Answers and Solutions: 25 – 1

Chapter 25

Portfolio Theory and Asset Pricing Models

ANSWERS TO END-OF-CHAPTER QUESTIONS

25-1 a. A portfolio is made up of a group of individual assets held in combination. An asset

that would be relatively risky if held in isolation may have little, or even no risk if held

in a well-diversified portfolio.

The feasible, or attainable, set represents all portfolios that can be constructed from a

given set of stocks. This set is only efficient for part of its combinations.

b. An indifference curve is the risk/return trade-off function for a particular investor and

reflects that investor’s attitude toward risk. The indifference curve specifies an

investor’s required rate of return for a given level of risk. The greater the slope of the

indifference curve, the greater is the investor’s risk aversion.

c. The Capital Asset Pricing Model (CAPM) is a general equilibrium market model

developed to analyze the relationship between risk and required rates of return on assets

when they are held in well-diversified portfolios. The SML is part of the CAPM.

Answers and Solutions: 25 – 2

d. The characteristic line for a particular stock is obtained by regressing the historical

returns on that stock against the historical returns on the general stock market. The

e. Arbitrage Pricing Theory (APT) is an approach to measuring the equilibrium risk/return

relationship for a given stock as a function of multiple factors, rather than the single

factor (the market return) used by the CAPM. The APT is based on complex

mathematical and statistical theory, but can account for several factors (such as GNP

and the level of inflation) in determining the required return for a particular stock.

Answers and Solutions: 25 – 3

SOLUTIONS TO END-OF-CHAPTER PROBLEMS

25-1 bi = iM (i / M) = 0.70(0.40/0.20) = 1.4.

25-3 r

^p = wAr

^A + (1 − wA) r

^B

= 0.30(12%) + 0.70(18%) = 16.20%

25-4 a.

.)rr(rb)rr(rr

M

iiM

RFMRFiRFMRFi

−+=−+=

Answers and Solutions: 25 – 4

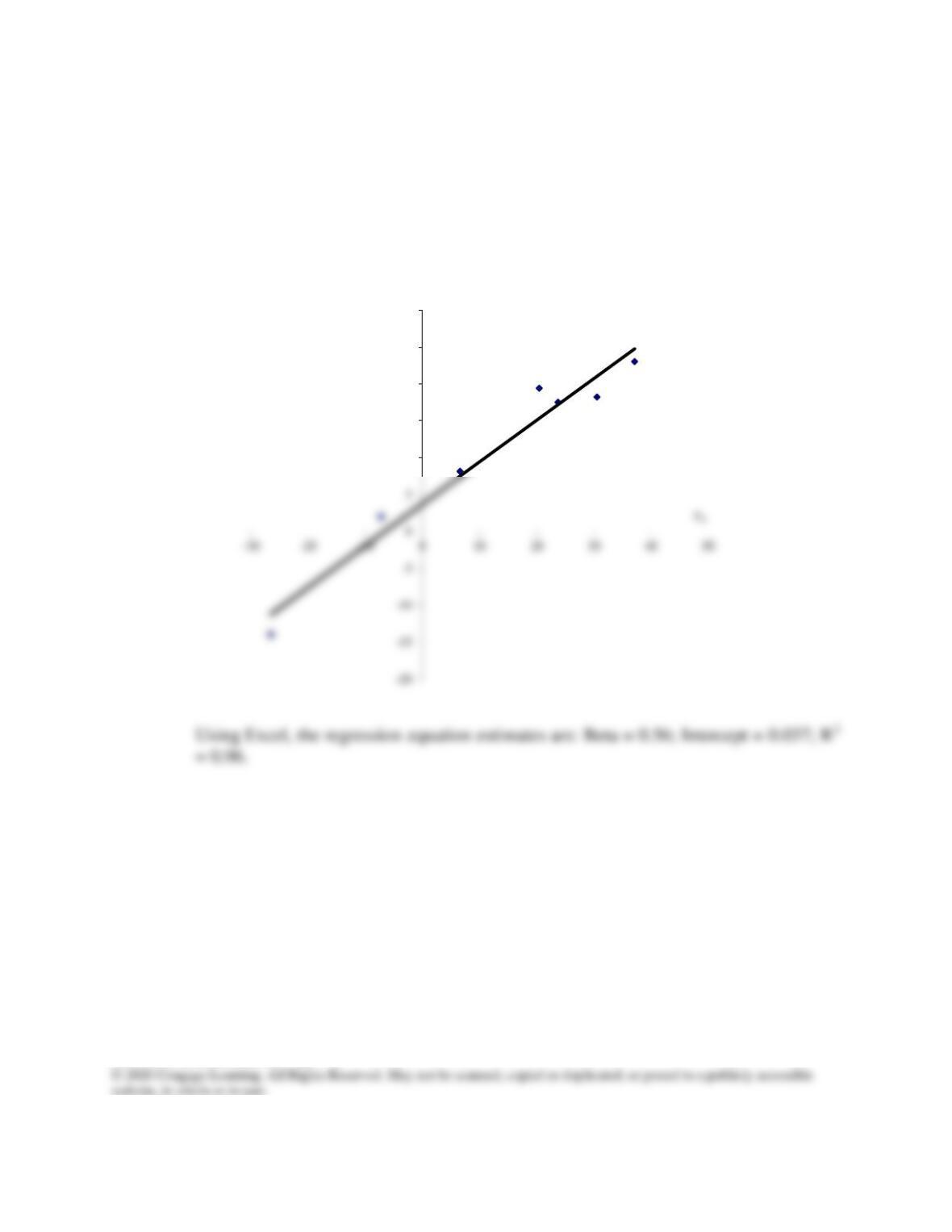

25-5 a. A plot of the approximate regression line is shown in the following figure:

10

15

20

25

30

r

X

(%)

Answers and Solutions: 25 – 5

b. The arithmetic average return for Stock X is calculated as follows:

The standard deviation of returns for the market portfolio is similarly determined to be

22.6 percent. The results are summarized below:

Stock X Market Portfolio

Average return,

Avg

r

10.6% 12.1%

Standard deviation, σ 13.1 22.6

c. Since Stock X is in equilibrium and plots on the Security Market Line (SML), and

given the further assumption that 𝑟

∧

𝑋= 𝑟

−

𝑋 and

MM rr =

—and this assumption often does

not hold—then this equation must hold:

Answers and Solutions: 25 – 7

d. The SML is plotted below. Data on the risk-free security (bRF = 0,

rRF = 8.6%) and Security X (bX = 0.56,

X

r

= 10.6%) provide the two points through

which the SML can be drawn. rM provides a third point.

e. In theory, you would be indifferent between the two stocks. Since they have the same

beta, their relevant risks are identical, and in equilibrium they should provide the same

k(%)

20

r(%)

Answers and Solutions: 25 – 8

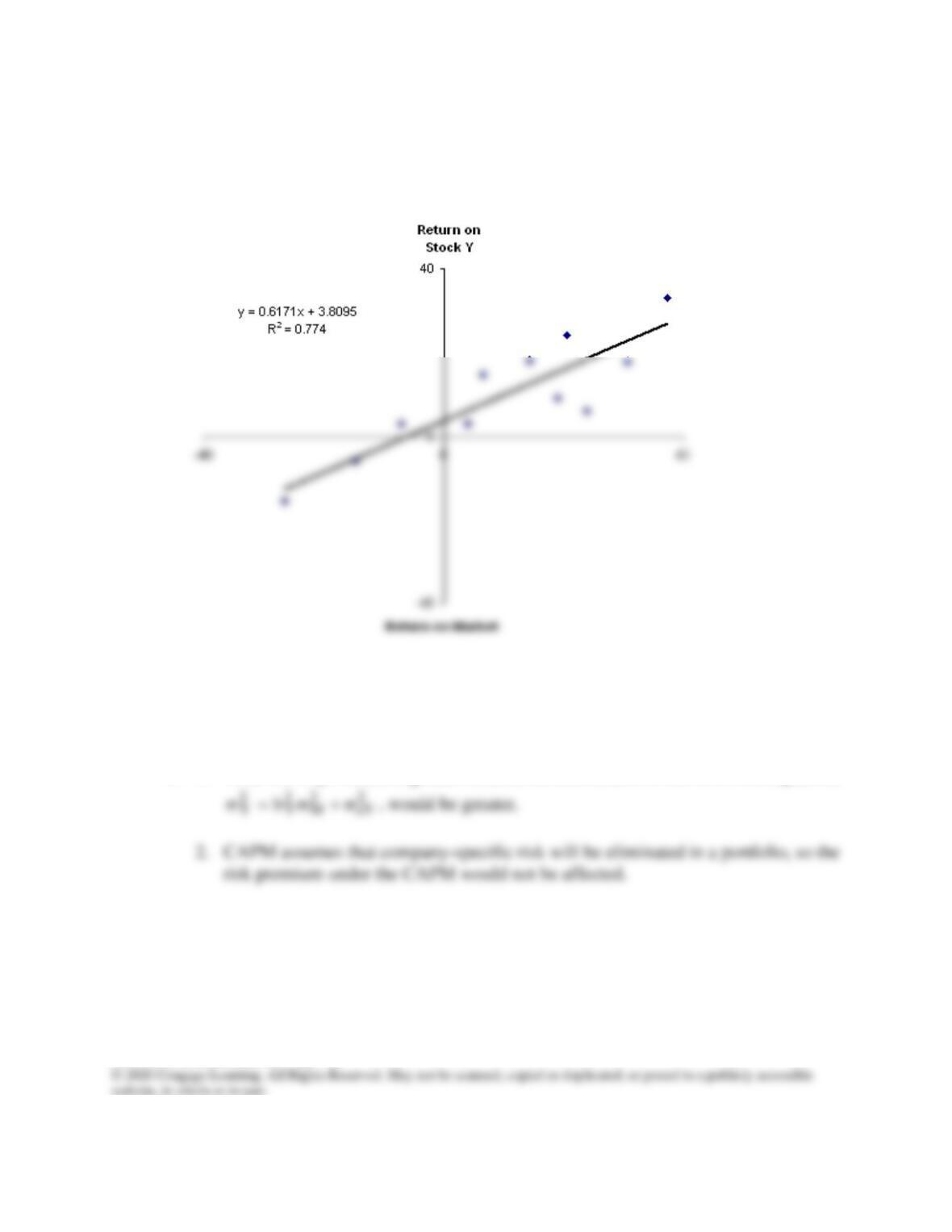

25-6

a. The regression graph is shown below. Using a spreadsheet, we find b = 0.62.

b. Because b = 0.62, Stock Y is about 62 percent as volatile as the market; thus, its relative

risk is about 62 percent of that of an average firm.

c. 1. Total risk

)( 2

Y

would be greater because the second term of the firm’s risk equation,

Answers and Solutions: 25 – 9

d. 1. The stock’s variance would not change, but the risk of the stock to an investor

holding a diversified portfolio would be greatly reduced.

Answers and Solutions: 25 – 10

SOLUTION TO SPREADSHEET PROBLEM

25-7 The detailed solution for the spreadsheet problem is available in the file Ch25 P07 Build

a Model Solution.xlsx on the textbook’s Web site.

Mini Case: 25 – 11

MINI CASE

You have been hired at the investment firm of Bowers & Noon. One of its clients doesn’t

understand the value of diversification or why stocks with the biggest standard deviations

don’t always have the highest expected returns. Your assignment is to address the client’s

concerns by showing the client how to answer the following questions.

a. Suppose asset A has an expected return of 10 percent and a standard deviation of

20 percent. Asset B has an expected return of 16 percent and a standard deviation

of 40 percent. If the correlation between A and B is 0.35, what are the expected

return and standard deviation for a portfolio comprised of 30 percent asset A and

70 percent asset B?

Answer:

r

ˆ

)w1(r

ˆ

wr

ˆBAAAP

−+=

b. Plot the attainable portfolios for a correlation of 0.35. Now plot the attainable

portfolios for correlations of +1.0 and -1.0.

Answer: