1

2

3

4

5

6

7

8

9

10

11

12

17

18

19

20

21

22

23

24

25

27

28

Compared to a 30-day credit period, this isn’t too bad since one would expect some customers to pay slowly.

DSO = 0.3(10) + 0.5(40) + 0.2(70) = 37 DAYS

29

30

31

32

33

34

35

36

(AR) = (DSO)(ADS) =

37

38

39

40

41

42

43

44

45

46

47

48

49

50

52

53

54

55

5. If loans have a cost of 12 percent, what is the annual dollar cost of carrying the receivables?

Also there is the opportunity cost of not having use of the profit component of the receivables.

A B C D E F G H I

11/23/2018

JAN $100

FEB 200

a. Discuss, in general, what it means for the brothers to set a collections policy. Answer: See Ch. 27 Mini Case Show.

AVERAGE DAILY SALES = ADS = 18,000 (100)/365 = 4,931.51$ per day

AR Financed = 0.75 x $ 182,466 = 136,849.32

Accounts Receivable

182,466 Notes Payable 136,849

Chapter 27. Mini Case for Providing and Obtaining Credit

Rich Jackson, a recent finance graduate, is planning to go into the wholesale building supply business with his brother, Jim, who

majored in building construction. The firm would sell primarily to general contractors, and it would start operating next January. Sales

would be slow during the cold months, rise during the spring, and then fall off again in the summer, when new construction in the area

slows. Sales estimates for the first 6 months are as follows (in thousands of dollars):

The terms of sale are net 30, but because of special incentives, the brothers expect 30 percent of the customers (by dollar value) to pay

on the 10th day following the sale, 50 percent to pay on the 40th day, and the remaining 20 percent to pay on the 70th day. No bad debt

losses are expected, because Jim, the building construction expert, knows which contractors are having financial problems.

b. Assume that, on average, the brothers expect annual sales of 18,000 items at an average price of $100 per item. (use a 365 day year.)

What is the firm’s expected days sales outstanding (DSO)?

(2.) What is its expected average daily sales (ADS)?

the firm’s credit policy. The DSO depends mainly on credit policy, although poor economic conditions can lead to a

reduction in customers’ ability to make payments.

(4.) Assume that the firm’s profit margin is 25 percent. How much of the receivables balance must be financed? What would the firm’s

balance sheet figures for accounts receivable, notes payable, and retained earnings be at the end of one year if notes payable are used

to finance the investment in receivables? Assume that the cost of carrying receivables had been deducted when the 25 percent profit

margin was calculated.

(3.) What is its expected average accounts receivable (AR) level?

Since 25% of the sales price is profit, only 75% of the AR must be financed:

56

57

58

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

measure of customers’ payment performance. The underlying cause of the problem with the DSO is the seasonal

variability in sales. If there were no seasonal pattern, and hence sales were a constant $200 each month, then the DSO

would be 27 days in both march and June, indicating that customers’ payment patterns had remained steady.

See above in question (D) for average daily sales and DSO at the end of the quarter.

89

90

91

92

93

94

95

96

97

98

100

101

102

103

104

105

106

107

108

109

110

111

A B C D E F G H I

Month (1)

Credit Sales

for Month (2)

Receivables

at End of

Month

ADS (4) DSO (5)

January $100 $70

Age of Account

(Days) AR %AR %

Monthly

Sales

Contribution

to AR

AR to Sales

Ratio

f. Construct aging schedules for the end of March and the end of June. Do these schedules properly measure

customers‘ payment patterns? If not, why not?

AR = 0.7(SALES IN THAT MONTH) + 0.2(SALES IN PREVIOUS MONTH).

Quarterly Statement

e. What is the firm’s forecasted average daily sales for the first 3 months? For the entire half-year? The days sales

outstanding is commonly used to measure receivables performance. What DSO is expected at the end of March? At

the end of June? What does the DSO indicate about customers’ payments? Is DSO a good management tool in this

situation? If not, why not?

g. Construct the uncollected balances schedules for the end of March and the end of June. Do these schedules

properly measure customers’ payment patterns?

March

June

March

Note that the end of June ageing schedule suggests that customers are paying more slowly than in the earlier quarter.

However we know that the payment pattern has remained constant, so the firm’s customers’ payment performance has

not changed. The apparent change is due to the seasonal fluctuations.

(1) Receivables are a function of the average daily sales and the days sales outstanding. Exogenous economic

factors such as the state of the economy and competition within the industry affect average daily sales, but so does

the firm’s credit policy. The DSO depends mainly on credit policy, although poor economic conditions can lead to a

reduction in customers’ ability to make payments.

59

62

(2) For a given level of receivables, the lower the profit margin, the higher the cost of carrying receivables, because

the greater the portion of each sales dollar that must actually be financed. Similarly, the higher the cost of financing,

the higher the dollar cost of carrying receivables.

predicted, what would the receivables level be at the end of each month? To reduce calculations, assume that 30

percent of the firm’s customers pay in the month of sale, 50 percent pay in the second month following the sale, and

the remaining 20 percent pay in the second month following the sale. Note that this is a different assumption than was

made earlier.

112

113

114

115

122

123

124

125

126

127

128

129

130

131

132

133

134

135

136

137

138

139

140

141

March $500 $350 70%

$410 90%

Quarter 2:

April $400 $0 0%

May $300 $60 20%

June $200 $140 70%

$200 90%

142

143

144

145

146

147

148

149

150

151

152

153

154

155

156

157

158

159

160

161

162

163

164

165

166

167

168

169

170

171

A B C D E F G H I

February $200 $40 20%

March $300 $210 70%

$250 90%

Predicted

Sales

Predicted

Contribution

to AR

Predicted AR to

Sales Ratio

Quarter 1:

January $150 $0 0%

February $300 $60 20%

The brothers are now considering a change in the firm’s credit policy. The change would entail (1) changing the

credit terms to 2/10, net 20, (2) employing stricter credit standards before granting credit, and (3) enforcing collections

with greater vigor than in the past. Thus, cash customers and those paying within 10 days would receive a 2 percent

discount, but all others would have to pay the full amount after only 20 days. The brothers believe that the discount

would both attract additional customers and encourage some existing customers to buy more from the firm–after all,

the discount amounts to a price reduction. Of course, these customers would take the discount and, hence, would

pay in only 10 days.

h. Assume that it is now July of Year 1, and the brothers are developing pro forma financial statements for the

following year. Further, assume that sales and collections in the first half-year matched the predicted levels. Using

the year 2 sales forecasts as shown next, what are next year’s pro forma receivables levels for the end of march and

March

i. Assume now that it is several years later. The brothers are concerned about the firm’s current credit terms, which

are now net 30, which means that contractors buying building products from the firm are not offered a discount, and

they are supposed to pay the full amount in 30 days. Gross sales are now running $1,000,000 a year, and 80 percent

(by dollar volume) of the firms paying customers generally pay the full amount on day 30, while the other 20 percent

pay, on average, on day 40. Two percent of the firm’s gross sales end up as bad debt losses.

get the discount. Of course, these benefits are offset to some degree by the dollar cost of the discounts themselves.

116

117

118

119

120

121

Quarter 2:

April $300 $0 0%

May $200 $40 20%

June $100 $70 70%

$110 90%

172

173

174

175

182

183

184

185

186

187

188

Thus, the new credit policy is expected to cut the DSO in half.

189

190

191

192

193

194

195

196

197

198

199

200

201

202

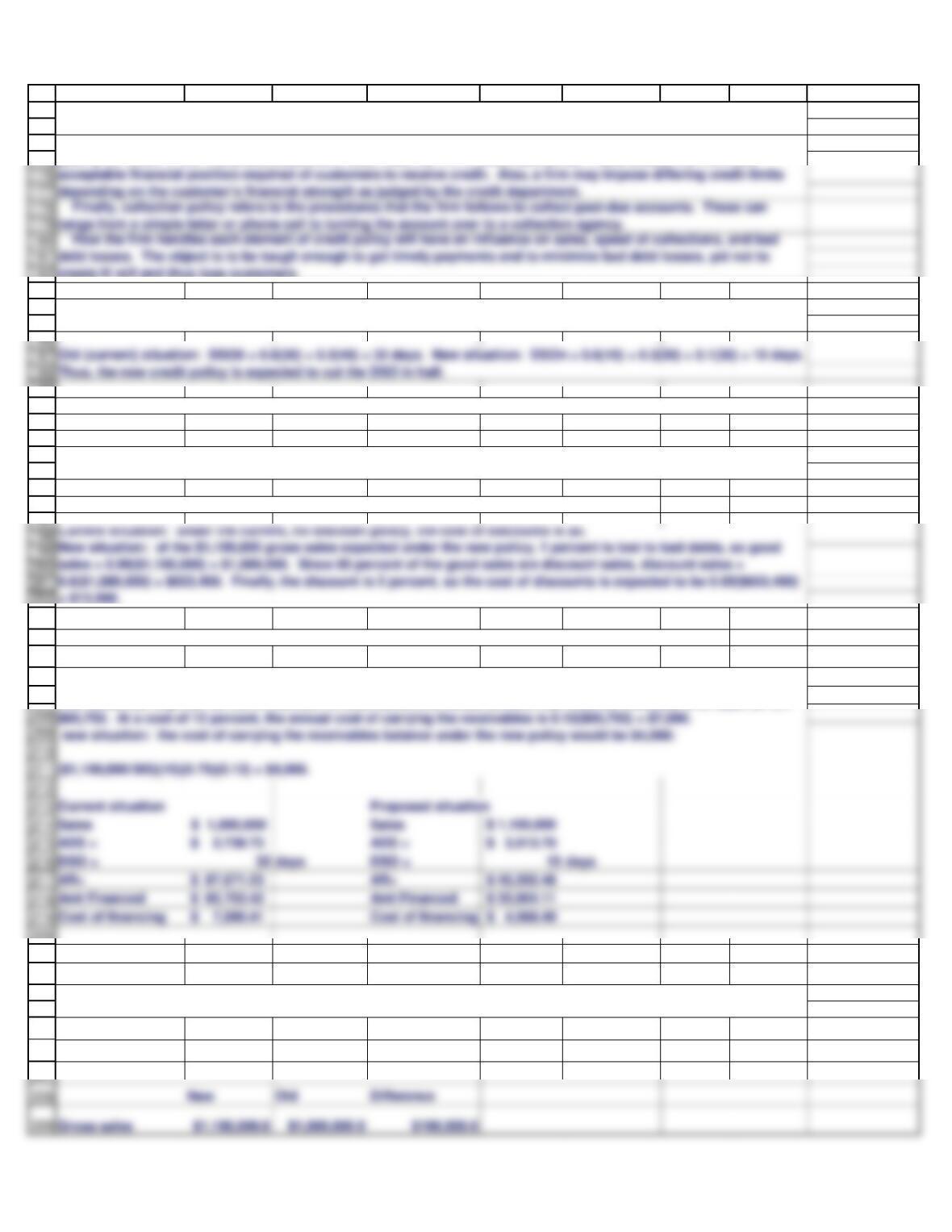

Current situation: under the current, no discount policy, the cost of discounts is $0.

New situation: of the $1,100,000 gross sales expected under the new policy, 1 percent is lost to bad debts, so good

sales = 0.99($1,100,000) = $1,089,000. Since 60 percent of the good sales are discount sales, discount sales =

= $13,068.

203

204

$65,753. At a cost of 12 percent, the annual cost of carrying the receivables is 0.12($65,753) = $7,890.

new situation: the cost of carrying the receivables balance under the new policy would be $4,068:

($1,100,000/365)(15)(0.75)(0.12) = $4,068.

205

206

207

220

221

222

223

224

229

225

226

227

A B C D E F G H I

Tax rate = 25%

create ill will and thus lose customers.

n. What is the incremental after-tax profit associated with the change in credit terms? Should the company make the

change? (assume a tax rate of 25 percent.)

Current situation: the firm’s average daily sales currently amount to $1,000,000/365 = $2,739.73. The DSO is 32 days,

so accounts receivable amount to 32($2,73973) = $87,671. However, only 75 percent of this total represents cash costs-

-the remainder is profit–so the investment in receivables (the actual amount that must be financed) is 0.75($87,671) =

m. What is the firm’s current dollar cost of carrying receivables? What would it be after the proposed change?

j. Under the current credit policy, what is the firm’s days sales outstanding (DSO)? What would the expected DSO be

if the credit policy change were made?

l. What would be the firm’s expected dollar cost of granting discounts under the new policy?

Old (current) situation: BDLo = 0.02($1,000,000) = $20,000. New situation: BDLn = 0.01($1,100,000) = $11,000. Thus, the

new policy is expected to cut bad debt losses sharply.

k. What is the dollar amount of the firm’s current bad debt losses? What losses would be expected under the new

Cash discounts generally produce two benefits: (1) they attract both new customers and expanded sales from

current customers, because people view discounts as a price reduction, and (2) discounts cause a reduction in the

days sales outstanding, since both new customers and some established customers will pay more promptly in order to

get the discount. Of course, these benefits are offset to some degree by the dollar cost of the discounts themselves.

The credit period is the length of time allowed to all “qualified” customers to pay for their purchases. In order to

qualify for credit in the first place, customers must meet the firm’s credit standards. These dictate the minimum

176

177

178

179

180

181

range from a simple letter or phone call to turning the account over to a collection agency.

How the firm handles each element of credit policy will have an influence on sales, speed of collections, and bad

depending on the customer’s financial strength as judged by the credit department.

230

231

232

233

240

241

242

243

244

245

246

247

248

249

250

251

252

253

254

255

256

257

258

259

260

261

262

263

264

266

267

268

269

270

271

273

274

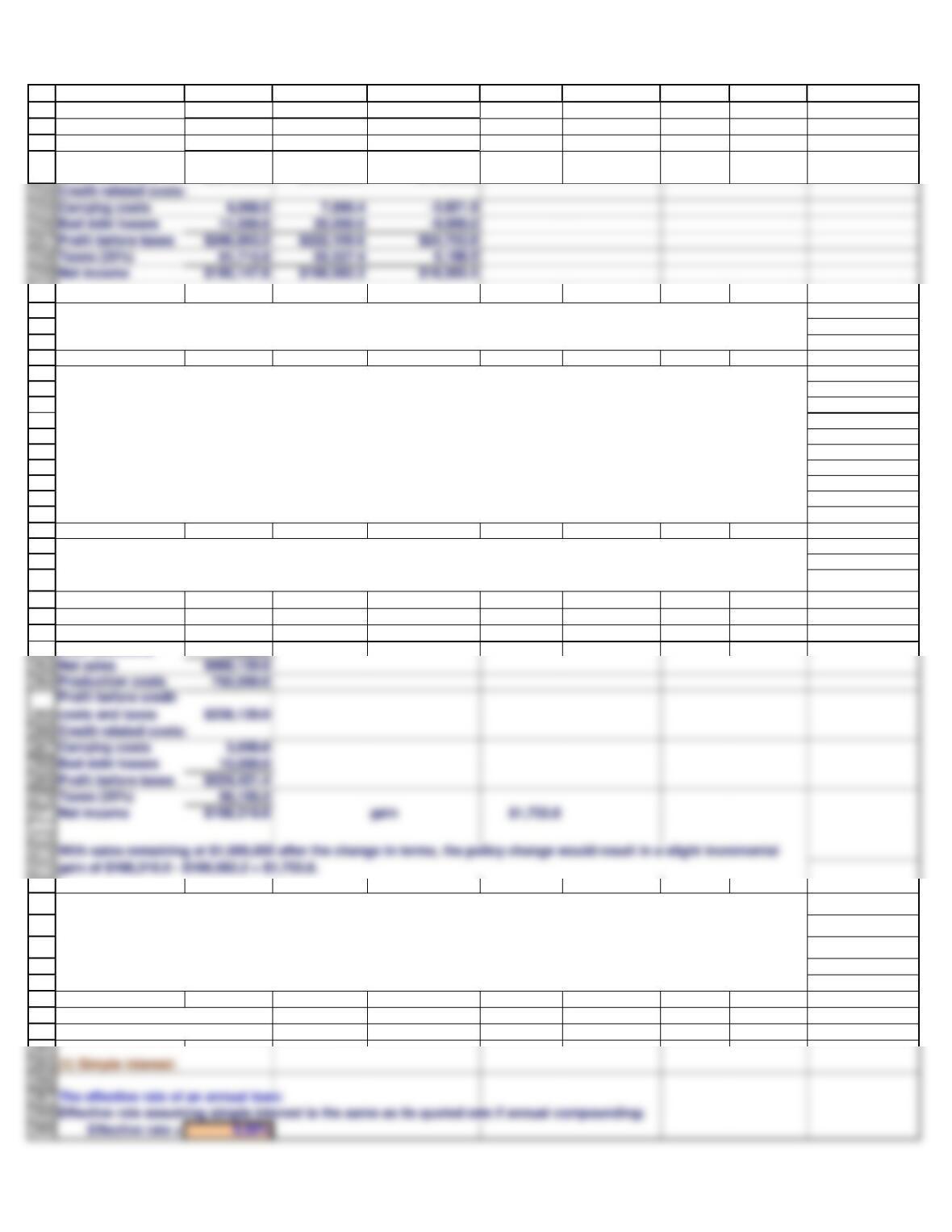

Net sales $988,120.0

Production costs 750,000.0

Profit before credit

costs and taxes

Credit-related costs:

Carrying costs 3,698.6

Bad debt losses 10,000.0

Profit before taxes $224,421.4

Taxes (25%) 56,105.3

Net income $168,316.0 gain $1,733.8

With sales remaining at $1,000,000 after the change in terms, the policy change would result in a slight incremental

gain of $168,316.0 – $166,582.2 = $1,733.8.

275

276

277

278

279

280

281

282

283

284

285

286

287

A B C D E F G H I

Less discounts 13,068.0 0.0 13,068.0

Net sales $1,086,932.0 $1,000,000.0 $86,932.0

Production costs 825,000.0 750,000.0 75,000.0

Profit before credit

costs and taxes

$261,932.0 $250,000.0 $11,932.0

New

Gross sales $1,000,000.0

Less discounts 11,880.0

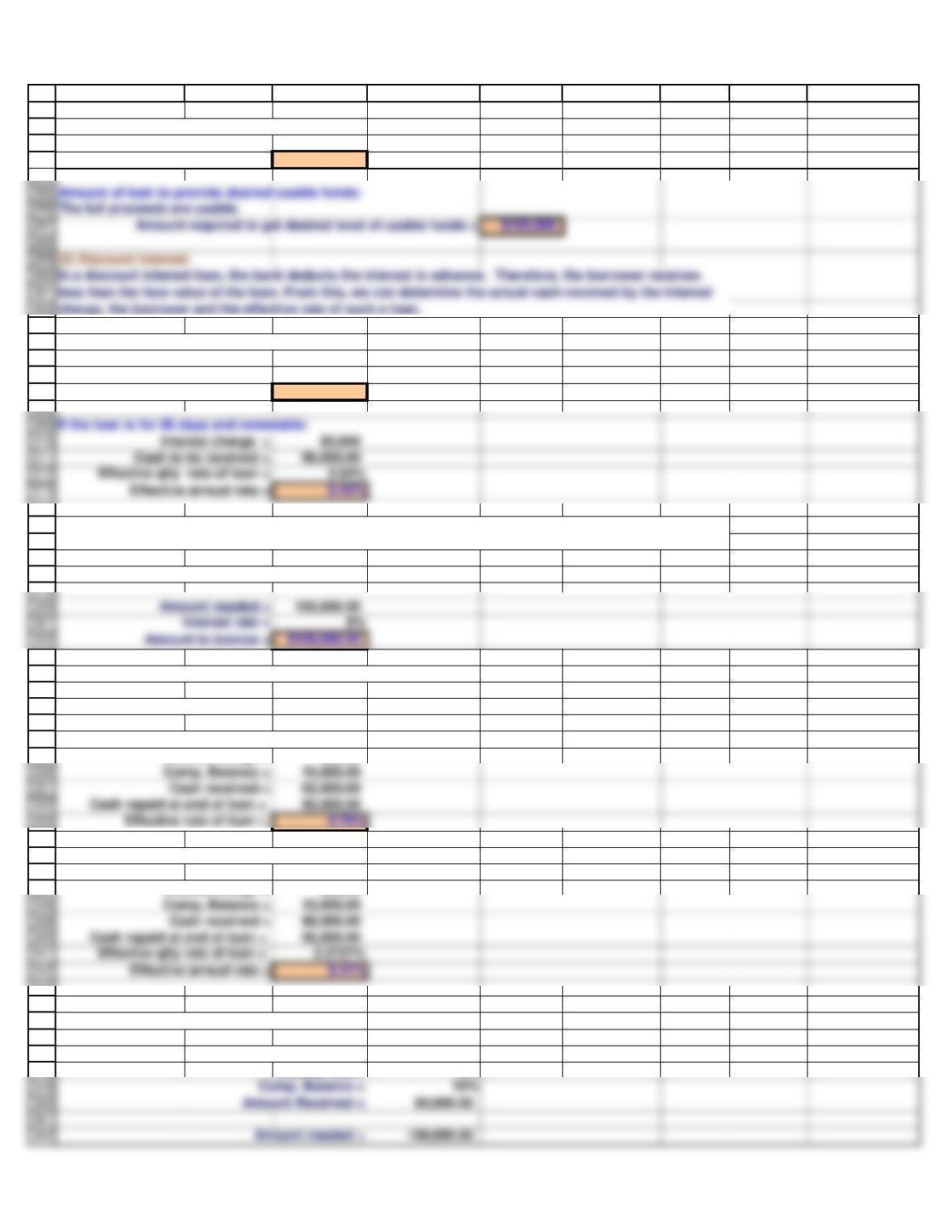

Desired loan amount = $100,000

Quoted interest rate = 8%

However, the new policy is not riskless. If the firm’s customers do not react as predicted, then the firm’s profits could

actually decrease as a result of the change. The amount of risk involved in the decision depends on the uncertainty

inherent in the estimates, especially the sales estimate. Typically, it is very difficult to predict customers‘ responses to

credit policy changes. Further, a credit policy change may prompt the company’s competitors to change their own

credit terms, and this could offset the expected increase in sales. Thus, the final decision is judgmental. If the

prospect of an annual$18,565.4 increase in net income is sufficient to compensate for the risks involved, then the

change should be made. (note: large, national companies often make credit policy changes in a given region in an

effort to determine how customers and competitors will react, and then use the information gained when setting

national policy. Note also that credit policy changes may not be announced in a “broadcast” sense so as to slow down

competitors’ reactions.)

o. Suppose the firm makes the change, but its competitors react by making similar changes to their own credit terms,

with the net result being that gross sales remain at the current $1,000,000 level. What would the impact be on the

firm’s post-tax profitability?

Thus, if expectations are met, the credit policy change would increase the firm’s annual after-tax profit by $18,565.4.

Since there are no non-cash expenses involved here, the $18,565.4 is also the incremental cash flow expected under

the new policy.

p. The brothers need $100,000 and are considering a 1-year bank loan with a quoted annual rate of 8%. The bank is

offering the following alternatives: (1) simple interest, (2) discount interest, (3) discount interest with a 10%

compensating balance, and (4) add-on interest on a 12-month installment loan. What is the effective annual cost rate

for each alternative? For the first three of these assumptions, what is the effective rate if the loan is for 90 days, but

renewable? How large must the face value of the loan amount actually be in each of the 4 alternatives to provide

$100,000 in usable funds at the time the loan is originated?

234

235

236

237

238

239

Credit-related costs:

Carrying costs 4,068.5 7,890.4 -3,821.9

Bad debt losses 11,000.0 20,000.0 –9,000.0

Profit before taxes $246,863.5 $222,109.6 $24,753.9

Taxes (25%) 61,715.9 55,527.4 6,188.5

Net income $185,147.6 $166,582.2 $18,565.4

290

291

292

293

303

304

305

306

307

308

309

310

311

312

313

If the loan is for 90 days and renewable:

Effective annual rate = 8.42%

314

315

316

317

318

319

320

321

322

323

324

325

326

327

328

329

330

331

332

333

Comp. Balance = 10,000.00

334

335

336

337

339

340

341

342

Effective annual rate = 9.41%

343

344

345

346

347

348

349

350

351

352

A B C D E F G H I

If the loan is for 90 days and renewable:

Number of compoundings a year =

4

Effective rate = 8.24%

The effective rate of an annual loan:

Interest charge = $8,000

Cash to be received = 92,000.00

Effective rate of loan = 8.70%

Amount of loan to provide desired usable funds:

(3) discount interest with a 10 percent compensating balance.

compensating bal. % = 10%

The effective rate of an annual loan:

Interest charge = $8,000

If the loan is for 90 days and renewable:

Interest charge = $2,000

Amount of loan to provide desired usable funds:

Loan Amount = 100,000.00

Interest rate = 8%

Notice that this is less than if the loan is for an entire year. The reason it is less is that you don’t have to

pay as much interest up front if you borrow for 90 days and then roll the loan 4 times a year.

294

295

296

297

298

299

300

301

302

Amount of loan to provide desired usable funds:

(2) Discount interest:

353

354

355

356

357

358

359

360

361

362

A B C D E F G H I

Loan Amount = $121,951.22

(4) Add-on interest on a 12-month installment loan.

Loan amount $100,000

Payments 12

Interest rate 8%

The effective rate of an annual loan:

Interest charge = $8,000 The interest charge is simply the interest rate times the loan amount.

363

364

365

366

367

368

369

370

371

372