Mini Case: 2 – 12

MINI CASE

Jenny Cochran, a graduate of The University of Tennessee with 4 years of experience as an

equities analyst, was recently brought in as assistant to the chairman of the board of

Computron Industries, a manufacturer of computer components.

During the previous year, Computron had doubled its plant capacity, opened new

sales offices outside its home territory, and launched an expensive advertising campaign.

Cochran was assigned to evaluate the impact of the changes. She began by gathering

financial statements and other data. Note: these are available in the file Ch02 Tool Kit.xlsx in

the Mini Case tab.

Balance Sheets

2018

2019

Assets

Cash and equivalents

$ 60

$ 50

Short-term investments

100

10

Accounts receivable

400

520

Inventories

620

820

Total current assets

$ 1,180

$ 1,400

Gross fixed assets

$ 3,900

$ 4,820

Less: Accumulated depreciation

1,000

1,320

Net plant and equipment

$ 2,900

$ 3,500

Total assets

$ 4,080

$ 4,900

Liabilities and equity

Accounts payable

$ 300

$ 400

Notes payable

50

250

Accruals

200

240

Total current liabilities

$ 550

$ 890

Long-term bonds

800

1,100

Total liabilities

$ 1,350

Common stock

1,000

1,000

Retained earnings

1,730

1,910

Total equity

$ 2,730

$ 2,910

Total liabilities and equity

$ 4,080

$ 4,900

Mini Case: 2 – 13

Income Statement

2018

2019

Net sales

$ 5,500

$ 6,000

Cost of goods sold (Excluding depr. & amort.)

4,300

4,800

Depreciation and amortizationa

290

320

Other operating expenses

350

420

Total operating costs

$ 4,940

$ 5,540

Earnings before interest and taxes (EBIT)

$ 560

$ 460

Less interest

68

108

Pre-tax earnings

$ 492

$ 352

Taxes (25%)

123

88

Net Income

$ 369

$ 264

Other Data

Stock price

Shares outstanding

Common dividends

Tax rate

Weighted average cost of capital (WACC)

Mini Case: 2 – 14

Statement of Cash Flows

2019

Operating Activities

Net Income before preferred dividends

$ 264

Noncash adjustments

Depreciation and amortization

Due to changes in working capital

Change in accounts receivable

(120)

Change in inventories

(200)

Change in accounts payable

100

Change in accruals

40

Net cash provided by operating activities

$ 404

320

Investing activities

Cash used to acquire fixed assets

$ (920)

Change in short-term investments

90

Net cash provided by investing activities

$ (830)

Financing Activities

Change in notes payable

$ 200

Change in long-term debt

300

Payment of cash dividends

(84)

Net cash provided by financing activities

$ 416

Cash and securities at beginning of the year

60

Cash and securities at end of the year

$ 50

a. What effect did the expansion have on sales and net income? What effect did the

expansion have on the asset side of the balance sheet? What effect did it have on

liabilities and equity?

Answer: Sales increased by $500 million (9% growth), but net income fell by $105 million.

Mini Case: 2 – 15

b. What do you conclude from the statement of cash flows?

Answer: Net CF from operations was positive, but was dragged down by a large net increase in

c. What is free cash flow? Why is it important? What are the five uses of FCF?

Answer: FCF is the amount of cash available from operations for distribution to all investors

d. What is Computron’s net operating profit after taxes (NOPAT)? What are

operating current assets? What are operating current liabilities? How much net

operating working capital and total net operating capital does Computron have?

Answer: NOPAT = EBIT(1 – TAX RATE)

Mini Case: 2 – 16

e. What is Computron’s free cash flow (FCF)? What are Computron’s “net uses” of

its FCF?

Answer: FCF = NOPAT – Net investment in capital

= $345 – ($4,250 – $3,480)

= $345 – $770

= -$425.

Mini Case: 2 – 17

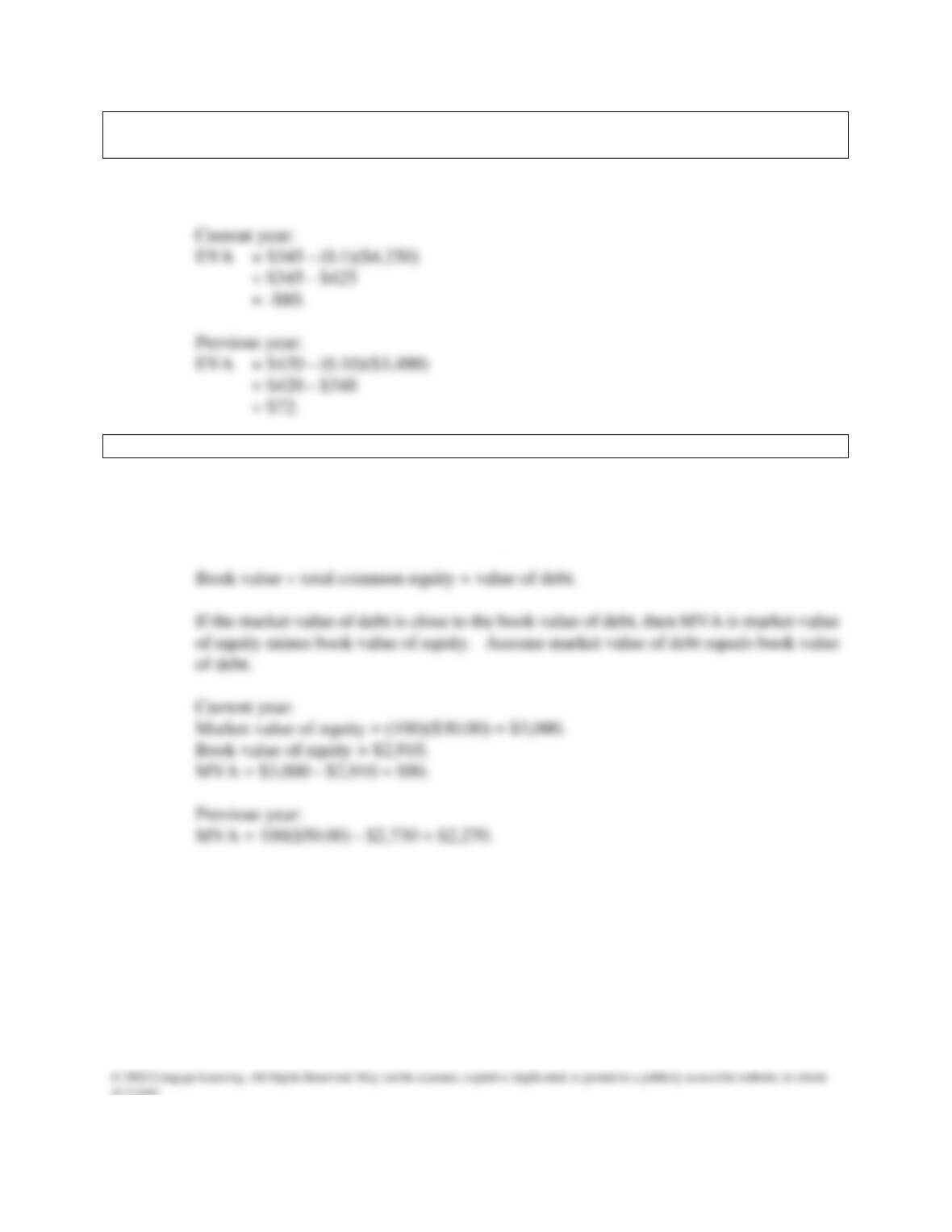

f. Calculate Computron’s return on invested capital (ROIC). Computron has a 10%

cost of capital (WACC). What caused the decline in the ROIC? Was it due to

operating profitability or capital utilization? Do you think Computron’s growth

added value?

ANSWER: ROIC = NOPAT / TOTAL NET OPERATING CAPITAL.

Current year:

ROIC = $345 / $4,250

= 8.1%.

Mini Case: 2 – 18

g. Cochran also has asked you to estimate Computron’s EVA. She estimates that the

after-tax cost of capital was 10 percent in both years.

ANSWER: EVA = NOPAT- (WACC)(CAPITAL).

h. What happened to Computron’s market value added (MVA)?

Answer: MVA = market value of the firm – book value of the firm.

Market value = (# shares of stock)(price per share) + value of debt.

Mini Case: 2 – 19

i. The Tax Cut and Jobs Act (TCJA) was signed into law in 2017. Briefly describe

its key provisions for corporate taxes.

Answer: The Tax Cut and Jobs Act (TCJA) made major changes to corporate taxes. The

changes will remain in place until Congress passes a new tax bill. Following are

explanations for some of the TCJA’s major changes and features.

Mini Case: 2 – 20

j. Assume that a corporation has $87 million of taxable income from operations. It

also received interest income of $8 million and dividend income of $10 million.

The federal tax rate is 21% and the dividend exclusion rate is 50%. What is its

taxable income and federal tax liability?

Answer: Calculation of the company’s tax liability:

Mini Case: 2 – 21

k. Briefly describe the TCJA’s key provisions for personal taxes.

Answer: The TCJA specifies the previous tax code for personal taxes is suspended and that

TCJA’s changes to personal taxes are for 2018-2025, after which they expire and the

personal tax code reverts to its pre-TCJA form. Following are explanations for some

of the TCJA’s major changes and features.

Mini Case: 2 – 22

l. Assume that you are in the 25% marginal tax bracket and that you have $20,000

to invest. You have narrowed your investment choices down to municipal bonds

yielding 7% or equally risky corporate bonds with a yield of 10%. Which one

should you choose and why? At what marginal tax rate would you be indifferent?

Answer: After-tax return income at T = 25%:

After-tax interest on corporate bond = 0.10($20,000) – (0.25)(0.10)($20,000) = $2,000

– $500 = $1,500.