560 Instructor’s Manual

A21-14. The Williams Act was designed to stem a wave of hostile takeovers through tender offers.

Target shareholders may have been unable to evaluate the terms of tender offers in the of-

ten short periods of time for which they were open. Sometimes select shareholders were

Q21-15. What are the restrictions faced by corporate insiders during corporate control events?

A21-15. Insider trading laws attempt to prevent informed trading on material nonpublic infor-

mation (inside information), like an upcoming takeover attempt. SEC Rule 10-b-5 out-

Q21-16. How have individual states become more active monitors of takeover activity?

A21-16. Individual states have become more active monitors of takeover activity. Some states

have adopted various antitakeover and anti-bust-up provisions and formed antitrust agen-

Q21-17.To whom is the board of directors accountable, and how should this responsibility affect

how the board of directors treats an acquisition bid?

Solutions to End-of-Chapter Problems

Overview of Corporate Control Activities

P21-1. A firm has four divisions—food, cookware, retail, and credit services—that generate reve-

nues of $1.5 million, $3.8 million, $5.7 million, and $3.1 million, respectively. Compute

the Herfindahl Index (HI) for the firm. The firm is considering the purchase of a rival re-

tailer, which would increase the retail division’s revenues by another $3.2 million. The

firm is also considering selling its credit services division. Assuming these two actions oc-

cur, what will the HI become? What is the HI if the sale of the credit division does not oc-

cur but the rival is acquired?

Chapter 21 Mergers, Acquisitions and Corporate Control

561

A21-1. Sum all of the sales: $1.5 million + $3.8 million + $5.7 million + $3.1 million = $14.1

million

P21-2. HHG Consultants has been asked to analyze Carol & Carroll Co. (C&C), which has one

retail division. C&C is concerned that it is not focused on its core mission of sales despite

only having one division. Each store is divided into departments: casual clothing (CC),

formal clothing (FC), outerwear (OW), shoes (S), and specialty items (SI). C&C’s initial

impression is that all of the departments contribute equally to sales. However, examination

of each department’s actual sales reveals that the breakdown is very different: $5.2 billion

(CC), $2.7 billion (FC), $3.75 billion (OW), $4.5 billion (S), and $1.7 billion (SI). Com-

pute a Herfindahl Index based on the departments having equal sales and based on the ac-

tual sales. Your conclusion concerning the firm’s becoming unfocused will be based on the

actual HI being lower than the equivalent sales HI scenario. What does your analysis find

with regard to the focus of C&C’s retailing division?

P21-3. Firm X has three divisions that generate revenues of $1.3 billion, $2.5 billion, and $5.2

billion. Firm Y is a competitor with three associated divisions that generate $2 billion each.

Using a Herfindahl Index to measure focus, determine if both Firm X and Firm Y share-

holders would see a merger as an action that would increase or rather decrease focus.

A21-3. Firm X sum of sales: $1.3 billion + $2.5 billion + $5.2 billion = $9 billion

562 Instructor’s Manual

P21-4. Shareholders of the firm Up-4-Grabs (U4G) have been offered $36.00 per share in cash for

each of their U4G shares currently selling for $29.53. What is the control premium being

offered in this cash deal? U4G is also considering a stock-swap offer from another firm,

BuyNow, Inc. (BYN). BYN will issue one share for every two shares of U4G. At what

price will BYN shares be equivalent to the control premium available in the cash offer?

When news leaks out about the merger, BYN shares increase to $77.00 and U4G shares in-

crease to $35.24. What control premium does BYN offer now?

P21-5. HBABB Corp. has purchased all of the 10 million shares of BOBCO stock for $43.75 a

share. BOBCO’s net asset value is $350 million. How much goodwill does HBABB need

to consider on its balance sheet? Suppose part of the deal requires HBABB to pay $30 mil-

lion of BOBCO’s debt. Refigure the net asset value (i.e., reduce the debt by $30 million)

and then recalculate the goodwill. One of your accountants tells you that the net asset value

should not be changed and that the $30 million used for BOBCO’s debt should be added to

the purchase price. Refigure the goodwill calculation and determine if there really is a dif-

ference. If there is a difference, which calculation is correct?

A21-5. Goodwill: $43.75*10 million – $350 million = $87.5 million

P21-6. Mega Service Corporation (MSC) is offering to exchange 2.5 shares of its own stock for

each share of target firm Norman Corporation stock as consideration for a proposed mer-

ger. There are 10 million Norman Corp shares outstanding, and its stock price was $60 be-

fore the merger offer. MSC’s pre-offer stock price was $30. What is the control premium

percentage offered? Now suppose that, when the merger is consummated eight months lat-

er, MSC’s stock price drops to $25. At that point, what is the control premium percentage

and total transaction value?

A21-6. The pre-offer value of Norman Corporation is $600 million (10 million shares × $60/share)

Chapter 21 Mergers, Acquisitions and Corporate Control

563

P21-7. Bulldog Industries is offering, as consideration for merger target Blazerco, 1.5 shares of

their stock for each share of Blazerco. There are 1 million shares of Blazerco outstanding,

and its stock price was $50 before the merger offer. Bulldog’s preoffer stock price was

$40. What is the control premium percentage offered? Now suppose that when the merger

is consummated six months later, Bulldog’s stock price drops to $30. At that point, what is

the control premium percentage and total transaction value?

A21-7. The pre-offer value of Blazerco is $50 million (1 million shares × $50/share) and Bulldog

P21-8. You are the director of capital acquisitions for Crimson Software Company. One of the

projects you are considering is the acquisition of Geekware, a private software company

that produces software for finance professors. Dave Vanzandt, the owner of Geekware, is

amenable to the idea of selling his enterprise to Crimson, but he has certain conditions that

must be met before selling. The primary condition set forth is a nonnegotiable, all-cash

purchase price of $20 million. Your project analysis team estimates that the purchase of

Geekware will generate the following marginal cash flow:

Year

Cash Flow

1

$1,000,000

2

3,000,000

3

5,000,000

4

7,500,000

5

7,500,000

Of the $20 million in cash needed for the purchase, $5 million is available from retained

earnings, with a required return of 12%, and the remaining $15 million will come from a

new debt issue yielding 8%. Crimson’s tax rate is 40%. Should you recommend acquiring

Geekware to your CEO?

A21-8. First, we calculate the weighted average cost of capital (WACC), which is the required re-

turn on the proposed acquisition.

564 Instructor’s Manual

P21-9. You are the director of capital acquisitions for Morningside Hotel Company. One of the

projects you are deliberating is the acquisition of Monroe Hospitality, a company that owns

and operates a chain of bed-and-breakfast inns. Susan Sharp, Monroe’s owner, is willing to

sell her company to Morningside only if she is offered an all-cash purchase price of $5 mil-

lion. Your project analysis team estimates that the purchase of Monroe Hospitality will

generate the following after-tax marginal cash flow:

Year

Cash Flow

1

$1,000,000

2

1,500,000

3

2,000,000

4

2,500,000

5

3,000,000

If you decide to go ahead with this acquisition, it will be funded with Morningside’s stand-

ard mix of debt and equity at the firm’s weighted average (after-tax) cost of capital of 9%.

Morningside’s tax rate is 30%. Should you recommend acquiring Monroe Hospitality to

your CEO?

A21-9. We use the 9.0% WACC to find the present value of the forecast marginal cash

flow.

P21-10. Firm A plans to acquire Firm B. The acquisition would result in incremental cash flows for

Firm A of $10 million in each of the first five years. Firm A expects to divest Firm B at the

end of the fifth year for $100 million. The β for Firm A is 1.1, which is expected to remain

unchanged after the acquisition. The risk-free rate, Rf, is 7%, and the expected market rate

Chapter 21 Mergers, Acquisitions and Corporate Control

565

of return, Rm, is 15%. Firm A is financed by 80% equity and 20% debt, and this lever-

age will also remain unchanged after the acquisition. Firm A pays interest of 10% on its

debt, which will also remain unchanged after the acquisition.

a. Disregarding taxes, what is the maximum price that Firm A should pay for Firm B?

b. Firm A has a stock price of $30 per share and 10 million shares outstanding. If Firm B

shareholders are to be paid the maximum price determined in part (a) via a new stock

issue, how many new shares will be issued, and what will be the postmerger stock

price?

A21-10. a. First calculate the cost of capital that should be applied to this investment.

b. Number of new shares issued at assumed $30/share price:

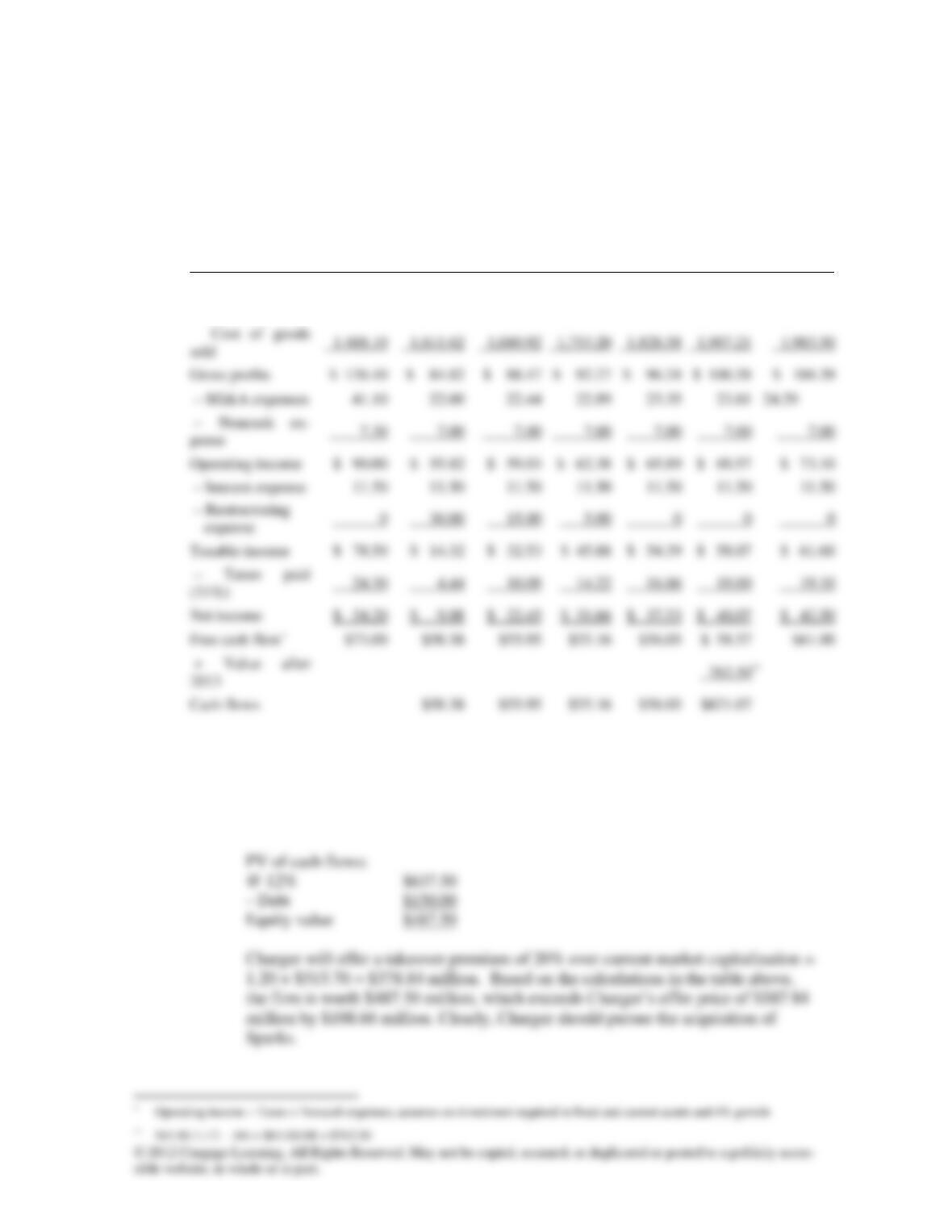

P21-11. Charger Incorporated and Sparks Electrical Company are competitors in the business of

electrical components distribution. Sparks is the smaller firm and has garnered the attention

of the management of Charger, as Sparks has taken away market share from the larger firm

by increasing its sales force over the past few years. Charger is considering a takeover offer

for Sparks and has asked you to serve on the acquisition valuation team that will turn into

the due diligence team if an offer is made and accepted. Given the following information

and assumptions:

a. Make your recommendation about whether or not the acquisition should be pursued.

b. Assume Sparks has accepted the takeover offer from Charger, and now the new subsid-

iary must be consolidated within Charger’s financial statements. Taking Sparks’s most

recent balance sheet and a restated market value of assets of $295.6 million, calculate

the goodwill that must be booked for this transaction.

566 Instructor’s Manual

Sparks Electrical Company

Condensed Balance Sheet

Previous Year (2011) ($ in millions)

Current assets

$ 12.2

Fixed assets

Total assets

Current liabilities

Long-term debt

150.0

Total liabilities

Total liabilities and equity

$457.7

Sparks Electrical Company

Condensed Income Statement

Previous Five Years ($ in millions)

2011

2010

2009

2008

2007

Revenues

$1,626.5

$1,614.1

$1,485.2

$1,380.5

$1,373.4

Less: Cost of goods sold

Gross profit

$ 138.4

$ 23.2

$ 109.1

ciation & amortization)

6.7

6.6

Less: Operating expense

Operating profit (EBIT)

$ 79.7

$ 67.5

Less: Interest expense

(EBT)

Less: Taxes paid

Net income

$ 46.9

$ 38.7

Assumptions:

• Sparks would become a wholly owned subsidiary of Charger.

• Revenues will continue to grow at 4.3% for the next five years and will level off at

4% thereafter.

Chapter 21 Mergers, Acquisitions and Corporate Control

567

• Charger will offer Sparks a takeover premium of 20% over current market capi-

talization.

A21-11. a. Assume Charger is an all equity firm and plans on remaining so after the merger

and that the appropriate discount rate is Charger’s 12% cost of equity. The cash flows

and present values are calculated in the following table:

Cash Flow Development ($ in millions)

2011

2012

2013

2014

2015

2016

2017

Revenues

$1,626.50

$1,696.44

$1,769.39

$1,845.47

$1,924.83

$2,007.59

$2,087.90

Operating income

$ 62.38

$ 65.89

$ 69.57

Taxable income

$ 54.39

$ 58.07

Cash flows

* Operating income – Taxes + Noncash expenses; assumes no investment required in fixed and cur-

rent assets and 4% growth

** $61.00 / (.12 – .04) = $61.00/.08 = $762.50

568 Instructor’s Manual

P21-12. Referring to Problem 21-11, assume it is now two years after the acquisition of Sparks, and

you must perform a goodwill impairment test of the subsidiary. Growth expectations have

been lowered to 3% going forward. Using the following five-year projection of cash flows

and a 12% cost of equity, estimate the value of the subsidiary beyond year 5, the current

value of the subsidiary, the current value of goodwill, and any goodwill impairment. Total

assets (excluding intangibles) are now $612.5 million, and total liabilities are $175.0 mil-

lion.

Cash Flow Projections for Next Five Years

2014

2015

2016

2017

2018

Revenues

$1,815.2

$1,869.7

$1,925.7

$1,983.5

$2,043.0

1,724.4

1,776.2

1,884.3

1,940.9

Gross profit

$ 90.8

$ 93.5

$ 99.2

$ 102.1

$ 23.0

$ 23.5

$ 24.4

7.0

7.0

7.0

Less: Operating expense

$ 30.0

$ 30.5

$ 31.4

Operating profit (EBIT)

Less: Interest expense

Earnings before taxes (EBT)

$ 44.3

$ 51.5

$ 56.3

Less: Taxes paid

13.7

16.0

17.4

Net income

Free cash flow

A21-12.These values were calculated by applying the following equation for each year using the

relevant values from the table:

Chapter 21 Mergers, Acquisitions and Corporate Control

569

Discounting back to today (the beginning of 2011) at the 12% rate we get:

The current value of the subsidiary is the sum of the horizon value and the present value of

the cash flows from 2011-2015.

P21-13.

Firms AFD, TYU, CHG, and LAN are competitors within an industry. Their respective

sales figures are $2.8 billion, $3.9 billion, $4.8 billion, and $2.1 billion. What is the Her-

findahl Index (HI) for the industry? Is the industry considered highly concentrated, moder-

ately concentrated, or not concentrated? Assuming that two more firms—QBC ($3.6

billion in sales) and RTY ($2.7 billion in sales)—are added to the industry figures, does the

concentration level of the industry change? (Recompute HI to determine this.) If the three

smallest firms (AFD, LAN, and RTY) merged, would the FTC be concerned? If so, why?

(Note: The HI is measured in units of %2. For example, 50% × 50% = 2,500%2 (or, in dec-

imal form, 0.50 × 0.50 = 0.25). To make the conversion from decimal to percentage form

mathematically, multiply the answer by 10,000; using the same example, this yields 0.50 ×

0.50 × 10,000 = 2,500.)

570 Instructor’s Manual

Sum of sales with two more firms in industry: $13.6 billion + $3.6 billion + $2.7 billion =

$19.9 billion

P21-14.

Bogey Inc. (BOG), with a share price of $36 and EPS of $3, purchases Zoe Corp., with a

pre-acquisition share price of $20 and EPS of $2, for a 10% premium. If the deal is fi-

nanced exclusively with BOG equity and no material synergies are expected, is the deal

accretive or dilutive to BOG shareholders?

A21-14. BOG’s P/E multiple is 12x ($36 / $3). Zoe’s post-acquisition implied P/E is 11x [($20 x

P21-15.Following the previous question, what if BOG instead financed the acquisition entirely

with debt at an after-tax cost of 9%? Would the deal be accretive or dilute to earnings for

BOG shareholders?

A21-15. For this problem, again pretend BOG has 1 share worth $36 and the entire company is

P21-16. GRJ Corp. just reported $10 million in after-tax earnings and management expects to grow

at 3% in perpetuity with a weighted average cost of capital of 13%:

. a. How would you value GRJ using a growing perpetuity formula?

b. If GRJ’s market capitalization is $100 million, what does this say about the market’s

perception of management’s growth and/or cost of capital expectations?

A21-16.

Chapter 21 Mergers, Acquisitions and Corporate Control

571

P21-17.Posada Corp. (POS) expects to earn EBITDA of $4.2 million next year and expects slow

but steady growth thereafter. POS’s three key competitors (nearly identical operations and

growth prospects) are JET (EBITDA of $5.1 million, Market Capitalization of $30.3 mil-

lion), PET (EBITDA of $2.8 million, Market Capitalization of $15.4 million) and MO

(EBITDA of $6.5 million, Market Capitalization of $40 million). What would you estimate

POS’s market valuation to be?

A21-17. As illustrated in the below table, you can average the EBITDA multiples of the three

P21-18. You are assessing a potential acquisition for a client and your analyst informs you that the

historic EBITDA multiple based on Public Comparables is 5.8 and the historic EBITDA

multiple based on Precedent Transactions is 7.3. If the target is expecting EBITDA of $90

million, what are the valuations under each method? Can you rationalize the difference be-

tween the two?

P21-19. A given market was initially segmented evenly among 20 firms (Phase 1). Five years later,

the market was still segmented evenly among competing firms, but there were now only 10

firms (Phase 2). Eventually six firms emerged with equal portions of the market (Phase 3),

but a move toward deregulation of the industry has prompted two of the firms to merge.

Determine the Herfindahl–Hirschman Index for the three phases. Next, determine whether

the merger will cause the industry to be considered highly concentrated. In a preemptive

move (fearing the FTC), the merged firms agree to sell off portions of the market to the

other four firms so that the market will be equally divided among all five firms. How does

this affect the HI, and is the merger viable under these circumstances?

572 Instructor’s Manual

THOMSON ONE Business School Edition: Since P21-20 is based on using a live database, an-

swers will vary from moment to moment. This is a chance for your students to use a version of a

tool that CFAs use every day.

Answer to MiniCase

Mergers, Acquisitions, and Corporate Control

Jackson Enterprises (JE) is offering a 25% takeover premium to Michael Studios, Inc. (MSI) for

the firm’s 2 million outstanding shares, which are currently trading for a pre-offer price of $20 per

share.

The balance sheet for MSI is:

Assets

Liabilities

The sales (in millions) for the industry by company are:

Sales

ABC

$89

CWC

66

Assignment

1. Determine the amount Jackson Enterprises is willing to pay in terms of goodwill.

2. If JE’s shares are currently trading at $62.43, then how many shares should JE offer for every

Chapter 21 Mergers, Acquisitions and Corporate Control

573

Answers

1. Jackson Enterprises is willing to pay $25 per share ($20 * 1.25), or $50,000,000 for MSI.

3.

Assets

Current

$15,000,000

Total

$82,500,000

Current

4.

Pre-merger

Post-merger

Sales

Market

Share

Market Share

Squared

Sales

Market

Share

Market

Share

Squared

ABC

89

23.99%

0.0575

89

23.99%

0.0575

66

17.79%

0.0316

66

17.79%

0.0316

KOJ

42

11.32%

0.0128

42

11.32%

0.0128

18

4.85%

0.0024