Chapter 23

Problems 1-10

Input boxes in tan

Output boxes in yellow

Given data in blue

Calculations in red

Answers in green

Chapter 23

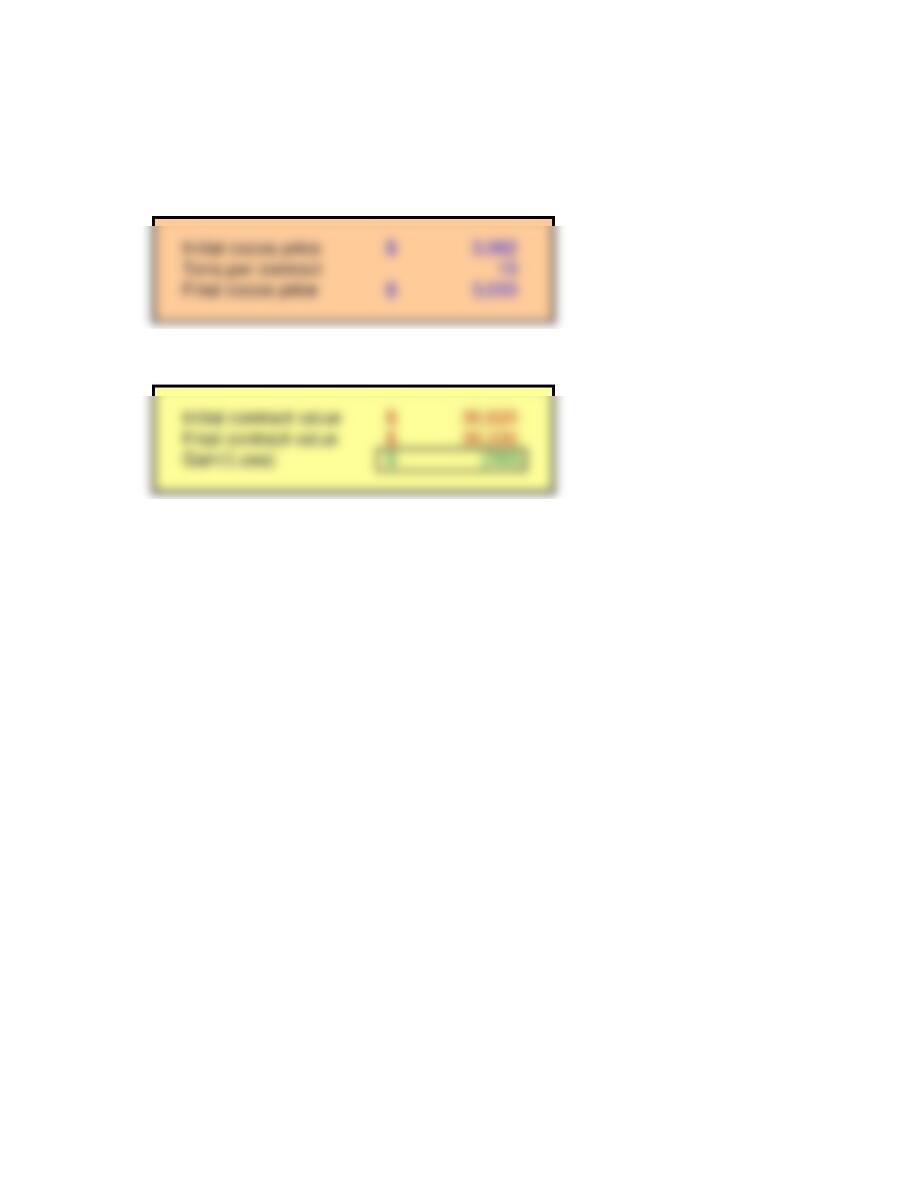

Question 1

Input Area:

Output Area:

Initial contract value 30,620$

Final contract value 30,330$

Initial cocoa price 3,062$

Tons per contract 10

Final cocoa price 3,033$

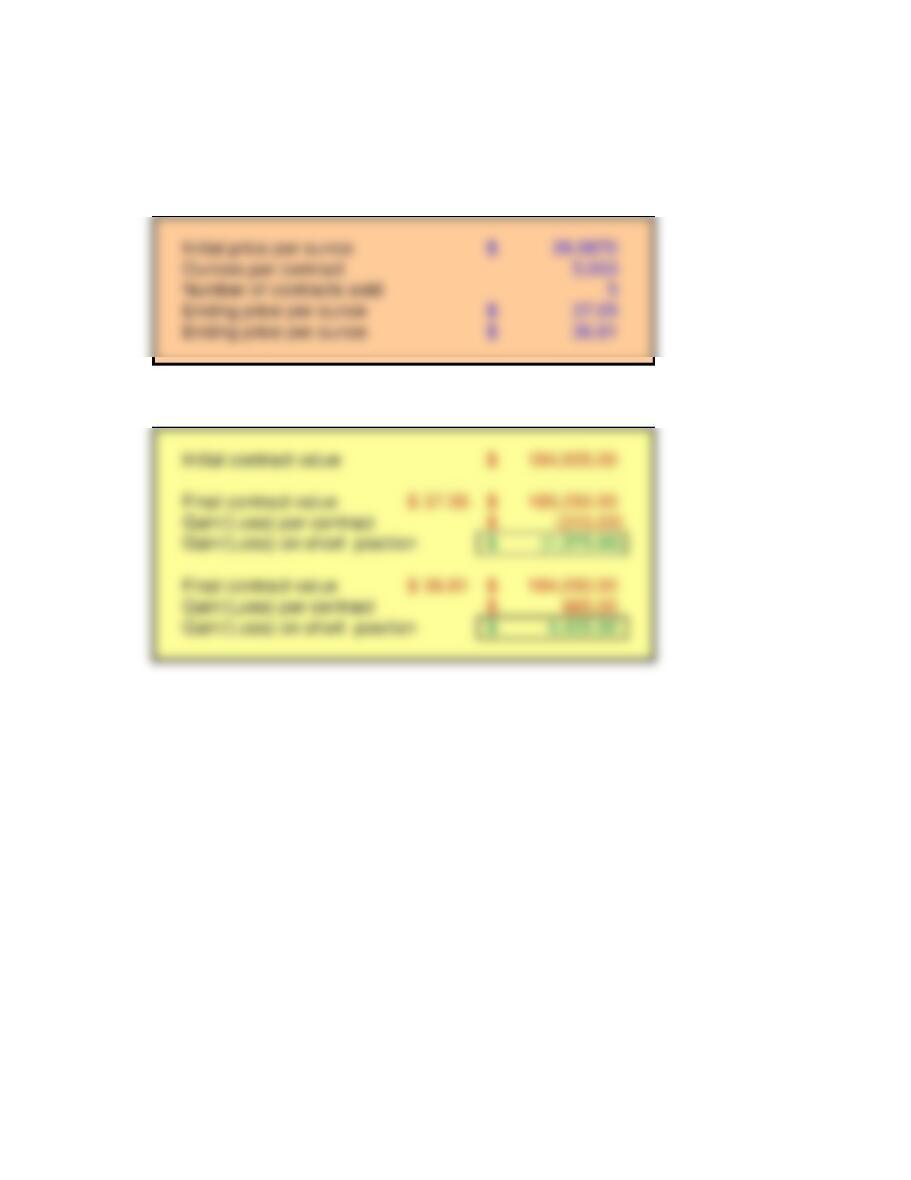

Chapter 23

Question 2

Input Area:

Output Area:

Initial contract value 184,935.00$

Final contract value 37.05$ 185,250.00$

Gain/(Loss) per contract (315.00)$

Final contract value 36.81$ 184,050.00$

Gain/(Loss) per contract 885.00$

Initial price per ounce 36.9870$

Ounces per contract 5,000

Number of contracts sold 5

Ending price per ounce 37.05$

Ending price per ounce 36.81$

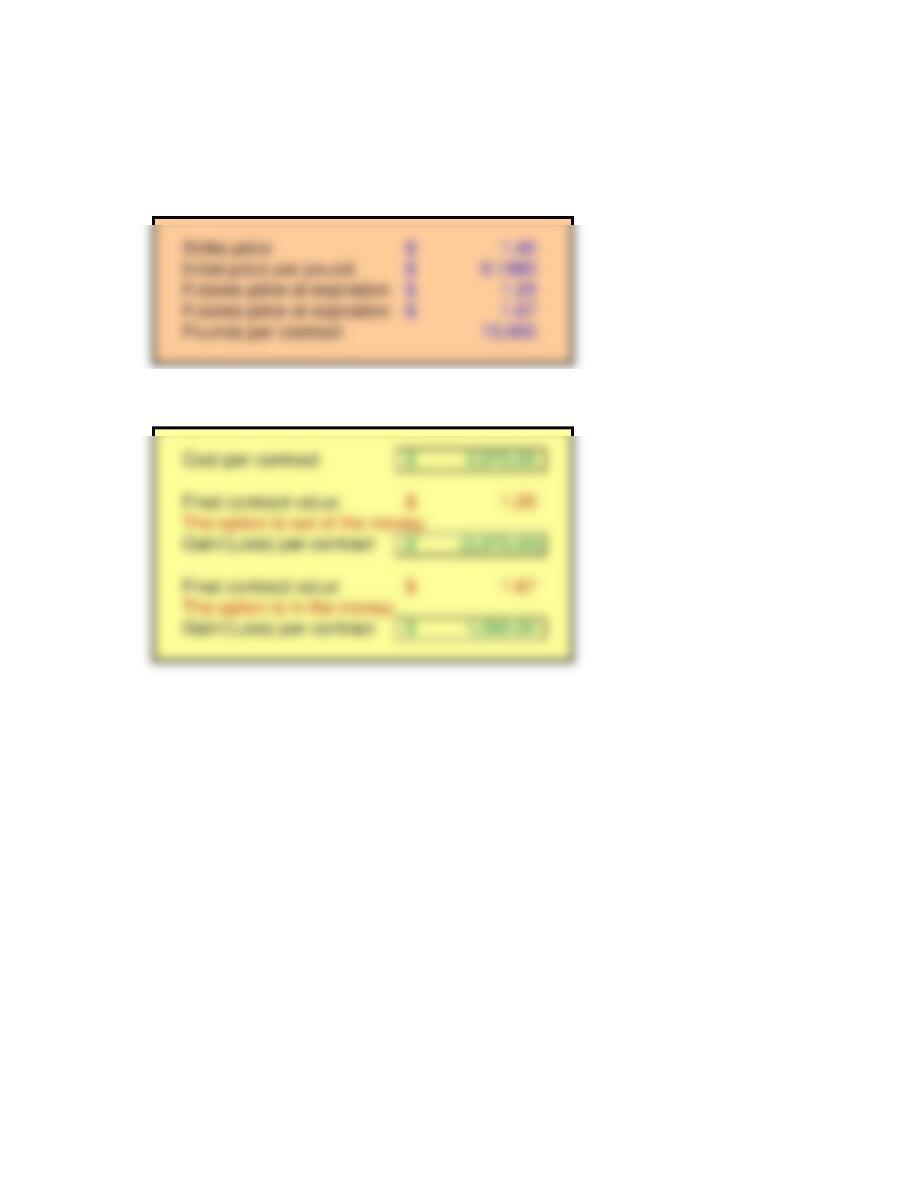

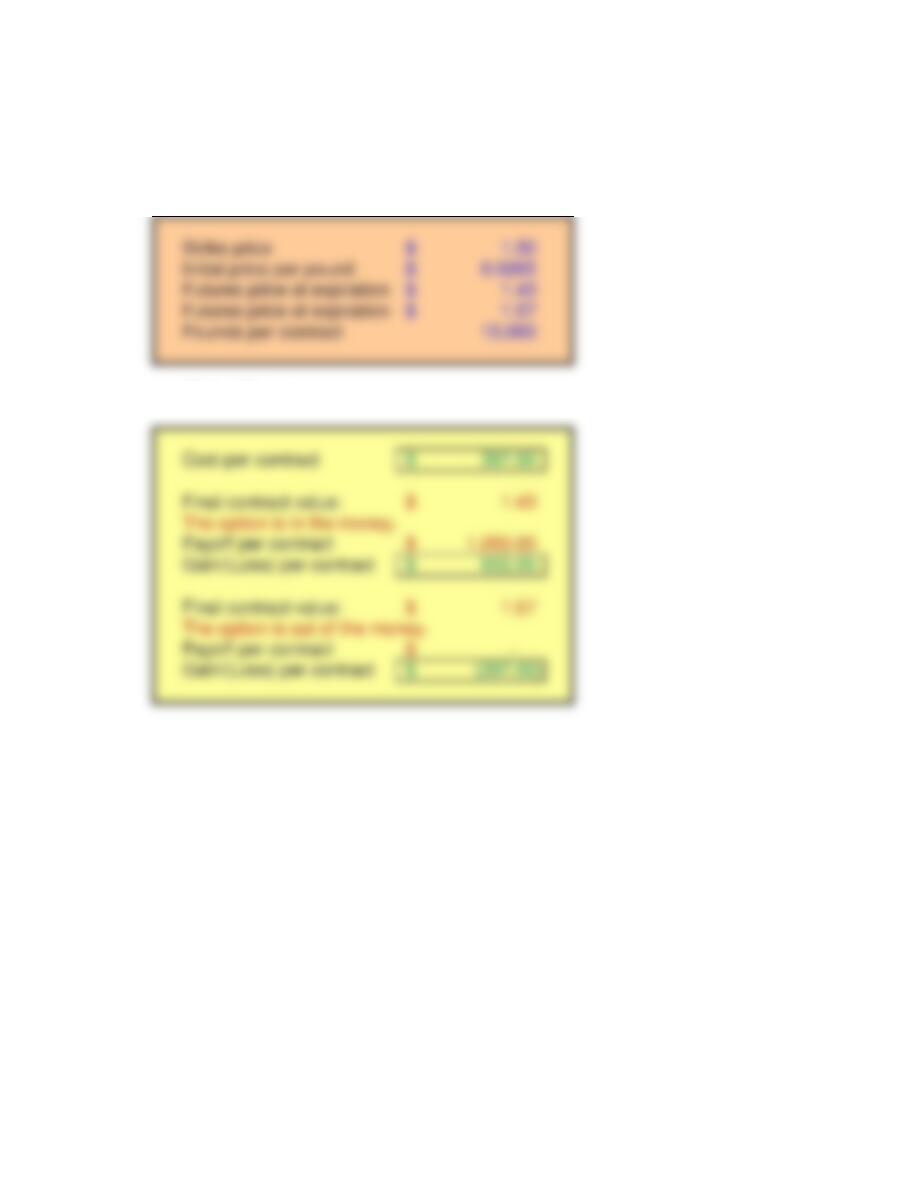

Chapter 23

Question 3

Input Area:

Output Area:

Final contract value: 1.29$

Final contract value: 1.67$

Strike price 1.40$

Initial price per pound 0.1980$

Futures price at expiration 1.29$

Futures price at expiration 1.67$

Pounds per contract 15,000

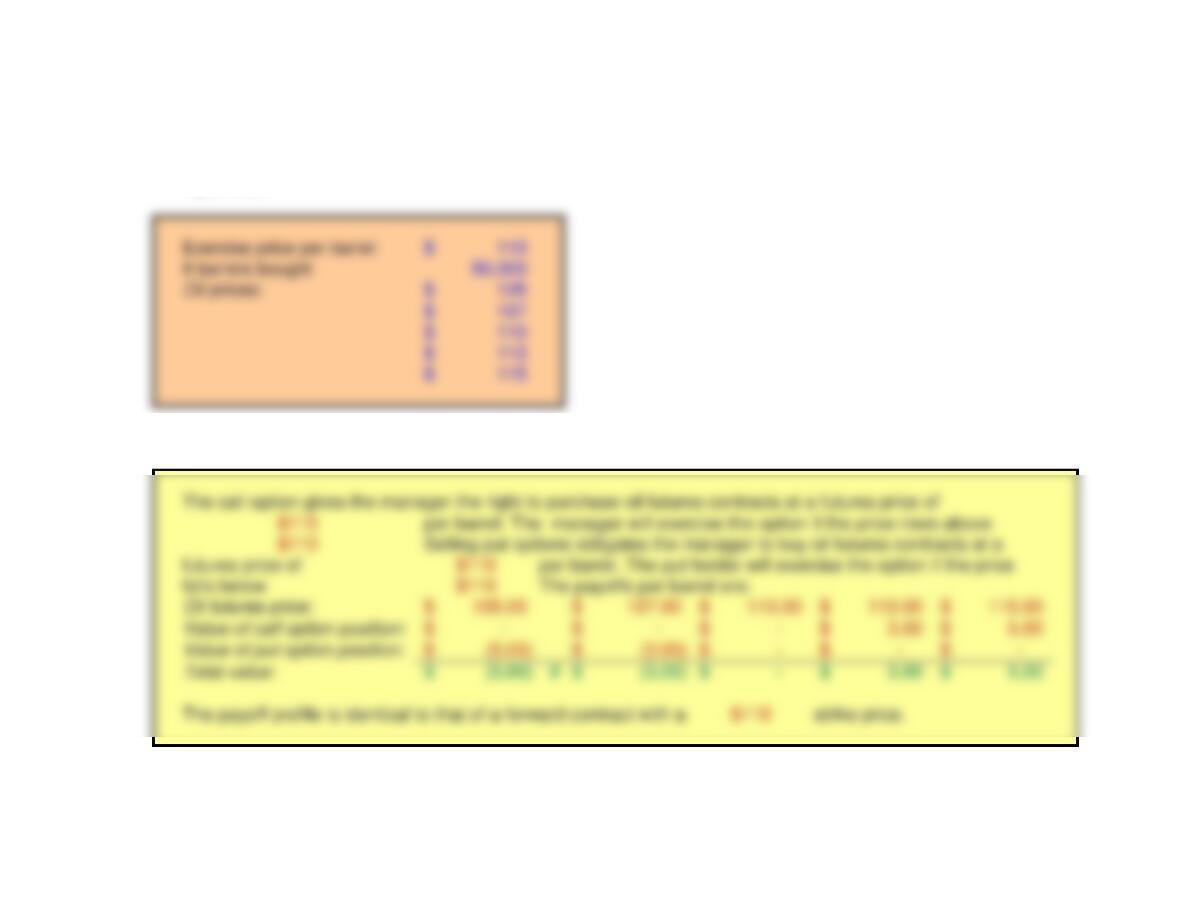

Chapter 23

Question 4

Input Area:

Output Area:

futures price of $110 per barrel. The put holder will exercise the option if the price

falls below $110 The payoffs per barrel are:

Oil futures price: 105.00$ 107.00$ 110.00$ 113.00$ 115.00$

Value of call option position: –$ –$ –$ 3.00$ 5.00$

Value of put option position: (5.00)$ (3.00)$ –$ –$ –$

Exercise price per barrel 110$

# barrels bought 50,000

Oil prices: 105$

Chapter 23

Question 5

Input Area:

Output Area:

Final contract value: 1.43$

Payoff per contract 1,050.00$

Final contract value: 1.57$

Payoff per contract –$

Strike price 1.50$

Initial price per pound 0.0265$

Futures price at expiration 1.43$

Futures price at expiration 1.57$

Pounds per contract 15,000

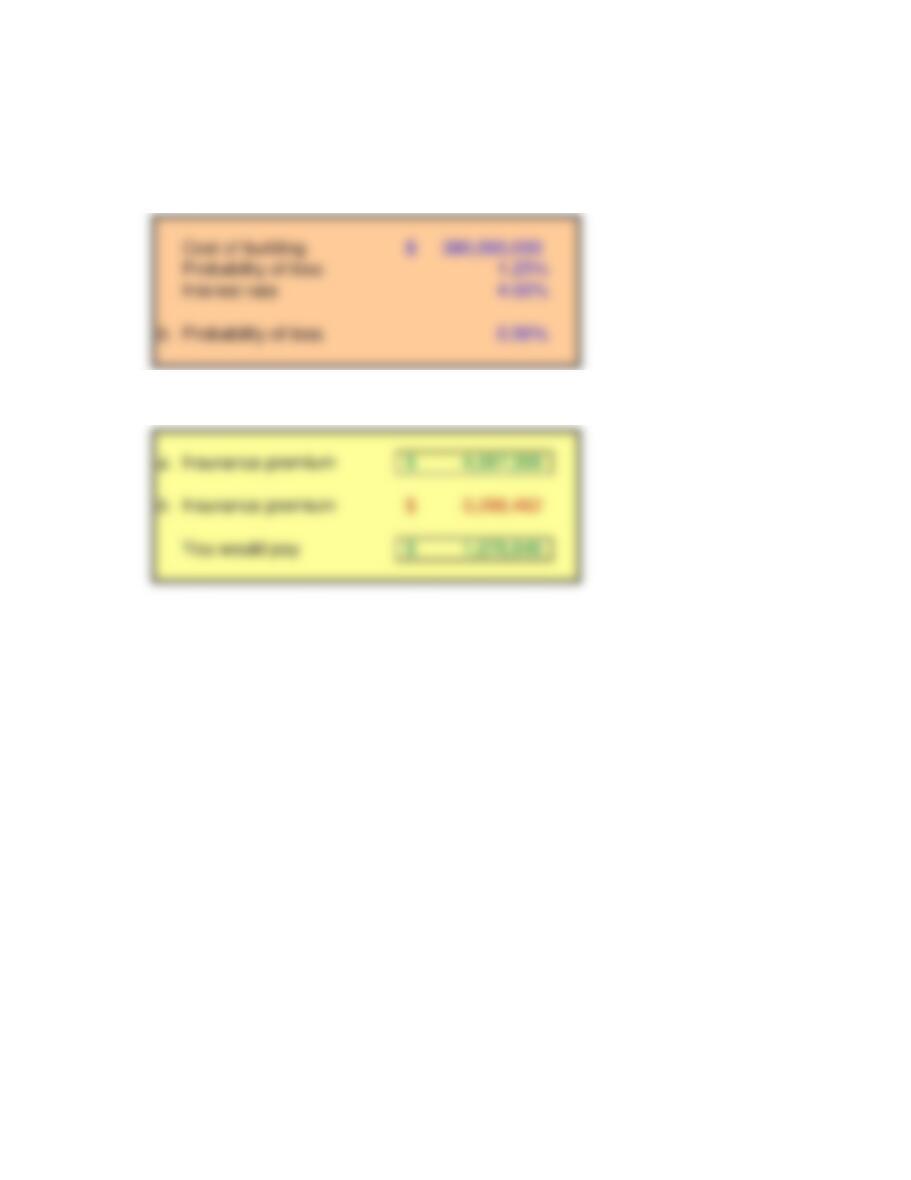

Chapter 23

Question 6

Input Area:

Output Area:

Cost of building 450,000,000$

Probability of loss 1.50%

Chapter 23

Question 7

Input Area:

Output Area:

prices so you would buy: 26

December corn futures contracts. By

price of 6.0025$

per bushel of corn, or 780,325$

Final contract value 757,900$

While the price of corn your firm needs has

less expensive since March, your profit from

Bushels bought 130,000

Bushels per contract 5,000

Contract price per bushel 6.0025$

Ending price per bushel 5.8300$

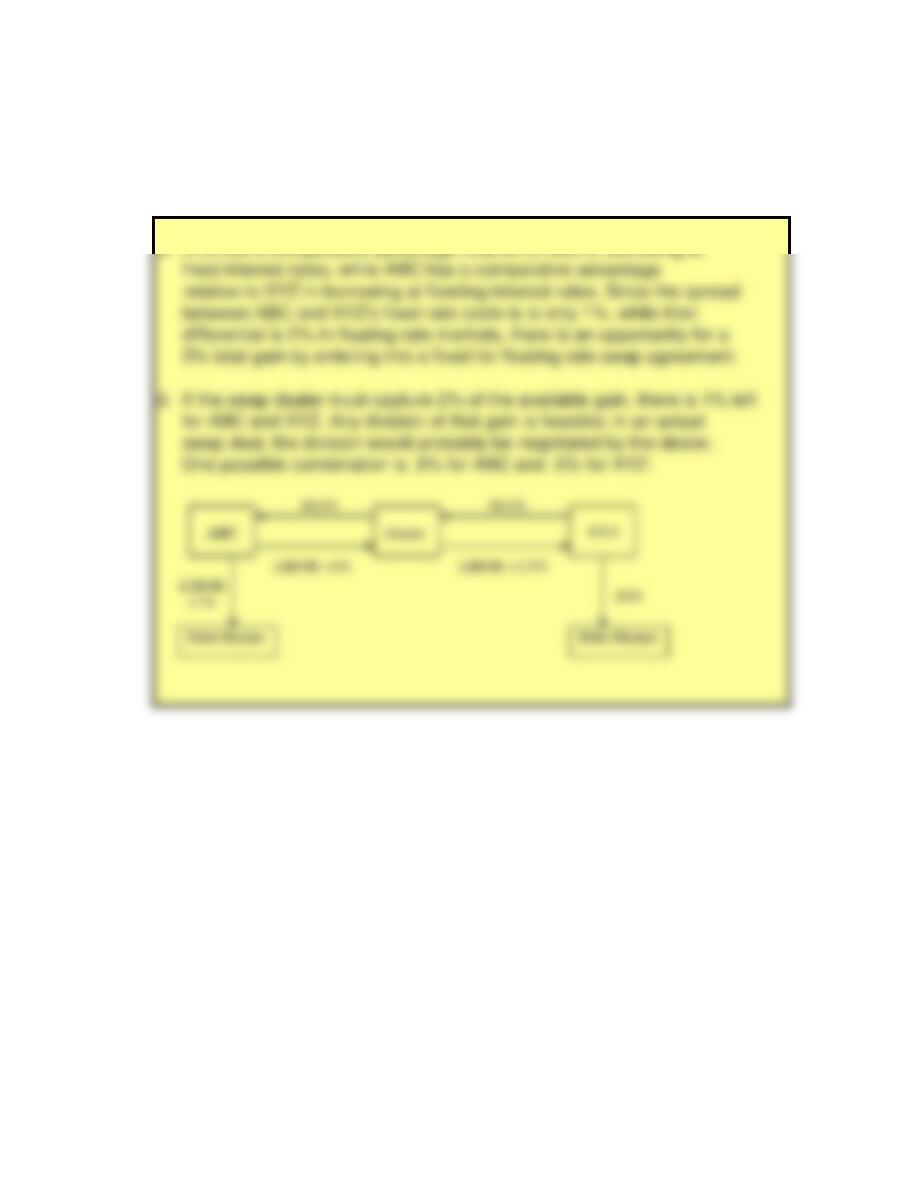

Chapter 23

Question 8

Output Area:

One possible combination is .5% for ABC and .5% for XYZ:

Chapter 23

Question 9

Output Area:

The financial engineer can replicate the payoffs of owning a put option by selling a forward contract and buying a call. For

example, suppose the forward contract has a settle price of $50 and the exercise price of a call is also

Coal futures price: 40$ 45$ 50$ 55$ 60$

Value of call option position: –$ –$ –$ 5$ 10$

Value of forward position: 10$ 5$ –$ (5)$ (10)$

Total value: 10$ 5$ –$ –$ –$

Value of put position: 10$ 5$ –$ –$ –$

The payoffs for the combined position are exactly the same as those of owning a put. This means that, in general, the relationship

between puts, calls, and forwards must be such that the cost of the two strategies will be the same, or an arbitrage opportunity

exists. In general, given any two of the instruments, the third can be synthesized.

Chapter 23

Question 10

Input Area:

Output Area:

Cost of building 380,000,000$