511

Chapter 19 Options

Chapter Overview

The Opening Focus looks at U.S. Congress’s enactment of the TARP or the Troubled As-

set Relief Program passed in 2008. This TARP cost initially $700 billion dollars to tax payers. But

in the process the U.S. government was allowed to make equity investments in financial institu-

tions. Initially the TARP investment program cost the taxpayers a 26% loss on the investment.

The value of the investments was determined using Black and Scholes option pricing model. By

Opening Focus Discussion Questions:

1. How could the investment into banks such as Wells Fargo, JP Morgan and Bank of America be

similar to an option? Several of these banks actually showed a profit during the downward

trend 2008, why did they participate in the TARP program?

2. In what respect are options like gambling? In what respect are they like insurance?

This chapter covers:

19-1. Options Vocabulary

19-2. Option Payoff Diagrams

Technology

1. Smart Practices Video. Myron Scholes of Stanford University and chairman of Oak Hill Plat-

2. Smart Ethics Video. John Eck, president of broadcast and network operations for NBC, dis-

cusses how use of derivatives can raise accounting questions.

4. Smart Concepts. A step-by-step explanation of the binomial option pricing model.

6. Smart Ideas Video. Myron Scholes believes companies should expense employee stock op-

tion grants.

7. Smart Solutions. Step-by-step solutions to problems P19-6 and P19-8, option payoff dia-

gramming.

512 Instructor’s Manual

Lecture Guide

While options can be viewed as betting on a desired outcome – price up, price down, price

stable, price moving within a certain range, etc. – options also can be used as insurance. Using op-

tions can in fact decrease, not increase, risk. The market for derivative securities, which include

19-1 Options Vocabulary

There are no easy shortcuts to learning and memorizing basic options terminology. Show-

19-1a Option Trading

This section breaks down a simple example of the trading of an option between two GE

employees. It explains that not all options are issued by the corporation on which the option is on.

• Student Involvement: Have the student think of a company where an option would be a

good choice for making money or as insurance.

Table 19.1 Option Price Quotes for Opti-Tech Corp.

19-1b Option Prices

This section introduces more terminology, explaining when options are in, out and at the

money. The instructor might wish to use a numerical example, for example, a call option with a

19-2 Option Payoff Diagrams

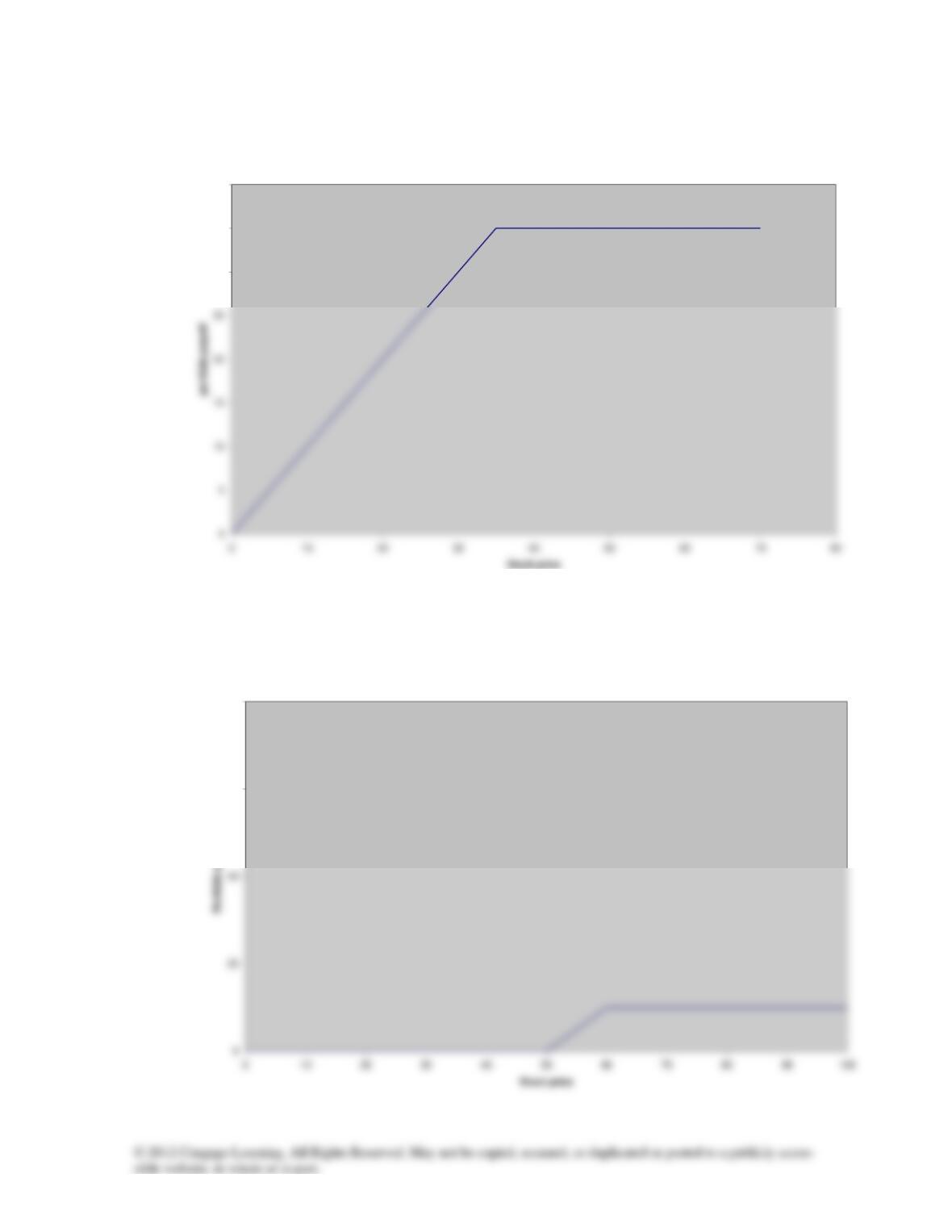

19-2a Call Option Payoffs

Figure 19-1 Payoff of a Call Option with X = $75

Chapter 19 Options 513

The value of options at expiration is best illustrated with “hockey stock” diagrams which

19-2b Put Option Payoffs

Figure 19-2 Payoff of Put Option with X = $75

This section diagrams buying (going long) and selling (going short) with put options and

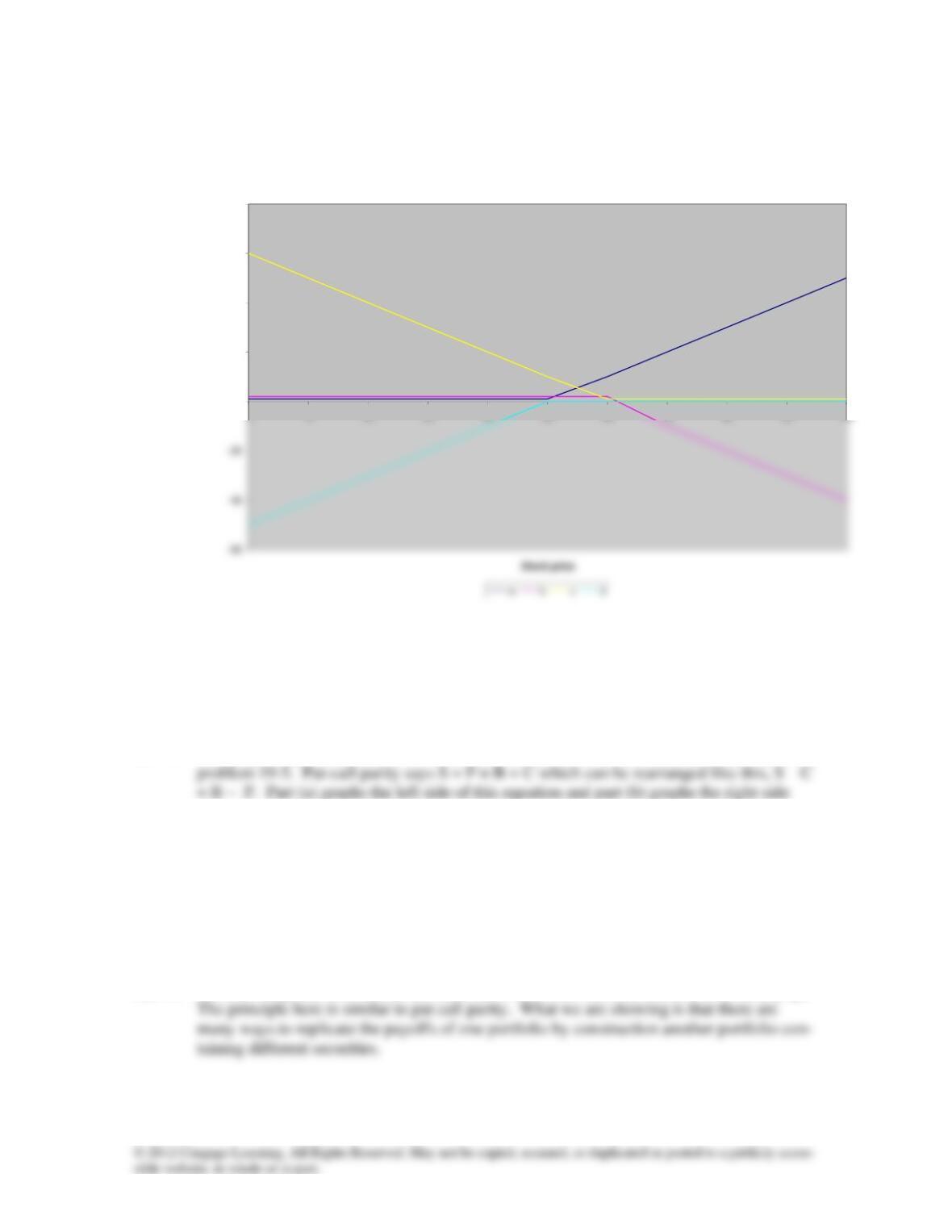

19-2c Payoffs for Portfolios of Options and Other Securities

Note that put and call options can be combined to create literally any payout pattern de-

sired. For example, Figure 19-3 illustrates a combination of buying a call and buying a put option

Figure 19.3 Payoff to Portfolio Containing 1 Call and 1 Put (X = $30)

Additional payoff patterns, like straddles, can be devised by combining options, stocks and

bonds, and often there are several ways to achieve the same payoff pattern.

Figure 19.4 Payoff Diagrams

These sections illustrate that different combinations of securities can be combined to create

the same payoff patterns. Spending time on each of the figures in this section can help students to

grasp some of the many ways options can be used to hedge one’s position in an investment.

Figure 19.5 Payoff from One Long Share and One Long Put (X=40)

19-2d Put-Call Parity

The previous sections illustrate the put-call parity relationship. This is a relationship that

can be used to price a put when the call price is known and visa versa – just rearrange terms of the

equation on the slide with P, put price on one side to get the put price when the other variables are

514 Instructor’s Manual

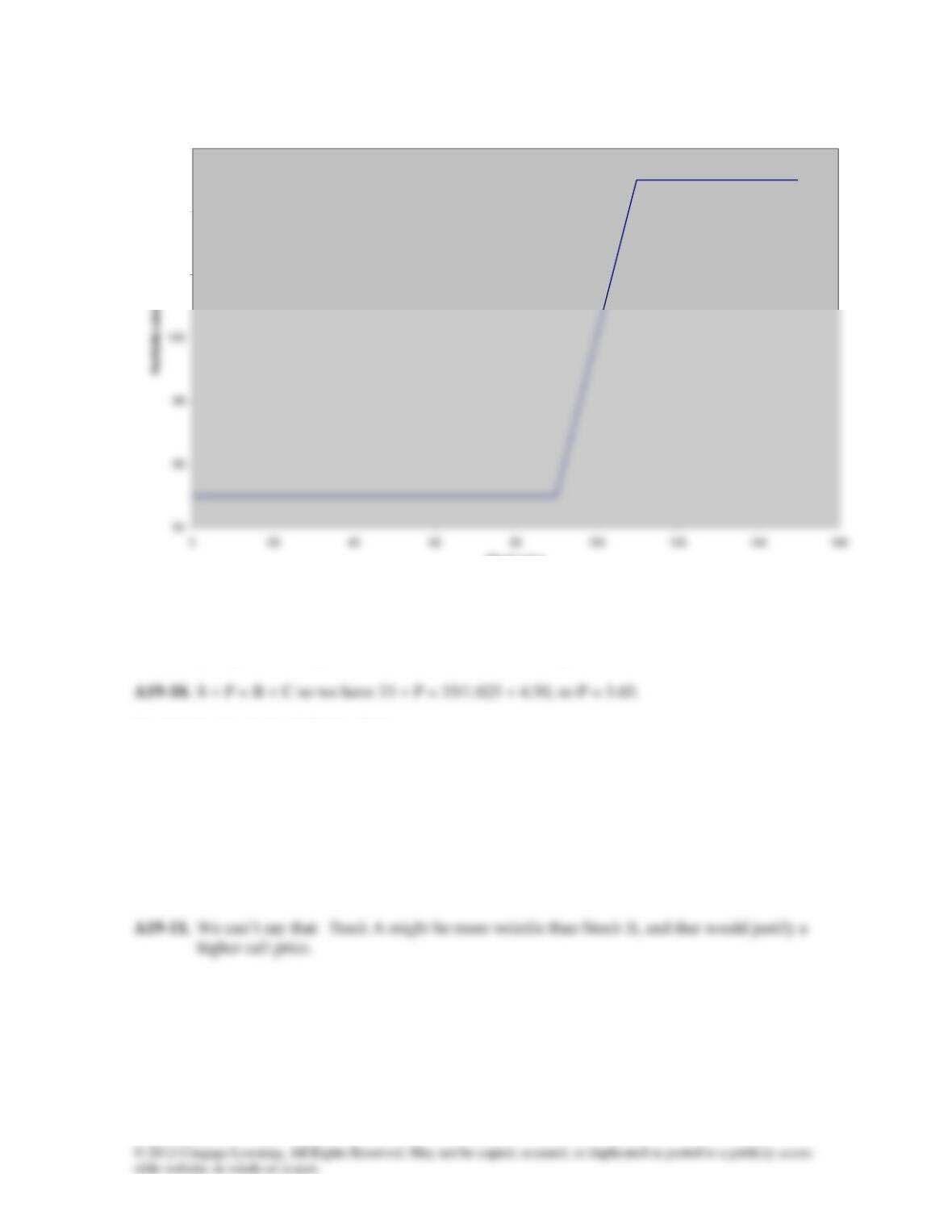

Figure 19.6 Payoff on Portfolio of One Bond (FV=$75) and One Call (X = $75)

19-3 Qualitative Analysis of Option Prices

19-3a Factors that Influence Option Values

The instructor can use the payoff diagrams for options to illustrate the impact of changes in

the option pricing variables on option value. For example, if you look at the diagram for the payoff

of a call option, the X axis is the value of the underlying asset. As this increases, call option value

Table 19-2 Prices of Option Contracts on Whirlpool Stock, February 18, 2011

Table 19-3 Prices of March Option Contracts on Whirlpool Stock

Table 19.4 Prices of Option Contracts on Two Stocks, February 18, 2011

Figure 19-7 Daily Percentage Changes Whirlpool and MOSAIC

Options are primarily written on young, riskier companies, rather than stable, mature com-

19-4 Option Pricing Models

19-4a Binomial Option Pricing

The binomial model is a simplified model that assumes that an asset can take on only one of

two values in the future. Looking at these values and the probability of each occurring, you can

backtrack and calculate the value of an option on the asset. This model works because it assumes

Chapter 19 Options 515

Figure 19-8 Binomial Option Pricing

19-4b Black and Scholes Model

The Black-Scholes option pricing model was a ground breaking (and Nobel prize-winning)

achievement in pricing derivative securities. The Black-Scholes model presents a set of equations

using the five variables (stock price, exercise price, time to expiration, volatility and risk-free rate)

from Chapter 18 that can be used to price options and other derivative securities. The equations

look difficult, but can be solved using a calculator and a set of standard normal distribution tables,

Note that the Black-Scholes model assumes continuous compounding. While this is not true in

reality, it is close enough. With the increase in markets around the world, most stocks can be trad-

ed 24/7 (or reasonably close to continuously.) The model makes options considerably easier to

price because four of the five inputs (all except volatility) are readily observable. Volatilities are

not as easy to determine. If you use past information to calculate volatility, which past period

should you use? Will the past volatility be representative of the future or will volatility change in

the future?

Fig. 19-9 Multistage Binomial Trees

Fig. 19.10 Standard Normal Distribution

19-5 Options in Corporate Finance

This section covers employee stock options, warrants, and convertibles.

19-5a Employee Stock Options

Many firms use stock option grants (ESOs) as part of their compensation structure. They

are essentially call options that give the employee the right to buy shares of stock in the company

19-5b Warrants and Convertibles

Warrants are securities that are issued by firms and that grant investors the right to buy

516 Instructor’s Manual

Fig. 19.11The Value of a Convertible Bond

Options Summary

It is becoming more and more common to spot options in projects – real options. A com-

pany rarely accepts a project in isolation. There may be an abandonment value to a project if the

Enrichment Exercises

Ask students to apply the binomial pricing model in the following example. ABC Company has

invented a new technology that will dramatically decrease the cost of new cars. There is a 50%

chance the test results will be as expected so that whomever purchases the license for the technolo-

First, the value of the technology if the test is successful is 18/0.1 = $180 million. The value if the

technology is not successful is 6/0.1 = $60 million. At a price of $130 million, no one will buy the

technology if the test is unsuccessful. It is a good price if the technology is successful. Multiply-

ing the value of a “good test” by the probability of its occurring realizes: 0.5 x $180 million = $90

million. This is a year 0 cash flow, since the perpetuity formula states that CF1/r = value in year 0,

and $18 million is a year 1 cash flow, if the test is successful. The cost of the investment is a 0.5

probability x $130 = $65 million.

Year 1 Year 2

Chapter 19 Options 517

Show the class a 60-minute PBS special, “The Trillion Dollar Bet,” which can be ordered from

pbs.org. This program talks about the development of the Black-Scholes model, including inter-

Answers to Concept Review Questions

1. The stock price and the option premium determine what an investor has to pay to acquire the

stock or the option in the market. These prices are determined by market forces, while the ex-

2. A long position means buying an option, and a short position means selling the option. The

person who takes the long position has the right to buy (call) or sell (put) the underlying stock,

4. An increase in the strike price would increase the value of a put option, because it would entitle

the option holder to sell the stock for a higher price.

5. If an investor who owned a share of a particular stock also bought a put option with a strike

price of $50 and sold a call option with a strike price of $50, the resulting portfolio would pay

6. Selling a call and buying a put are similar in the sense that both positions are most (least) prof-

itable when the underlying stock price falls (rises). However, the similarities end there. An

7. Figure 19.3 shows how an investor can profit from a stock’s volatility. If investors expect a

518 Instructor’s Manual

8. If an asset’s risk increases, its price declines. The opposite true for options, because options

have asymmetric payoffs, meaning that how an option’s payoff changes as the underlying stock

9. Calls and puts respond differently to changes in the underlying stock price, but they both tend

to increase in value as time to expiration and volatility of the underlying stock increases.

10. To value options using the binomial method, it is not necessary to know the expected return on

the stock for the same reason that it is not necessary to know the probabilities of up and down

11. The binomial model assumes that if a portfolio of stock and options has a payoff identical to

that provided by a risk-free bond, then the price of the portfolio must be the same as the price

12. Employee stock options are different from the options that trade on the exchanges and in the

13. Firms should be required to show an expense on their income statement for employee stock

14. If a warrant and a call option have the same strike price, the same expiration date, and the same

Solutions to Self-Test Problems

ST19-1. Several call options on Cuban Cigars Inc. are available for trading. The expiration date,

strike price, and current premium for each of these options appear below.

Strike

Expiration

Premium

$40

July

$6.00

$50

July

$1.75

Chapter 19 Options 519

A: As the accompanying diagram shows, this portfolio has a zero payoff if the stock price is

2

3

4

5

ST19-2. A stock currently sells for $36. In the next six months, the stock will either go up to $42

or it will fall to $31. If the risk-free rate is 4% per year, calculate the current market

A: First draw the tree illustrating how the stock price will move and list the payoff of the

option at each terminal node of the tree.

Stock Values Option Pays

42 $7

520 Instructor’s Manual

the stock price goes down the payoff on the portfolio will be 31 + 0h. Set these expres-

sions equal to each other to find h:

Answers to End-of-Chapter Questions

Q19-1. Explain why an option is a derivative security.

Q19-2. Is buying an option more or less risky than buying the underlying stock?

A19-2. The option is more risky than the underlying stock if the absolute dollar amounts invested

in each is equal. With options, there is a very significant chance that the investor will lose

100% of the money invested. There is also a very good chance of a very high positive re-

turn. The likelihood of such extreme returns on stocks is very low. For example, inves-

Chapter 19 Options 521

Q19-3. What is the difference between an option’s price and its payoff?

A19-3. The option price or premium is what one pays for the option in the market, or what one

Q19-4. List five factors that influence the prices of calls and puts.

Q19-5. What are the economic benefits that options provide?

A19-5. They provide incentives which help align the interests of managers and investors. They

Q19-6. What is the primary advantage of settling options contracts in cash?

Q19-7. Suppose you want to invest in a particular company. What are the pros and cons of buy-

ing the company’s shares as compared to buying their options?

Q19-8. Suppose you want to make an investment that will be profitable if a company’s stock

price falls. What are the pros and cons of buying a put option on the company’s stock

versus short selling the stock?

A19-8. If you buy a put option, the most you can lose is the option premium. If you short the

Q19-9. Suppose you own an American call option on Pfizer stock. Pfizer stock has gone up in

value considerably since you bought the option, so your investment has been profitable.

There is still one month to go before the option expires, but you decide to go ahead and

take your profits in cash. Describe two ways that you could accomplish this goal. Which

one is likely to leave you with the highest cash payoff?

A19-9. You could exercise your option, buying Pfizer at the strike price and selling it at the high-

Q19-10. Look at the Opti-tech call option prices in Table 19.1. Call prices increase as the strike

price decreases, holding the expiration month constant. The strike prices decrease in in-

crements of $2.50. Do the call option prices increase in constant increments? That is,

522 Instructor’s Manual

does the call price increase by the same amount as the strike price drops from $35 to

$32.50 to $30 and so on?

A19-10. No, the option value does not change by $2.50 each time the strike price changes by

Solutions to End-of-Chapter Problems

Options Vocabulary

P19-1. If the underlying stock price is $25, indicate whether each of the options below is in the

money, at the money, or out of the money.

Strike

Call

Put

$20

$25

$30

A19-1.

Strike

Call

Put

$20

In the money

Out of the money

$30

Out of the money

In the money

P19-2. The stock of Spears Entertainment currently sells for $28. A call option on this stock has

a strike price of $25 and it sells for $5.25. A put option on this stock has a strike price of

$30, and it sells for $3.10. What is the intrinsic value of each option? What is the time

value of each option?

Option Payoff Diagrams

P19-3. Draw payoff diagrams for each of the positions below (X = strike price).

a. Buy a call with X = $50

b. Sell a call with X = $60

c Buy a put with X = $60

d. Sell a put with X = $50

Chapter 19 Options 523

Solution to Problem 15-4

0

20

40

60

80

010 20 30 40 50 60 70 80 90 100

Option payoff

P19-4. Draw payoff diagrams for each of the portfolios below (X = strike price).

a. Buy a share of stock and short a call with X = $35

b. Buy a risk-free zero-coupon bond with a face value of $35 and sell a put with X =

$35.

c. Explain how these payoff diagrams relate to the concept of put-call parity.

A19-4. The graphs in parts (a) and (b) are actually identical and look as shown immediately after

P19-5. Draw payoff diagrams for each of the following portfolios (X = strike price):

a. Buy a call with X = $50, and sell a call with X = $60

b. Buy a bond with a face value of $10, short a put with X = $60, and buy a put with X =

$50

c. Buy a share of stock, buy a put option with X = $50, sell a call with X = $60, short a

bond (i.e., borrow) with a face value of $50.

d. What principle do these diagrams illustrate?

A19-5. All three diagrams are exactly the same and look as shown at the bottom of the next page.

A15-3.

524 Instructor’s Manual

Solution to Problem 15-5

30

35

40

Problem 15-6 Solution

60

80

Problem 19-4

Problem 19-5

Chapter 19 Options 525

P19-6. Draw a payoff diagram for the following portfolio: Buy two call options, one with X =

$20 and one with X = $30, and sell two call options, both with X = $25.

A19-6.

Problem 15-7 Solution

30

P19-7. Refer to the data in the following table.

Strike Price

Put Price

$30

$1.00

$35

$3.50

$40

$6.50

Suppose an investor purchases 1 put with X = $30 and one put with X = $40 and sells two

puts with X = $35. Draw a payoff diagram for this position. In your diagram, show the

gross payoff (ignoring the costs of buying and selling the options) and the net payoff. In

what range of stock prices does the investor make a net profit? What is the investor’s

maximum potential dollar profit and maximum potential dollar loss?

A19-7. The maximum net dollar gain and loss are $4.50 and -$0.50 respectively. The portfolio

526 Instructor’s Manual

Problem 15-8 Solution

15

20

P19-8. Draw a payoff diagram for the following portfolios:

a. Buy a bond with a face value of $80, buy a call with X = $80, and sell a put with X =

$80.

b. Buy a share of stock, buy a put with X = $80, and sell a call with X = $80.

c. Buy a share of stock, buy a put with X = $80, and sell a bond with a face value of

$80.

A19-8. These are all just applications of put call parity, S + P = B + C. In part (a), the graph

P19-9. Suppose that Lisa Emerson owns a share of Zytex Chemical stock which is worth $100

per share. Lisa purchases a put option on this stock with a strike price of $95 and she sells

a call option with a strike price of $105. Plot the payoff diagram for Lisa’s new portfolio

and explain how it relates to this chapter’s opening focus.

Chapter 19 Options 527

Problem 15.9 Solution

102

104

106

Stock price

P19-10. Imagine that a stock sells for $33. A call option with X = $35 and an expiration date in

six months sells for $4.50. The annual risk-free rate is 5 percent. Calculate the price of a

put option that expires in six months and has a strike price of $35.

Qualitative Analysis of Option Prices

P19-11. Examine the data in the table below. Given that both stocks trade for $50 and both op-

tions have a $45 strike price and a July expiration date, can we say that the option of

Company A is overvalued or that the option of Company B is undervalued? Why or why

not?

Company

Stock Price

Expiration

Strike Price

Call Price

A

$50

July

$45

$7.50

B

$50

July

$45

$6.75

P19-12. Examine the data in the table below. The call option on company #1 is out of the money

by $1 and so is the call option on company #2. Given that the options expire at the same

time, is it surprising that their prices are so different? Why or why not?

Company

Stock Price

Expiration

Strike Price

Call Price

#1

$49

August

$50

$6.00

#2

$19

August

$20

$3.75

528 Instructor’s Manual

P19-13. Suppose an American call option is in the money, so S > X. Demonstrate that the market

price of this call (C) cannot be less than the difference between the stock price and the ex-

ercise price. That is, explain why this must be true: C ≥ S – X. (Hint: consider what

would happen if C < S – X).

A19-13. If the call sold for less than its intrinsic value (S – X), then arbitrage would be possible.

P19-14. a. A call option expires in three months and has X = $40. The underlying stock is worth

$42 today. In three months, the stock may increase by $7 or decrease by $6. The

risk-free rate is 2% per year. Use the binomial model to value the call option.

b. A put option expires in three months and has X = $40. The underlying stock is worth

$42 today. In three months the stock may increase by $7 or decrease by $6. The risk-

free rate is 2% per year. Use the binomial model to value the put option.

c. Given the call and put prices you calculated in parts (a) and (b), check to see if put-

call parity holds.

A19-14. a. 49 + 9h = 36 + 0h so h = −13/9. Buying 1 share and selling 13/9 calls gives a risk-

P19-15. A stock is worth $20 today, and it may increase or decrease $5 over the next year. If the

risk-free rate of interest is 6%, calculate the market price of the at-the-money put and call

options on this stock that expire in one year. Which option is more valuable, the put or

the call? Is it always the case that a call option is worth more than a put if both are tied to

the same underlying stock, have the same expiration date, and are at the money? (Hint:

use put-call parity to prove the statement true or false.)

A19-15. Value the call first. 25 + 5h = 15 + 0h so h = –2 and the risk-free payoff is 15. The PV

Chapter 19 Options 529

P19-16. Explain the following paradox. A put option is a highly volatile security. If the underly-

ing stock has a positive beta, then a put option on that stock will have a negative beta (be-

cause the put and the stock move in opposite directions). According to the CAPM, an

asset with a negative beta, such as the put option, has an expected return below the risk-

free rate. How can an equilibrium exist in which a highly risky security such as a put op-

tion offers an expected return below a much safer security such as a Treasury bill?

A19-16. A put option is like an insurance policy for stocks because when stocks go down, puts go

up. Adding a put to a stock portfolio provides protection against downside risk, and in-

P19-17. A particular stock sells for $27. A call option on this stock is available with a strike price

of $28 and an expiration date in four months. If the risk-free rate equals 6% and the

standard deviation of the stock’s return is 40%, what is the price of the call option? Next,

recalculate your answer assuming that the market price of the stock is $28. How much

does the option price change in dollar terms? How much does it change in percentage

terms?

P19-18. Temex Foods stock currently sells for $48. A call option on this stock is available with a

strike price of $45 and an expiration date six months in the future. The standard deviation

of the stock’s return is 45%, and the risk-free interest rate is 4%. Calculate the value of

the call option. Next, use put-call parity to determine the value of a Temex put option that

also has a $45 strike price and six months until expiration.

Options in Corporate Finance

P19-19. A convertible bond has a par value of $1,000 and a conversion ratio of 20. If the underly-

ing stock currently sells for $40 and the bond sells at par, what is the conversion premi-

um? The conversion value?

Answer to MiniCase

Options

You have recently spent one of your Saturday afternoons at an options seminar presented by Deriv-

atives Traders Incorporated. Interested in putting some of your new knowledge to work, you start

by thinking about possible returns from an investment in the volatile common stock of Purchase-

Pro.com, Incorporated (PPRO). Four options currently trade on PPRO. Two are call options, one

with a strike price of $35 and the other with a strike price of $45. The other two are put options,

530 Instructor’s Manual

Assignment

1. You believe the price of PPRO will rise and are therefore considering either (a) taking a long

position in a $45 call by paying a premium of $3, or (b) taking a short position in a $45 put for

which you will receive a premium of $3. If the stock price is $50 on the expiration date,

which position makes you better off?

2. You believe the price of PPRO will fall and are therefore considering either (a) taking a long position

in a $35 put, paying a premium of $2, or (b) taking a short position in a $35 call, receiving a premi-

um of $2. If the stock price is $30 on the expiration date, which position makes you better off?

3. Assume you can buy or sell either the call or the put options, with a strike price of $35. The

call option has a premium of $3, and the put option has a premium of $2. Which of these op-

tion contracts can be used to form a long straddle? What is the payoff if the stock price closes

at $38 on the option expiration date? What is the payoff if the stock price closes at $28 on the

option expiration date?

4. Assume you can buy or sell either the call or the put options, with a strike price of $35. The

call option has a premium of $3, and the put option has a premium of $2. Which of these op-

tion contracts can be used to form a short straddle? What is the payoff if the stock price closes

at $38 on the option expiration date? What is the payoff if the stock price closes at $28 on the

option expiration date?

Answers

1. If the stock price goes from $40 to $50 per share you are better writing the $45 put (a short po-

sition in the put results in a profit of $3 per option, while the long position in the call results in

2. If the stock price goes from $40 to $30 per share you are better buying the $35 put (a long posi-

tion in the put results in a profit of $3 per option, while the short position in the call results in a

3. To form a long straddle both the $35 call and $35 put options are purchased (long positions).

The total cost is $5 per straddle (the $3 premium on the call option and the $2 premium on the

4. To form a short straddle one would write both the $35 call and $35 put options (short posi-

tions). The total cost is $5 per straddle (the $3 premium on the call option and the $2 premium