CHAPTER 24 –

1

CHAPTER 25

DERIVATIVES AND HEDGING RISK

Answers to Concepts Review and Critical Thinking Questions

1. Since the firm is selling futures, it wants to be able to deliver the lumber; therefore, it is a supplier.

2. Buying call options gives the firm the right to purchase pork bellies; therefore, it must be a consumer

3. Forward contracts are usually designed by the parties involved for their specific needs and are rarely

sold in the secondary market, so forwards are somewhat customized financial contracts. All gains and

losses on the forward position are settled at the maturity date. Futures contracts are standardized to

4. The firm is hurt by declining oil prices, so it should sell oil futures contracts. The firm may not be able

to create a perfect hedge because the quantity of oil it needs to hedge doesn’t match the standard

5. The firm is directly exposed to fluctuations in the price of natural gas since it is a natural gas user. In

6. Buying the call options is a form of insurance policy for the firm. If cotton prices rise, the firm is

protected by the call, while if prices actually decline, they can just allow the call to expire worthless.

7. A put option on a bond gives the owner the right to sell the bond at the option’s strike price. If bond

prices decline, the owner of a put option profits. However, since bond prices and interest rates move

8. The company would like to lock in the current low rates, or at least be protected from a rise in rates,

9. A swap contract is an agreement between parties to exchange assets over several time intervals in the

future. A swap contract is usually an exchange of cash flows, but not necessarily so. Since a forward

10. The firm will borrow at a fixed rate of interest, receive fixed rate payments from the dealer as part of

11. Transaction exposure is the short-term exposure due to uncertain prices in the near future. Economic

exposure is the long-term exposure due to changes in overall economic conditions. There are a variety

12. The risk is that the dollar will strengthen relative to the yen, since the fixed yen payments in the future

13. a. Buy oil and natural gas futures contracts, since these are probably its primary resource costs. If

it is a coal-fired plant, a cross-hedge might be implemented by selling natural gas futures, since

coal and natural gas prices are somewhat negatively related in the market; coal and natural gas

are somewhat substitutable.

14. The company must have felt that the combination of fixed rate bonds plus a swap would result in an

15. He is a little naïve about the capabilities of hedging. While hedging can significantly reduce the risk

of changes in foreign exchange markets, it cannot completely eliminate it. Basis risk is the primary

16. Kevin will be hurt if the yen loses value relative to the dollar over the next eight months. Depreciation

in the yen relative to the dollar results in a decrease in the ¥/$ exchange rate. Since Kevin is hurt by a

decrease in the exchange rate, he should take on a short position in yen-per-dollar futures contracts to

hedge his risk.

Solutions to Questions and Problems

NOTE: All end of chapter problems were solved using a spreadsheet. Many problems require multiple

steps. Due to space and readability constraints, when these intermediate steps are included in this solutions

manual, rounding may appear to have occurred. However, the final answer for each problem is found

without rounding during any step in the problem.

1. The initial price is $2,554 per metric ton and each contract is for 10 metric tons, so the initial contract

value is:

Initial contract value = ($2,554 per ton)(10 tons per contract)

2. The price quote is $16.541 per ounce and each contract is for 5,000 ounces, so the initial contract value

is:

Initial contract value = ($16.541 per oz.)(5,000 oz. per contract)

Initial contract value = $82,705

At a final price of $16.61 per ounce, the value of the position is:

Final contract value = ($16.61 per oz.)(5,000 oz. per contract)

3. The call options give the manager the right to purchase oil futures contracts at a futures price of $65

per barrel. The manager will exercise the option if the price rises above $65. Selling put options

obligates the manager to buy oil futures contracts at a futures price of $65 per barrel. The put holder

4. When you purchase the contracts, the initial value is:

Initial value = 10(100)($1,310)

Initial value = $1,310,000

At the end of the first day, the value of your account is:

Day 1 account value = 10(100)($1,317)

The Day 3 account value is:

Day 3 account value = 10(100)($1,306)

Day 3 account value = $1,306,000

So, your cash flow is:

Day 3 cash flow = $1,306,000 – 1,313,000

5. When you purchase the contracts, your cash outflow is:

Cash outflow = 25(42,000)($2.01)

Cash outflow = $2,110,500

At the end of the first day, the value of your account is:

Day 1 account value = 25(42,000)($2.03)

Day 2 cash flow = $52,500

The Day 3 account value is:

Day 3 account value = 25(42,000)($2.02)

Day 3 account value = $2,121,000

So, your cash flow is:

6. The duration of a bond is the average time to payment of the bond’s cash flows, weighted by the ratio

of the present value of each payment to the price of the bond. Since the bond is selling at par, the

market interest rate must equal 6.1 percent, the annual coupon rate on the bond. The price of a bond

selling at par is equal to its face value. Therefore, the price of this bond is $1,000. The relative value

of each payment is the present value of the payment divided by the price of the bond. The contribution

of each payment to the duration of the bond is the relative value of the payment multiplied by the

amount of time (in years) until the payment occurs. So, the duration of the bond is:

Year

PV of payment

Relative value

Payment weight

1

$57.49

.05749

.05749

2

.05419

.10837

3

888.32

.88832

7. The duration of a bond is the average time to payment of the bond’s cash flows, weighted by the ratio

of the present value of each payment to the price of the bond. Since the bond is selling at par, the

market interest rate must equal 8.6 percent, the annual coupon rate on the bond. The price of a bond

selling at par is equal to its face value. Therefore, the price of this bond is $1,000. The relative value

Year

PV of payment

Relative value

Payment weight

1

$79.19

.07919

.07919

2

72.92

.07292

.14584

3

67.14

.06714

.20143

4

$1,000

Duration =

8. The duration of a portfolio of assets or liabilities is the weighted average of the duration of the

portfolio’s individual items, weighted by their relative market values.

a. The total market value of assets in millions is:

Market value of assets = $43 + 555 + 340 + 103 + 498

Market value of assets = $1,539

CHAPTER 24 –

8

So, the market value weight of each asset is:

b. The total market value of liabilities in millions is:

Market value of liabilities = $605 + 395 + 285

Market value of liabilities = $1,285

Note that equity is not included in this calculation since it is not a liability. So, the market value

9. a. You’re concerned about a rise in corn prices, so you would buy July contracts. Since each contract

is for 5,000 bushels, the number of contracts you would need to buy is:

Number of contracts to buy = 160,000/5,000

Number of contracts to buy = 32

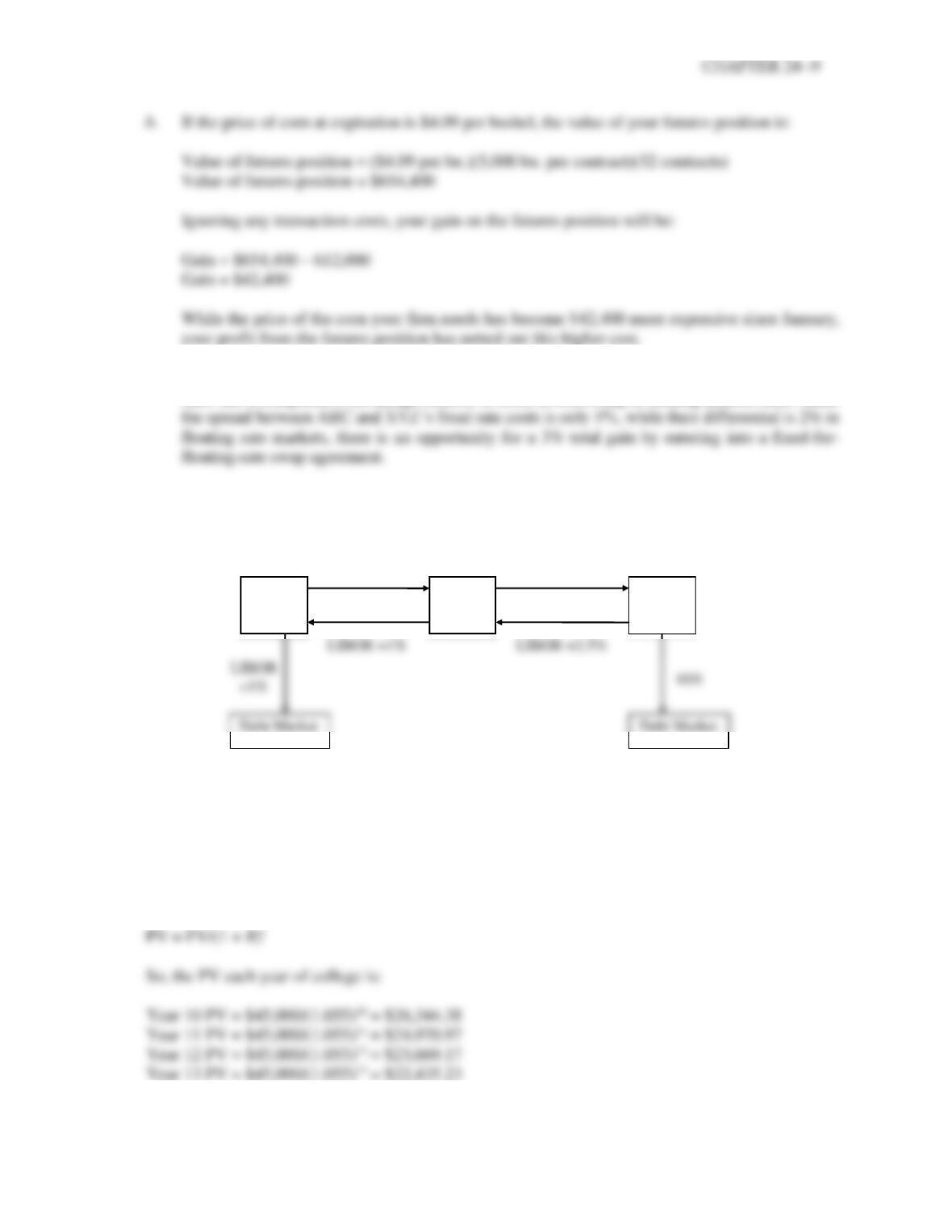

10. a. XYZ has a comparative advantage relative to ABC in borrowing at fixed interest rates, while

ABC has a comparative advantage relative to XYZ in borrowing at floating interest rates. Since

b. If the swap dealer must capture 2% of the available gain, there is 1% left for ABC and XYZ. Any

division of that gain is feasible; in an actual swap deal, the divisions would probably be negotiated

by the dealer. One possible combination is .5% for ABC and .5% for XYZ:

ABC

ABC

ABC

ABC

ABC

Dealer

LIBOR +1%

LIBOR +2.5%

10.5%

XYZ

10.0%

11. The duration of a liability is the average time to payment of the cash flows required to retire the

liability, weighted by the ratio of the present value of each payment to the present value of all payments

related to the liability. In order to determine the duration of a liability, first calculate the present value

of all the payments required to retire it. Since the cost is $45,000 at the beginning of each year for four

years, we can find the present value of each payment using the PV equation:

12. The duration of a bond is the average time to payment of the bond’s cash flows, weighted by the ratio

of the present value of each payment to the price of the bond. We need to find the present value of the

bond’s payments at the market rate. The relative value of each payment is the present value of the

payment divided by the price of the bond. The contribution of each payment to the duration of the

bond is the relative value of the payment multiplied by the amount of time (in years) until the payment

occurs. Since this bond has semiannual coupons, the years will include half-years. So, the duration of

the bond is:

Year

PV of payment

Relative value

Payment weight

.5

$20.50

.02077

.01039

1.0

20.01

.02027

.02027

1.5

19.53

.01979

.02969

2.0

926.78

.93916

Duration =

13. Let R equal the interest rate change between the initiation of the contract and the delivery of the asset.

Cash flows from Strategy 1:

Today

1 Year

Purchase silver

–S0

0

Borrow

Total cash flow

0

Purchase silver

0

Total cash flow

.23029

14. a. The forward price of an asset with no carrying costs or convenience value is:

Forward price = S0(1 + R)

Since you will receive the bond’s face value of $1,000 in 11 years and the 11 year spot interest

rate is currently 7 percent, the current price of the bond is:

b. If both the 1-year and 11-year spot interest rates unexpectedly shift downward by 2 percent, the

appropriate interest rate to use when pricing the bond is 5 percent, and the appropriate interest

rate to use in the forward pricing equation is 3 percent. Given these changes, the new price of the

bond will be:

15. a. The forward price of an asset with no carrying costs or convenience value is:

Forward price = S0(1 + R)

Since you will receive the bond’s face value of $1,000 in 18 months, we can find the price of

the bond today, which will be:

CHAPTER 24 –

12

b. It is important to remember that 100 basis points equals 1 percent and one basis point equals

.01%. Therefore, if all rates increase by 30 basis points, each rate increases by .003. So, the new

price of the bond today will be:

16. The financial engineer can replicate the payoffs of owning a put option by selling a forward contract

and buying a call. For example, suppose the forward contract has a settle price of $50 and the exercise

price of the call is also $50. The payoffs below show that the position is the same as owning a put with

an exercise price of $50: