Chapter 18

Capital Budgeting and Valuation with

Leverage

18–1. Explain whether each of the following projects is likely to have risk similar to the average risk of

the firm.

a. The Clorox Company considers launching a new version of Armor All designed to clean and

protect notebook computers.

b. Google, Inc., plans to purchase real estate to expand its headquarters.

c. Target Corporation decides to expand the number of stores it has in the southeastern United

States.

d. GE decides to open a new Universal Studios theme park in China.

18–2. Suppose Caterpillar, Inc., has 665 million shares outstanding with a share price of $74.77, and

$25 billion in debt. If in three years, Caterpillar has 700 million shares outstanding trading for

$83 per share, how much debt will Caterpillar have if it maintains a constant debt-equity ratio?

18–3. In 2015, Intel Corporation had a market capitalization of $134 billion, debt of $13.2 billion, cash

of $13.8 billion, and EBIT of nearly $16 billion. If Intel were to increase its debt by $1 billion and

use the cash for a share repurchase, which market imperfections would be most relevant for

understanding the consequence for Intel’s value? Why?

18-4. Backcountry Adventures is a Colorado-based outdoor travel agent that operates a series of

winter backcountry huts. Currently, the value of the firm (debt + equity) is $3.5 million. But

profits will depend on the amount of snowfall: If it is a good year, the firm will be worth $5

million, and if it is a bad year it will be worth $2.5 million. Suppose managers always keep the

debt to equity ratio of the firm at 25%, and the debt is riskless.

a. What is the initial amount of debt?

b. Calculate the percentage change in the value of the firm, its equity and its debt once the level

of snowfall is revealed, but before the firm adjusts the debt level to achieve its target debt to

equity ratio.

c. Calculate the percentage change in the value of outstanding debt once the firm adjusts to its

target debt-equity ratio.

d. What does this imply about the riskiness of the firm’s tax shields? Explain.

18-5. Suppose Goodyear Tire and Rubber Company is considering divesting one of its manufacturing

plants. The plant is expected to generate free cash flows of $1.5 million per year, growing at a

rate of 2.5% per year. Goodyear has an equity cost of capital of 8.5%, a debt cost of capital of

7%, a marginal corporate tax rate of 35%, and a debt-equity ratio of 2.6. If the plant has average

risk and Goodyear plans to maintain a constant debt-equity ratio, what after-tax amount must it

receive for the plant for the divestiture to be profitable?

We can compute the levered value of the plant using the WACC method. Goodyear’s WACC is

18-6. Suppose Alcatel-Lucent has an equity cost of capital of 10%, market capitalization of $10.8

billion, and an enterprise value of $14.4 billion. Suppose Alcatel-Lucent’s debt cost of capital is

6.1% and its marginal tax rate is 35%.

a. What is Alcatel-Lucent’s WACC?

b. If Alcatel-Lucent maintains a constant debt-equity ratio, what is the value of a project with

average risk and the following expected free cash flows?

c. If Alcatel-Lucent maintains its debt-equity ratio, what is the debt capacity of the project in

part b?

18-7. Acort Industries has 10 million shares outstanding and a current share price of $40 per share. It

also has long-term debt outstanding. This debt is risk free, is four years away from maturity, has

annual coupons with a coupon rate of 10%, and has a $100 million face value. The first of the

remaining coupon payments will be due in exactly one year. The riskless interest rates for all

maturities are constant at 6%. Acort has EBIT of $106 million, which is expected to remain

constant each year. New capital expenditures are expected to equal depreciation and equal $13

million per year, while no changes to net working capital are expected in the future. The

corporate tax rate is 40%, and Acort is expected to keep its debt-equity ratio constant in the

future (by either issuing additional new debt or buying back some debt as time goes on).

a. Based on this information, estimate Acort’s WACC.

b. What is Acort’s equity cost of capital?

a. We don’t know Acort’s equity cost of capital, so we cannot calculate WACC directly. However,

18-8. Suppose Goodyear Tire and Rubber Company has an equity cost of capital of 8.5%, a debt cost

of capital of 7%, a marginal corporate tax rate of 35%, and a debt-equity ratio of 2.6. Suppose

Goodyear maintains a constant debt-equity ratio.

a. What is Goodyear’s WACC?

b. What is Goodyear’s unlevered cost of capital?

c. Explain, intuitively, why Goodyear’s unlevered cost of capital is less than its equity cost of

capital and higher than its WACC.

18-9. You are a consultant who was hired to evaluate a new product line for Markum Enterprises. The

upfront investment required to launch the product line is $10 million. The product will generate

free cash flow of $750,000 the first year, and this free cash flow is expected to grow at a rate of

4% per year. Markum has an equity cost of capital of 11.3%, a debt cost of capital of 5%, and a

tax rate of 35%. Markum maintains a debt-equity ratio of 0.40.

a. What is the NPV of the new product line (including any tax shields from leverage)?

b. How much debt will Markum initially take on as a result of launching this product line?

c. How much of the product line’s value is attributable to the present value of interest tax

shields?

Chapter 18/Capital Budgeting and Valuation with Leverage 251

18–10. Consider Alcatel-Lucent’s project in Problem 6.

a. What is Alcatel-Lucent’s unlevered cost of capital?

b. What is the unlevered value of the project?

c. What are the interest tax shields from the project? What is their present value?

d. Show that the APV of Alcatel-Lucent’s project matches the value computed using the

WACC method.

c. Using the results from problem 6(c):

18–11. Consider Alcatel-Lucent’s project in Problem 6.

a. What is the free cash flow to equity for this project?

b. What is its NPV computed using the FTE method? How does it compare with the NPV based

on the WACC method?

a. Using the debt capacity calculated in problem 6, we can compute FCFE by adjusting FCF for

18–12. In year 1, AMC will earn $2000 before interest and taxes. The market expects these earnings to

grow at a rate of 3% per year. The firm will make no net investments (i.e., capital expenditures

will equal depreciation) or changes to net working capital. Assume that the corporate tax rate

equals 40%. Right now, the firm has $5000 in risk-free debt. It plans to keep a constant ratio of

debt to equity every year, so that on average the debt will also grow by 3% per year. Suppose the

risk-free rate equals 5%, and the expected return on the market equals 11%. The asset beta for

this industry is 1.11.

a. If AMC were an all-equity (unlevered) firm, what would its market value be?

b. Assuming the debt is fairly priced, what is the amount of interest AMC will pay next year? If

AMC’s debt is expected to grow by 3% per year, at what rate are its interest payments

expected to grow?

c. Even though AMC’s debt is riskless (the firm will not default), the future growth of AMC’s

debt is uncertain, so the exact amount of the future interest payments is risky. Assuming the

future interest payments have the same beta as AMC’s assets, what is the present value of

AMC’s interest tax shield?

d. Using the APV method, what is AMC’s total market value, V L? What is the market value of

AMC’s equity?

e. What is AMC’s WACC? (Hint: Work backward from the FCF and V L.)

f. Using the WACC method, what is the expected return for AMC equity?

g. Show that the following holds for AMC:

.

A E D

ED

D E D E

=+

++

h. Assuming that the proceeds from any increases in debt are paid out to equity holders, what

cash flows do the equity holders expect to receive in one year? At what rate are those cash

flows expected to grow? Use that information plus your answer to part (f ) to derive the

market value of equity using the FTE method. How does that compare to your answer in

part (d)?

b. Since the debt is risk-free, the interest rate paid on it must equal the risk-free rate of 5% (or else

Chapter 18/Capital Budgeting and Valuation with Leverage 253

d. The APV tells us that the value of a firm with debt equals the sum of the value of an all-equity

e. Next year’s FCF is

$2,000 0.6 $1,200=

. It is expected to grow at 3%, so the WACC must

satisfy:

g. From the CAPM,

E

must satisfy

( )

E

15% 5% 11% 5%= + −

, so we conclude

E1.66=

.

18–13. Prokter and Gramble (PKGR) has historically maintained a debt-equity ratio of approximately

0.20. Its current stock price is $50 per share, with 2.5 billion shares outstanding. The firm enjoys

very stable demand for its products, and consequently it has a low equity beta of 0.50 and can

borrow at 4.20%, just 20 basis points over the risk-free rate of 4%. The expected return of the

market is 10%, and PKGR’s tax rate is 35%.

a. This year, PKGR is expected to have free cash flows of $6.0 billion. What constant expected

growth rate of free cash flow is consistent with its current stock price?

b. PKGR believes it can increase debt without any serious risk of distress or other costs. With a

higher debt-equity ratio of 0.50, it believes its borrowing costs will rise only slightly to

4.50%. If PKGR announces that it will raise its debt-equity ratio to 0.5 through a leveraged

recap, determine the increase in the stock price that would result from the anticipated tax

savings.

254 Berk/DeMarzo, Corporate Finance, Fourth Edition

b. Initial Unlevered cost of capital (Eq. 18.6) = (125 / 150) 7% + (25 / 150) 4.2% = 6.53%

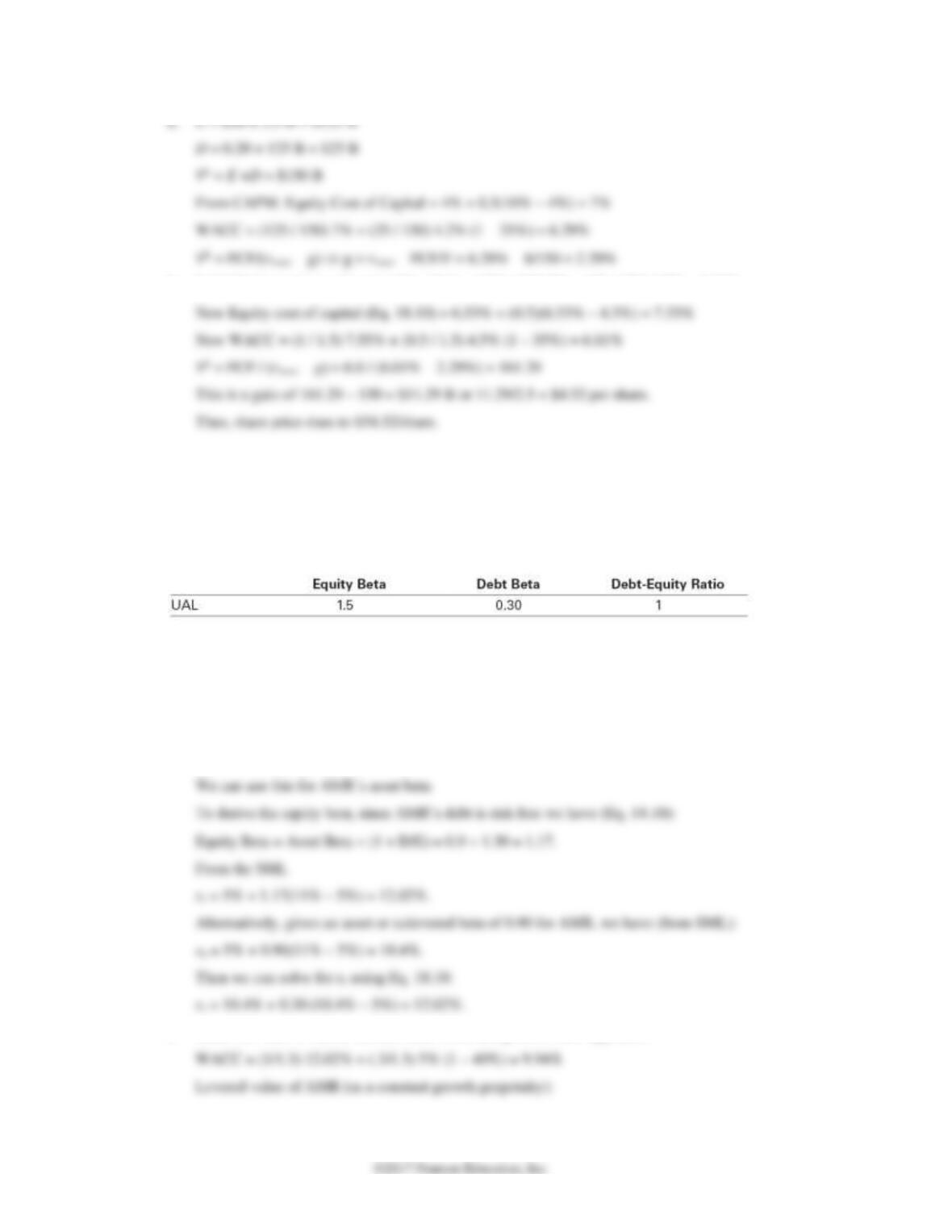

18–14. Amarindo, Inc. (AMR), is a newly public firm with 10 million shares outstanding. You are doing

a valuation analysis of AMR. You estimate its free cash flow in the coming year to be $15 million,

and you expect the firm’s free cash flows to grow by 4% per year in subsequent years. Because

the firm has only been listed on the stock exchange for a short time, you do not have an accurate

assessment of AMR’s equity beta. However, you do have beta data for UAL, another firm in the

same industry:

AMR has a much lower debt-equity ratio of 0.30, which is expected to remain stable, and its debt

is risk free. AMR’s corporate tax rate is 40%, the risk-free rate is 5%, and the expected return

on the market portfolio is 11%.

a. Estimate AMR’s equity cost of capital.

b. Estimate AMR’s share price.

a. From Eq. 14.9, UAL Asset beta = (1/2) 1.5 + (1/2) 0.3 = 0.90

b. Since D/E ratio is stable, we can value AMR using the WACC approach.

Chapter 18/Capital Budgeting and Valuation with Leverage 255

18–15. Remex (RMX) currently has no debt in its capital structure. The beta of its equity is 1.50. For

each year into the indefinite future, Remex’s free cash flow is expected to equal $25 million.

Remex is considering changing its capital structure by issuing debt and using the proceeds to buy

back stock. It will do so in such a way that it will have a 30% debt-equity ratio after the change,

and it will maintain this debt-equity ratio forever. Assume that Remex’s debt cost of capital will

be 6.5%. Remex faces a corporate tax rate of 35%. Except for the corporate tax rate of 35%,

there are no market imperfections. Assume that the CAPM holds, the risk-free rate of interest is

5%, and the expected return on the market is 11%.

a. Using the information provided, complete the following table:

b. Using the information provided and your calculations in part a, determine the value of the

tax shield acquired by Remex if it changes its capital structure in the way it is considering.

a. Before Change: From the SML,

5% 1.50 6% 14%

E

r= + =

b. We can compare Remex’s value with and without leverage. Without leverage (and no expected

growth),

18–16. You are evaluating a project that requires an investment of $90 today and provides a single cash

flow of $115 for sure one year from now. You decide to use 100% debt financing, that is, you will

borrow $90. The risk-free rate is 5% and the tax rate is 40%. Assume that the investment is fully

depreciated at the end of the year, so without leverage you would owe taxes on the difference

between the project cash flow and the investment, that is, $25.

a. Calculate the NPV of this investment opportunity using the APV method.

b. Using your answer to part a, calculate the WACC of the project.

c. Verify that you get the same answer using the WACC method to calculate NPV.

d. Finally, show that flow-to-equity also correctly gives the NPV of this investment opportunity.

a. FCF at year end (after tax) = 115 – 0.40 25 = 105

b. ru = rd = 5%, d = 90/101.71

18–17. Tybo Corporation adjusts its debt so that its interest expenses are 20% of its free cash flow. Tybo

is considering an expansion that will generate free cash flows of $2.5 million this year and is

expected to grow at a rate of 4% per year from then on. Suppose Tybo’s marginal corporate tax

rate is 40%.

a. If the unlevered cost of capital for this expansion is 10%, what is its unlevered value?

b. What is the levered value of the expansion?

c. If Tybo pays 5% interest on its debt, what amount of debt will it take on initially for the

expansion?

d. What is the debt-to-value ratio for this expansion? What is its WACC?

e. What is the levered value of the expansion using the WACC method?

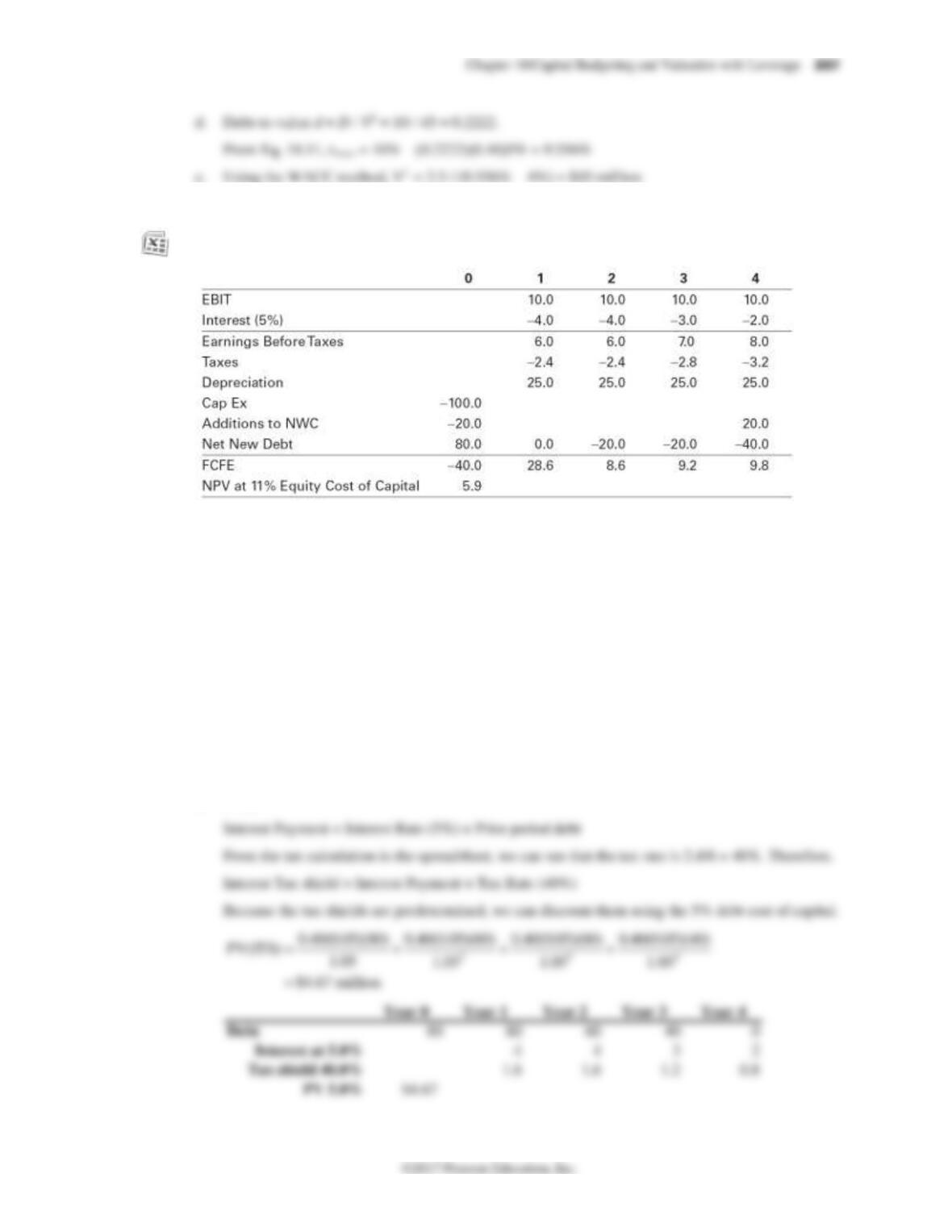

18–18. You are on your way to an important budget meeting. In the elevator, you review the project

valuation analysis you had your summer associate prepare for one of the projects to be

discussed:

Looking over the spreadsheet, you realize that while all of the cash flow estimates are correct,

your associate used the flow-to-equity valuation method and discounted the cash flows using the

company’s equity cost of capital of 11%. While the project’s risk is similar to the firm’s, the

project’s incremental leverage is very different from the company’s historical debt–equity ratio

of 0.20: For this project, the company will instead borrow $80 million upfront and repay $20

million in year 2, $20 million in year 3, and $40 million in year 4. Thus, the project’s equity cost

of capital is likely to be higher than the firm’s, not constant over time—invalidating your

associate’s calculation.

Clearly, the FTE approach is not the best way to analyze this project. Fortunately, you have your

calculator with you, and with any luck you can use a better method before the meeting starts.

a. What is the present value of the interest tax shield associated with this project?

b. What are the free cash flows of the project?

c. What is the best estimate of the project’s value from the information given?

a. First,

258 Berk/DeMarzo, Corporate Finance, Fourth Edition

b. We can use Eq. 7.5:

0 1 2 3 4

EBIT 10 10 10 10

Taxes -4 -4 -4 -4

c. With predetermined debt levels, the APV method is easiest.

18–19. Your firm is considering building a $600 million plant to manufacture HDTV circuitry. You

expect operating profits (EBITDA) of $145 million per year for the next 10 years. The plant will

be depreciated on a straight-line basis over 10 years (assuming no salvage value for tax

purposes). After 10 years, the plant will have a salvage value of $300 million (which, since it will

be fully depreciated, is then taxable). The project requires $50 million in working capital at the

start, which will be recovered in year 10 when the project shuts down. The corporate tax rate is

35%. All cash flows occur at the end of the year.

a. If the risk-free rate is 5%, the expected return of the market is 11%, and the asset beta for

the consumer electronics industry is 1.67, what is the NPV of the project?

b. Suppose that you can finance $400 million of the cost of the plant using 10-year, 9% coupon

bonds sold at par. This amount is incremental new debt associated specifically with this

project and will not alter other aspects of the firm’s capital structure. What is the value of

the project, including the tax shield of the debt?

Chapter 18/Capital Budgeting and Valuation with Leverage 259

Using Eq. 7.6:

b. Because the debt level is predetermined, we can use the APV approach. Because the bonds

initially trade at par, the interest payments are the 9% coupon payments of the bond. Assuming

annual coupons:

18-20. Parnassus Corporation plans to invest $150 million in a new generator that will produce free

cash flows of $20 million per year in perpetuity. The firm is all equity financed, with an equity

cost of capital of 10%.

a. What is the NPV of the project ignoring any costs of raising funds?

b. Suppose the firm will issue new equity to raise the $150 million, and has after-tax issuance

costs equal to 8% of the proceeds. What is the NPV of the project including these issuance

costs, assuming all future free cash flows generated by it will be paid out?

c. Suppose that instead of paying out the project’s future free cash flows, a substantial portion

of these free cash flows will be retained and invested in other projects, reducing Parnassus’

required fundraising in the future. Specifically, suppose the firm will reinvest all free cash

flows for the next 10 years, and then pay out the cash flows after that. If its issuance costs

remain constant at 8%, what is the NPV of the project including issuance costs in this case?

260 Berk/DeMarzo, Corporate Finance, Fourth Edition

18–21. DFS Corporation is currently an all-equity firm, with assets with a market value of $100 million

and 4 million shares outstanding. DFS is considering a leveraged recapitalization to boost its

share price. The firm plans to raise a fixed amount of permanent debt (i.e., the outstanding

principal will remain constant) and use the proceeds to repurchase shares. DFS pays a 35%

corporate tax rate, so one motivation for taking on the debt is to reduce the firm’s tax liability.

However, the upfront investment banking fees associated with the recapitalization will be 5% of

the amount of debt raised. Adding leverage will also create the possibility of future financial

distress or agency costs; shown below are DFS’s estimates for different levels of debt:

a. Based on this information, which level of debt is the best choice for DFS?

b. Estimate the stock price once this transaction is announced.

a. Because the debt is permanent, the value of the tax shield is 35% × D. From that we must deduct

the 5% issuance cost, and the PV of distress and agency costs to determine the net benefit of

leverage.

18–22. Your firm is considering a $150 million investment to launch a new product line. The project is

expected to generate a free cash flow of $20 million per year, and its unlevered cost of capital is

10%. To fund the investment, your firm will take on $100 million in permanent debt.

a. Suppose the marginal corporate tax rate is 35%. Ignoring issuance costs, what is the NPV of

the investment?

b. Suppose your firm will pay a 2% underwriting fee when issuing the debt. It will raise the

remaining $50 million by issuing equity. In addition to the 5% underwriting fee for the

equity issue, you believe that your firm’s current share price of $40 is $5 per share less than

its true value. What is the NPV of the investment including any tax benefits of leverage?

(Assume all fees are on an after-tax basis.)

Chapter 18/Capital Budgeting and Valuation with Leverage 261

18–23. Consider Avco’s RFX project from Section 18.3. Suppose that Avco is receiving government loan

guarantees that allow it to borrow at the 6% rate. Without these guarantees, Avco would pay

6.5% on its debt.

a. What is Avco’s unlevered cost of capital given its true debt cost of capital of 6.5%?

b. What is the unlevered value of the RFX project in this case? What is the present value of the

interest tax shield?

c. What is the NPV of the loan guarantees? (Hint: Because the actual loan amounts will

fluctuate with the value of the project, discount the expected interest savings at the

unlevered cost of capital.)

d. What is the levered value of the RFX project, including the interest tax shield and the NPV

of the loan guarantees?

a. We use Eq. 18.6 with the true debt cost:

c. The loan guarantee reduces the interest paid from 6.5% to 6% each year. Thus, the savings in year

18–24. Arden Corporation is considering an investment in a new project with an unlevered cost of

capital of 9%. Arden’s marginal corporate tax rate is 40%, and its debt cost of capital is 5%.

a. Suppose Arden adjusts its debt continuously to maintain a constant debt-equity ratio of

50%. What is the appropriate WACC for the new project?

b. Suppose Arden adjusts its debt once per year to maintain a constant debt-equity ratio of

50%. What is the appropriate WACC for the new project now?

c. Suppose the project has free cash flows of $10 million per year, which are expected to decline

by 2% per year. What is the value of the project in parts (a) and (b) now?

1.05

Alternatively, from Eq. 18.17:

18–25. XL Sports is expected to generate free cash flows of $10.9 million per year. XL has permanent

debt of $40 million, a tax rate of 40%, and an unlevered cost of capital of 10%.

a. What is the value of XL’s equity using the APV method?

b. What is XL’s WACC? What is XL’s equity value using the WACC method?

c. If XL’s debt cost of capital is 5%, what is XL’s equity cost of capital?

d. What is XL’s equity value using the FTE method?

c. If XL’s debt cost of capital is 5%, what is XL’s equity cost of capital?

From Eq. 18.20:

18–26. Propel Corporation plans to make a $50 million investment, initially funded completely with

debt. The free cash flows of the investment and Propel’s incremental debt from the project

follow:

Chapter 18/Capital Budgeting and Valuation with Leverage 263

Propel’s incremental debt for the project will be paid off according to the predetermined

schedule shown. Propel’s debt cost of capital is 8%, and its tax rate is 40%. Propel also estimates

an unlevered cost of capital for the project of 12%.

a. Use the APV method to determine the levered value of the project at each date and its initial

NPV.

b. Calculate the WACC for this project at each date. How does the WACC change over time?

Why?

c. Compute the project’s NPV using the WACC method.

d. Compute the equity cost of capital for this project at each date. How does the equity cost of

capital change over time? Why?

e. Compute the project’s equity value using the FTE method. How does the initial equity value

compare with the NPV calculated in parts (a) and (c)?

a. Note that this answer actually uses the APV method instead of the WACC method.

Year 0 1 2 3

Year 0 1 2 3

b. We can compute the WACC at each date using Eq. 18.21. The debt–to-value ratio, d, is given by

D/VL. The debt persistence is given by Ts(c D), where Ts =PV(ITS) (since all tax shields are

predetermined):

Year 0 1 2

3

264 Berk/DeMarzo, Corporate Finance, Fourth Edition

c. We can compute the levered value of the project by discounting the FCF using the WACC at each

date:

d. We can compute the project’s equity cost of capital using Eq. 18.20. Note that Ds = D − Ts = D

− PV(ITS):

Year 0 1 2 3

e. We first compute FCFE at each date by deducting the after-tax interest expenses (equivalently,

deducting interest and adding back the tax shield) and adding net increases in debt:

Year 0 1 2 3

Then, we compute the equity value of the project by discounting FCFE using rE at each date:

18–27. Gartner Systems has no debt and an equity cost of capital of 10%. Gartner’s current market

capitalization is $100 million, and its free cash flows are expected to grow at 3% per year.

Gartner’s corporate tax rate is 35%. Investors pay tax rates of 40% on interest income and 20%

on equity income.

a. Suppose Gartner adds $50 million in permanent debt and uses the proceeds to repurchase

shares. What will Gartner’s levered value be in this case?

b. Suppose instead Gartner decides to maintain a 50% debt-to-value ratio going forward. If

Gartner’s debt cost of capital is 6.67%, what will Gartner’s levered value be in this case?

18–28. Revtek, Inc., has an equity cost of capital of 12% and a debt cost of capital of 6%. Revtek

maintains a constant debt-equity ratio of 0.5, and its tax rate is 35%.

a. What is Revtek’s WACC given its current debt-equity ratio?

b. Assuming no personal taxes, how will Revtek’s WACC change if it increases its debt-equity

ratio to 2 and its debt cost of capital remains at 6%?

c. Now suppose investors pay tax rates of 40% on interest income and 15% on income from

equity. How will Revtek’s WACC change if it increases its debt-equity ratio to 2 in this case?

d. Provide an intuitive explanation for the difference in your answers to parts (b) and (c).

266 Berk/DeMarzo, Corporate Finance, Fourth Edition