1

2

3

4

5

6

7

8

9

10

11

17

18

19

20

21

22

23

24

25

26

27

28

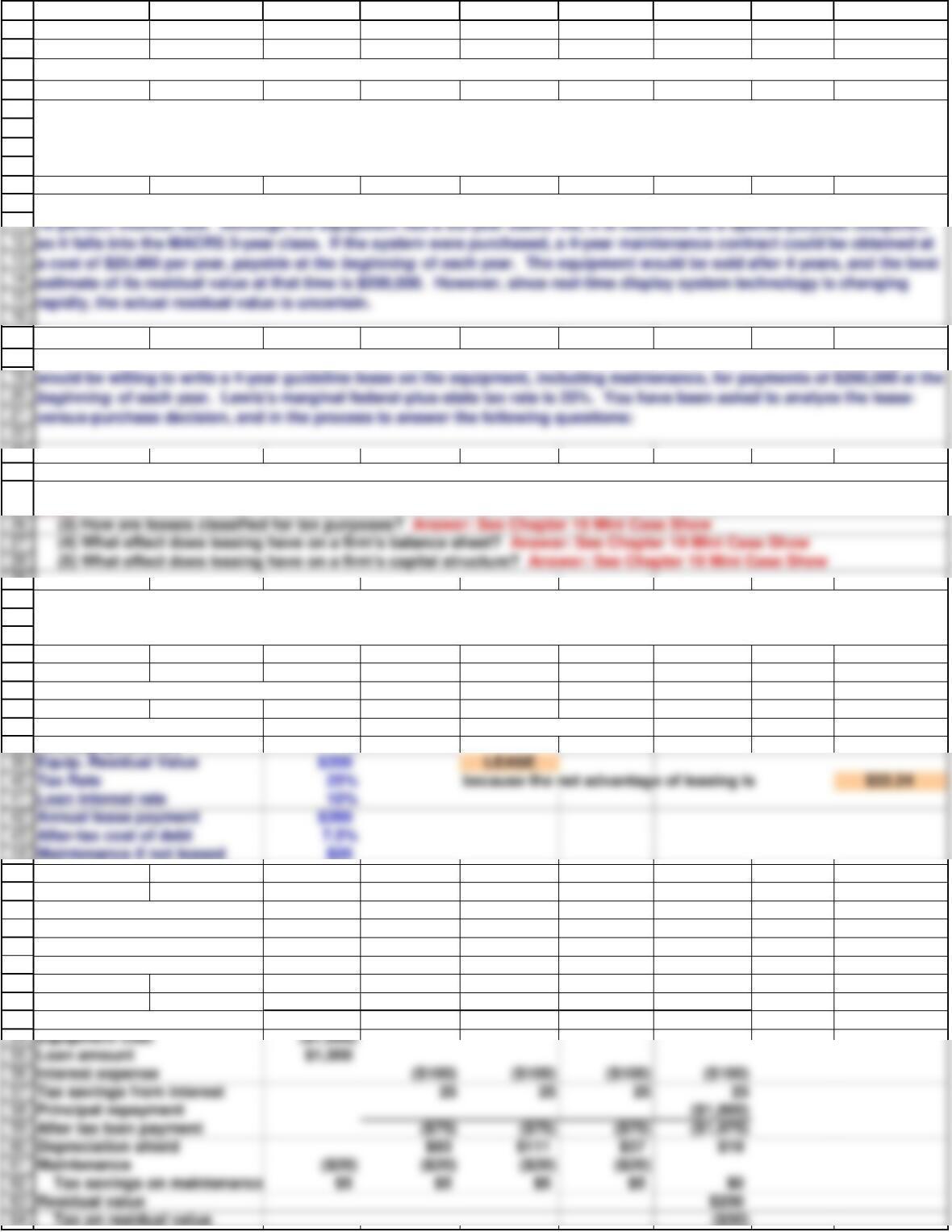

(4) What effect does leasing have on a firm’s balance sheet? Answer: See Chapter 19 Mini Case Show

(3) How are leases classified for tax purposes? Answer: See Chapter 19 Mini Case Show

(5) What effect does leasing have on a firm’s capital structure? Answer: See Chapter 19 Mini Case Show

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

Equip. Residual Value $200 LEASE

Tax Rate 25% because the net advantage of leasing is $22.24

Loan interest rate 10%

Annual lease payment $260

After-tax cost of debt 7.5%

Maintenance if not leased $20

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

60

62

63

64

Equipment cost ($1,000)

Loan amount $1,000

Interest expense ($100) ($100) ($100) ($100)

Tax savings from interest 25 25 25 25

Principal repayment ($1,000)

After tax loan payment ($75) ($75) ($75) ($1,075)

Depreciation shield $83 $111 $37 $19

Tax savings on maintenance

Residual value $200

Tax on residual value ($50)

A B C D E F G H I

11/23/2018

Input Data

(all dollar figures in thousands)

New Equipment cost $1,000 KEY OUTPUT

New Equipment life 4

NPV LEASE ANALYSIS

Depreciation Rate 33.33% 44.45% 14.81% 7.41%

Depreciation Expense 333.30 444.50 148.10 74.10

BV at end of year 666.70 222.20 74.10 –

Year = 0 1 2 3 4

Present Value of Owning

b. (1) What is the present value cost of owning the equipment? (Hint: Set up a time line which shows the net cash flows

over the period t = 0 to t = 4, and then find the PV of these net cash flows, or the PV cost of owning.)

Chapter 19. Mini Case for Lease Financing

Lewis Securities Inc. has decided to acquire a new market data and quotation system for its Richmond home office. The

system receives current market prices and other information from several on-line data services, then either displays the

information on a screen or stores it for later retrieval by the firm’s brokers. The system also permits customers to call up

current quotes on terminals in the lobby.

(2) What are the four primary types of leases, and what are their characteristics? Answer: See Chapter 19 Mini Case

Show

The equipment costs $1,000,000, and, if it were purchased, Lewis could obtain a term loan for the full purchase price at a

As an alternative to the borrow-and-buy plan, the equipment manufacturer informed Lewis that Consolidated Leasing

a. (1) Who are the two parties to a lease transaction? Answer: See Chapter 19 Mini Case Show

12

13

14

15

16

65

66

67

68

69

70

74

75

76

77

78

79

80

81

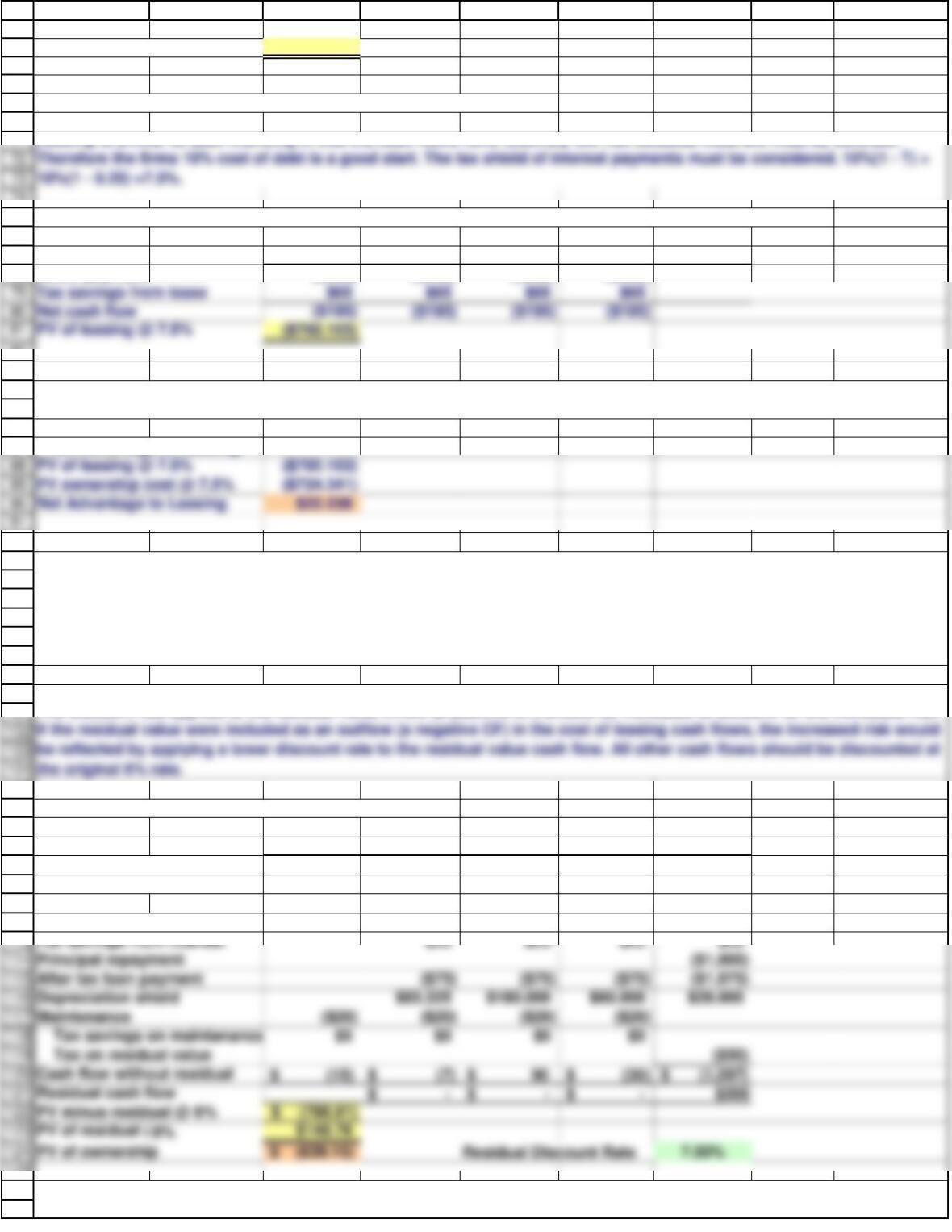

Tax savings from lease $65 $65 $65 $65

Net cash flow ($195) ($195) ($195) ($195)

82

83

84

85

86

87

88

89

90

91

PV of leasing @ 7.5% ($702.103)

PV ownership cost @ 7.5% ($724.341)

Net Advantage to Leasing $22.238

92

93

94

95

96

97

98

99

100

101

102

103

104

If the residual value were included as an outflow (a negative CF) in the cost of leasing cash flows, the increased risk would

105

106

107

108

109

110

111

112

113

114

115

116

117

118

119

120

121

122

Tax savings from interest $25 $25 $25 $25

Principal repayment ($1,000)

After tax loan payment ($75) ($75) ($75) ($1,075)

Depreciation shield $83.325 $180.000 $60.000 $28.000

Tax savings on maintenance

Tax on residual value ($50)

Cash flow without residual $ (15) $ (7) $ 90 $ (30) $ (1,097)

Residual cash flow $ – $ – $ – $200

PV minus residual @ 6% (788.91)$

PV of residual @

125

126

127

A B C D E F G H I

Net cash flow ($15.000) ($6.675) $21.125 ($52.975) ($906.475)

PV ownership cost @ 7.5 ($724.341)

c. What is Lewis’s present value cost of leasing the equipment? (Hint: Again, construct a time line.)

Year = 0 1 2 3 4

Lease payment ($260) ($260) ($260) ($260)

Net Advantage of Leasing

Alter the Residual Discount Rate to see the effect on PV

Year = 0 1 2 3 4

Present Value of Owning

Equipment cost ($1,000)

Loan amount $1,000

Interest expense ($100) ($100) ($100) ($100)

d. What is the net advantage to leasing (NAL)? Does your analysis indicate that Lewis should buy or lease the equipment?

Explain.

The lessor owns the equipment when the lease expires. Therefore, residual value risk is passed from the lessee to the

lessor. The increased residual value risk makes the lease more attractive to the lessee.

The discount rate applied to the residual value inflow (a positive CF) should be increased to account for the increased risk.

e. Now assume that the equipment’s residual value could be as low as $0 or as high as $400,000, but that $200,000 is the

expected value. Since the residual value is riskier than the other cash flows in the analysis, this differential risk should be

incorporated into the analysis. Describe how this could be accomplished. (No calculations are necessary, but explain how

you would modify the analysis if calculations were required.) What effect would increased uncertainty about the residual

value have on Lewis’s lease-versus-purchase decision?

(2) What is the discount rate for the cash flows of owning?

Leasing is similar to debt financing in that the cash flows have relatively low risk because most are fixed by contract.

71

72

73

128

129

130

134

135

136

137

138

139

140

141

142

143

144

145

146

147

148

149

150

151

152

153

154

155

156

157

158

159

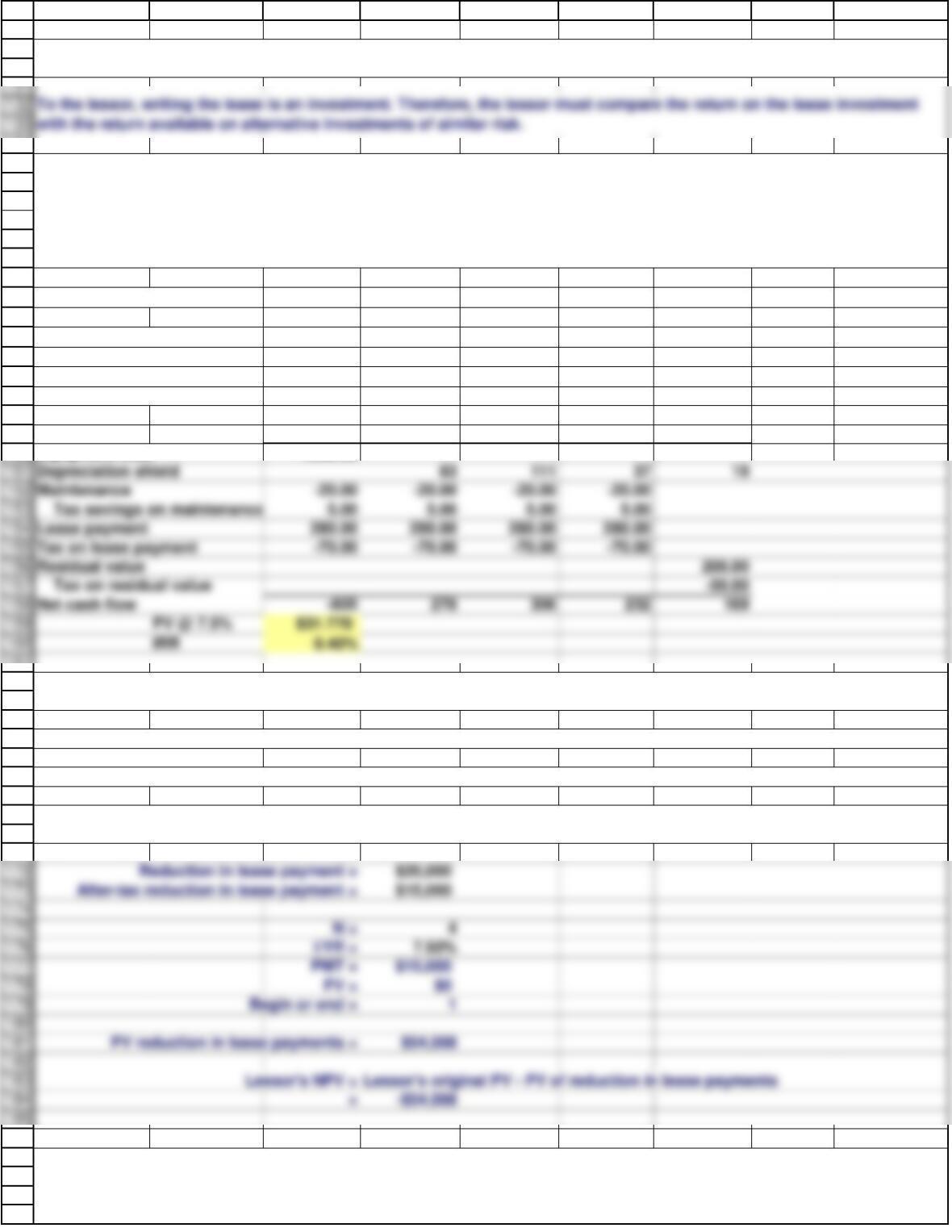

Depreciation shield 83 111 37 19

Tax savings on maintenance

Lease payment 280.00 280.00 280.00 280.00

Tax on lease payment -70.00 -70.00 -70.00 -70.00

Residual value 200.00

Tax on residual value -50.00

Net cash flow -805 278 306 232 169

161

162

163

164

165

166

167

168

169

170

171

172

173

174

175

176

177

178

179

180

181

182

183

184

185

186

187

188

189

190

A B C D E F G H I

NPV LEASOR’S ANALYSIS

Lease payment = $280

Lessor’s tax rate = 25%

Lessor’s pre-tax interest rate =

10%

After-tax discount rate = 7.50%

Year = 0 1 2 3 4

Equipment cost -1000.00

With lease payments of $260,000, the lessor’s cash flows would be equal, but opposite in sign, to the lessee’s NAL.

(22,238)

h. Lewis’s management has been considering moving to a new downtown location, and they are concerned that these

plans may come to fruition prior to the expiration of the lease. If the move occurs, Lewis would buy or lease an entirely

new set of equipment, and hence management would like to include a cancellation clause in the lease contract. What

impact would such a clause have on the riskiness of the lease from Lewis’s standpoint? From the lessor’s standpoint? If

you were the lessor, would you insist on changing any of the lease terms if a cancellation clause were added? Should the

cancellation clause contain any restrictive covenants and/or penalties of the type contained in bond indentures or

provisions similar to call premiums?

f. The lessee compares the cost of owning the equipment with the cost of leasing it. Now put yourself in the lessor’s

shoes. In a few sentences, how should you analyze the decision to write or not write the lease?

g. (1) Assume that the lease payments were actually $280,000 per year, that Consolidated Leasing is also in the 25 percent

tax bracket, and that it also forecasts a $200,000 residual value. Also, to furnish the maintenance support, Consolidated

would have to purchase a maintenance contract from the manufacturer at the same $20,000 annual cost, again paid in

advance. Consolidated Leasing can obtain an expected 10 percent pre-tax return on investments of similar risk. What

would Consolidated’s NPV and IRR of leasing be under these conditions?

(2) What do you think the lessor’s NPV would be if the lease payments were set at $260,000 per year? (Hint: The lessor’s

cash flows would be a “mirror image” of the lessee’s cash flows.)

Thus, lessor’s NPV =

If all inputs are symmetrical, leasing is a zero-sum game.

To verify this, note that a $20,000 reduction in each lease payment would reduce the lessor’s inflows by $20,000(0.75) =

$15,000 at the beginning of each year.

131

132

191

192

193

197

198

A B C D E F G H I

i. What are some other issues in lease analysis? Answer: See Chapter 19 Mini Case Show

h. Lewis’s management has been considering moving to a new downtown location, and they are concerned that these

plans may come to fruition prior to the expiration of the lease. If the move occurs, Lewis would buy or lease an entirely

new set of equipment, and hence management would like to include a cancellation clause in the lease contract. What

impact would such a clause have on the riskiness of the lease from Lewis’s standpoint? From the lessor’s standpoint? If

you were the lessor, would you insist on changing any of the lease terms if a cancellation clause were added? Should the

cancellation clause contain any restrictive covenants and/or penalties of the type contained in bond indentures or

provisions similar to call premiums?

194

195