1

2

3

4

5

6

7

11

12

13

14

15

16

17

18

19

24

25

26

27

31

32

33

34

46

A B C D E F G H I J K

11/23/2018

Situation

Proposition I.

Input Data Firm U Firm L

No Debt Some Debt

SL = VL − D

b. Assume that Firms U and L are in the same risk class, and that both have EBIT = $560,000. Firm U uses no debt financing, and its cost of equity

is rsU = 14%. Firm L has $1 million of debt outstanding at a cost of rd = 8%. There are no taxes. Assume that the MM assumptions hold, and then:

1. The weighted average cost of capital is independent of the firm’s capital structure.

2. The WACC of a firm with debt is equal to the unlevered cost of equity.

Chapter 21. Mini Case

David Lyons, the CEO of Lyons Solar Technologies, is concerned about his firm’s level of debt financing. The company uses short-term debt to

a. Business Week recently ran an article on companies‘ debt policies, and the names Modigliani and Miller (MM) were mentioned several times

as leading researchers on the theory of capital structure. Briefly, who are MM, and what assumptions are embedded in the MM and Miller

models? Answer: See Chapter 21 Mini Case Show

matter, he poses the following questions to you, his recently hired assistant.

47

48

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

89

90

91

92

A B C D E F G H I J K

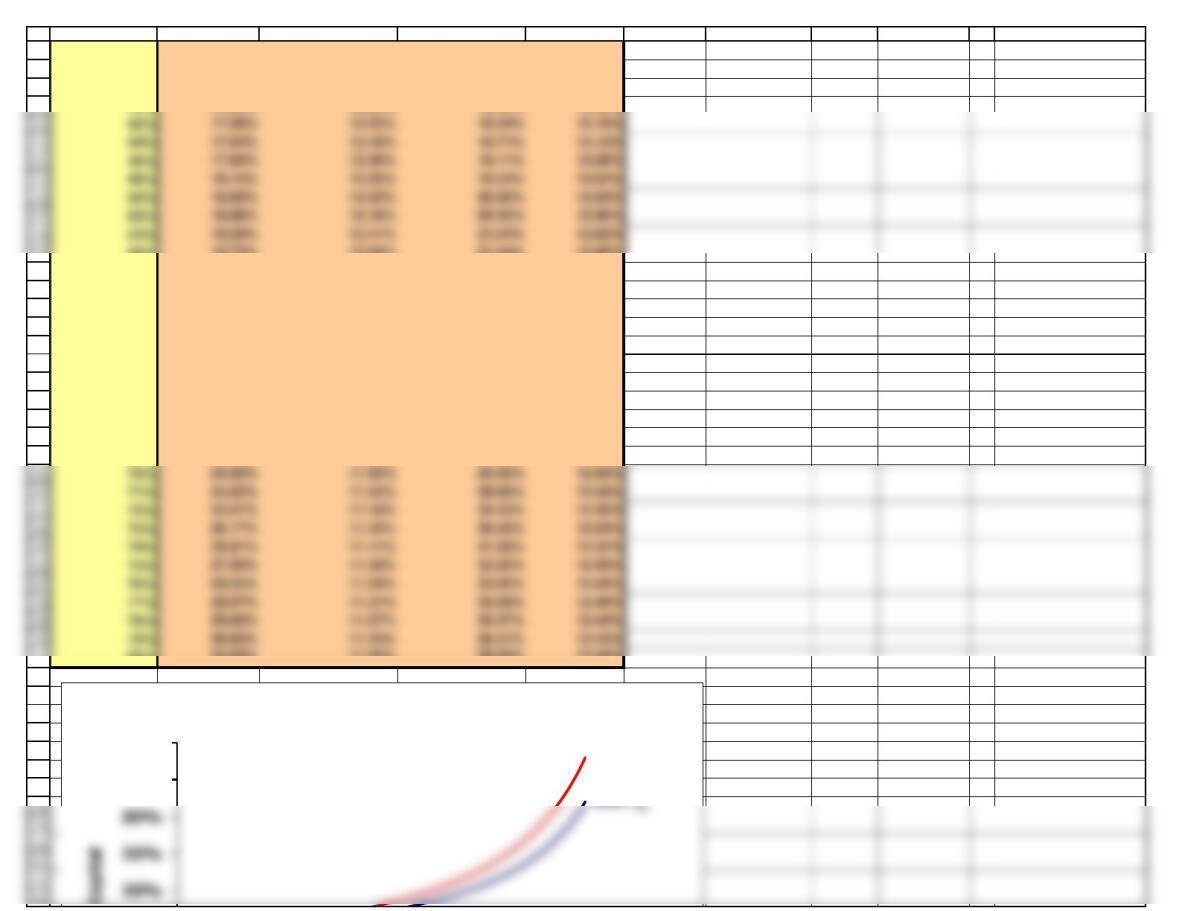

= $3,000,000

MM without Taxes (Millions of dollars)

D

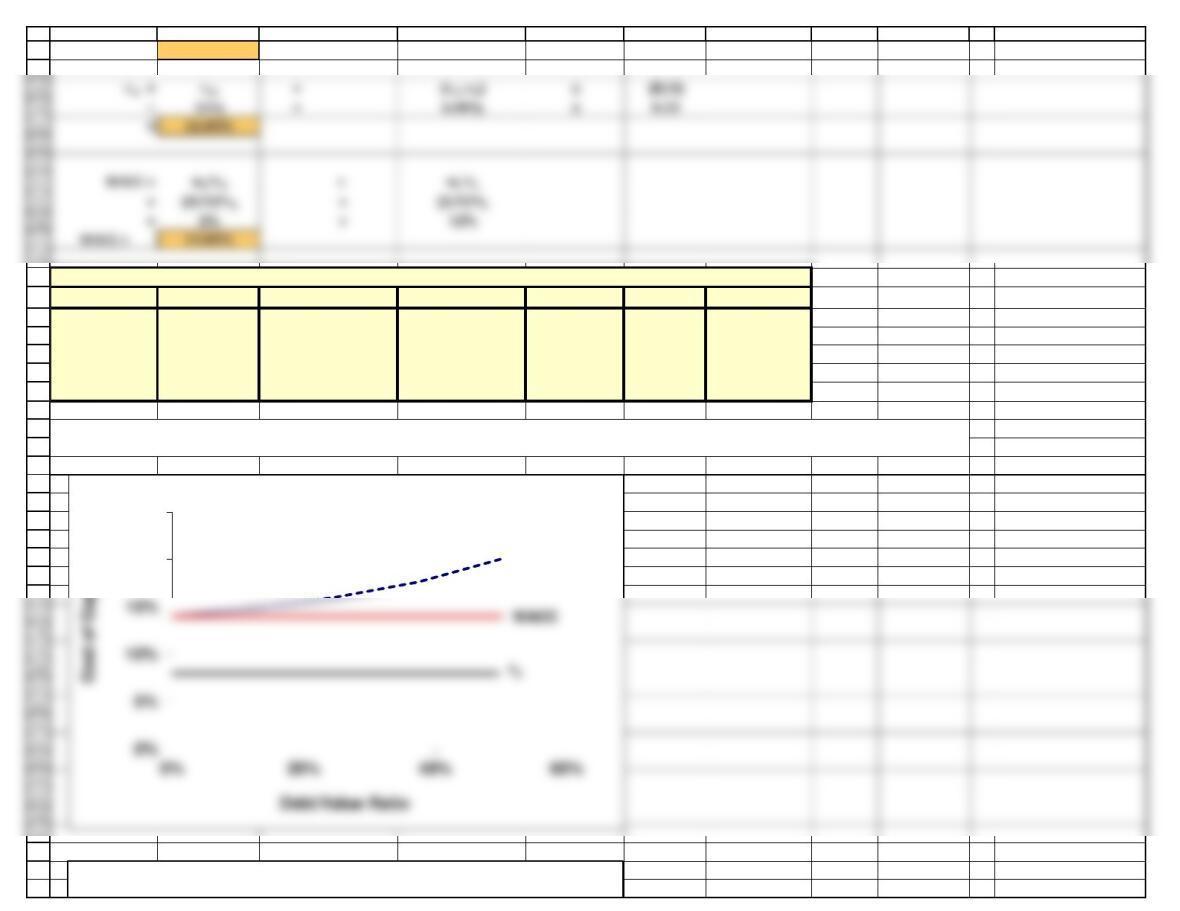

VUSD/VLrdrsWACC

0.0 $4.00 $4.00 0.00% 8.00% 14.00% 14.00%

0.5 $4.00 $3.50 12.50% 8.00% 14.86% 14.00%

1.0 $4.00 $3.00 25.00% 8.00% 16.00% 14.00%

1.5 $4.00 $2.50 37.50% 8.00% 17.60% 14.00%

2.0 $4.00 $2.00 50.00% 8.00% 20.00% 14.00%

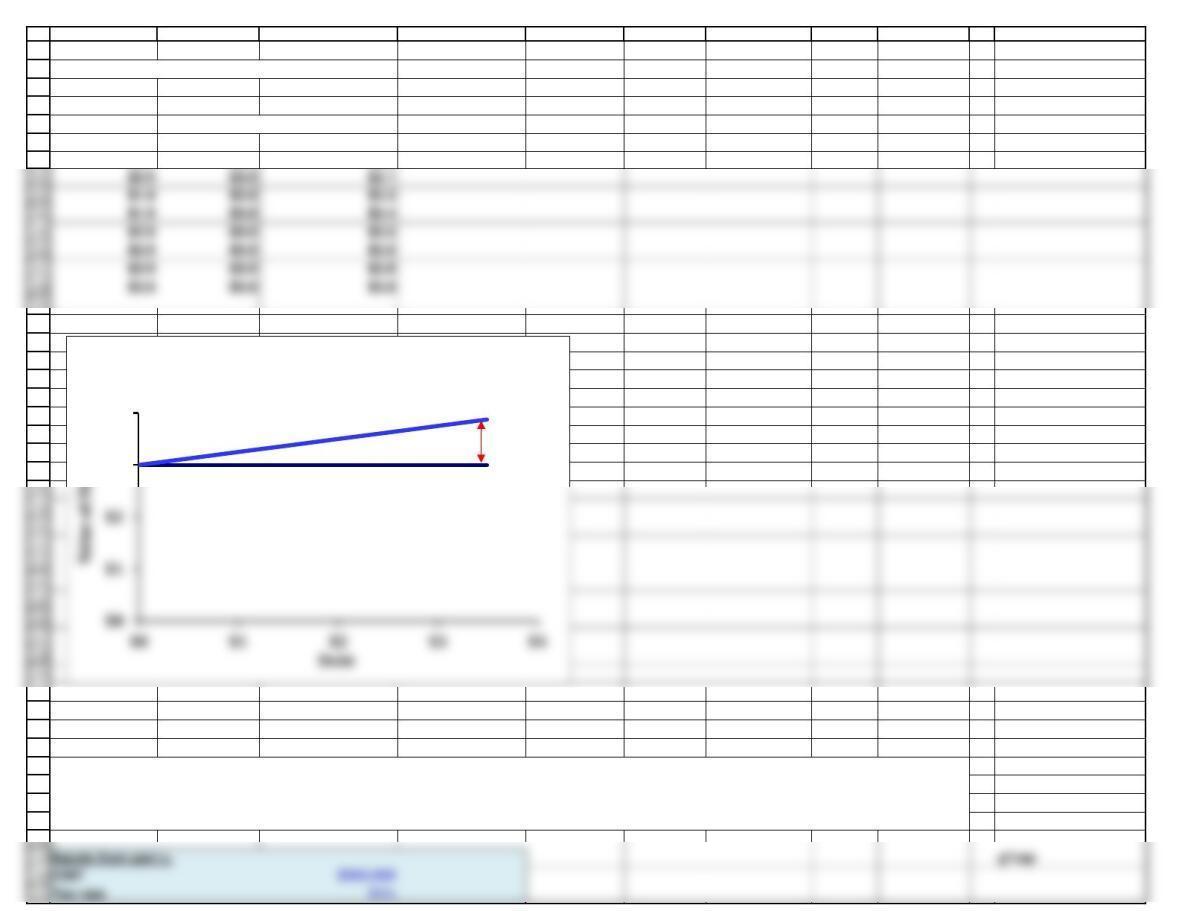

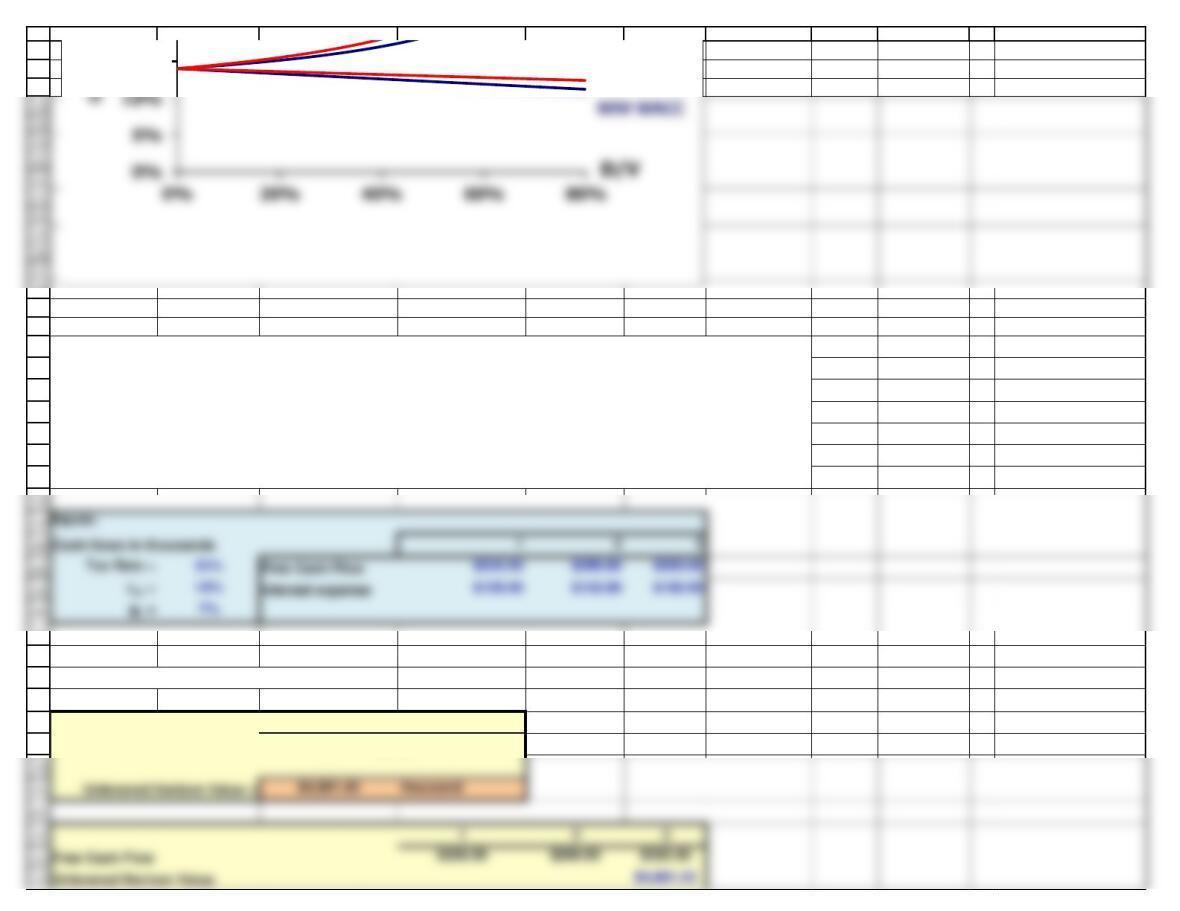

b(2): Graph (a) the relationships between capital costs and leverage as measured by D/V, and (b) the relationship between value and D.

20%

25%

Without Taxes

rs

$5 Without Taxes (Millions of Dollars)

rsU 14% 14% 14% 14%

93

94

95

96

97

98

99

112

113

114

115

116

117

118

126

127

128

129

130

131

A B C D E F G H I J K

Modigliani and Miller with CorporateTaxes

Firm U Firm L 25% Tax Rate 25% Tax Rate

Input Data No Debt Some Debt No Debt Some Debt

EBIT $560,000 $560,000 $560,000 $560,000

Debt $0 $1,000,000 $0 $1,000,000

rd8.0% 8.0%

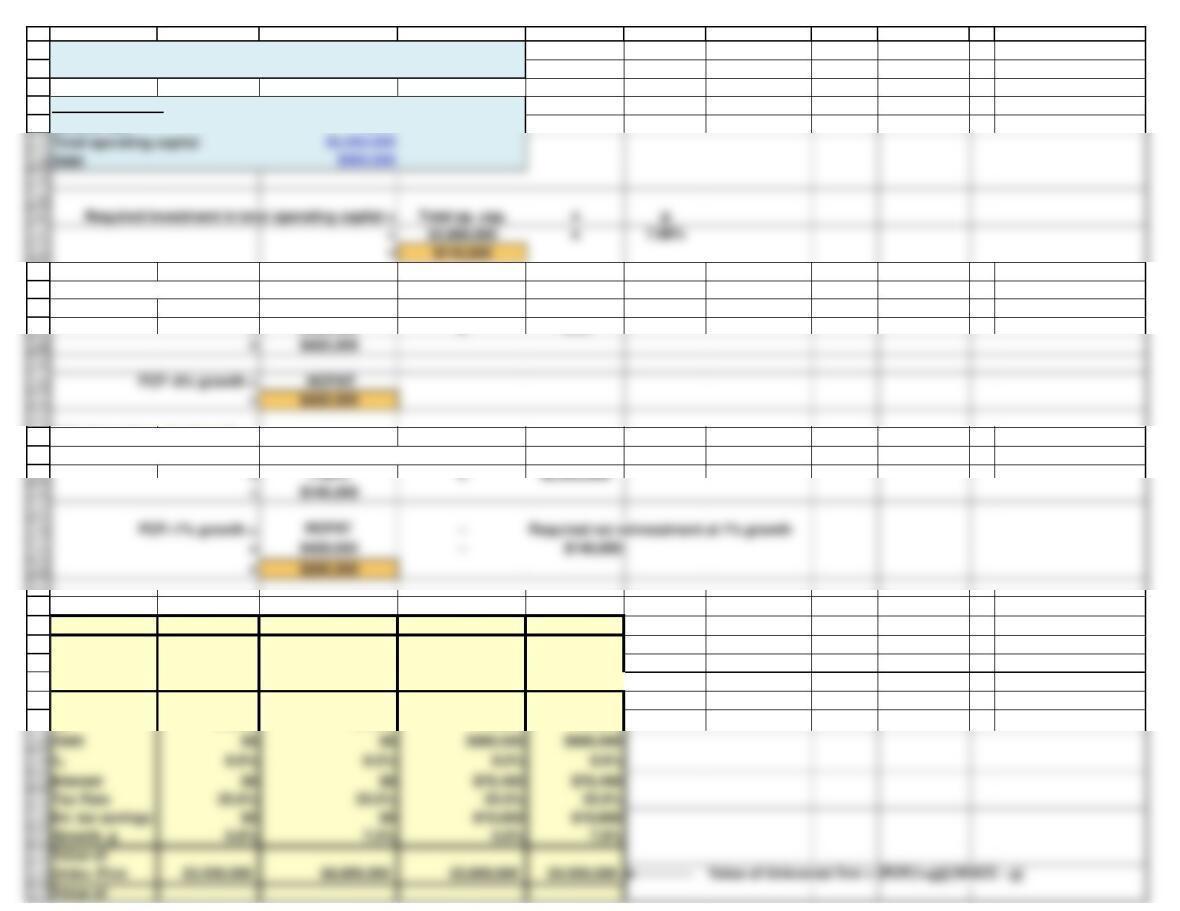

c. Using the data given in Part b, but now assuming that Firms L and U are both subject to a 25 percent corporate tax rate, repeat the

analysis called for in b(1) and b(2) under the MM with-tax model.

$3

$4

$5

Without Taxes (Millions of Dollars)

VU= VL

139

140

141

148

149

150

151

152

153

154

155

156

157

165

166

167

168

169

170

184

A B C D E F G H I J K

V Tax Shield

$0 $0 $0 $250,000

V Total $4,000,000 $4,000,000 $3,000,000 $3,250,000

S (V stock) $4,000,000 $3,000,000 $3,000,000 $2,250,000 V stock = V total – Debt

Effects of Leverage: MM Models

MM with Corporate Taxes (Millions of dollars)

Tc = 25.00%

DV S D/V

rdrd x (1-T) rsWACC

$0.00 $3.000 $3.000 0.00% 8.00% 6.00% 14.00% 14.00%

$0.50 $3.125 $2.625 16.00% 8.00% 6.00% 14.86% 13.44%

$1.00 $3.250 $2.250 30.77% 8.00% 6.00% 16.00% 12.92%

Value of Tax Shield = T x Debt

Value of Firm = Value of Unlevered Firm +T x Debt

50%

60%

With Taxes

rs

Tax rate

185

186

187

188

189

190

191

199

200

201

202

203

204

205

206

207

208

220

221

222

223

224

225

226

227

A B C D E F G H I J K

The Relationship Between Value and Debt

Debt T = 0 T = 25%

$0.0 $3.0 $3.0

Levered value

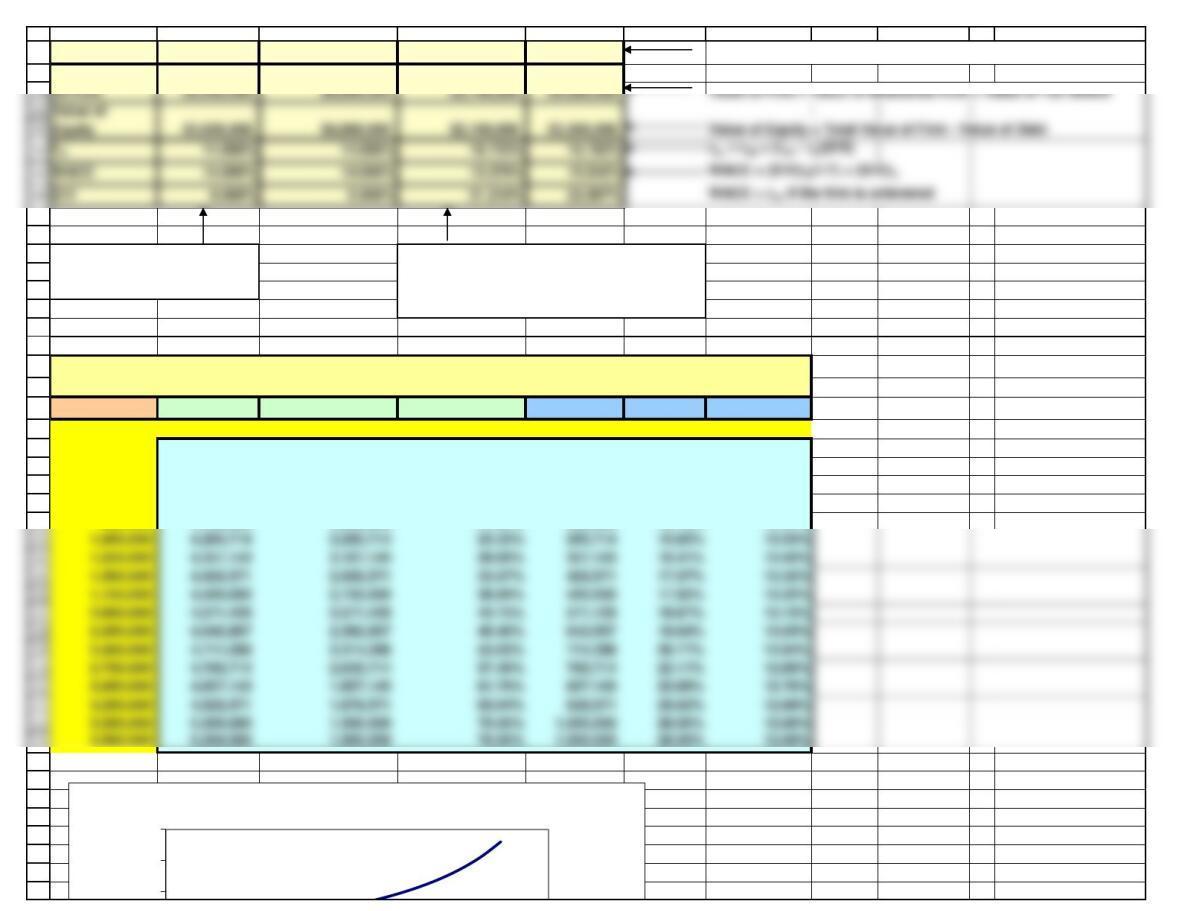

d. Suppose that Firms U and L have the same input values as in Part c except for debt of $980,000. Also, both firms have total net operating

capital of $2,000,000 and both firms are expected to grow at a constant rate of 7%. (Assume that the EBIT in Part c is expected at t = 1.) Use

the compressed adjusted present value (APV) model to estimate the value of U and L. Also estimate the levered cost of equity and the

weighted average cost of capital.

$3

$4

Value of a Levered Firm: The Impact of

Taxes and Debt (Millions of dollars)

VU

VL

TD

$0.5 $3.0 $3.1

$1.0 $3.0 $3.3

rd8.0% 8.0% 8.0% 8.0%

232

233

234

235

236

244

245

246

247

253

254

261

262

263

264

265

266

267

268

A B C D E F G H I J K

Unlevered cost of equity

14% = WACC if D = 0

Cost of debt

8%

Additional Inputs

Growth rate

7.00%

FCF Calculation: No Growth

NOPAT = EBIT x (1-T)

= $560,000 x 75%

FCF Calculation: 7% Growth

Required inv. in op. cap. = g x Total net operating capital

Firm U Firm U Firm L Firm L

25% Tax Rate 25% Tax Rate 25% Tax Rate 25% Tax Rate

zero Debt zero Debt some Debt some Debt

and no growth and 7% growth and no growth and 7% growth

Exp. FCF $420,000 $280,000 $420,000 $280,000

rsU 14.00% 14.00% 14.00% 14.00%

1,000,000 4,285,714 3,285,714 23.33% 285,714 15.83% 13.53%

1,250,000 4,357,143 3,107,143 28.69% 357,143 16.41% 13.43%

1,500,000 4,428,571 2,928,571 33.87% 428,571 17.07% 13.32%

1,750,000 4,500,000 2,750,000 38.89% 500,000 17.82% 13.22%

2,000,000 4,571,429 2,571,429 43.75% 571,429 18.67% 13.13%

2,250,000 4,642,857 2,392,857 48.46% 642,857 19.64% 13.03%

2,500,000 4,714,286 2,214,286 53.03% 714,286 20.77% 12.94%

3,000,000 4,857,143 1,857,143 61.76% 857,143 23.69% 12.76%

3,250,000 4,928,571 1,678,571 65.94% 928,571 25.62% 12.68%

3,500,000 5,000,000 1,500,000 70.00% 1,000,000 28.00% 12.60%

278

279

286

287

288

289

290

291

292

293

294

295

296

297

298

299

300

301

302

315

316

317

318

319

320

321

322

A B C D E F G H I J K

Tax Shield $0 $0 $140,000 $280,000

Value of Tax Shield = [(rd)(T)(D)(1+g)] / ( rU – g)

Total Value

CAPV with growth: rTS = rsU.growth = 7.00%

T = 25.00%

DV S D/V Tax shield

rsL WACC

$4,280,000 $3,300,000 22.897% $280,000 15.782% 13.542%

– 4,000,000 4,000,000 0.00% – 14.00% 14.00%

250,000 4,071,429 3,821,429 6.14% 71,429 14.39% 13.88%

500,000 4,142,857 3,642,857 12.07% 142,857 14.82% 13.76%

750,000 4,214,286 3,464,286 17.80% 214,286 15.30% 13.64%

980,000 4,280,000 3,300,000 22.90% 280,000 15.78% 13.54%

This column will NOT be the same as the

“25% tax rate, some debt” column from part c

because we are discounting the tax shield at

rsU instead of rd.

This column is the same as the

“25% tax rate no debt” column

from part c.

20%

25%

30%

Cost of capital

Cost of Capital with growth

WACC = (D/V)rd(1-T) + (S/V)rs

WACC = rsU if the firm is unlevered

14.50% 13.65% 14.67% 13.80%

14.79% 13.48% 15.06% 13.70%

15.13% 13.30% 15.50% 13.60%

15.50% 13.13% 16.00% 13.50%

323

333

334

335

336

337

338

342

343

344

345

346

347

348

349

350

351

352

353

358

359

360

361

362

367

A B C D E F G H I J K

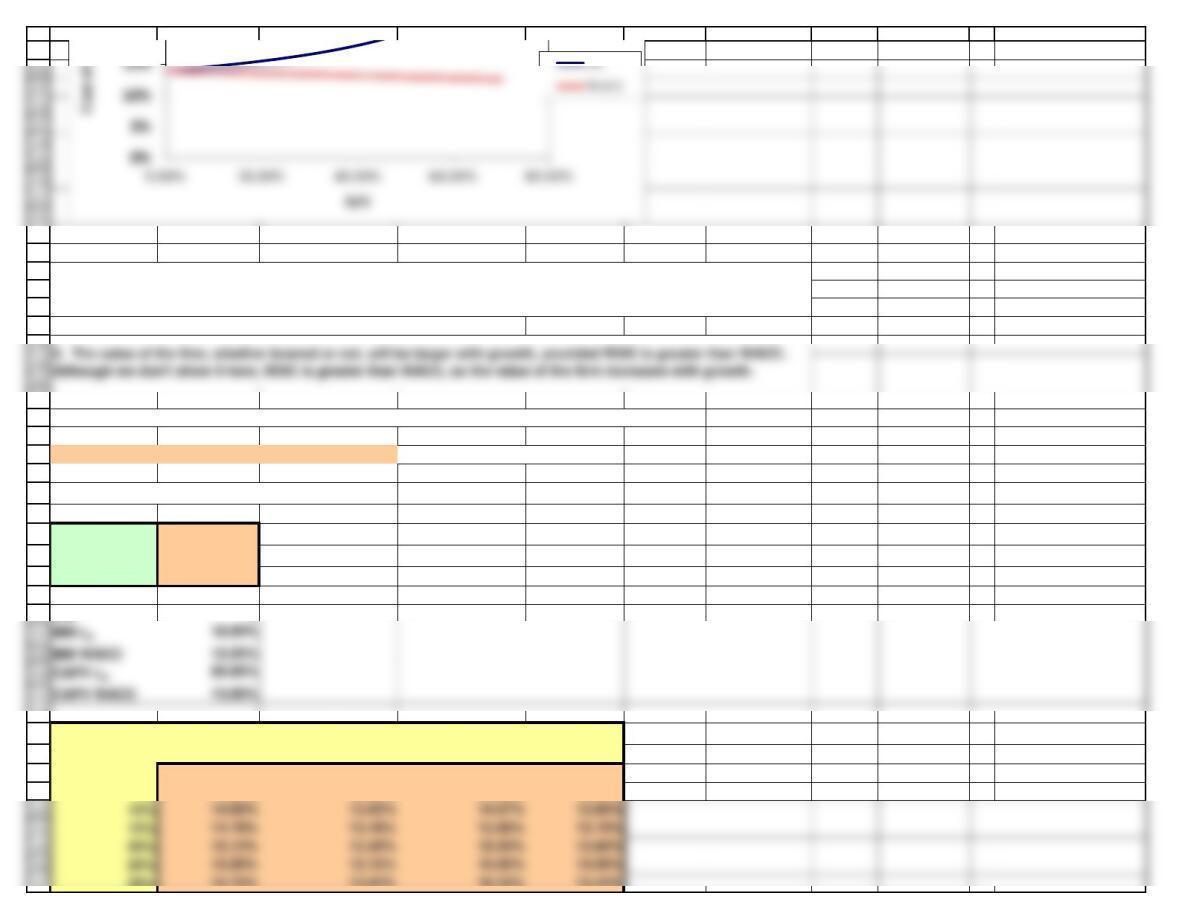

Things to note:

2. The gain from debt is larger with growth than without growth.

The increase in the firm’s value as a result of $1,000,000 in debt over its unlevered value is:

7.00% of the unlevered value

MM versus Compressed APV rsL and WACC

rd8.0%

rsU 14.00%

Tax Rate 25%

D/V

50%

D/S 1

MM rsL MM WACC APV rsL APV WACC

D/V

18.50% 12.25% 20.00% 13.00%

0%

14.00% 14.00% 14.00% 14.00%

5%

14.24% 13.83% 14.32% 13.90%

28%

15.75% 13.02% 16.33% 13.44%

Increase in value =

1. The gain from the tax shield will be lower using the compressed APV model than under MM because the CAPV

model discounts the interest tax shield at the unlevered cost of equity, which is larger than the cost of debt. The

MM model discounts the tax shield at the cost of debt.

20%

25.02% 11.52% 28.69% 12.58%

25.57% 11.48% 29.43% 12.56%

26.17% 11.45% 30.22% 12.54%

26.81% 11.41% 31.08% 12.52%

27.50% 11.38% 32.00% 12.50%

28.25% 11.34% 33.00% 12.48%

29.07% 11.31% 34.09% 12.46%

29.95% 11.27% 35.27% 12.44%

30.93% 11.24% 36.57% 12.42%

368

369

370

371

379

380

381

382

383

384

385

386

387

388

389

390

401

402

403

404

405

406

407

408

A B C D E F G H I J K

31%

16.02% 12.92% 16.70% 13.38%

34%

16.32% 12.81% 17.09% 13.32%

37%

16.64% 12.71% 17.52% 13.26%

40%

17.00% 12.60% 18.00% 13.20%

56%

19.73% 12.04% 21.64% 12.88%

58%

20.21% 11.97% 22.29% 12.84%

60%

20.75% 11.90% 23.00% 12.80%

61%

21.04% 11.87% 23.38% 12.78%

62%

21.34% 11.83% 23.79% 12.76%

63%

21.66% 11.80% 24.22% 12.74%

64%

22.00% 11.76% 24.67% 12.72%

65%

22.36% 11.73% 25.14% 12.70%

66%

22.74% 11.69% 25.65% 12.68%

67%

23.14% 11.66% 26.18% 12.66%

68%

23.56% 11.62% 26.75% 12.64%

69%

24.02% 11.59% 27.35% 12.62%

80%

32.00% 11.20% 38.00% 12.40%

35%

40%

Cost of Capital

Costs of Capital for MM and APV

APV rsL

17.26% 12.53% 18.34% 13.16%

17.54% 12.46% 18.71% 13.12%

17.83% 12.39% 19.11% 13.08%

18.15% 12.32% 19.54% 13.04%

18.50% 12.25% 20.00% 13.00%

18.88% 12.18% 20.50% 12.96%

19.28% 12.11% 21.04% 12.92%

415

416

417

428

429

430

431

432

433

434

435

436

437

444

445

446

447

448

449

A B C D E F G H I J K

Estimate the unlevered value of operations

rsU – g

Unlevered Horizon Value =

e. Suppose the expected free cash flow for Year 1 is $250,000 but it is expected to grow faster than 7% during the

next 3 years: FCF2 = $290,000 and FCF3 = $320,000, after which it will grow at a constant rate of 7%. The expected

interest expense at Year 1 is $128,000, but it is expected to grow over the next couple of years before the capital

structure becomes constant: Interest expense at Year 2 will be $152,000, at Year 3 it will be $192,000 and it will

grow at 7% thereafter. What is the estimated horizon unlevered value of operations (i.e., the value at Year 3

immediately after the FCF at Year 3)? What is the current unlevered value of operations? What is the horizon value

of the tax shield at Year 3? What is the current value of the tax shield? What is the current total value? The tax rate

and unlevered cost of equity remain at 25% and 14%, respectively.

(Free Cash Flow)(1+g)

APV WACC

15%

20%

456

459

460

461

462

463

468

469

470

476

477

478

479

A B C D E F G H I J K

Total

$250.00 $290.00 $5,211.43

Estimate the value of the tax shield

1 2 3

Interest tax shield

$32.00 $38.00 $48.00

Estimate the total value of operations

Vops = Tax shield value + Unlevered value = $4,544.95 thousand

( Tax Shield)(1+g)

Tax Shield Horizon Value =

rsU – g