Mini Case: 3 – 15

Income Statements

2018

2019

2020E

Net sales

$5,500

$6,000

$6,600

Cost of goods sold (Excluding depr.)

4,300

4,800

5,210

Depreciation

290

320

370

Other operating expenses

350

420

400

(EBIT)

$ 560

$ 460

$ 620

Less interest

68

108

100

Pre-tax earnings

$ 492

$ 352

$ 520

Taxes (25%)

123

88

130

Net Income

$ 369

$ 264

$ 390

Note: “E” denotes the “estimated forecast.” Also, Computron has no amortization.

Other Data

2018

2019

2020E

Per Share Information

EPS

$3.69

$2.64

$3.90

DPS

$0.90

$0.84

$1.00

Book Value Per Share

$27.30

$29.10

$32.00

Additional Information

Dividends

$90

$84

$100

Additions to retained earnings

$180

$290

100

100

100

$50.00

$30.00

Lease payments

$20

$20

$20

Tax rate

Note: “E” denotes the “estimated forecast.”

Mini Case: 3 – 16

Ratio Analysis

2018

2019

2020E

Industry

Average

Profit margin

6.7%

4.4%

7.2%

Operating profit margin

10.2%

7.7%

10.4%

Basic earning power

13.7%

9.4%

15.6%

ROA

5.4%

10.8%

ROE

13.5%

9.1%

15.4%

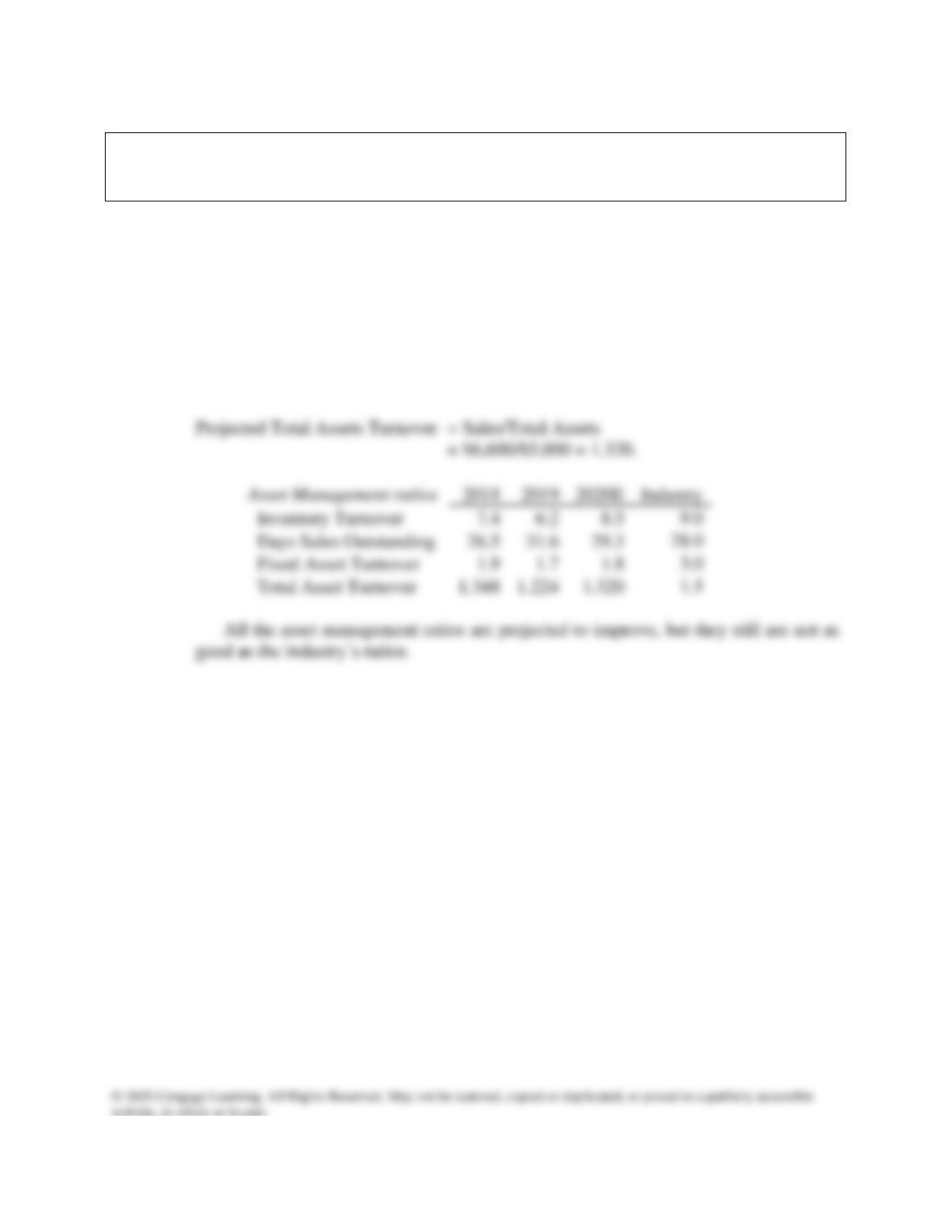

Inventory turnover

7.4

6.2

9.0

Days sales outstanding

26.5

31.6

28.0

Fixed assets turnover

1.9

1.7

3.0

Total assets turnover

1.5

Current

2.1

1.6

2.5

Quick

1.0

0.7

1.4

Debt ratio

20.8%

27.6%

15.0%

Debt-to-equity ratio

0.31

0.46

0.22

Liabilities-to-assets ratio

33.1%

40.6%

30.0%

Earnings multiplier

1.5

1.7

1.5

8.2

EBITDA coverage

9.9

6.3

17.2

Price/earnings (P/E)

13.6

11.4

16.8

Market/book

1.8

1.0

2.6

Note: “E” denotes the “estimated forecast.”

a. Why are ratios useful? What three groups use ratio analysis and for what reasons?

Answer: Ratios facilitate comparison of (1) one company over time and (2) one company versus

other companies. Ratios are used by managers to help improve the firm’s performance,

Mini Case: 3 – 17

b. Calculate the projected profit margin, operating profit margin, basic earning

power (BEP), return on assets (ROA), and return on equity (ROE). What can you

say about these ratios?

Answer: Projected Profit Margin = Net Income/Sales = $390/$6,600 = 5.9%.

Projected Operating Profit Margin = EBIT/Sales = $620/$6,600 = 9.4%.

Profitability Ratios

2018

2019

2020E

Industry

Average

Profit margin

6.7%

4.4%

5.9%

7.2%

Operating profit margin

10.2%

7.7%

9.4%

10.4%

Mini Case: 3 – 18

c. Calculate the projected inventory turnover, days sales outstanding (DSO), fixed

assets turnover, and total assets turnover. How does Computron’s utilization of

assets stack up against other firms in its industry?

Answer: Projected Inventory Turnover = COGS/Inventory

= ($5,210 + $370)/$700= 8.5.

Projected DSO = Receivables/(Sales/365)

= $530/($6,600/365) = 29.3 Days.

Projected Fixed Assets Turnover = Sales/Net Fixed Assets

= $6,600/$3,700 = 1.8.

Mini Case: 3 – 19

d. Calculate the projected current and quick ratios based on the projected balance

sheet and income statement data. What can you say about the company’s liquidity

position and its trend?

Answer: Projected Current Ratio = Current Assets/Current Liabilities

= $1,200/$700 = 1.9.

Mini Case: 3 – 20

e. Calculate the projected debt ratio, the debt-to-equity ratio, liabilities-to-assets

ratio, earnings multiplier, times-interest-earned, and EBITDA coverage ratios.

How does Computron compare with the industry with respect to financial

leverage? What can you conclude from these ratios?

Answer: Projected Debt Ratio = Total Debt/Total Assets

= ($100+ $1,100)/$5,000 = 24.0%.

Projected Debt-to-Equity Ratio = Total Debt/Common Equity

= ($100 + $1,100)/$3,200 = 0.38.

Proj. EBITDA Cov. =

+Payments

Lease

EBITDA

/

++ Payments

Lease

Repayments

Loan

Interest

= ($620 + $370 + $20)/($100 + $20) = 8.4.

Debt Management ratios

2018

2019

2020E

Industry

Debt Ratio

20.8%

27.6%

24.0%

15.0%

Debt-to-Equity Ratio

0.31

0.46

0.38

0.22

Liabilities-to-assets Ratio

33.1%

40.6%

36.0%

32.0%

Earnings Multiplier

Times Interest Earned

EBITDA Coverage Ratio

Mini Case: 3 – 21

f. Calculate the projected price/earnings ratio and market/book ratio. Do these

ratios indicate that investors are expected to have a high or low opinion of the

company?

Answer: EPS = Net Income/Shares Outstanding = $390/100 = $3.90.

Projected Price/Earnings = Price Per Share/Earnings Per Share

= $49.00/$3.90 = 12.6.

Market Value Ratios

2018

2019

2020E

Industry

Average

Earnings per share

$3.69

$2.64

$3.90

na

Price/earnings (P/E)

13.6

11.4

12.6

16.8

Book value per share

na

Market/book

Mini Case: 3 – 22

g. Perform a common size analysis and percent change analysis. What do these

analyses tell you about Computron?

Answer: For the common size balance sheets, divide all items in a year by the total assets for

that year. For the common size income statements, divide all items in a year by the

sales in that year.

Common Size Balance Sheets

Assets

2018

2019

2020E

Industry

Cash and equivalents

1.5%

1.0%

1.2%

1.5%

Short-term investments

2.5%

0.2%

1.0%

24.9%

Accounts receivable

9.8%

11.5%

Inventories

12.1%

Total Current Assets

50.0%

Net Fixed Assets

50.0%

Total Assets

100.0%

100.0%

Common Size Balance Sheets

Liabilities and equity

2018

2019

2020E

Industry

Accounts payable

7.4%

8.2%

6.6%

6.8%

Notes payable

1.2%

5.1%

2.0%

3.0%

Accruals

4.9%

4.9%

5.4%

10.2%

Total current liabilities

20.0%

Long-term bonds

Total liabilities

32.0%

Common

27.2%

Retained earnings

Total common equity

68.0%

Total liabilities and equity

Mini Case: 3 – 23

Common Size

Income Statements

2018

2019

2020E

Industry

Net sales

100.0%

100.0%

100.0%

100.0%

COGS except depr.

78.2%

80.0%

78.9%

69.0%

Depreciation

5.3%

5.3%

5.6%

3.3%

Other Expenses

6.4%

7.0%

6.1%

17.3%

EBIT

10.2%

7.7%

9.4%

10.4%

Less interest

1.2%

1.8%

1.5%

0.8%

Pre-tax earnings

8.9%

5.9%

7.9%

9.6%

Taxes (25%)

2.2%

1.5%

2.0%

2.4%

Net Income

6.7%

4.4%

5.9%

7.2%

Computron has higher proportion of net fixed assets than the industry.

Computron’s total debt is 24% (the combined percentages of notes payable and long-

term bonds) of its assets, which is higher than the industry’s combined debt

For the percent change analysis, divide all items in a row by the value in the first

year of the analysis.

Percentage Change

Income Statements

2018

2019

2020E

Net sales

0%

9.1%

20.0%

Costs of Goods Sold

0%

11.6%

21.2%

Depreciation

0%

10.3%

27.6%

Other Expenses

0%

20.0%

14.3%

EBIT

0%

10.7%

Less interest

0%

58.8%

47.1%

Pre-tax earnings

0%

Taxes (25%)

0%

Net Income

0%

Percent Change

Balance Sheets

Assets

2018

2019

2020E

Cash and equivalents

0%

-16.7%

0.0%

Short-term investments

0%

-90.0%

-50.0%

Accounts receivable

0%

30.0%

32.5%

Inventories

0%

32.3%

6.5%

Total Current Assets

0%

18.6%

10.2%

Net Fixed Assets

0%

20.7%

27.6%

Total Assets

0%

20.1%

22.5%

Mini Case: 3 – 25

Percent Change Balance

Sheets

Liabilities and equity

2018

2019

2020E

Accounts payable

0%

33.3%

10.0%

Notes payable

0%

400.0%

100.0%

Accruals

0%

20.0%

35.0%

Total current liabilities

0%

61.8%

27.3%

Long-term bonds

0%

37.5%

37.5%

Total liabilities

0%

47.4%

33.3%

Common stock

0%

Retained earnings

0%

10.4%

27.2%

Total common equity

0%

17.2%

Total liabilities and equity

0%

20.1%

22.5%

We see that in the most recent year, total assets grew by 20.1% relative to the

baseline (with inventory growing by 32.3%). However, actual sales only grew by

9.1%, which indicates trouble, with unsold inventory causing much of the problem.

Other expenses also grew rapidly, causing a steep decline in net income (-28.5%).

Part of this decline is due to the 58.8% increase in interest expense.

Mini Case: 3 – 26

h. Use the extended DuPont equation to provide a breakdown of Computron’s

projected return on equity. How does the projection compare with the previous

years and with the industry’s DuPont equation?

Answer: DuPont Equation:

ROE =

Profit

Margin

Total Assets

Turnover

Equity

Multiplier

ROE2018 = (6.7%)(1.348)(1.495) = 13.5%

ROE2019 = (4.4%)(1.224)(1.684) = 9.1%

Computron’s profit margin and total assets turnover ratio were below the industry

average. It had a higher equity multiplier because it had more debt, which boosted its

ROE. Otherwise, its ROE would have been even lower than the industry ROE.

i. What are some potential problems and limitations of financial ratio analysis?

Answer: Some potential problems are listed below:

Mini Case: 3 – 27

1. Comparison with industry averages is difficult if the firm operates many different

divisions.

2. Different operating and accounting practices distort comparisons.

3. Sometimes hard to tell if a ratio is “good” or “bad.”

j. What are some qualitative factors analysts should consider when evaluating a

company’s likely future financial performance?

Answer: Top analysts recognize that certain qualitative factors must be considered when

evaluating a company. These factors, as summarized by the American Association Of

Individual Investors (AAII), are as follows:

1. Are the company’s revenues tied to one key customer?

2. To what extent are the company’s revenues tied to one key product?

3. To what extent does the company rely on a single supplier?