Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

CHAPTER 4

DISCOUNTED CASH FLOW VALUATION

Answers to Concepts Review and Critical Thinking Questions

2. Assuming positive cash flows and interest rates, the present value will fall and the future value will

rise.

4. Yes, they should. APRs generally don’t provide the relevant rate. The only advantage is that they are

easier to compute, but, with modern computing equipment, that advantage is not very important.

6. It’s a reflection of the time value of money. TMCC gets to use the $24,099 immediately. If TMCC

uses it wisely, it will be worth more than $100,000 in thirty years.

7. This will probably make the security less desirable. TMCC will only repurchase the security prior to

8. The key considerations would be: (1) Is the rate of return implicit in the offer attractive relative to

other, similar risk investments? and (2) How risky is the investment; i.e., how certain are we that we

will actually get the $100,000? Thus, our answer does depend on who is making the promise to repay.

10. The price would be higher because, as time passes, the price of the security will tend to rise toward

$100,000. This rise is a reflection of the time value of money. As time passes, the time until receipt of

the $100,000 grows shorter, and the present value rises. In 2019, the price will probably be higher for

CHAPTER 4 -

2

Solutions to Questions and Problems

NOTE: All-end-of chapter problems were solved using a spreadsheet. Many problems require multiple

steps. Due to space and readability constraints, when these intermediate steps are included in this solutions

manual, rounding may appear to have occurred. However, the final answer for each problem is found

without rounding during any step in the problem.

Basic

1. The time line for the cash flows is:

0

10

$600.60 × 10 = $6,006 in interest.

The total balance will be $7,800 + 6,006 = $13,806

2. To find the FV of a lump sum, we use:

FV = PV(1 + r)t

a.

0

10

3. To find the PV of a lump sum, we use:

PV = FV/(1 + r)t

0

6

PV

$13,827

4. To answer this question, we can use either the FV or the PV formula. Both will give the same answer

since they are the inverse of each other. We will use the FV formula, that is:

FV = PV(1 + r)t

Solving for r, we get:

CHAPTER 4 -

4

0

4

–$189

$287

FV = $287 = $189(1 + r)4; r = ($287/$189)1/4 – 1 = .1101, or 11.01%

5. To answer this question, we can use either the FV or the PV formula. Both will give the same answer

since they are the inverse of each other. We will use the FV formula, that is:

FV = PV(1 + r)t

Solving for t, we get:

6. To find the length of time for money to double, triple, etc., the present value and future value are

irrelevant as long as the future value is twice the present value for doubling, three times as large for

tripling, etc. To answer this question, we can use either the FV or the PV formula. Both will give the

same answer since they are the inverse of each other. We will use the FV formula, that is:

FV = PV(1 + r)t

Solving for t, we get:

t = ln(FV/PV)/ln(1 + r)

7. The time line is:

0

20

8. The time line is:

0

4

–$1,680,000

$1,100,000

To answer this question, we can use either the FV or the PV formula. Both will give the same answer

since they are the inverse of each other. We will use the FV formula, that is:

9. The time line is:

0

1

…

∞

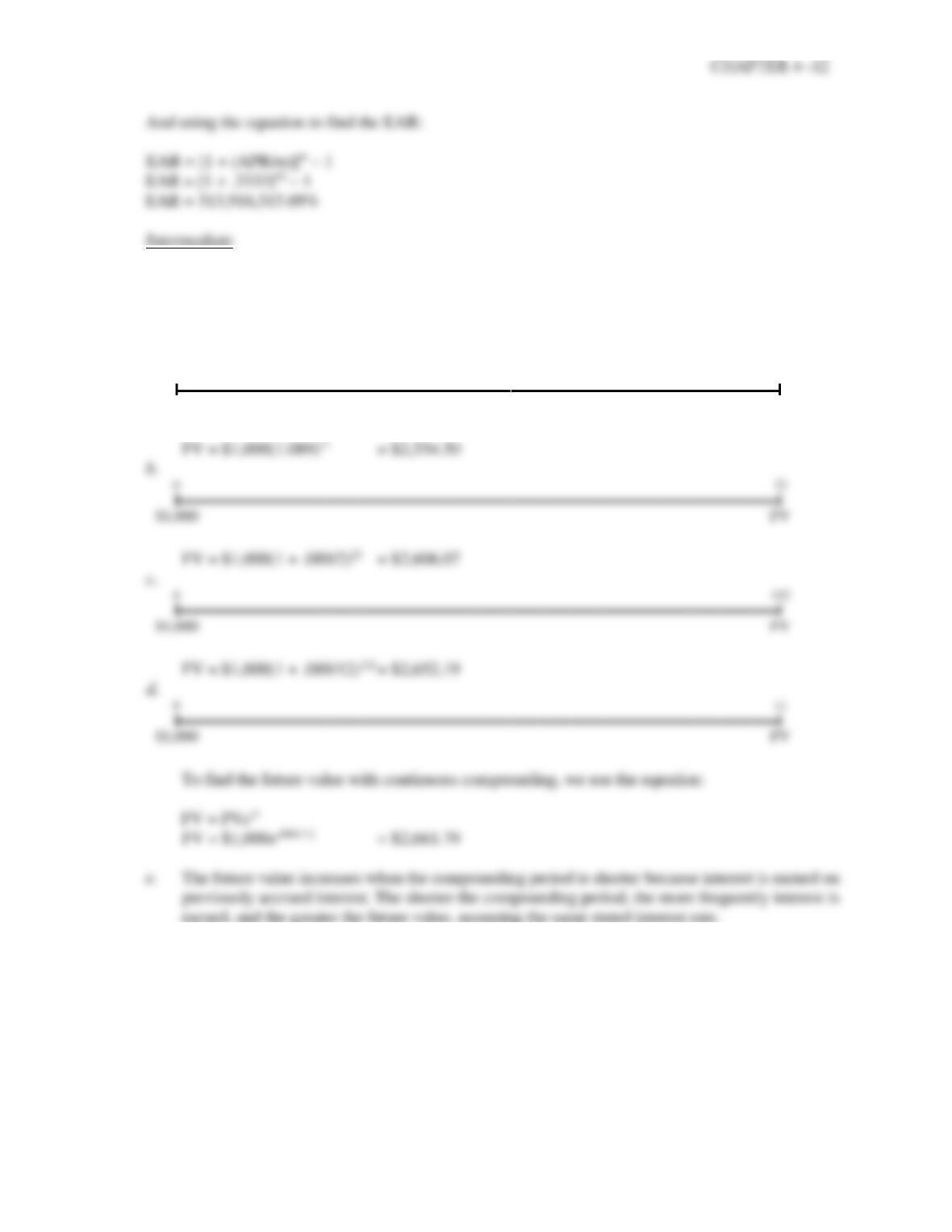

10. To find the future value with continuous compounding, we use the equation:

FV = PVert

a.

0

9

11. The time line is:

0

1

2

3

4

PV

$795

$945

$1,325

$1,860

12. The times lines are:

0

1

2

3

4

5

6

7

8

9

PV

$4,350

$4,350

$4,350

$4,350

$4,350

$4,350

$4,350

$4,350

$4,350

0

1

2

3

4

5

PV

$6,900

$6,900

$6,900

$6,900

$6,900

13. To find the PVA, we use the equation:

PVA = C({1 – [1/(1 + r)]t}/r)

0

1

…

15

PV

$5,200

$5,200

$5,200

$5,200

$5,200

$5,200

$5,200

$5,200

$5,200

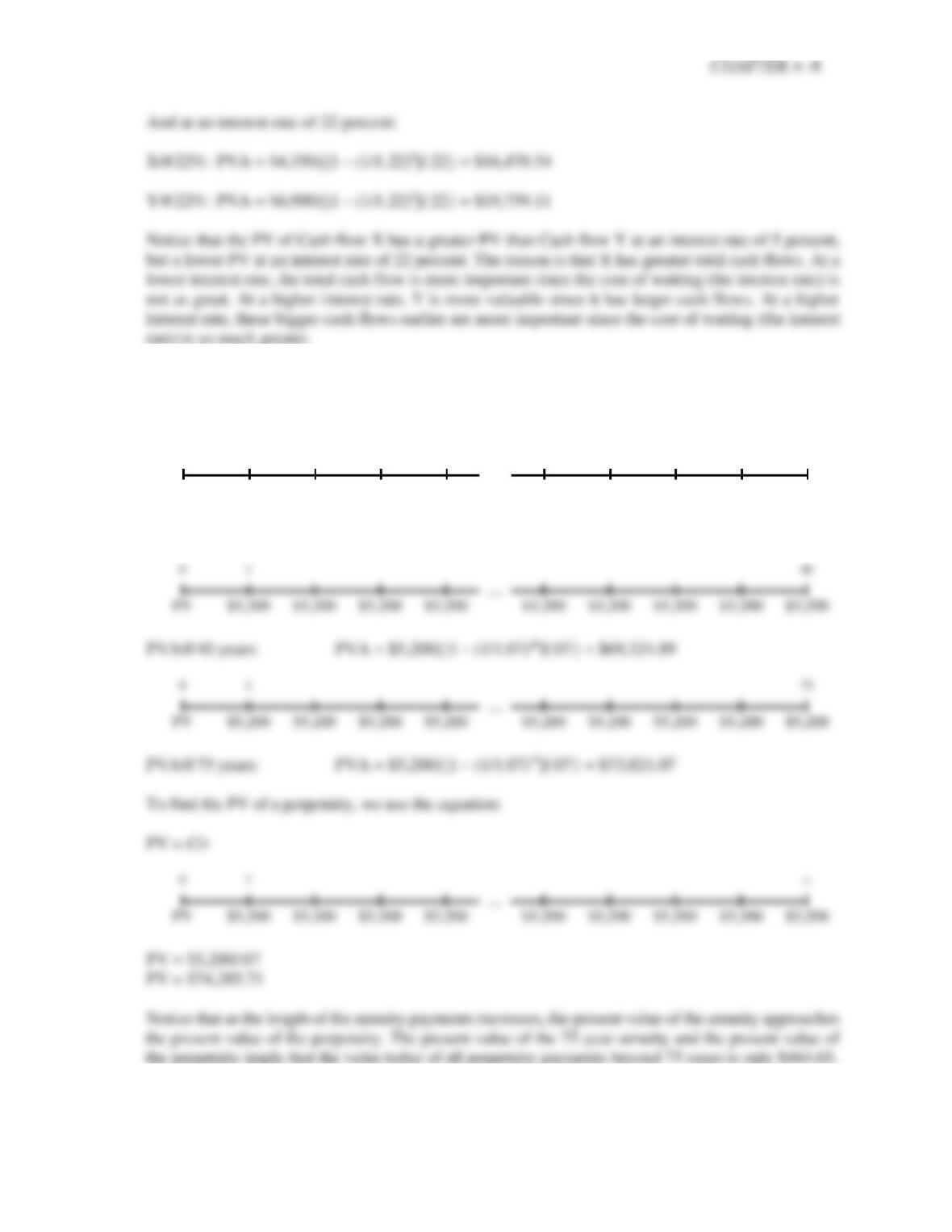

PVA@15 years: PVA = $5,200{[1 – (1/1.07)15]/.07} = $47,361.15

14. The time line is:

0

1

…

∞

PV

$15,000

$15,000

$15,000

$15,000

$15,000

$15,000

$15,000

$15,000

$15,000

This cash flow is a perpetuity. To find the PV of a perpetuity, we use the equation:

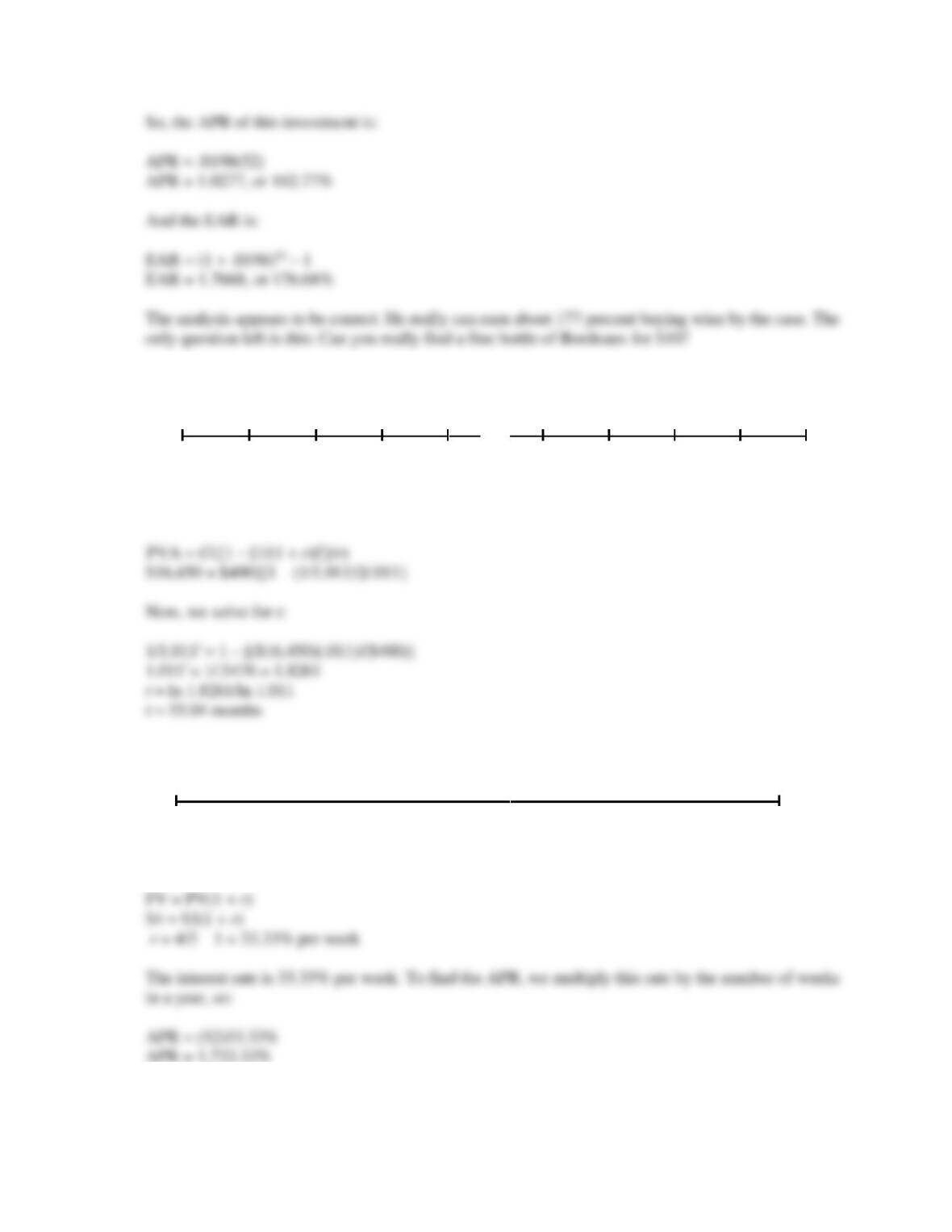

15. For discrete compounding, to find the EAR, we use the equation:

EAR = [1 + (APR/m)]m – 1

16. Here, we are given the EAR and need to find the APR. Using the equation for discrete

compounding:

EAR = [1 + (APR/m)]m – 1

We can now solve for the APR. Doing so, we get:

17. For discrete compounding, to find the EAR, we use the equation:

EAR = [1 + (APR/m)]m – 1

18. The cost of a case of wine is 10 percent less than the cost of 12 individual bottles, so the cost of a case

will be:

Cost of case = (12)($10)(1 – .10)

Cost of case = $108

CHAPTER 4 -

11

19. The time line is:

0

1

…

?

–$16,450

$400

$400

$400

$400

$400

$400

$400

$400

$400

Here, we need to find the length of an annuity. We know the interest rate, the PV, and the payments.

Using the PVA equation:

20. The time line is:

0

1

$3

$4

Here, we are trying to find the interest rate when we know the PV and FV. Using the FV equation:

21. To find the FV of a lump sum with discrete compounding, we use:

FV = PV(1 + r)t

a.

0

11

$1,000

FV

22. The total interest paid by First Simple Bank is the interest rate per period times the number of periods.

In other words, the interest paid by First Simple Bank over 10 years will be:

.053(10) = .53

CHAPTER 4 -

13

First Complex Bank pays compound interest, so the interest paid by this bank will be the FV factor of

$1, or:

23. Although the stock and bond accounts have different interest rates, we can draw one time line, but we

need to remember to apply different interest rates. The time line is:

0

1

...

360

361

…

660

Stock

$850

$850

$850

$850

$850

C

C

C

Bond

$350

$350

$350

$350

$350

We need to find the annuity payment in retirement. Our retirement savings end at the same time the

retirement withdrawals begin, so the PV of the retirement withdrawals will be the FV of the retirement

savings. So, we find the FV of the stock account and the FV of the bond account and add the two FVs.

24. The time line is:

0

4

–$1

$4

Since we are looking to quadruple our money, the PV and FV are irrelevant as long as the FV is four

times as large as the PV. The number of periods is four, the number of quarters per year. So:

25. Here, we need to find the interest rate for two possible investments. Each investment is a lump sum,

so:

G:

0

6

–$65,000

$125,000

H:

0

10

–$65,000

$205,000

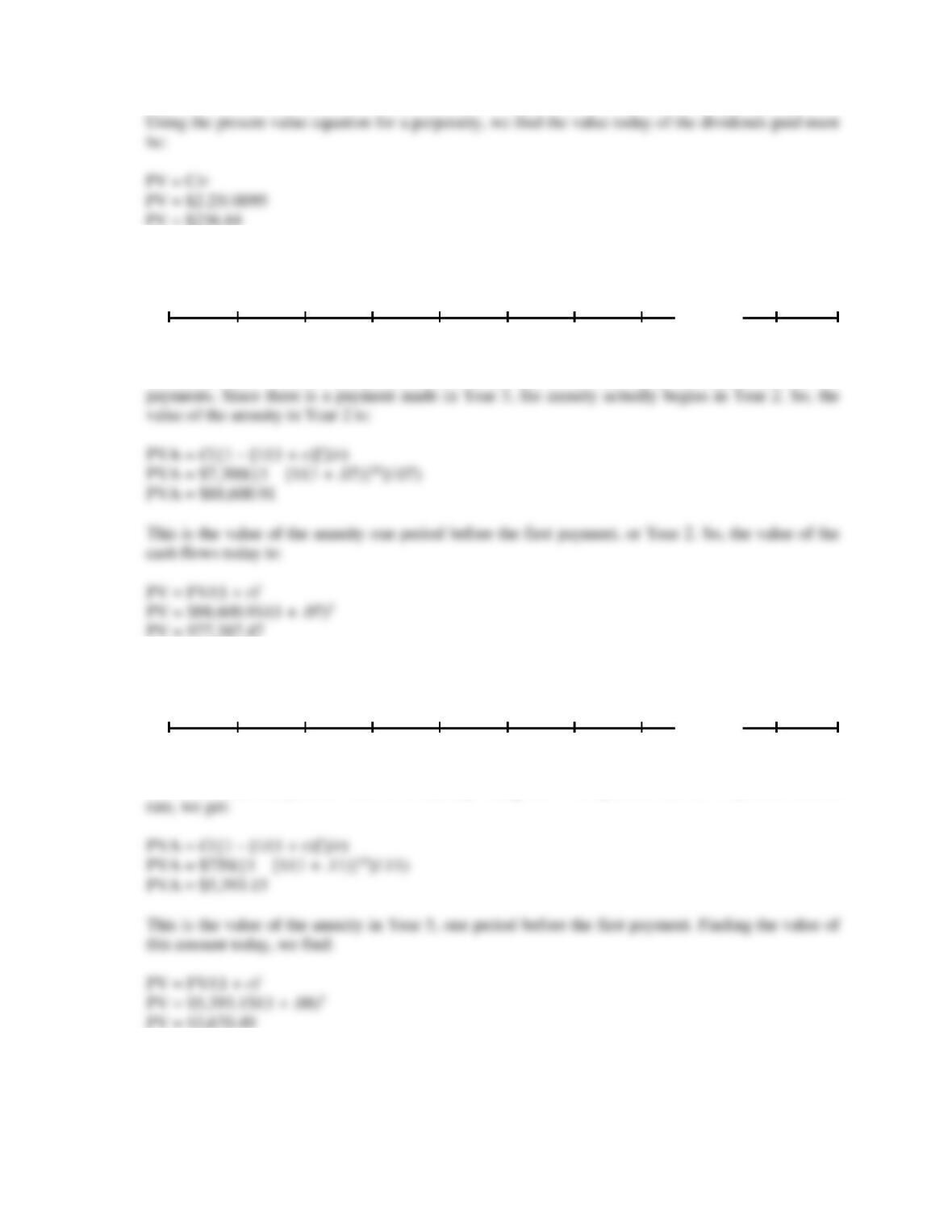

26. This is a growing perpetuity. The present value of a growing perpetuity is:

PV = C/(r – g)

27. The dividend payments are made quarterly, so we must use the quarterly interest rate. The quarterly

interest rate is:

The time line is:

0

1

…

∞

PV

$2.25

$2.25

$2.25

$2.25

$2.25

$2.25

$2.25

$2.25

$2.25

CHAPTER 4 -

15

28. The time line is:

0

1

2

3

4

5

6

7

…

30

PV

$7,300

$7,300

$7,300

$7,300

$7,300

$7,300

$7,300

We can use the PVA annuity equation to answer this question. The annuity has 28 payments, not 27

29. The time line is:

0

1

2

3

4

5

6

7

…

20

PV

$750

$750

$750

$750

We need to find the present value of an annuity. Using the PVA equation, and the 11 percent interest

30. The amount borrowed is the value of the home times one minus the down payment, or:

Amount borrowed = $725,000(1 – .20)

Amount borrowed = $580,000

The time line is:

31. The time line is:

0

12

$12,400

FV

32. The time line is:

0

1

…

∞

–$2,750,000

$273,000

$273,000

$273,000

$273,000

$273,000

$273,000

$273,000

$273,000

$273,000

33. The company will accept the project if the present value of the increased cash flows is greater than

the cost. The cash flows are a growing perpetuity, so the present value is:

34. Since your salary grows at 3.7 percent per year, your salary next year will be:

Next year’s salary = $74,500(1 + .037)

Next year’s salary = $77,256.50

This means your deposit next year will be:

35. The time line is:

0

1

…

20

PV

$4,700

$4,700

$4,700

$4,700

$4,700

$4,700

$4,700

$4,700

$4,700

36. The time line is:

0

1

…

?

–$40,000

$350

$350

$350

$350

$350

$350

$350

$350

$350

37. The time line is:

0

1

…

60

–$88,000

$1,725

$1,725

$1,725

$1,725

$1,725

$1,725

$1,725

$1,725

$1,725

Here, we are given the PVA, number of periods, and the amount of the annuity. We need to solve for

CHAPTER 4 -

19

38. The time line is:

0

1

…

360

PV

$1,025

$1,025

$1,025

$1,025

$1,025

$1,025

$1,025

$1,025

$1,025

The amount of principal paid on the loan is the PV of the monthly payments you make. So, the present

value of the $1,025 monthly payments is:

39. The time line is:

0

1

2

3

4

–$6,700

$1,400

?

$2,300

$2,700

We are given the total PV of all four cash flows. If we find the PV of the three cash flows we know, and

CHAPTER 4 -

20

40. The time line is:

0

1

2

3

4

5

6

7

8

9

10

$1M

$1.335M

$1.67M

$2.005M

$2.34M

$2.675M

$3.01M

$3.345M

$3.68M

$4.015M

$4.35M

41. Here, we are finding the interest rate for an annuity cash flow. We are given the PVA, number of

periods, and the amount of the annuity. We need to solve for the interest rate. We should also note that

the PV of the annuity is not the amount borrowed since we are making a down payment on the

warehouse. The amount borrowed is: