Answers and Solutions: 3 – 1

Chapter 3

Analysis of Financial Statements

ANSWERS TO END-OF-CHAPTER QUESTIONS

3-1 a. A liquidity ratio is a ratio that shows the relationship of a firm’s cash and other current

assets to its current liabilities. The current ratio is found by dividing current assets by

current liabilities. It indicates the extent to which current liabilities are covered by those

assets expected to be converted to cash in the near future. The quick, or acid test, ratio

is found by taking current assets less inventories and then dividing by current liabilities.

assets, it measures the percentage of assets financed by debtholders. The debt-to-equity

ratio is the total debt divided by the total common equity. The times-interest-earned

ratio is determined by dividing earnings before interest and taxes by the interest

charges. This ratio measures the extent to which operating income can decline before

the firm is unable to meet its annual interest costs. The EBITDA coverage ratio is

similar to the times-interest-earned ratio, but it recognizes that many firms lease assets

and also must make sinking fund payments. It is found by adding EBITDA and lease

payments then dividing this total by interest charges, lease payments, and sinking fund

payments over one minus the tax rate.

Answers and Solutions: 3 – 2

e. Market value ratios relate the firm’s stock price to its earnings and book value per share.

The price/earnings ratio is calculated by dividing price per share by earnings per share–

-this shows how much investors are willing to pay per dollar of reported profits. The

price/free cash flow is calculated by dividing price per share by free cash flow per

share. This shows how much investors are willing to pay per dollar of free cash flow.

Market-to-book ratio is simply the market price per share divided by the book value

per share. Book value per share is common equity divided by the number of shares

outstanding.

3-2 The emphasis of the various types of analysts is by no means uniform nor should it be.

Management is interested in all types of ratios for two reasons. First, the ratios point out

weaknesses that should be strengthened; second, management recognizes that the other

parties are interested in all the ratios and that financial appearances must be kept up if the

firm is to be regarded highly by creditors and equity investors. Equity investors are

interested primarily in profitability, but they examine the other ratios to get information on

the riskiness of equity commitments. Long-term creditors are more interested in the debt

ratio, TIE, and fixed-charge coverage ratios, as well as the profitability ratios. Short-term

creditors emphasize liquidity and look most carefully at the liquidity ratios.

Answers and Solutions: 3 – 3

3-4 Differences in the amounts of assets necessary to generate a dollar of sales cause asset

turnover ratios to vary among industries. For example, a steel company needs a greater

3-5 a. Cash, receivables, and inventories, as well as current liabilities, vary over the year for

firms with seasonal sales patterns. Therefore, those ratios that examine balance sheet

figures will vary unless averages (monthly ones are best) are used.

3-6 Firms within the same industry may employ different accounting techniques, which make

it difficult to compare financial ratios. More fundamentally, comparisons may be

misleading if firms in the same industry differ in their other investments. For example,

comparing PepsiCo and Coca-Cola may be misleading because apart from their soft drink

business, Pepsi also owns other businesses such as Frito-Lay, Pizza Hut, Taco Bell, and

KFC.

Answers and Solutions: 3 – 4

SOLUTIONS TO END-OF-CHAPTER PROBLEMS

3-1 DSO = 20 days; ADS = $20,000; AR = ?

3-2 TA = $200 million, notes payable =$5 million, and LT debt = $25 million.

3-3 TA = $10,000,000,000; CL = $1,000,000,000; LT debt = $3,000,000,000; CE =

$6,000,000,000; Shares outstanding = 800,000,000; P0 = $75; M/B = ?

3-4 Earnings per share = $1.50; FCF per share = $3.00; P/FCF = 8.0; P/E = ?

P/FCF = 8.0

P/$3.00 = 8.0

P = $24.00.

Answers and Solutions: 3 – 5

3-6 ROA = 12%; PM = 5%; ROE = 20%; S/TA = ?; A/E = ?

ROA = NI/A; PM = NI/S; ROE = NI/E

3-7 CA = $3,000,000;

CL

CA

= 1.5;

CL

I – CA

= 1.0;

CL = ?; I = ?

1.5 =

CL

$3,000,000

1.5 =

CL

CA

3-8 We are given ROA = 4%, ROE = 7%, and TAT = Sales/Total assets = 1.2.

From DuPont equation: ROA = Profit margin Total assets turnover

4% = Profit margin (1.2)

Profit margin = 4%/1.2 = 3.33%.

Answers and Solutions: 3 – 7

3-9 Present current ratio =

$525,000

$1,312,500

= 2.5.

Minimum current ratio =

NP + $525,000

NP + $1,312,500

= 2.0.

3-10 TIE = EBIT/Interest expense, so find EBIT and Interest expense.

Interest = $600,000 0.08 = $48,000.

Net income = $3,000,000 0.03 = $90,000.

Pre-tax income = $90,000/(1 – T) = $90,000/0.75 = $120,000.

Answers and Solutions: 3 – 8

3-11 1. Sales = (1.5)(Total assets) = (1.5)($400,000) = $600,000.

2. Cost of goods sold = (Sales)(1 – 0.25) = ($600,000)(0.75)

= $450,000.

8. Common stock =Total liabilities

and equity – TL – Retained earnings

= $400,000 – $160,000 – $100,000 = $140,000.

Answers and Solutions: 3 – 9

3-12 1. Current assets

Current liabilities = 3.0

sliabilitieCurrent

$810,000

= 3.0

Current liabilities = $810,000/3 = $270,000.

2. Current assets − Inventories

Current liabilities = 1.4

$270,000

sInventorie – $810,000

= 1.4

Answers and Solutions: 3 – 10

3-13 a. (Dollar amounts in thousands.)

Industry

Firm Average

Current assets

Current liabilities =

$2,925,000

$1, 225, 000

= 2.39 2.0

000,375,6$

Sales

Fixed assets

=

000,350,1$

000,500,7$

= 5.56 12.1

Sales

Total assets

=

000,275,4$

000,500,7$

= 1.754 3.0

Sales

incomeNet

=

$114,000

$7,500,000

= 1.52% 1.2%

incomeNet

Answers and Solutions: 3 – 11

b. For the firm,

Equity multiplier (EM) =

$4, 275, 000

$2,650,000

= 1.61%.

ROE = PM T.A. turnover EM = 1.52% 1.754 1.61 = 4.3%.

For the industry, ROE = 1.2% 3 2.5 = 9%.

Answers and Solutions: 3 – 12

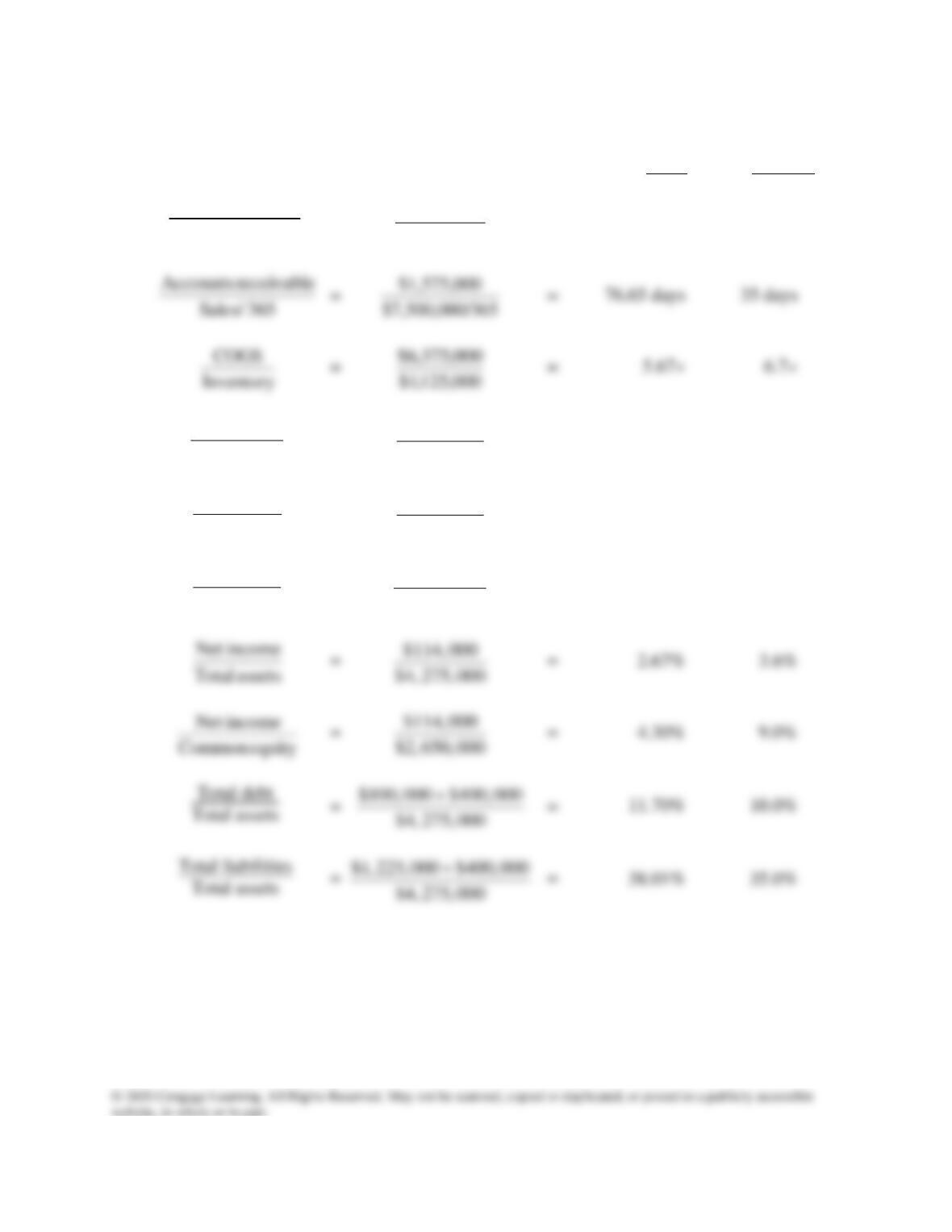

3-14 Here are the firm’s base case ratios and other data as compared to the industry:

Firm Industry Comment

Quick $511,000/$602,000 = 0.85 1.0 Weak

Current $1,405,000/$602,000 = 2.33 2.7 Weak

Inventory turnover $3,580,000/$894,000 = 4.00 7.0 Poor

Days sales outstanding $439,000/$11,753 = 37.35 days 32 days Poor

The firm appears to be badly managed—all of its ratios are worse than the industry averages,

and the result is low earnings, a low P/E, P/CF ratio, a low stock price, and a low M/B

ratio. The company needs to do something to improve.

Answers and Solutions: 3 – 13

SOLUTION TO SPREADSHEET PROBLEM

3-15 The detailed solution for the problem is available is in the file Ch03 P15 Build a Model

Solution.xlsx and is available at the textbook’s web site.

Mini Case: 3 – 14

MINI CASE

The first part of the case, presented in Chapter 2, discussed the situation of Computron

Industries after an expansion program. A large loss occurred in 2019, rather than the

expected profit. As a result, its managers, directors, and investors are concerned about the

firm’s survival.

shown next.

Balance Sheets

2018

2019

2020E

Assets

Cash and equivalents

$ 60

$ 50

$ 60

Short-term investments

100

10

50

Accounts receivable

400

520

530

Inventories

620

820

660

Total current assets

$1,180

$1,400

$1,300

Net Fixed Assets

2,900

3,500

3,700

Total Assets

$4,080

$4,900

$5,000

Liabilities and equity

Accounts payable

$ 300

$ 400

$ 330

Notes payable

50

250

100

Accruals

200

240

270

Total current liabilities

$ 550

$ 890

$ 700

Long-term bonds

800

1,100

1,100

Total liabilities

$1,350

$1,990

$1,800

Common stock (100,000

shares)

1,000

1,000

1,000

Retained earnings

1,730

1,910

2,200

Total common equity

$2,730

$2,910

$3,200

Total liabilities and equity

$4,080

$4,900

$5,000

Note: “E” denotes the “estimated forecast.”