1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

23

24

25

26

27

28

29

30

31

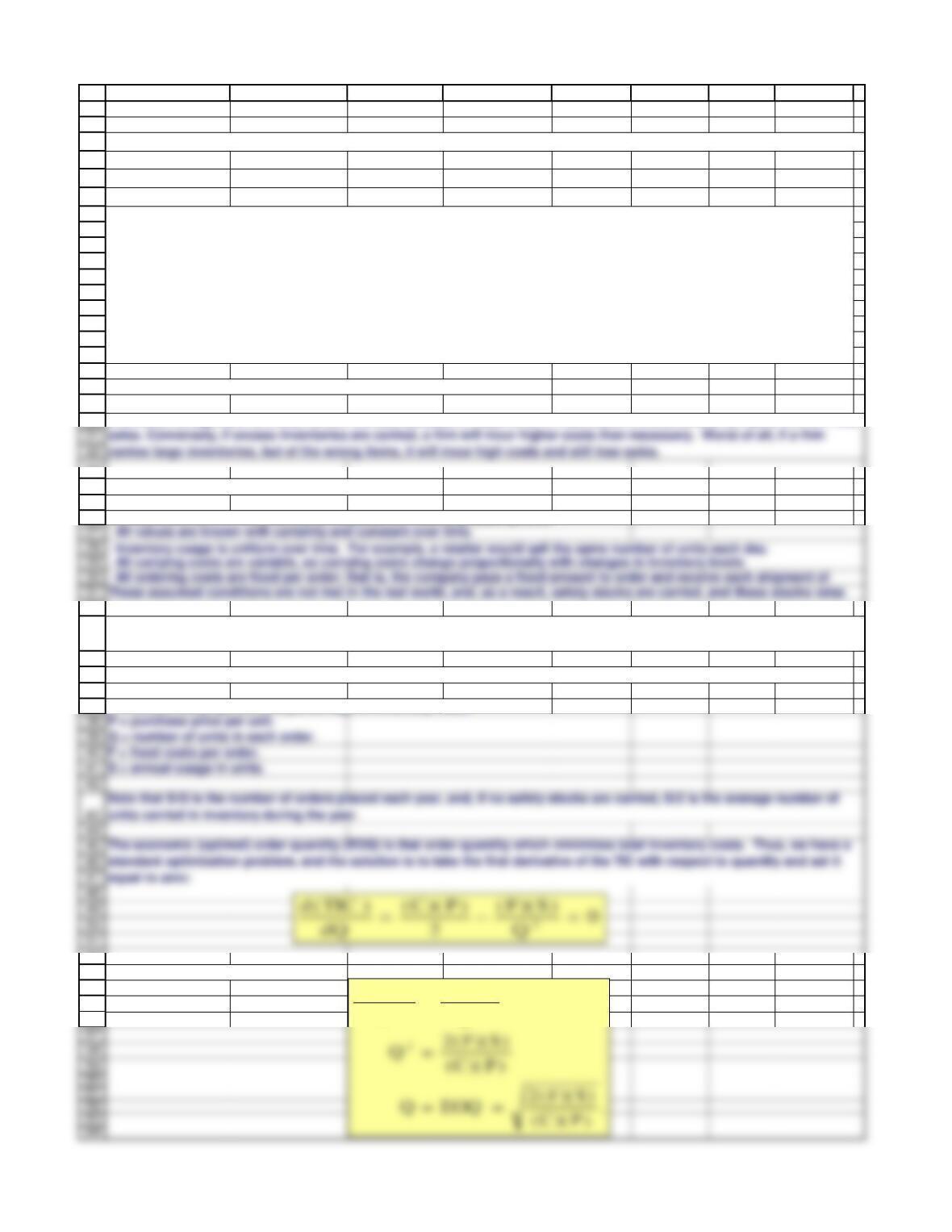

· All values are known with certainty and constant over time.

· All carrying costs are variable, so carrying costs change proportionally with changes in inventory levels

These assumed conditions are not met in the real world, and, as a result, safety stocks are carried, and these stocks raise

· All ordering costs are fixed per order; that is, the company pays a fixed amount to order and receive each shipment of

32

33

34

35

36

37

38

39

40

41

42

44

45

46

47

48

49

50

51

P = purchase price per unit.

Q = number of units in each order.

F = fixed costs per order.

S = annual usage in units.

units carried in inventory during the year.

The economic (optimal) order quantity (EOQ) is that order quantity which minimizes total inventory costs. Thus, we have a

equal to zero:

52

53

54

55

56

57

58

59

60

61

62

63

64

A B C D E F G H I

11/23/2018

C = annual carrying cost as a percentage of inventory value.

Solving for Q gives us:

Chapter 28. Mini Case for Advanced Issues in Cash Management and Inventory Control

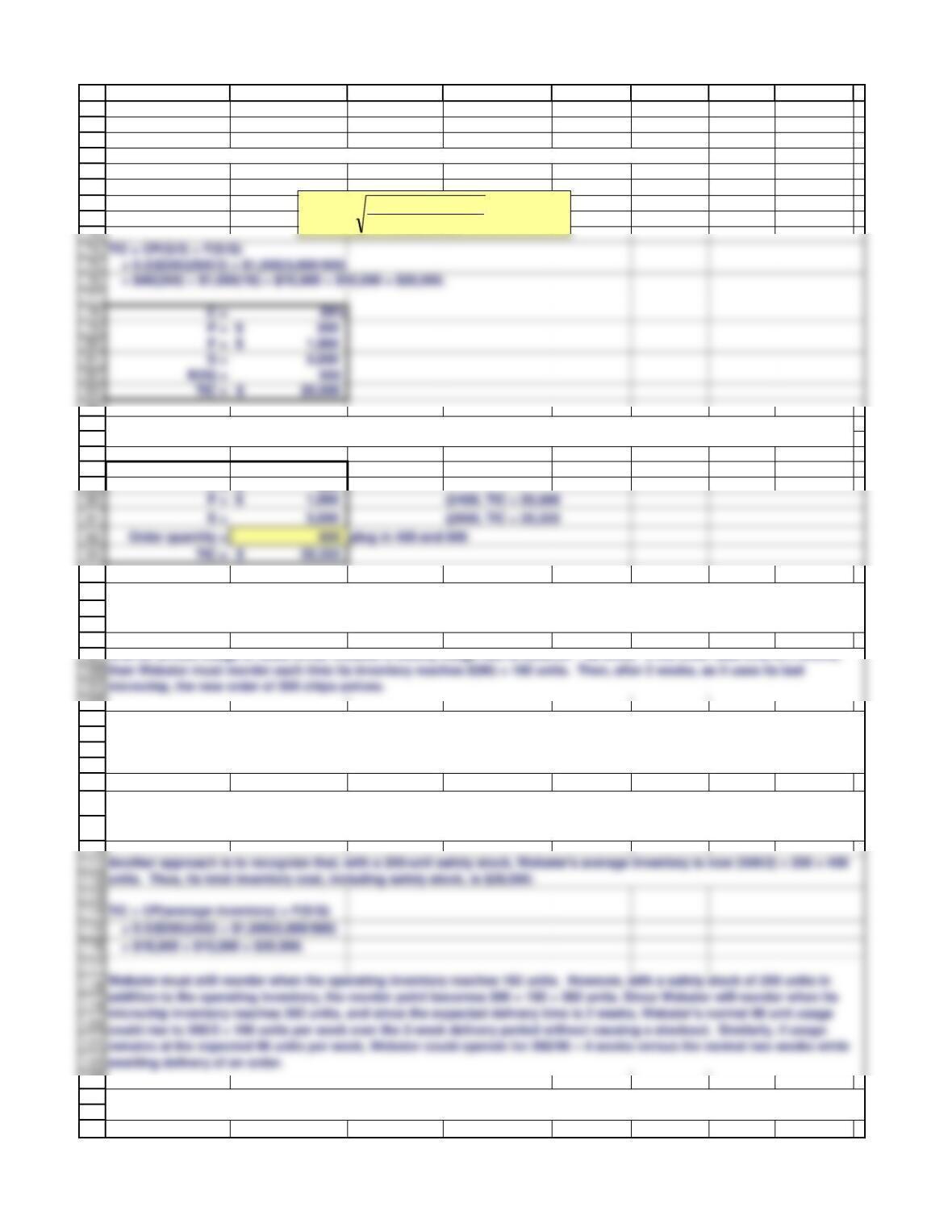

Andria Mullins, financial manager of Webster Eelectronics, has been asked by the firm’s CEO, Fred Weygandt, to evaluate

the company’s inventory control techniques and to lead a discussion of the subject with the senior executives. Andria

plans to use as an example one of Webster’s “big ticket” items, a customized computer microchip which the firm uses in

its laptop computer. Each chip costs Webster $200, and in addition it must pay its supplier a $1,000 setup fee on each

order. Further, the minimum order size is 250 units; Webster’s annual usage forecast is 5,000 units; and the annual

carrying cost of this item is estimated to be 20 percent of the average inventory value.

Andria plans to begin her session with the senior executives by reviewing some basic inventory concepts, after which

she will apply the EOQ model to Webster’s microchip inventory. As her assistant, you have been asked to help her by

answering the following questions:

a. Why is inventory management vital to the health of most firms?

b. What assumptions underlie the EOQ Model?

The standard form of the EOQ model requires the following assumptions:

TIC = total carrying costs + total ordering costs = CP(Q/2) + F(S/Q)

Inventory management is critical to the financial success of most firms. If insufficient inventories are carried, a firm will lose

c. Write out the formula for the total costs of carrying and ordering inventory, and then use the formula to derive the EOQ

model.

Q

)S)(F(

2

)P)(C(

2

=

21

22

carries large inventories, but of the wrong items, it will incur high costs and still lose sales.

65

66

67

68

69

70

71

72

84

85

86

87

88

89

90

94

95

96

97

98

99

100

101

then Webster must reorder each time its inventory reaches 2(96) = 192 units. Then, after 2 weeks, as it uses its last

microchip, the new order of 500 chips arrives.

102

103

104

105

106

107

108

109

110

111

112

113

114

115

116

117

could rise to 392/2 = 196 units per week over the 2-week delivery period without causing a stockout. Similarly, if usage

remains at the expected 96 units per week, Webster could operate for 392/96 » 4 weeks versus the normal two weeks while

awaiting delivery of an order.

Another approach is to recognize that, with a 200-unit safety stock, Webster’s average inventory is now (500/2) + 200 = 450

units. Thus, its total inventory cost, including safety stock, is $28,000:

123

124

125

126

A B C D E F G H I

C = 20%

P = $ 200

With an annual usage of 5,000 units, Webster’s weekly usage rate is 5,000/52 ~ 96 units. If the order lead time is 2 weeks,

g. Of course, there is uncertainty in Webster’s usage rate as well as in delivery times, so the company must carry a safety

stock to avoid running out of chips and having to halt production. If a 200-unit safety stock is carried, what effect would

this have on total inventory costs? What is the new reorder point? What protection does the safety stock provide if usage

increases, or if delivery is delayed?

d. What is the EOQ for custom microchips? What are total inventory costs if the EOQ is ordered?

f. Suppose it takes 2 weeks for Webster’s supplier to set up production, make and test the chips, and deliver them to

Webster’s plant. Assuming certainty in delivery times and usage, at what inventory level should Webster reorder? (assume

a 52-week year, and assume that Webster orders the EOQ amount.

e. What is Webster’s added cost if it orders 400 units at a time rather than the EOQ quantity? What if it orders 600 per

order?

There are two ways to view the impact of safety stocks on total inventory costs. Webster’s total cost of carrying the

operating inventory is $20,000 (see part d). Now the cost of carrying an additional 200 units is CP(safety stock) =

0.2($200)(200) = $8,000. Thus, total inventory costs are increased by $8,000, for a total of $20,000 + $8,000 = $28,000.

h. Now suppose Webster’s supplier offers a discount of 1 percent on orders of 1,000 or more. Should Webster take the

discount? Why or why not?

units500

)200($2.0

)000,5)(000,1($2

EOQ ==

73

74

75

76

77

78

79

80

81

82

83

C = 20%

P = $ 200

S = 5,000

127

128

129

130

131

135

136

137

138

139

140

141

142

143

144

145

146

147

148

149

150

151

152

153

154

155

156

157

158

159

160

161

(2.) The use of air freight for deliveries.

Air freight would presumably shorten delivery times and reduce the need for safety stocks. It might or might not affect the

Just-in-time procedures are designed specifically to reduce inventories. If a just in time system were put in place, it would

largely obviate the need for using the EOQ model.

(1.) The use of just-in-time procedures.

162

163

164

165

166

167

168

Computerized control systems would, generally, enable the company to keep better track of its existing inventory. This

would probably reduce safety stocks, and it might or might not affect the EOQ.

169

170

171

172

173

174

176

177

This reduces inventory holdings of final goods.

178

179

180

181

182

183

184

185

186

187

188

189

Total cash needs per year 1,200,000.00

EOQ = Optimal cash transfer 33,123

Number of times to liquidate per year 36.2

Number of weeks between liquidations 1.435

A B C D E F G H I

Monthly cash deficit (cash needs) 100,000.00

Opportunity cost for cash 7%

Brokerage costs for each transaction 32

(4.) The manufacturing plant is redesigned and automated. Computerized process equipment and state-of-the-art

robotics are installed, making the plant highly flexible in the sense that the company can switch from the production of

one item to another at a minimum cost and quite quickly. This makes short production runs more feasible than under the

old plant setup.

(3.) The use of a computerized inventory control system, wherein as units were removed from stock, an electronic

system automatically reduced the inventory account and, when the order point was hit, automatically sent an electronic

message to the supplier placing an order. The electronic system ensures that inventory records are accurate, and that

orders are placed promptly.

Applying this to cash management:

Note that we have reduced the unit price by the amount of the discount. Since total costs are $24,800 if Webster orders

1,000 chips at a time, the incremental annual cost of taking the discount is $24,800 – $20,000 = $4,800. However, Webster

would save 1 percent on each chip, for a total annual savings of 0.01($200)(5,000) = $10,000. Thus, the net effect is that

Webster would save $10,000 – $4,800 = $5,200 if it takes the discount, and hence it should do so.

First, note that since the discount will only affect the orders for the operating inventory, the discount decision need not take

account of the safety stock. Webster’s current total cost of its operating inventory is $20,000 (see part d). If Webster

increases its order quantity to 1,000 units, then its total costs for the operating inventory would be $24,800:

i. For many firms, inventory usage is not uniform throughout the year, but, rather, follows some seasonal pattern. Can the

EOQ model be used in this situation? If so, how?

The EOQ model can still be used if there are seasonal variations in usage, but it must be applied to shorter periods during

which usage is approximately constant. For example, assume that the usage rate is constant, but different, during the

summer and winter periods. The EOQ model could be applied separately, using the appropriate annual usage rate, to each

period, and during the transitional fall and spring seasons inventories would be either run down or built up with special

seasonal orders.

j. How would these factors affect an EOQ analysis?

132

133

134

190

191

192

193

A B C D E F G H I

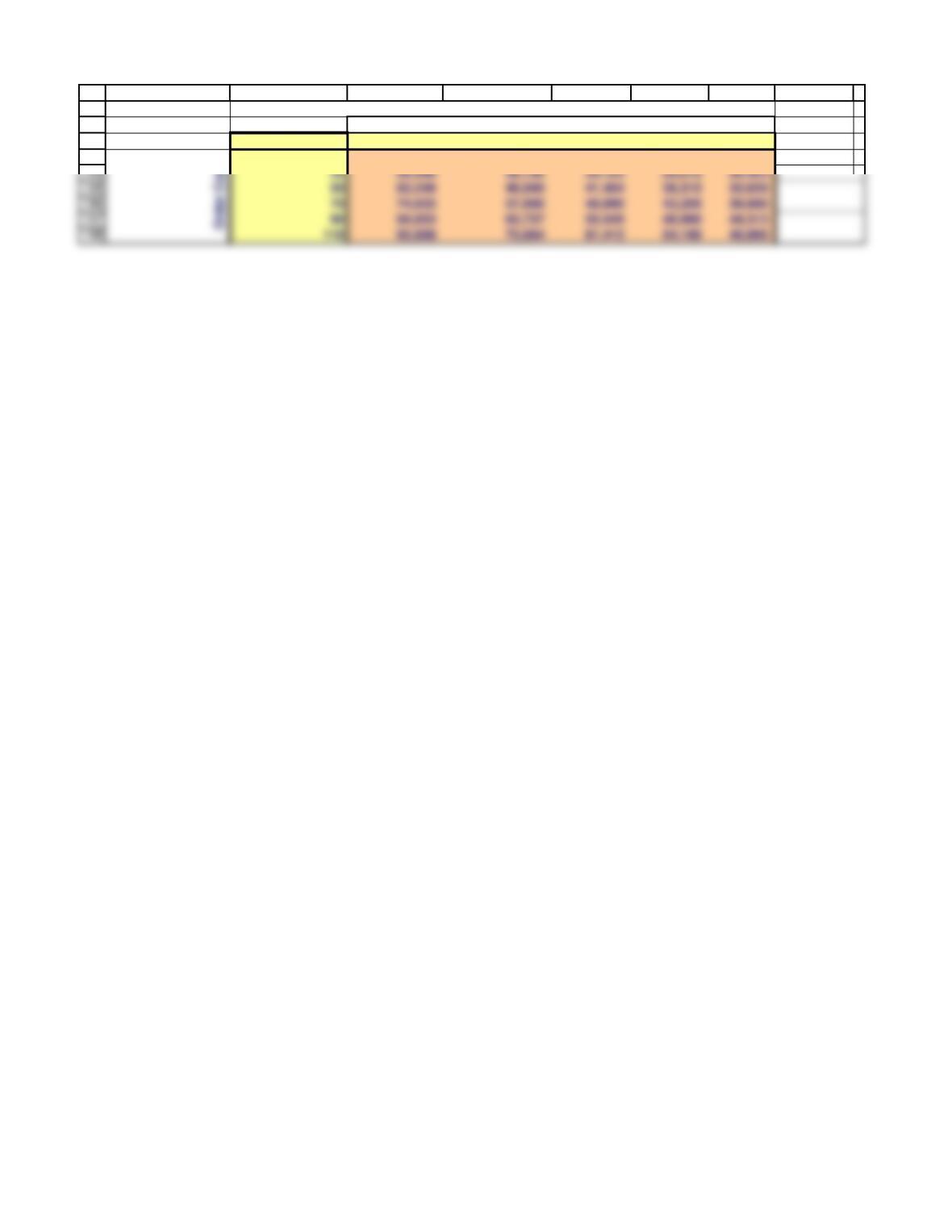

33,123 3% 5% 7% 9% 11%

10 28,284 21,909 18,516 16,330 14,771

Carrying Cost

Optimal cash transfer size for various order costs and carrying costs

194

195

196

197

198

32 50,596 39,192 33,123 29,212 26,423

50 63,246 48,990 41,404 36,515 33,029

70 74,833 57,966 48,990 43,205 39,080

90 84,853 65,727 55,549 48,990 44,313