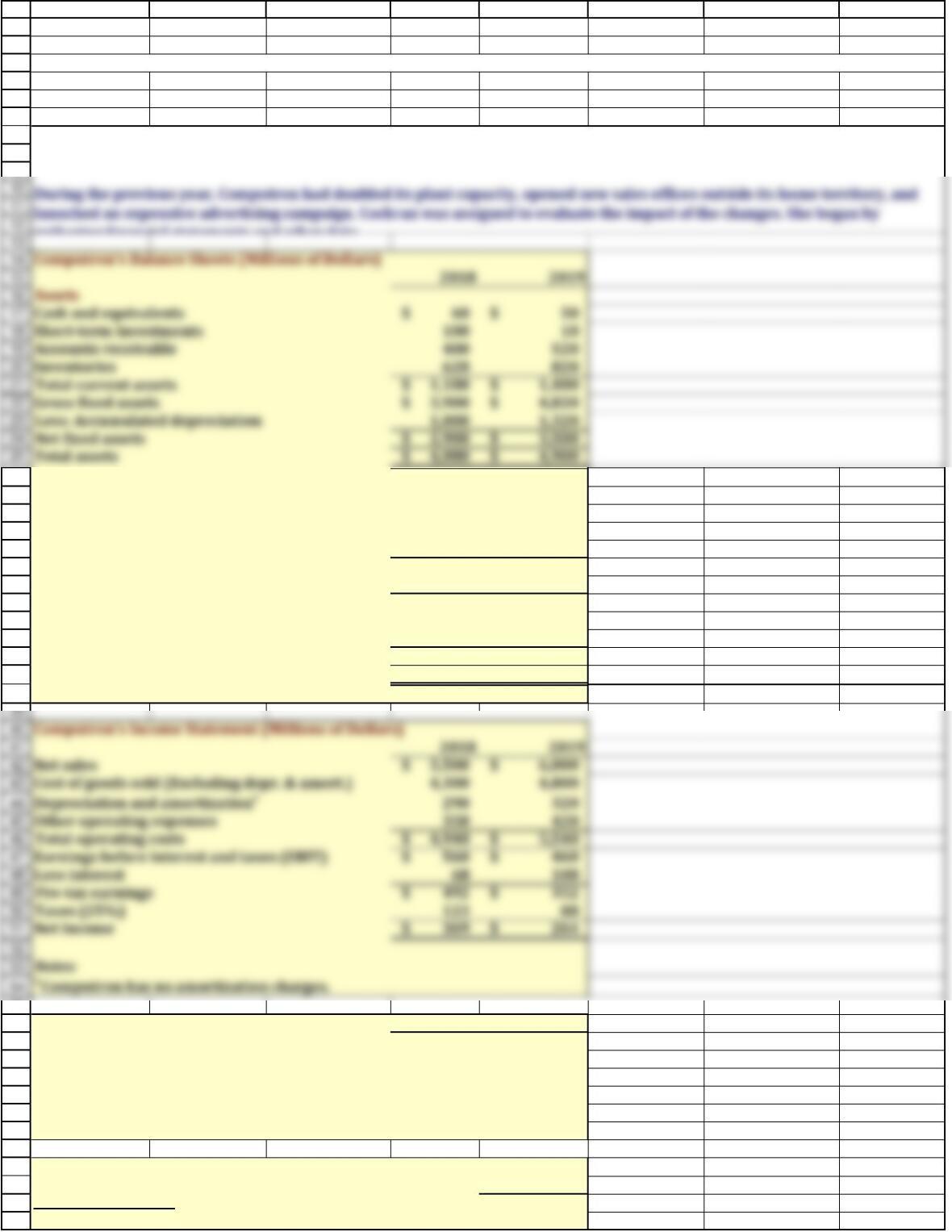

Computron’s Income Statement (Millions of Dollars)

Net sales 5,500$ 6,000$

Cost of goods sold (Excluding depr. & amort.) 4,300 4,800

Other operating expenses 350 420

Total operating costs 4,940$ 5,540$

Earnings before interest and taxes (EBIT) 560$ 460$

Less interest 68 108

Pre-tax earnings 492$ 352$

Taxes (25%) 123 88

Net Income 369$ 264$

1

2

3

4

5

6

7

8

9

26

27

28

29

30

31

32

33

34

35

36

37

38

55

56

57

58

59

60

61

62

63

64

65

66

67

A B C D E F G H

11/20/2018

Situation

Liabilities and equity

Accounts payable 300$ 400$

Notes payable 50 250

Accruals 200 240

Total current liabilities 550$ 890$

Long-term bonds 800 1,100

Total liabilities 1,350$ 1,990$

Common stock 1,000 1,000

Retained earnings 1,730 1,910

Total equity 2,730$ 2,910$

Total liabilities and equity 4,080$ 4,900$

Other Data 2018 2019

Stock price $50.00 $30.00

Shares outstanding (millions) 100 100

Common dividends (millions) $90 $84

Tax rate 25% 25%

Weighted average cost of capital (WACC) 10.00% 10.00%

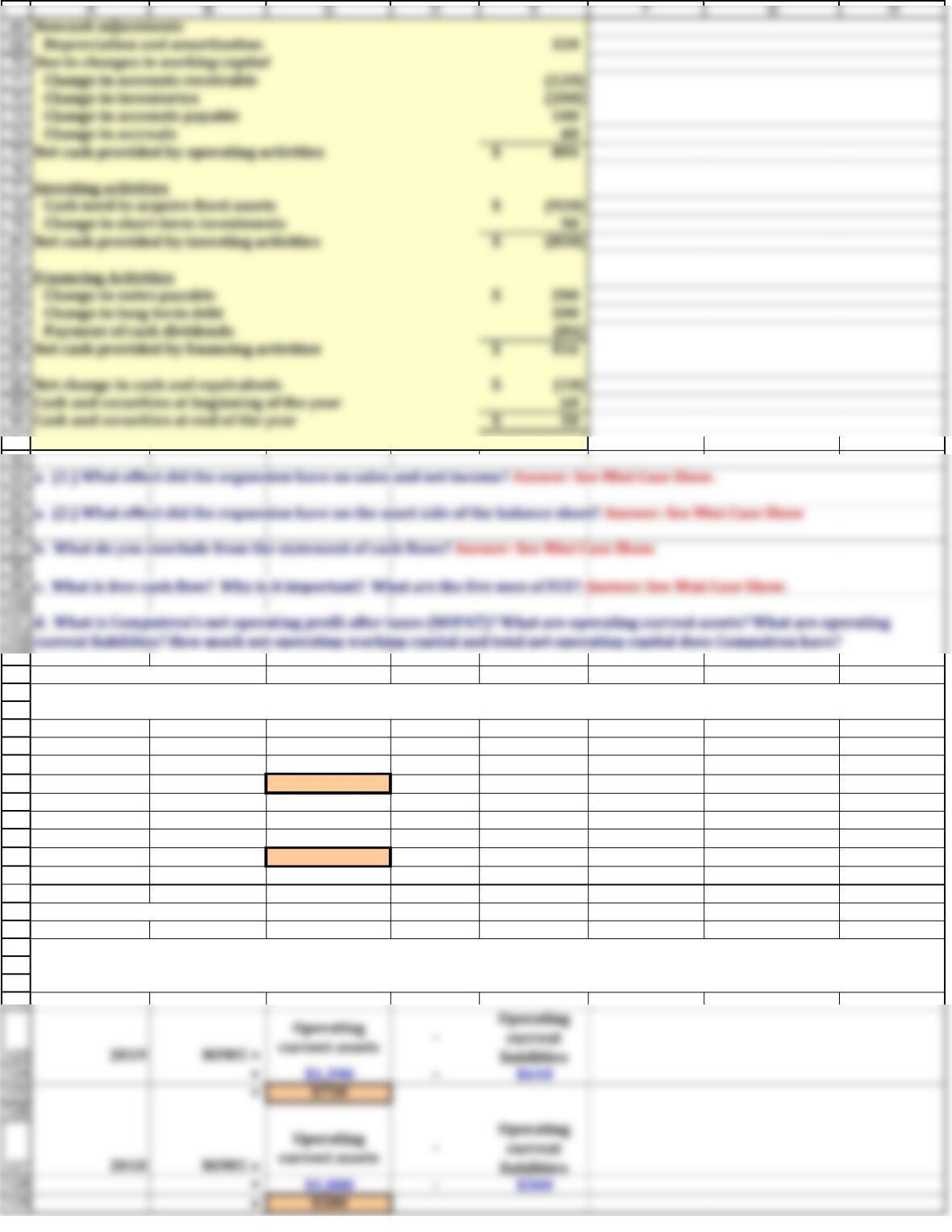

Computron’s Statement of Cash Flows (Millions of Dollars)

2019

Operating Activities

Net Income before preferred dividends 264$

Chapter 2 Mini Case

Jenny Cochran, a graduate of The University of Tennessee with 4 years of experience as an equities analyst, was recently brought

in as assistant to the chairman of the board of Computron Industries, a manufacturer of computer components.

Computron’s Balance Sheets (Millions of Dollars)

Assets

Cash and equivalents 60$ 50$

Short-term investments 100 10

Accounts receivable 400 520

Gross fixed assets 3,900$ 4,820$

Less: Accumulated depreciation 1,000 1,320

Net fixed assets 2,900$ 3,500$

Total assets 4,080$ 4,900$

= $1,390 −$640

= $750

= $1,080 −$500

= $580

91

103

104

105

106

107

108

109

110

111

112

113

114

115

116

117

118

119

120

121

Net Operating Profit After Taxes

2019 NOPAT = EBIT x ( 1 – T )

= $460 x75%

= $345

2018 NOPAT = EBIT x ( 1 – T )

= $560 x75%

= $420

Net Operating Working Capital

NOPAT is the amount of profit Computron would generate if it had no debt and held no financial assets.

Those current assets used in operations are called operating current assets, and the current liabilities that result from

operations are called operating current liabilities. Net operating working capital is equal to operating current assets minus

operating current liabilities.

Depreciation and amortization 320

Change in accounts receivable (120)

Change in inventories (200)

Change in accounts payable 100

Change in accruals 40

Net cash provided by operating activities 404$

Investing activities

Cash used to acquire fixed assets (920)$

Change in short-term investments 90

Net cash provided by investing activities (830)$

Financing Activities

Change in notes payable 200$

Change in long-term debt 300

Payment of cash dividends (84)

Net cash provided by financing activities 416$

Cash and securities at beginning of the year 60

= $345.0 $4,250

= 8.1%

2018 ROIC = NOPAT ÷ Operating Capital

= $420.0 $3,480

= 12.1%

Operating Profitability

= $345.0 $6,000

= 5.8%

= $420.0 $6,000

= 7.0%

Capital Utilization

= $4,250.0 $6,000

= 70.8%

The operating profitability (OP) ratio shows how many dollars of operating profit are generated by each dollar of sales.

The capital utilization (CR) ratio shows how many dollars of operating assets are needed to generated a dollar of sales.

130

131

132

133

134

135

136

137

138

139

140

141

142

143

144

145

146

160

161

162

163

164

165

166

167

168

A B C D E F G H

Total Net Operating Capital (TNOC)

TNOC = NOWC + net operating long-term assets

2019 TNOC = NOWC + Fixed assets

= $750 +$3,500

= $4,250

2018 TNOC = NOWC + Fixed assets

= $580 +$2,900

= $3,480

e. What is Computron’s free cash flow (FCF)? What are Computron’s “net uses” of its FCF?

Free Cash Flow

Return on Invested Capital

2019 ROIC = NOPAT ÷ Operating Capital

f. Calculate Computron’s return on invested capital (ROIC). Computron has a 10% cost of capital (WACC). What caused the

decline in the ROIC? Was it due to operating profitability or capital utilization? Do you think Computron’s growth added value?

The Return on Invested Capital tells us the amount of NOPAT per dollar of operating capital.

Computron’s Free Cash Flow calculation is the cash flow actually availabe for distribution to investors after the company has

= $345.0 −$770

= -$425

Uses of FCF 2019

After-tax interest payment = $81

Reduction (increase) in debt = -$500

Payment of dividends = $84

Repurchase (Issue) stock = $0

Purchase (Sale) of short-term investments = -$90

Total uses of FCF = -$425

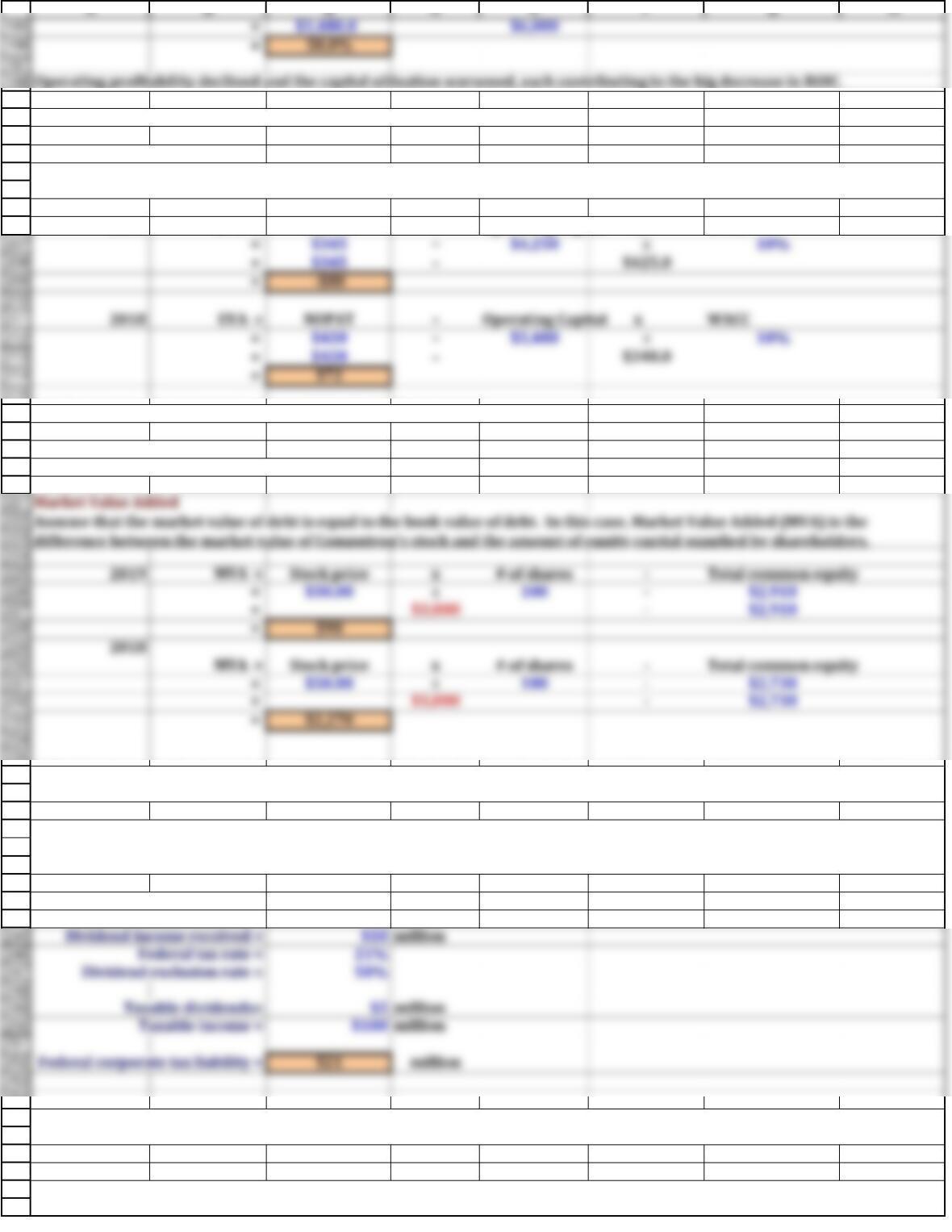

Market Value Added

Taxable dividends= $5 million

199

200

201

202

203

204

205

206

215

216

217

218

219

220

235

236

237

238

239

240

241

242

243

244

254

255

256

257

258

259

260

g. What is Computron’s EVA? The cost of capital was 10% in both years.

Economic Value Added

2019 EVA = NOPAT −Operating Capital x WACC

h. What happened to Computron’s market value added (MVA)?

Year-end common stock price $50.00 $30.00

Year-end shares outstanding (in millions) 100 100

Operating income = $87 million

Interest income received = $8 million

k. The Tax Cut and Jobs Act was signed into law in 2017. Briefly describe its key provisions related to personal taxation. Answer:

See Mini Case Show.

j. Assume that a corporation has $87 million of taxable income from operations. It also received interest income of $8 million

and dividend income of $10 million. The federal tax rate is 21% and the dividend exclusion rate is 50%. What is the company’s

federal tax liability?

l. Assume that you are in the 25% marginal tax bracket and that you have $20,000 to invest. You have narrowed your

investment choices down to municipal bonds yielding 7% or equally risky corporate bonds with a yield of 10%. Which one

should you choose and why? At what marginal tax rate would you be indifferent?

i. The Tax Cut and Jobs Act was signed into law in 2017. Briefly describe its key provisions related to corporate tax taxation.

Answer: See Mini Case Show.

Economic Value Added represents Computron’s residual income that remains after the cost of all capital, including equity

capital, has been deducted.

Operating profitability declined and the capital utlization worsened, each contributing to the big decrease in ROIC.

Solve for T

261

262

263

264

265

266

270

271

272

273

280

281

282

283

284

285

A B C D E F G H

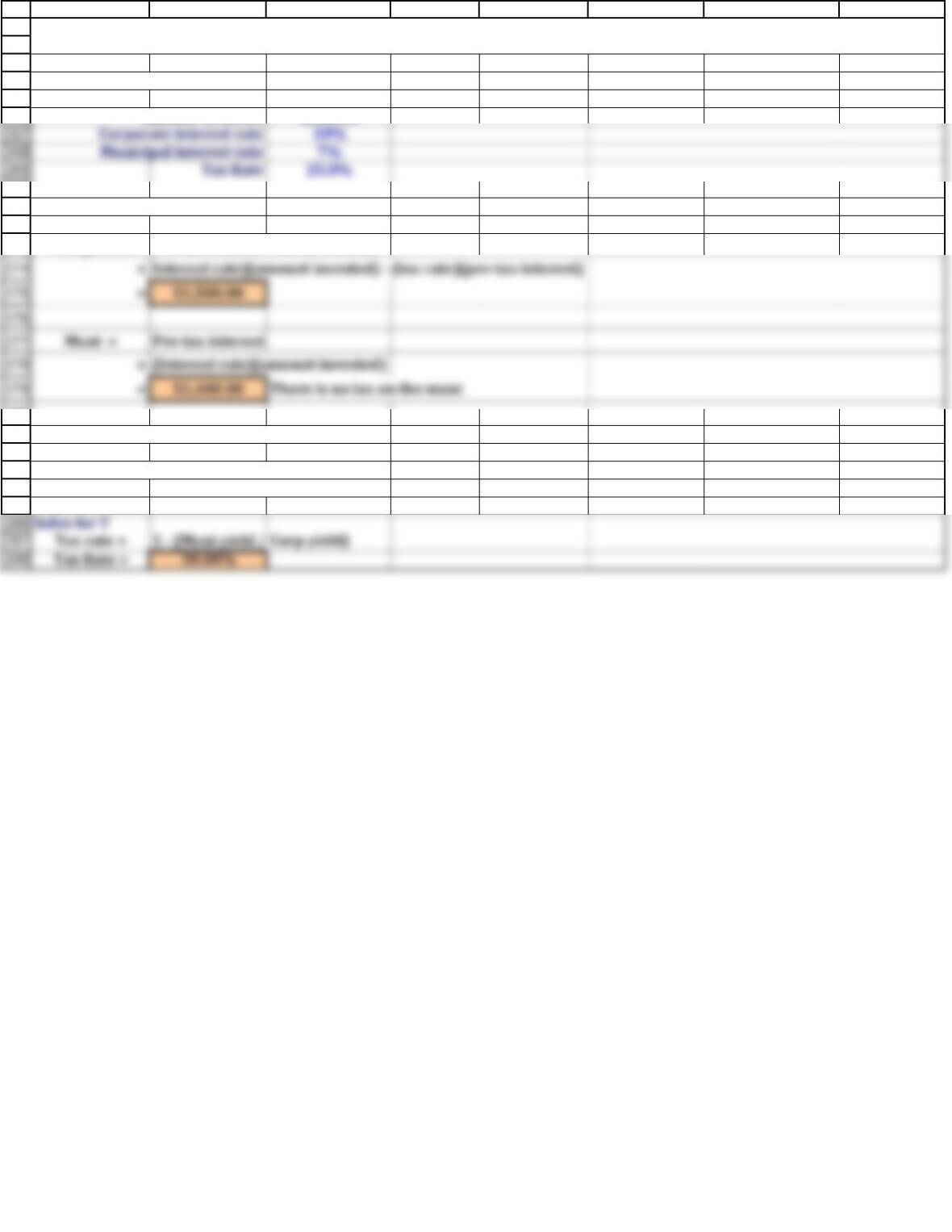

Taxable vs. Tax Exempt bonds

Amount to invest $20,000

After-tax interest

Corporate = Pre-tax interest – tax on interest

Tax rate at which you would be indifferent

After-tax yield on muni versus corp bond

Muni Yield = Corp Yield *(1-Tax rate)

l. Assume that you are in the 25% marginal tax bracket and that you have $20,000 to invest. You have narrowed your

investment choices down to municipal bonds yielding 7% or equally risky corporate bonds with a yield of 10%. Which one

should you choose and why? At what marginal tax rate would you be indifferent?