Chapter 16 CFIN6

Chapter 16 Solutions

16-1 The following table shows the initial forecast and the AFN:

Current Growth Initial Forecast

Total assets $800,000 x 1.20 $960,000

Accounts payable/Accruals $150,000 x 1.20 $180,000

Notes payable 25,000 25,000

AFN $124,000

Sales $250,000 x 1.20 $300,000

Net profit margin 5.0% 5.0%

Net income $ 12,500 $ 15,000

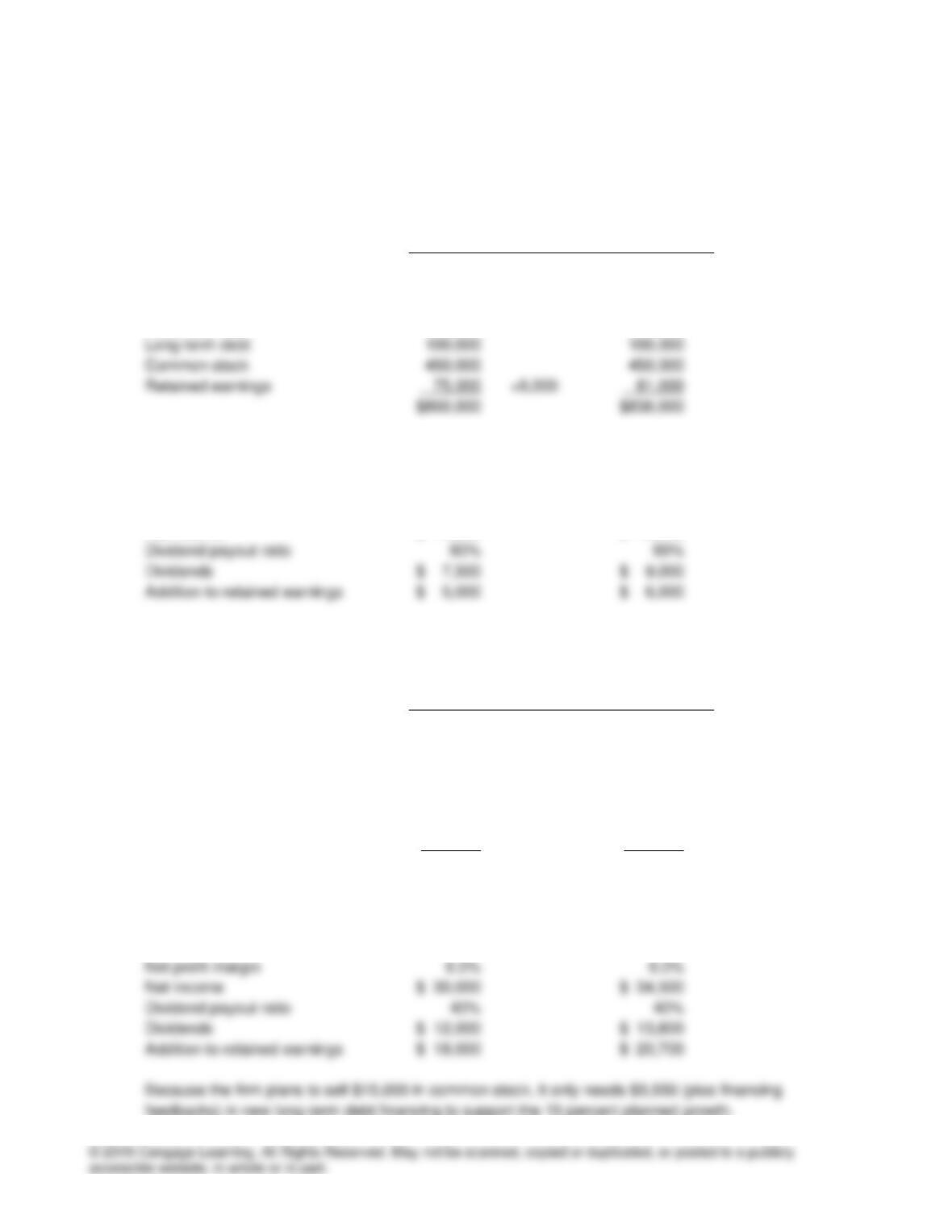

16-2 The following table shows the initial forecast and the AFN:

Current Growth Initial Forecast

Total assets $400,000 x 1.15 $460,000

Accounts payable $125,000 x 1.15 $143,750

Notes payable 0 0

Long-term debt 37,000 37,000

Common stock 140,000 +$15,000 155,000

Retained earnings 98,000 +20,770 118,700

$400,000 $454,450

AFN $ 5,550

Sales $500,000 x 1.15 $575,000

feedbacks) in new long-term debt financing to support the 15 percent planned growth.

Chapter 16 CFIN6

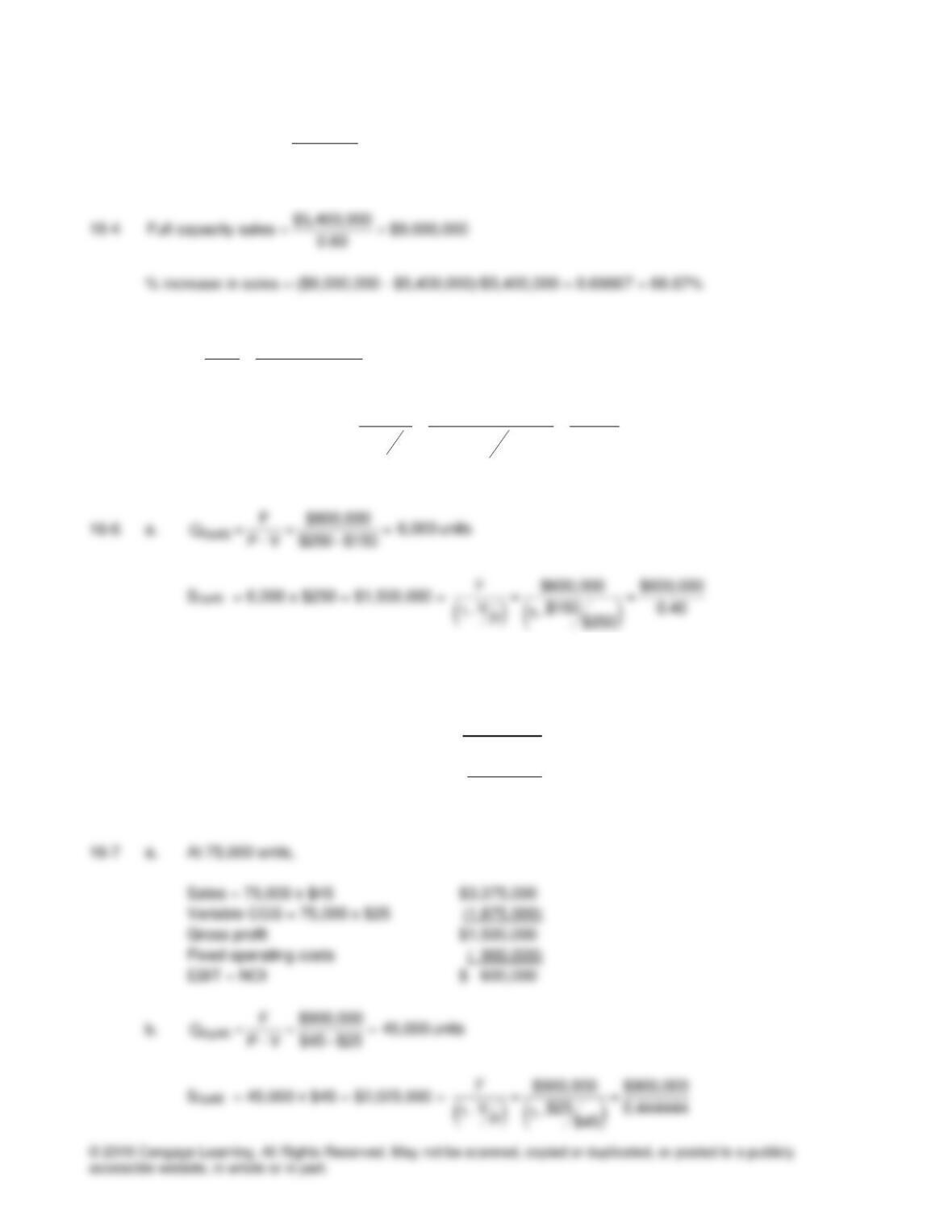

16-3

$810,000

Full capacity sales $900,000

0.90

==

16-5

OpBE F $1,500

= = = 200 units

QP – V $25.00 $17.50−

SOpBE = 200 x $25 = $5,000 =

( )

()

F $1,500 $1,500

= =

$17.50

V0.30

1 – 1

P$25.00

−

b. At 10,000 units,

Sales = 10,000 x $250 $2,500,000

Variable CGS = 10,000 x $150 (1,500,000)

Gross profit $1,000,000

Fixed operating costs ( 600,000)

EBIT = NOI $ 400,000

Chapter 16 CFIN6

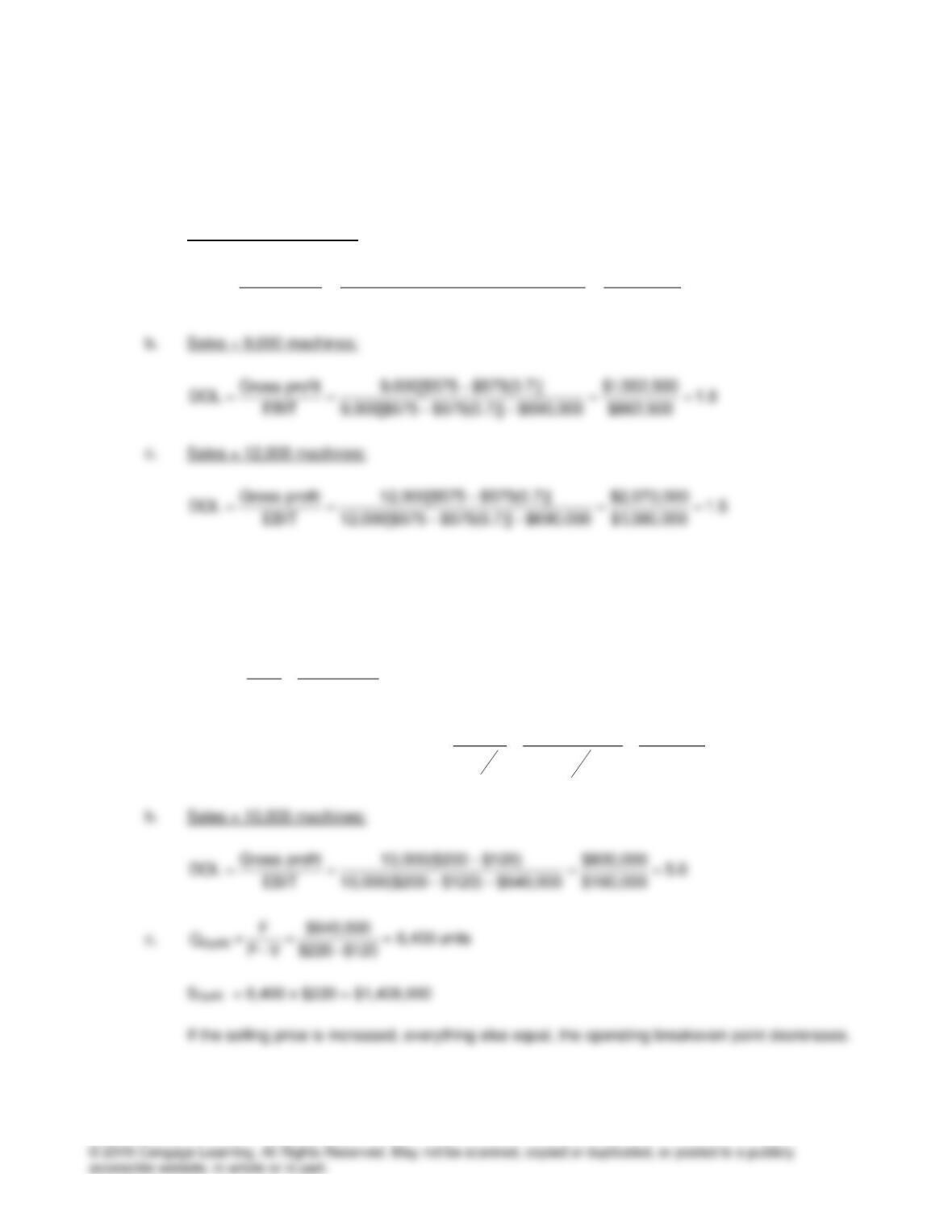

16-8 Selling price = $575

Fixed operating costs = $690,000

Variable operating costs = 70% x Sales

a. Sales = 6,000 machines:

Gross profit 6,000[$575 $575(0.7)] $1,035,000

DOL 3.0

EBIT 6,000[$575 $575(0.7)] $690,000 $345,000

−

= = = =

−−

16-9 Selling price = $200

Fixed operating costs = $640,000

Variable operating costs = $120

a.

OpBE F $640,000

= = = 8,000 units

QP – V $200 $120−

SOpBE = 8,000 x $200 = $1,600,000 =

( )

()

F $640,000 $640,000

= =

$120

V0.40

1 – 1

P$200

−

Chapter 16 CFIN6

16–10 Selling price = $1,400

Fixed operating costs = $420,000

Variable operating costs = 80% of sales

b. ODM: Sales = 2,000 units

=

−

= = = =

−−

Q 2,000 Gross profit 2,000[$1,400 $1,400(0.8)] $560,000

DOL 4.0

EBIT 2,000[$1,400 $1,400(0.8)] $420,000 $140,000

Sales = 2,000 x $1,400 $2,800,000

Variable CGS = 2,000 x ($1,400)(0.8) (2,240,000)

Gross profit $ 560,000

Fixed operating costs ( 420,000)

EBIT = NOI $ 140,000

CWI: Sales = 2,500 units

=

−

= = = =

−−

Q 2,500 Gross profit 2,500[$1,400 $1,400(0.8)] $700,000

EBIT 2,500[$1,400 $1,400(0.8)] $420,000 $280,000

16–11 EBITFinBE = $100,000(0.10) + $240,000(0.08) = $10,000 + $19,200 = $29,200

16–12 Interest = $15,000(0.09) + $48,000(0.06) = $1,350 + $2,880 = $4,230

Chapter 16 CFIN6

16–13 a. EBIT $99,000

Interest (33,000) = $300,000 x 0.11

Earnings before taxes (EBT) $66,000

Taxes (30%) (19,800)

Net Income $46,200

EBIT $99,000

DFL 1.5

EBT $66,000

= = =

( )

( )

$18,480

Dps 1 0.30

1T

EBIT $99,000 $99,000

DFL 2.5

$39,600

$99,000 $33,000

EBIT I −

−

= = = =

−−

−+

16–14 Net income = $46,800

Marginal tax rate = 35%

Interest = $36,000

16–15 EBIT = $2,250

Marginal tax rate = 40%

Interest = $1,000

Shares of common stock = 500

Chapter 16 CFIN6

16–16 DOL = 3.5

DFL = 2.0

a. DTL = DOL x DFL = 3.5 x 2.0 = 7.0

16–17 DFL = 4.0

DTL = 10.0

Sales = $600,000

Profit margin = 8%

a. DTL = DOL x DFL

DOL = 10.0/4.0 = 2.5

16–18 Sales = $400,000

EBIT = $125,000

DOL = 2.0

Actual EBIT = $125,000[1 + (-0.10)(2.0)] = $125,000(0.80) = $100,000

DTL = DOL x DFL = 2.0 x 4.0 = 8.0

Actual EPS = $2.50[1 + (-0.10)(8.0)] = $2.50(0.20) = $0.50

16–19 Selling price = $180

Variable cost per unit = $135

Chapter 16 CFIN6

Marginal tax rate = 40%

Sales = 11,000

Gross profit 11,000[$180 $135] $495,000

DOL 4.0

EBIT 11,000($180 $135) $371,250 $123,750

−

= = = =

−−

16–20 Selling price = $10

Variable cost per unit = 75% of selling price = $10(0.75) = $7.50

Fixed operating costs = $100,000

Interest = $37,500

Marginal tax rate = 35%

Sales = 65,000

b.

Gross profit 65,000($10.00 $7.50) $162,500

DOL 2.6

EBIT 65,000($10.00 $7.50) $100,000 $62,500

−

= = = =

−−

EBIT 65,000($10.00 $7.50) $100,000 $62,500

DFL 2.5

EBT 65,000($10.00 $7.50) $100,00 $37,500 $25,000

−−

= = = =

− − −