4,823.15

Using a financial calculator, enter N = 20, I/Y= 12, PV = –500, and PMT = 0; compute FV = 4,823.15

r = 3%

Interest payments

…

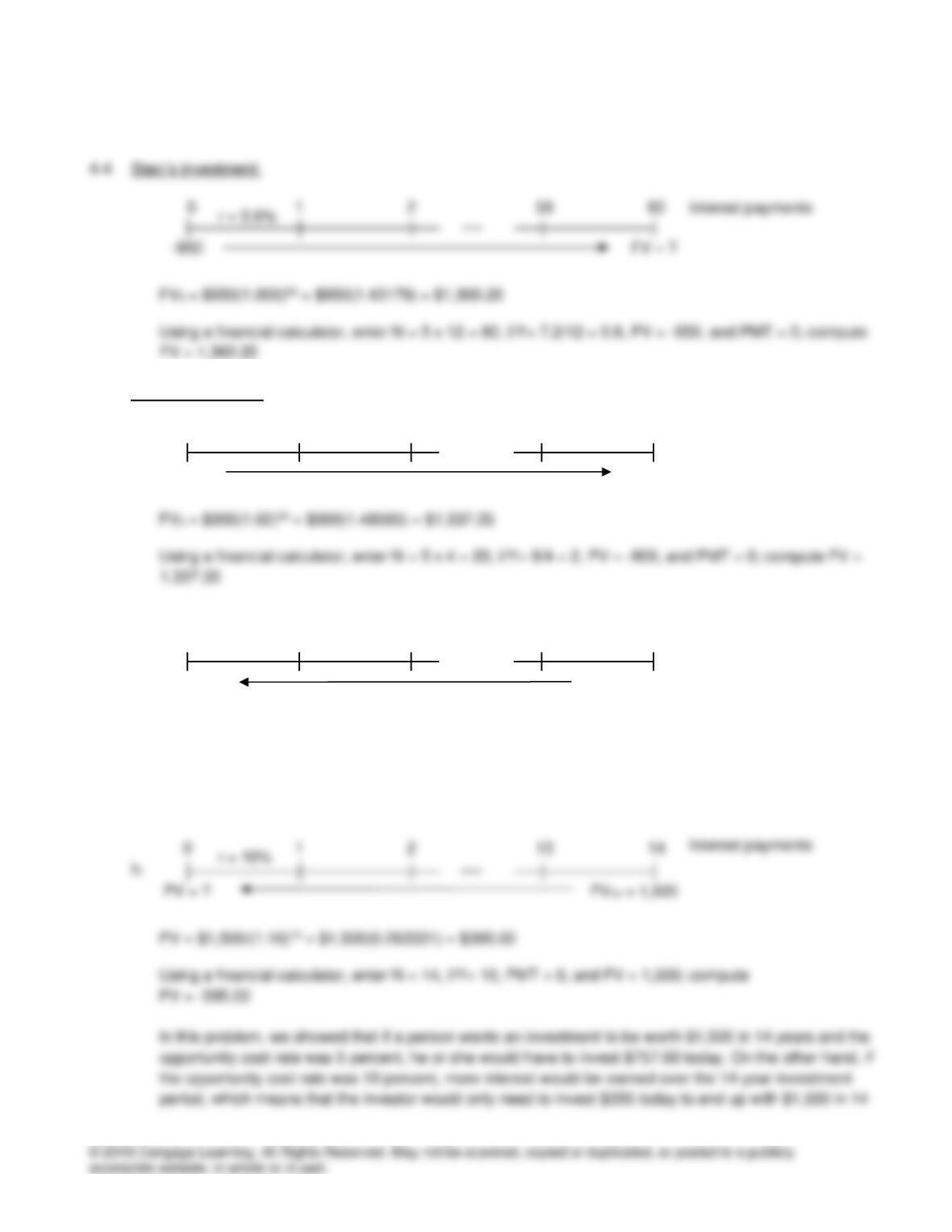

0 1 2 239 240

c.

–500 FV = ?

FV20 = $500(1.01)240 = $500(10.89255) = $5,446.28

r = 4%

r = 12%

…

r = 1%

Interest payments

Interest payments

…

Chapter 4 CFIN6

Using a financial calculator, enter N = 20 x 12 = 240, I/Y= 12/12 = 1, PV = –500, and PMT = 0; compute

FV = 5,446.28

r = 0.6%

Interest payments

…

Shelli’s investment:

0 1 2 19 20

–900 FV = ?

0 1 2 13 14

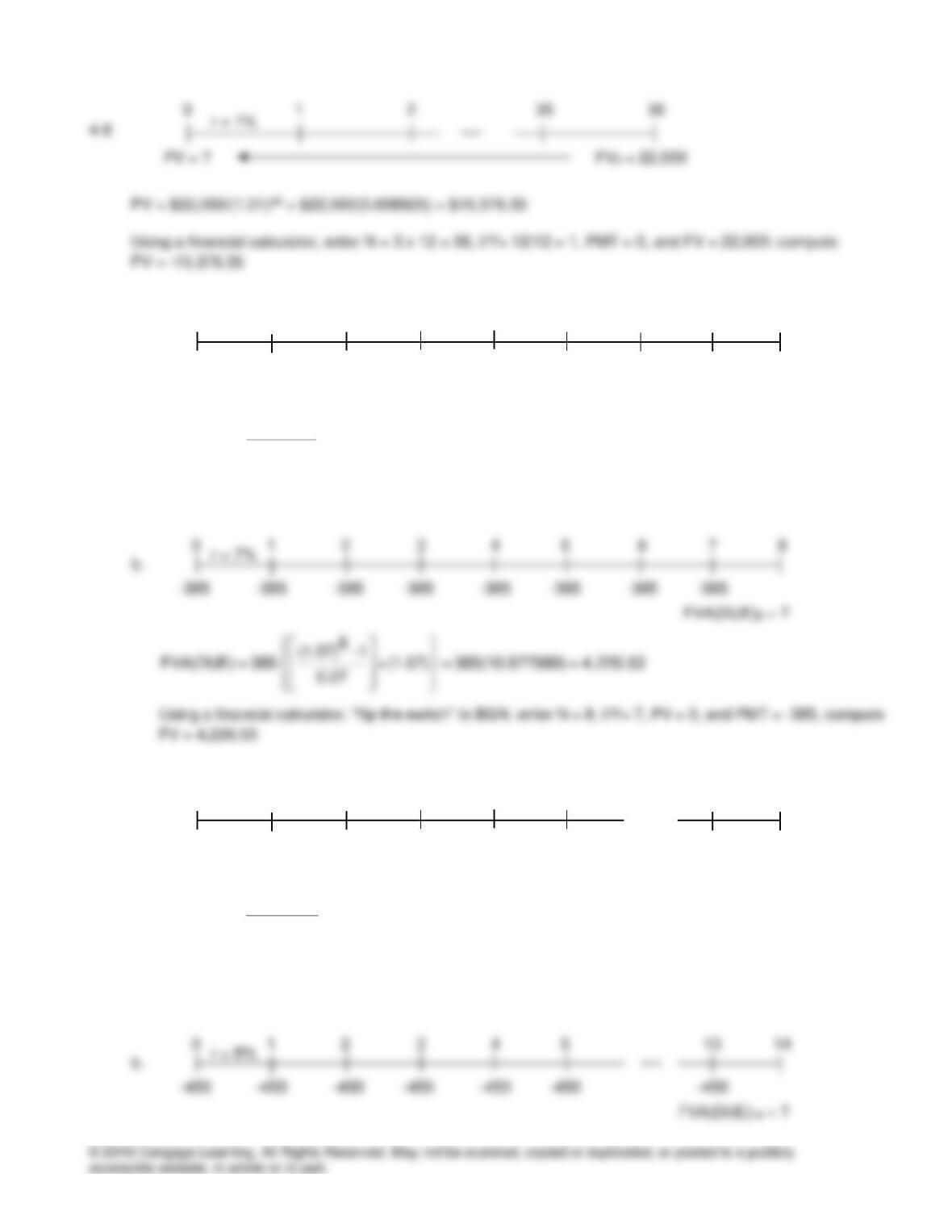

4-5 a.

PV = ? FV14 = 1,500

PV = $1,500/(1.05)14 = $1,500(0.505068) = $757.60

Using a financial calculator, enter N = 14, I/Y= 5, PMT = 0, and FV = 1,500; compute

PV = -757.60

r = 10%

Interest payments

…

r = 2%

Interest payments

r = 5%

Interest payments

…

…

Chapter 4 CFIN6

years. Simply stated, the more interest you can earn during an investment period, the less you need to

invest today to receive a particular amount in the future.

r = 7%

Interest payments

…

0 1 2 3 4 5

4-7 a.

PV = ? FV5 = 2,500

PV = $2,500/(1.09)5 = $2,500(0.649931) = $1,624.83

Using a financial calculator, enter N = 5, I/Y= 9, PMT = 0, and FV = 2,500; compute

PV = -1,624.83

Interest payments

…

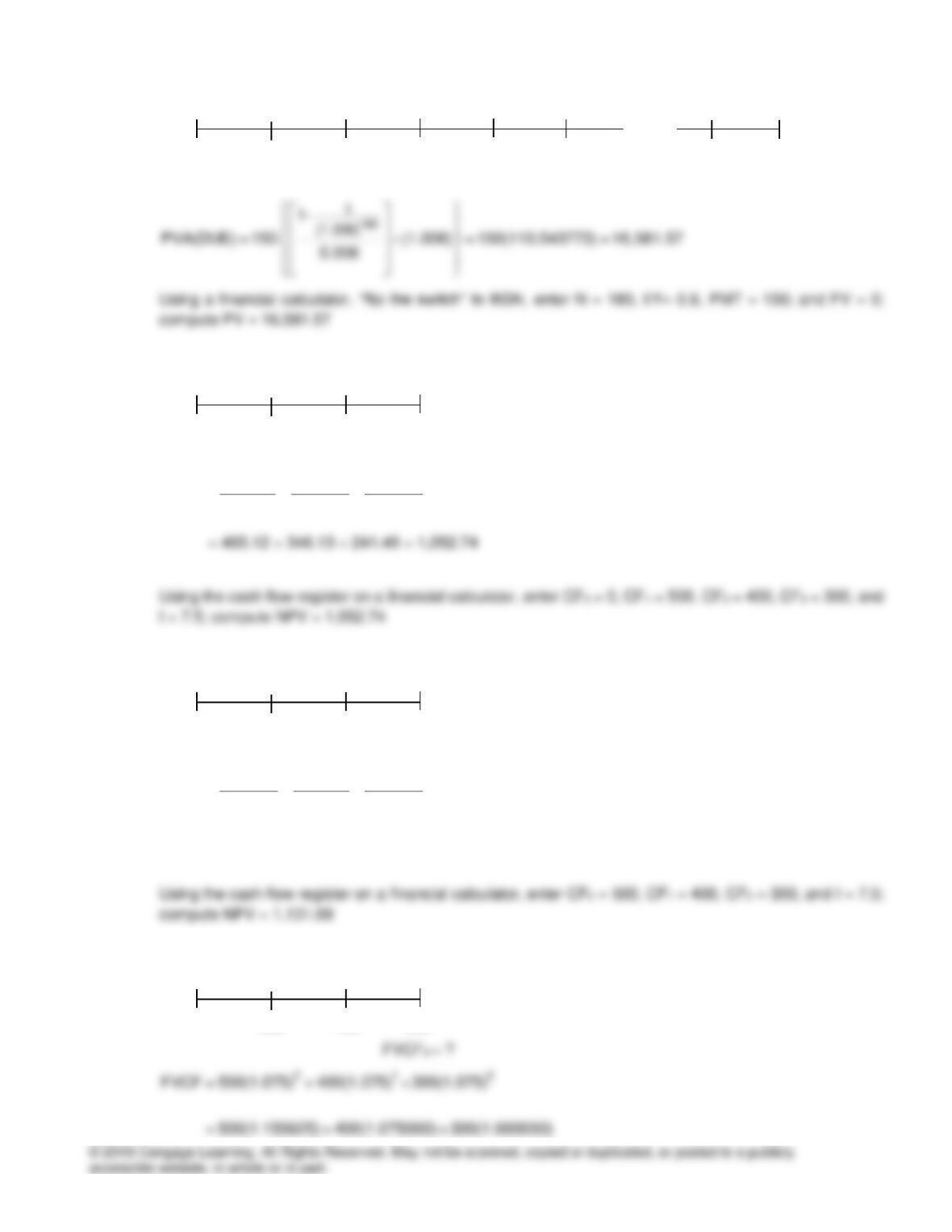

0 1 2 59 60

c.

PV = ? FV5 = 2,500

PV = $2,500/(1.0075)60 = $2,500(0.638700) = $1,596.75

Using a financial calculator, enter N = 5 x 12 = 60, I/Y= 9/12 = 0.75, PMT = 0, and FV = 2,500; compute

PV = -1,596.75

r = 9%

Interest payments

r = 0.75%

Interest payments

…

Chapter 4 CFIN6

r = 1%

…

0 1 2 3 4 5 6 7 8

4-9 a.

–385 –385 –385 –385 –385 –385 –385 –385

FVA8 = ?

8

(1.07) –1

FVA = 385 = 385(10.259803) = 3,950.02

0.07

Using a financial calculator, enter N = 8, I/Y= 7, PV = 0, and PMT = –385, compute FV = 3,950.02

0 1 2 3 4 5 13 14

4-10 a.

-450 –450 –450 –450 –450 –450 –450

FVA14 = ?

14

(1.08) –1

FVA = 450 = 450(24.214920) =10,896.71

0.08

Using a financial calculator, enter N = 14, I/Y= 8, PV = 0, and PMT = –450, compute FV = 10,896.71

r = 8%

…

r = 7%

r = 8%

…

Chapter 4 CFIN6

0 1 2 3 4 5 59 60

4-11 a.

–100 –100 –100 –100 –100 –100 –100

FVA = ?

60

(1.005) –1

FVA =100 =100(69.770031) = 6,977.00

0.005

Using a financial calculator, enter N = 5 x 12 = 60, I/Y= 6/12 = 0.5, PV = 0, and PMT = -100; compute FV

= 9,977

r = 0.5%

…

0 1 2 3 4 5 14 15

4-12 a.

PVA = ? 230 230 230 230 230 230 230

r = 11%

…

r = 11%

…

r = 0.5%

…

Chapter 4 CFIN6

0 1 2 3 4 5 107 108

4-13 a.

PVA = ? 450 450 450 450 450 450 450

108

1

(1.007)

1-

PVA = 450 = 450(75.602985) = 34,021.34

0.007

Using a financial calculator, enter N = 9 x 12 = 108, I/Y= 8.4/12 = 0.7, PMT = 450, and FV = 0; compute

PV = -34,021.34

r = 0.7%

…

0 1 2 3 4 5 179 180

4-14 a.

PVA = ? 150 150 150 150 150 150 150

r = 0.7%

…

r = 0.6%

…

Chapter 4 CFIN6

0 1 2 3 4 5 179 180

b.

150 150 150 150 150 150 150

PVA(DUE) = ?

0 1 2 3

4-15 a.

PVCF3 = ? 500 400 300

+

1 2 3

500 400 300

PVCF = + = 500(0.930233)+ 400(0.865333)+ 300(0.804961)

(1.075) (1.075) (1.075)

0 1 2 3

b.

500 400 300

+

0 1 2

500 400 300

PVCF = + = 500(1.000000)+ 400(0.930233)+ 300(0.865333)

(1.075) (1.075) (1.075)

= 500.00 + 372.09 + 259.60 = 1,131.69

0 1 2 3

4-16 a.

500 400 300

r = 0.6%

…

r = 7.5%

r = 7.5%

r = 7.5%

Chapter 4 CFIN6

0 1 2 3

b.

500 400 300

3 2 1

+FVCF = 500(1.075) + 400(1.075) 300(1.075)

0 1 2 3 4 5 -1

4-17 a.

PVP = ? 320 320 320 320 320 320 320

320

PVP = = 8,000.00

0.04

0 1 2 3 4 5 -1

b.

PVP = ? 320 320 320 320 320 320 320

r = 10%

r = 7.5%

r = 4%

…

r = 8%

…

Chapter 4 CFIN6

When more interest is earned during an investment period, less money must be invested today to

receive a particular amount in the future.

0 1 2 8 9 10

4-18

-1,250 3,550

Using a calculator, enter N = 10, PV = -1,250, PMT = 0, and FV = 3,550; compute I/Y= 11%.

4-19 0 1 2 n-1 n Months

12,000 -526 -526 -526 -526

Use either the trial-and-error

calculator to solve for n.

4-20 0 1 2 n-1 n Years

–2,260 4,750

n

n

FV PV(1 r)

4,750 2,260(1.07)

=+

=

r = ?

…

r = 0.4%

…

r = 7%%

…

Solve for n using logarithms,

the trial-and-error method, or

a financial calculator.

Chapter 4 CFIN6

Alternative solution (using logarithms):

n

n

4,750 2,260(1.07)

4,750

(1.07) 2.10177

2,260

=

==

4-21 rEAR = (1 + r/m)m – 1.0

CanAm: rEAR = [1 + (0.12/12)]12 – 1.0 = (1.01)12 – 1.0 = 0.1268 = 12.68%

4-22 a. APR = 6.0%

b. rEAR = [1 + (0.06/12)]12 – 1.0 = (1.005)12 – 1.0 = 0.0617 = 6.17%

4-23 a. 0 1 2 119 120 Months

PVA = 50,000 PMT PMT PMT PMT

b. After three years of payments, William is faced with the following cash flow timeline:

0 1 2 83 84 Months

PVA = ? 511 511 511 511

…

r = 0.35%

…

r = 0.35%

Chapter 4 CFIN6

184

(1.0035)

1

PVA 510.99 0.0035

−

=

4-24 a. 0 1 2 359 360 Months

PVA = 220,000 PMT PMT PMT PMT

b. Because it is 12 years after she bought the house, Sarah Jean has 216 = (30 – 12) x 12 payments

remaining and she is now faced with the following cash flow timeline:

0 1 2 215 216 Months

PVA = ? 1,319 1,319 1,319 1,319

This is an ordinary annuity because Sarah Jean made her most recent mortgage payment today,

which means her next payment is due in one month, not today.

4-25 a. 0 1 2 59 60 Months

PVA = 32,000 PMT PMT PMT PMT

…

r = 0.5%

…

r = 0.5%

…

r = 0.25%

Chapter 4 CFIN6

b. After making 24 payments, Nona would have 36 payments remaining and she would be faced with

the following cash flow timeline:

0 1 2 35 36 Months

PVA = ? 575 575 575 575

…

r = 0.25%