1

2

3

4

5

6

7

8

9

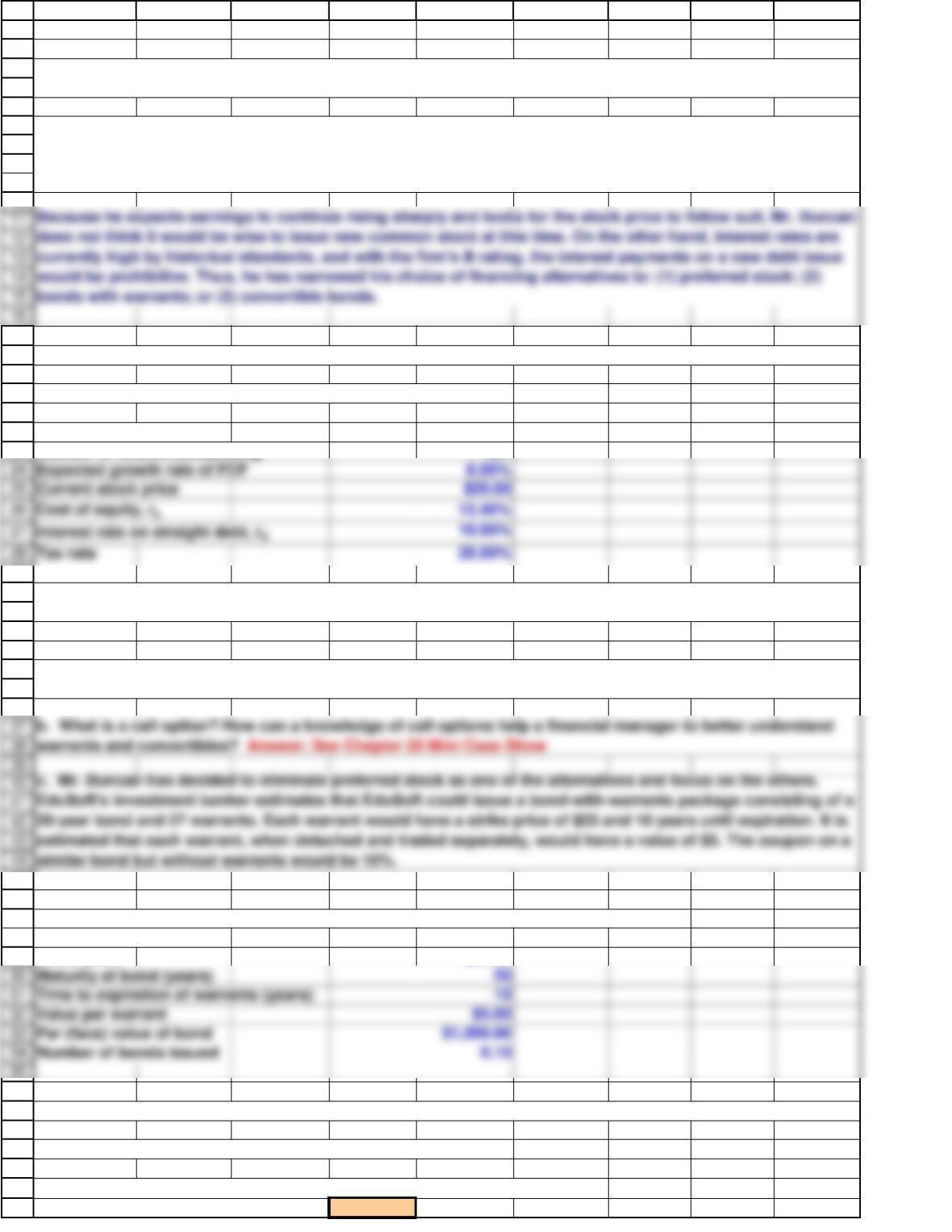

Expected growth rate of FCF 8.00%

Current stock price $20.00

Tax rate 25.00%

b. What is a call option? How can a knowledge of call options help a financial manager to better understand

warrants and convertibles? Answer: See Chapter 20 Mini Case Show

estimated that each warrant, when detached and traded separately, would have a value of $5. The coupon on a

similar bond but without warrants would be 10%.

17

18

19

20

21

22

23

29

30

31

32

33

34

35

36

Maturity of bond (years) 20

Time to expiration of warrants (years) 10

Value per warrant $5.00

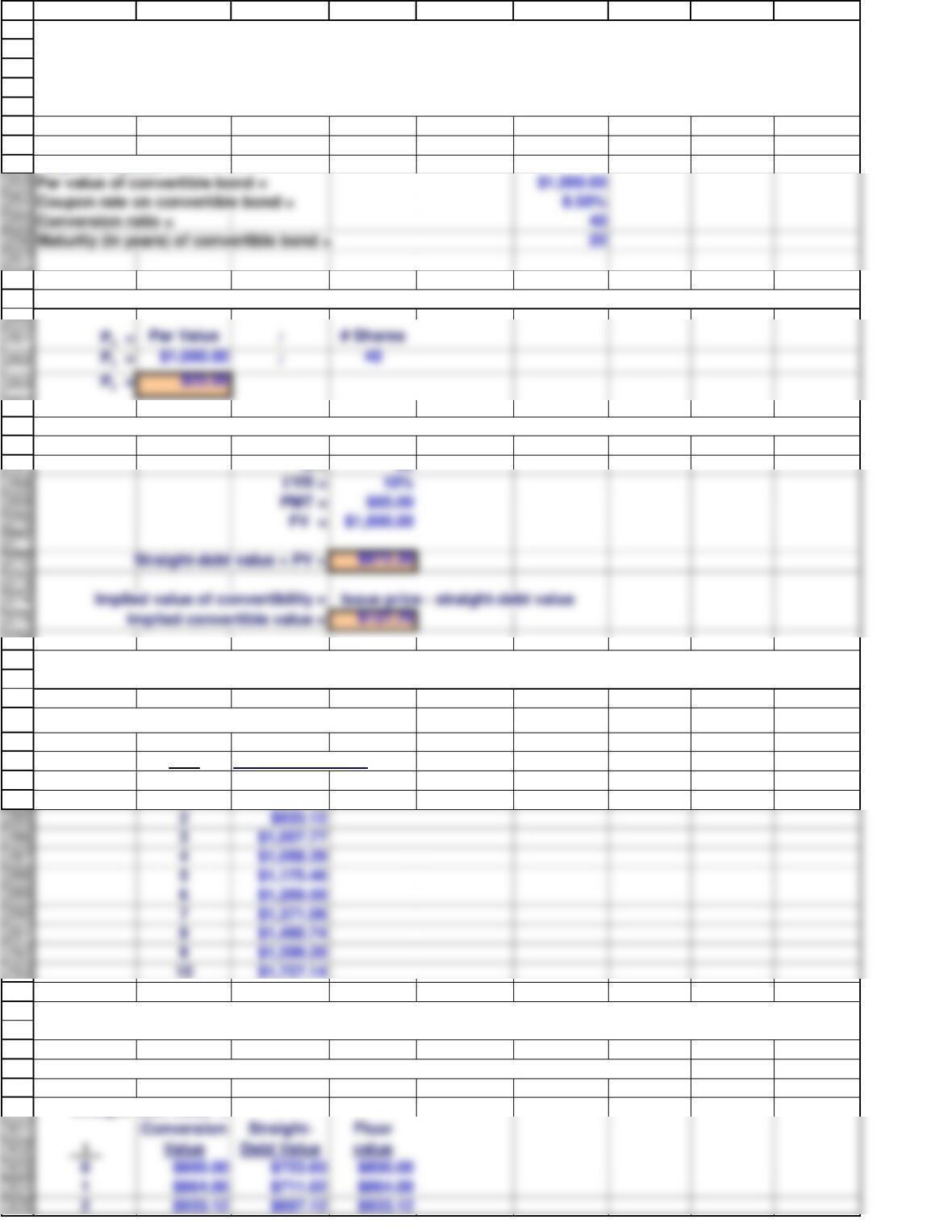

Par (face) value of bond $1,000.00

Number of bonds issued 0.10

45

46

47

48

49

56

57

58

59

60

61

62

A B C D E F G H I

11/23/2018

Inputs (Note: All values are in millions, except per share data.)

Value of operations $500.00

Number of shares outstanding 20

Data for Bonds with Warrants (Note: All values are in millions, except per share data.)

Warrants per bond 27

Strike price $25.00

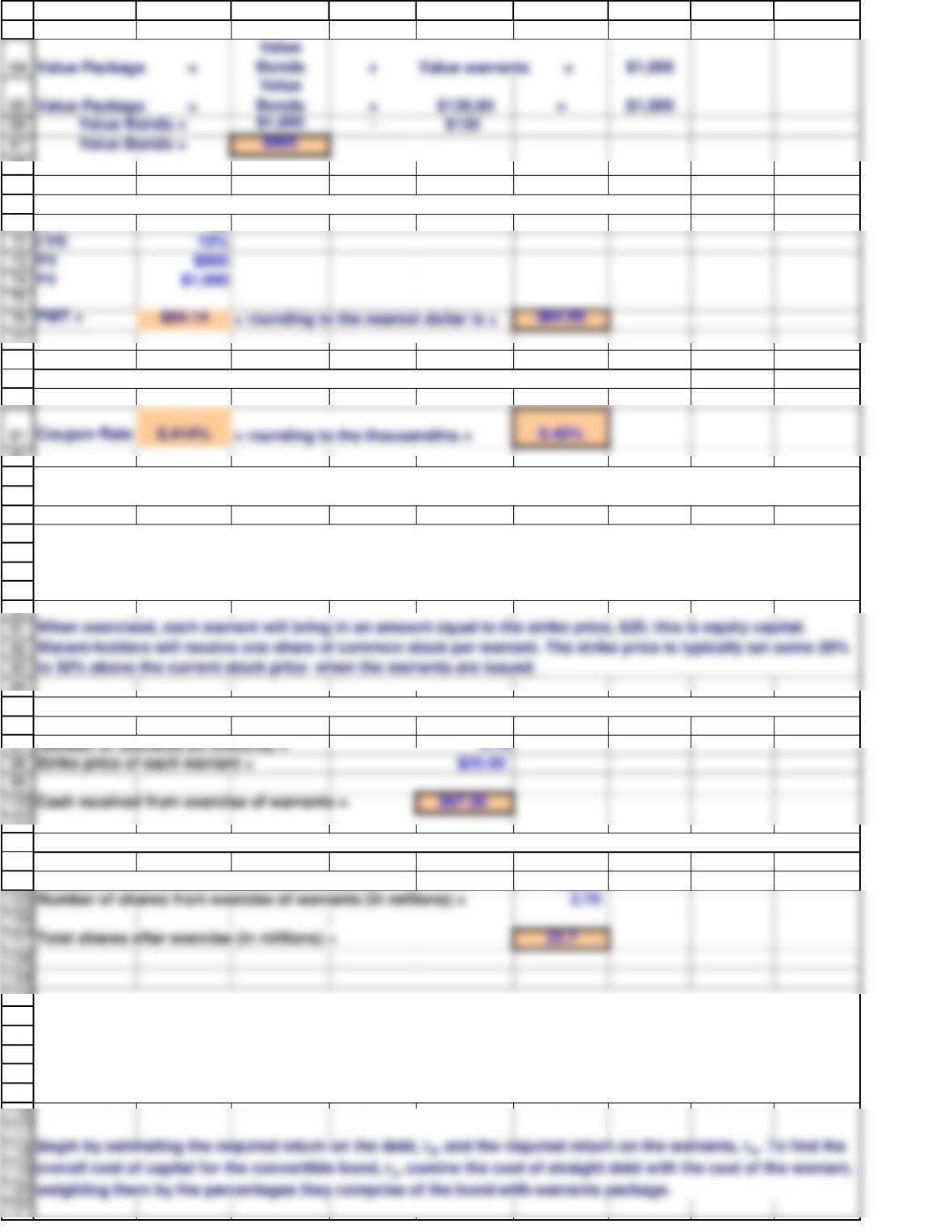

First, find the value of the embedded straight bond.

Value of warrants per bond = (Warrant per bond) x (Value per warrant)

Value of warrants per bond = $135.00

Chapter 20. Mini Case for Hybrid Financing: Preferred Stock, Warrants, and Convertibles

(1) What coupon rate should be set on the bond with warrants if the total package is to sell for $1,000?

Paul Duncan, financial manager of EduSoft Inc., is facing a dilemma. The firm was founded 5 years ago to

provide educational software for the rapidly expanding primary and secondary school markets. Although

EduSoft has done well, the firm’s founder believes an industry shakeout is imminent. To survive, EduSoft must

grab market share now, and this will require a large infusion of new capital.

a. How does preferred stock differ from both common equity and debt? Is preferred stock more risky than

common stock? What is floating rate preferred stock? Answer: See Chapter 20 Mini Case Show

As Duncan’s assistant, you have been asked to help in the decision process by answering the following

questions:

The following data apply to all three alternatives:

bonds with warrants; or (3) convertible bonds.

63

75

76

68

69

70

71

77

78

79

80

82

83

84

85

86

to 30% above the current stock price when the warrants are issued.

99

Strike price of each warrant = $25.00

87

88

89

94

95

96

Number of shares from exercise of warrants (in millions) = 2.70

101

102

103

104

110

weighting them by the percentages they comprise of the bond-with-warrants package.

111

112

113

114

115

A B C D E F G H I

N20

Number of shares before exercise (in millions) = 20.00

(3) Will the warrants bring in additional capital when exercised? If EduSoft issues 100,000 bond-with-warrant

packages, how much cash will EduSoft receive when the warrants are exercised? How many shares of stock

will be outstanding after the warrants are exercised? (EduSoft currently has 20 million shares outstanding).

(4) Because the presence of warrants causes a lower coupon rate on the accompanying debt issue, shouldn’t

all debt be issued with warrants? To answer this, estimate the expected stock price in 10 years when the

warrants are expected to be exercised, then estimate the return to the holders of the bond-with– warrants

packages. Use the corporate valuation model to estimate the expected stock price in 10 years. Assume that

EduSoft’s current value of operations is $500 million and it is expected to grow at 8% per year.

How much cash will the firm receive when the warrants are exercised?

How many shares of stock will there be after the warrants are exercised?

(2) When would you expect the warrants to be exercised? What is a stepped-up-exercise price? Answer: See

Chapter 20 Mini Case Show

Use the required payment to determine the required coupon rate.

Find the payment such that the bond with warrant is issued at par.

67

122

123

124

Coupon rate 8.40%

PMT $84

Number of bonds (in millions) 0.10

125

126

127

128

129

130

131

132

140

141

142

143

144

145

146

147

148

149

150

155

156

157

158

159

Intrinsic value of equity $1,056.79

÷ Number of shares $22.70

Intrinsic price per share $46.55

170

171

172

179

180

181

182

A B C D E F G H I

The cost of debt debt is the cost of straight debt = rd = 10%

Current valuation analysis

Required inputs:

Total intrinsic value of firm $500

− Debt $100

Intrinsic value of equity $400

÷ Number of shares 20

Intrinsic price per share $20.00

Valuation analysis in 10 years when warrants expire

Required inputs:

Number of years until expiration = 10

N10

I10%

Intrinsic stock price in at expiration

Value of operations $1,079.46

Estimating the expected return to the warrant-holders

How much will the bonds be worth in 10 years? (There will be 10 years remaining to maturity.)

To find the cost of warrants, we will find the expected profit of the warrant holders and the expected return. If

the warrants are very likely to be in the money at expiration, then we can approximate the expected profit by

first estimating the expected stock price at expiration. We begin by performing a current valuation analysis and

then we repeat the analysis assuming 10 years have passed and the value of operations has grown at it

expected growth rate.

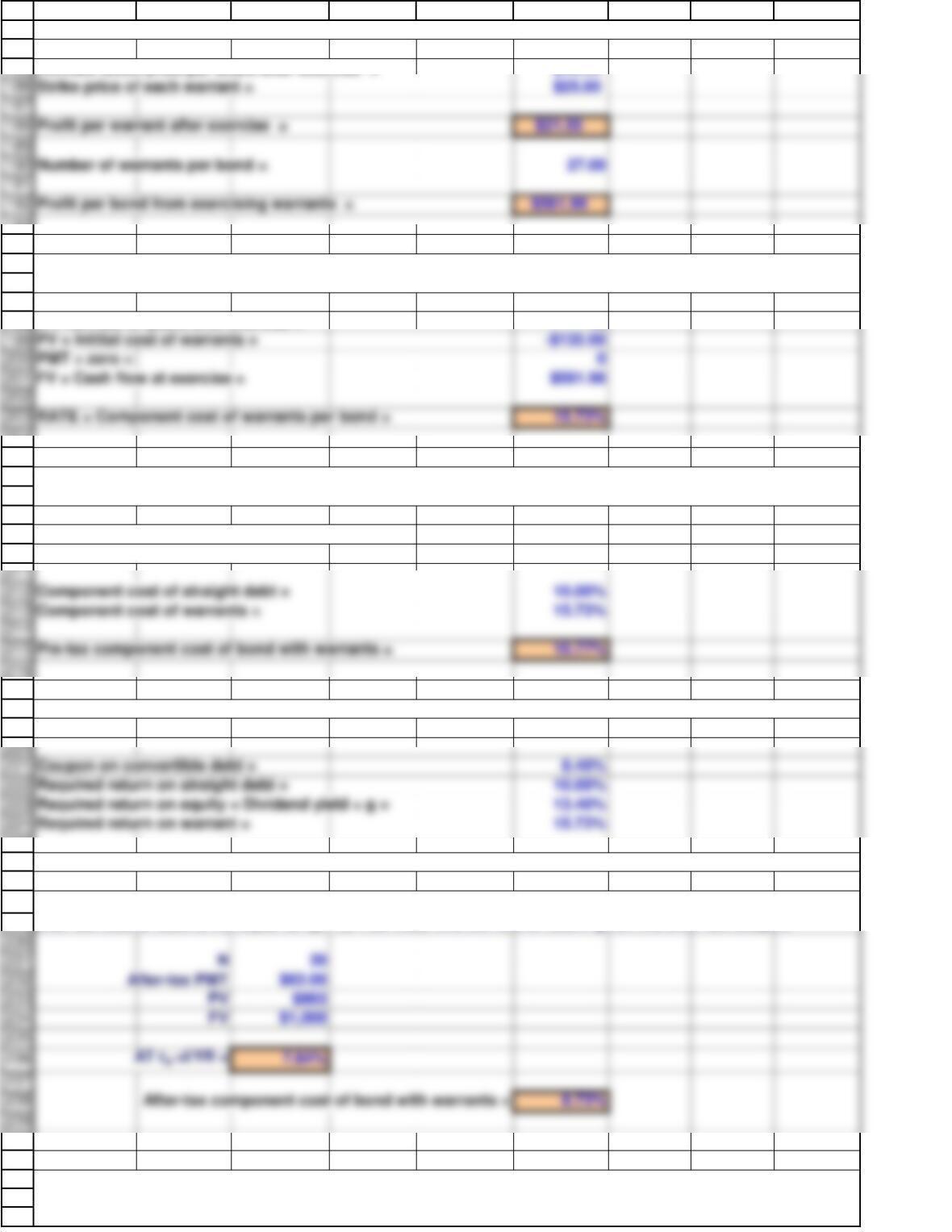

The per warrant profit to the warrant-holder is equal to the stock price minus the strike price. The total profit

per bond is equal to the total number warrants per bond multiplied by the profit per warrant.

Initial value of debt = Number of bonds x Iissue price $100

Value of operations $500

183

184

185

PV = Intitial cost of warrants = -$135.00

PMT = zero = 0

FV = Cash flow at exercise = $581.98

193

194

195

196

197

198

Component cost of straight debt = 10.00%

Component cost of warrants = 15.73%

204

205

206

207

208

209

210

Coupon on convertible debt = 8.40%

Required return on straight debt = 10.00%

Required return on equity = Dividend yield + g = 13.40%

Required return on warrant = 15.73%

217

218

219

225

226

227

228

229

240

241

242

243

244

A B C D E F G H I

Intrinsic stock price per share after exercise = $46.55

N = Number of years until exercise = 10

% straight bond in bond with warrants = 86.50%

% warrants in bond with warrants = 13.50%

(5) How would you expect the cost of the bond with warrants to compare with the cost of straight debt? With

(6) If the corporate tax rate is 25%, what is the after-tax cost of the bond with warrants?

Because the bond portion of the package was issued at a discount (its value was only $865, not $1,000), its

after-tax cost of debt is not equal to rd(1-T). You must find the rate of return given the after-tax coupon.

The per warrant profit to the warrant-holder is equal to the stock price minus the strike price. The total profit

per bond is equal to the total number warrants per bond multiplied by the profit per warrant.

The component cost per warrant is the IRR of an investment in warrants at time 0 and a cash flow from

exercising.

The pre-tax component cost of the bond with warrants is the weighted average of the pre-tax component costs

of the straight bond and the warrants.

d. As an alternative to the bond with warrants, Mr. Duncan is considering convertible bonds. The firm’s

investment bankers estimate that EduSoft could sell a 20-year, 8.5 percent annual coupon, callable convertible

bond for its $1,000 par value, whereas a straight-debt issue would require a 12 percent coupon. The

convertibles would be call protected for 5 years, the call price would be $1,100, and the company would

probably call the bonds as soon as possible after their conversion value exceeds $1,200. Note, though, that

the call must occur on an issue date anniversary. EduSoft’s current stock price is $20, its last dividend was

$1.00, and the dividend is expected to grow at a constant 8 percent rate. The convertible could be converted

into 40 shares of EduSoft stock at the owner’s option.

Strike price of each warrant = $25.00

Number of warrants per bond = 27.00

245

246

247

248

249

250

251

252

258

259

264

265

266

2$933.12

276

277

278

279

280

281

282

283

284

294

295

296

297

298

299

300

A B C D E F G H I

Required inputs:

Inputs:

N = 20

Conversion value = CVt = CR(P0)(1 + g)t.

t Conversion value

0$800.00

1$864.00

The floor value is the higher of the straight debt value and the conversion value.

Straight-debt value =

(2) What is the convertible’s straight-debt value? What is the implied value of the convertibility feature?

(1) What conversion price is built into the bond?

(3) What is the formula for the bond’s expected conversion value in any year? What is its conversion value at

Year 0? At Year 10?

(4) What is meant by the “floor value” of a convertible? What is the convertible’s expected floor value at Year

0? At Year 10?

d. As an alternative to the bond with warrants, Mr. Duncan is considering convertible bonds. The firm’s

investment bankers estimate that EduSoft could sell a 20-year, 8.5 percent annual coupon, callable convertible

bond for its $1,000 par value, whereas a straight-debt issue would require a 12 percent coupon. The

convertibles would be call protected for 5 years, the call price would be $1,100, and the company would

probably call the bonds as soon as possible after their conversion value exceeds $1,200. Note, though, that

the call must occur on an issue date anniversary. EduSoft’s current stock price is $20, its last dividend was

$1.00, and the dividend is expected to grow at a constant 8 percent rate. The convertible could be converted

into 40 shares of EduSoft stock at the owner’s option.

314

315

316

317

318

319

320

321

322

323

324

325

332

333

334

335

336

337

338

339

340

341

342

343

344

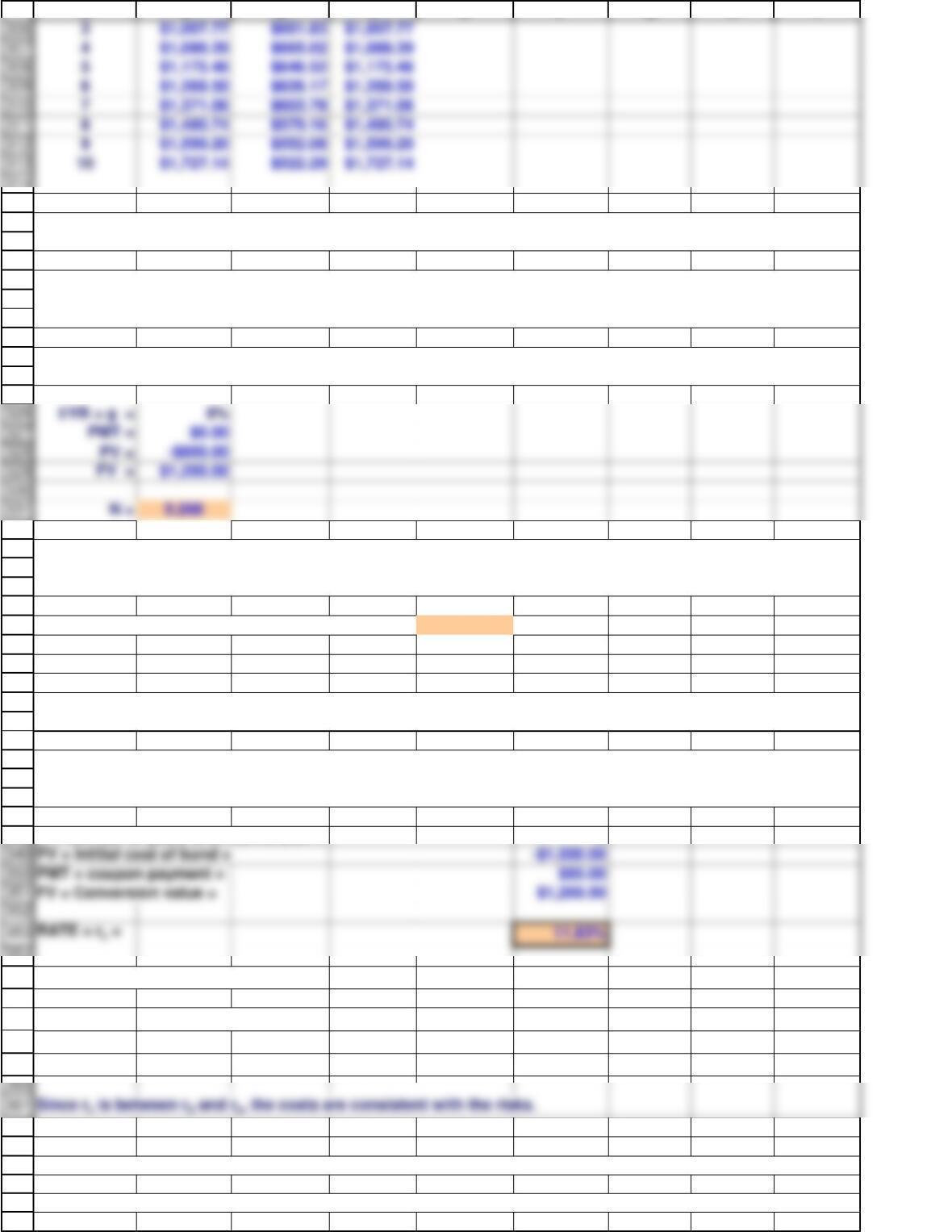

PV = Intitial cost of bond = -$1,000.00

PMT = coupon payment = $85.00

FV = Conversion value = $1,269.50

345

346

347

348

Since rc is between rd and rs, the costs are consistent with the risks.

354

355

356

357

358

359

362

363

364

365

366

367

A B C D E F G H I

Bond will be called (and converted) in year: 6

N = Number of years until conversion = 6

For consistency, need rd < rc < rs.

10.00%

rc = 11.83%

rs = 13.40%

Recall that the bond can be called only on an anniversary date, so we must round the number of years that we

just found up to the next integer. Also, we must verify that the year is at least as great as the number of years

the bond is protected from calls.

The bondholder will receive the coupon each year until conversion (including the year of the conversion). At

conversion, the bondholder will also receive the conversion value. We can find the return using the RATE

function.

rd =

(7) What is the after-tax cost of the convertible bond?

Use the after-tax coupon payment, then find the rate of return.

(5) Assume that EduSoft intends to force conversion by calling the bond as soon as possible after its

conversion value exceeds 20 percent above its par value, or 1.2($1,000) = $1,200. When is the issue expected

to be called? (Hint: Recall that the call must be made on an anniversary date of the issue.)

A convertible will generally sell above its floor value prior to maturity because convertibility constitutes a call

option that has value.

Notice that the conversion value grows at the same rate as the stock. So the first step is to find the number of

years until the initial conversion value grows to the value at which it will be called.

(6) What is the expected return on the convertible to EduSoft? Does this cost appear to be consistent with the

convertible bond’s risk?

368

369

377

378

379

380

381

382

A B C D E F G H I

Pre-tax coupon payment = $85.00

After-tax coupon payment = $63.75

e. Mr. Duncan believes that the costs of both the bond with warrants and the convertible bond are close

enough to one another to call them even, and also consistent with the risks involved. Thus, he will make his

decision based on other factors. What are some of the factors which he should consider? Answer: See

Chapter 20 Mini Case Show