3. Quick ratio = $400,000/$1,500,000 = 0.27.

The quick ratio indicates that current assets, excluding inventory, are only sufficient

to cover 27% of current liabilities, which is very bad.

Answers and Solutions: 16 – 16

SPREADSHEET PROBLEM

16-18 The detailed solution for the spreadsheet problem, Ch16 P18 Build a Model

Solution.xlsx, is available on the textbook’s Web site.

Mini Case: 16 – 17

MINI CASE

Karen Johnson, CFO for Raucous Roasters (RR), a specialty coffee manufacturer, is

rethinking her company’s working capital policy in light of a recent scare she faced when

RR’s corporate banker, citing a nationwide credit crunch, balked at renewing RR’s line of

credit. Had the line of credit not been renewed, RR would not have been able to make payroll,

potentially forcing the company out of business. Although the line of credit was ultimately

renewed, the scare has forced Johnson to examine carefully each component of RR’s working

capital to make sure it is needed, with the goal of determining whether the line of credit can

be eliminated entirely. In addition to (possibly) freeing RR from the need for a line of credit,

Johnson is well aware that reducing working capital will improve free cash flow.

Historically, RR has done little to examine working capital, mainly because of poor

communication among business functions. In the past, the production manager resisted

Johnson’s efforts to question his holdings of raw materials, the marketing manager resisted

questions about finished goods, the sales staff resisted questions about credit policy (which

affects accounts receivable), and the treasurer did not want to talk about the cash and

securities balances. However, with the recent credit scare, this resistance became

unacceptable and Johnson has undertaken a company-wide examination of cash, marketable

securities, inventory, and accounts receivable levels.

Mini Case: 16 – 18

Johnson also knows that decisions about working capital cannot be made in a

vacuum. For example, if inventories could be lowered without adversely affecting operations,

then less capital would be required, and free cash flow would increase. However, lower raw

materials inventories might lead to production slowdowns and higher costs, and lower

finished goods inventories might lead to stock-outs and loss of sales. So, before inventories

are changed, it will be necessary to study operating as well as financial effects. The situation

is the same with regard to cash and receivables. Johnson has begun her investigation by

collecting the ratios shown below.

RR

Industry

Current

1.75

2.25

Quick

0.92

1.16

Total liabilities/assets

Turnover of cash and securities

Days sales outstanding (365-day basis)

Inventory turnover

Fixed assets turnover

7.75

Total assets turnover

2.60

3.00

Profit margin on sales

2.07%

3.50%

Return on equity (ROE)

Payables deferral period

a. Johnson plans to use the preceding ratios as the starting point for discussions with

RR’s operating team. Based on the data, does RR seem to be following a relaxed,

moderate, or restricted current asset usage policy?

Answer: A company with a relaxed current asset usage policy would carry relatively large

amounts of current assets relative to sales. It would be guarding against running out of

Mini Case: 16 – 19

b. How can one distinguish between a relaxed but rational working capital policy

and a situation in which a firm simply has excessive current assets because it is

inefficient? Does RR’s working capital policy seem appropriate?

Answer: RR may choose to hold large amounts of inventory to avoid the costs of “running

short,” and to cater to customers who expect to receive their coffee immediately. RR

c. Calculate the firm’s cash conversion cycle given annual sales are $660,000 and

cost of goods represent 80% of sales. Assume a 365-day year.

Answer: A firm’s cash conversion cycle is calculated as:

Mini Case: 16 – 20

d. Is there any reason to think that RR may be holding too much inventory?

Answer: As pointed out in part a, RR’s inventory turnover (10.8) is considerably lower than the

e. If RR reduces its inventory without adversely affecting sales, what effect should

this have on free cash flow: (1) in the short run and (2) in the long run?

Answer: A one-time reduction in inventory causes an identical one-time increase in free cash

f. Johnson knows that RR sells on the same credit terms as other firms in its

industry. Use the ratios presented earlier to explain whether RR’s customers pay

more or less promptly than those of its competitors. If there are differences, does

that suggest RR should tighten or loosen its credit policy? What four variables

make up a firm’s credit policy, and in what direction should each be changed by

RR?

Answer: RR’s DSO is 45.63 days as compared with 32 days for the average firm in its industry.

This suggests that RR’s customers are paying less promptly than those of its

Mini Case: 16 – 21

g. Does RR face any risks if it tightens its credit policy?

Answer: A tighter credit policy may discourage sales. Some customers may choose to go

h. If the company reduces its DSO without seriously affecting sales, what effect

would this have on its free cash flow (1) in the short run and (2) in the long run?

Answer: Similar to the situation with inventory, a one-time reduction in DSO causes an identical

Mini Case: 16 – 22

i. What is the impact of higher levels of accruals, such as accrued wages or accrued

taxes? Is it likely that RR could make changes to accruals?

Answer: Higher levels of accruals increase free cash flow. No, RR could not make greater use

j. Assume that RR purchases $200,000 (net of discounts) of materials on terms of

1/10, net 30, but that it can get away with paying on the 40th day if it chooses not

to take discounts. How much free trade credit can the company get from its

equipment supplier, how much costly trade credit can it get, and what is the

percentage cost of the costly credit? Should RR take discounts?

Answer: If RR’s net purchases are $200,000 annually, then, with a 1% discount, its gross

purchases are $200,000/0.99 = $202,020. Net daily purchases from this supplier are

Mini Case: 16 – 23

k. Cash doesn’t earn interest, so why would a company have a positive target cash

balance?

Answer: 1. Transactions balances. A company must have some cash to pay current bills.

2. Precautionary balances (i.e.,“Safety stock”) to handle unexpected needs. These

balances can be low if a company has credit line or other holdings of short-term

securities.

Mini Case: 16 – 24

l. What might RR do to reduce its target cash balance without harming operations?

Answer: 1. Synchronize cash inflows and outflows.

m. RR tries to match the maturity of its assets and liabilities. Describe how RR could

adopt either a more aggressive or more conservative financing policy.

Answer: There are three alternative current asset financing policies: aggressive, moderate, and

relaxed. A moderate financing policy matches asset and liability maturities. (Of course

exact maturity matching is not possible because of (1) the uncertainty of asset lives and

Mini Case: 16 – 25

n. What are the advantages and disadvantages of using short-term debt as a source

of financing?

Answer: Although using short-term credit is generally riskier than using long-term credit, short-

term credit does have some significant advantages. A short-term loan can be obtained

much faster than long-term credit. Lenders insist on a more thorough financial

o. Would it be feasible for RR to finance with commercial paper?

Answer: It would not be feasible for RR to finance with commercial paper. Commercial paper

is unsecured, short-term debt issued by large, financially strong firms and sold

Mini Case: 16 – 26

p. In an attempt to better understand RR’s cash position, Johnson developed a cash

budget. Data for the first 2 months of the year are shown below. (Note that

Johnson’s preliminary cash budget does not account for interest income or

interest expense.) She has the figures for the other months, but they are not

shown. After looking at the cash budget, answer the following questions.

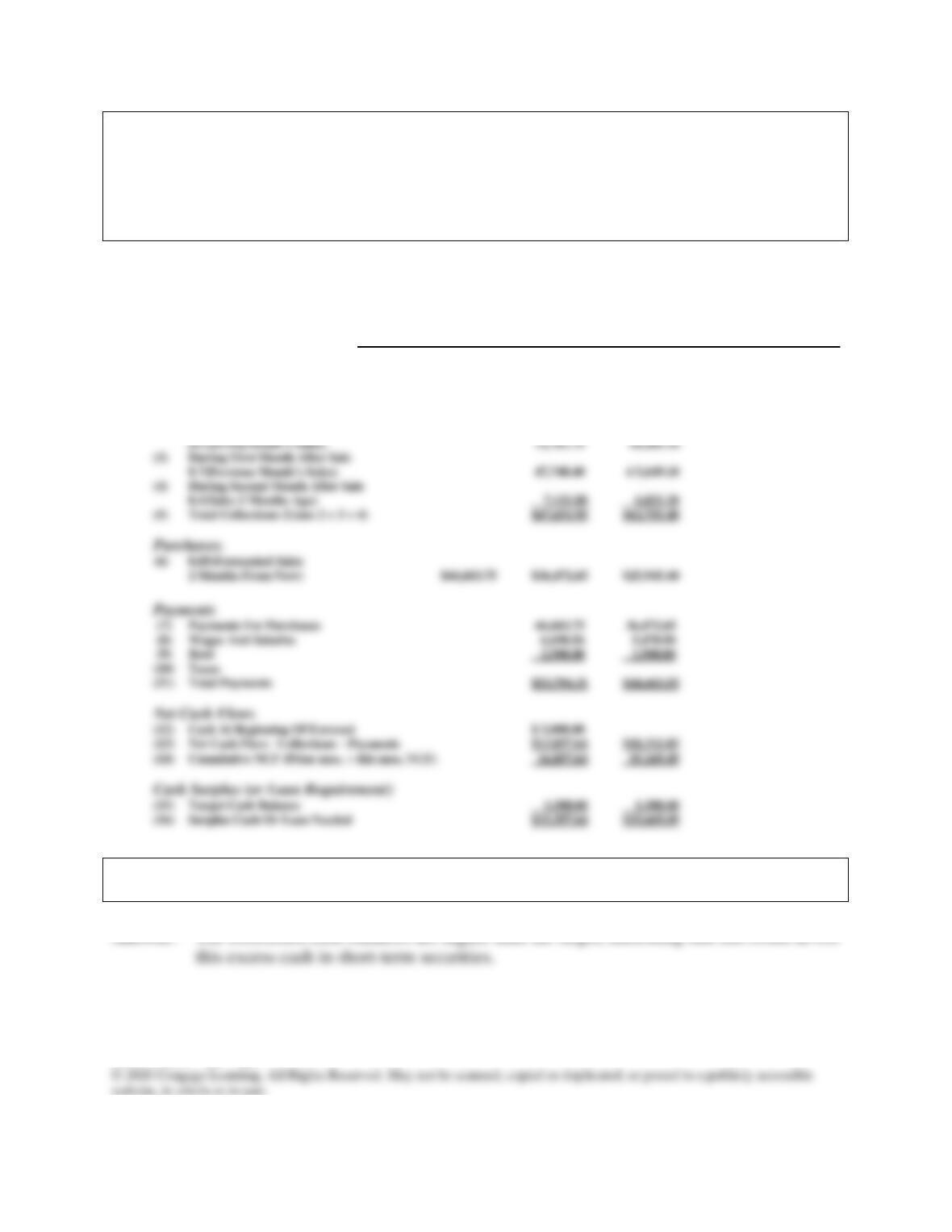

RR’S CASH BUDGET FOR JANUARY AND FEBRUARY

November December January February March April

Sales

(1) Sales (Gross) $71,218 $68,212.00 $65,213.00 $52,475.00 $42,909 $30,524

Collections:

(2) During Month Of Sale

e. 1. What does the cash budget show regarding the target cash level?

Answer: The forecasted cash balances are higher than the target, indicating that RR could invest

Mini Case: 16 – 27

e. 2. Should depreciation expense be explicitly included in the cash budget? Why or

why not?

Answer: No, depreciation expense is a noncash charge and should not appear explicitly in the

e. 3. What are some other potential cash inflows besides collections?

Answer: 1. Proceeds from fixed asset sales.

e. 4. How can interest earned or paid on short-term securities or loans be incorporated

in the cash budget?

Answer: 1. Interest earned: Add line in the collections section.

e. 5. In her preliminary cash budget, Johnson has assumed that all sales are collected

and thus that RR has no bad debts. Is this realistic? If not, how would bad debts

be dealt with in a cash budgeting sense? (Hint: Bad debts will affect collections

but not purchases.)

Answer: It is not realistic to assume zero bad debts. When credit is granted, bad debts should