Days sales outstanding (365-day basis) 45.63 32.00

Inventory turnover 10.80 20.00

Fixed assets turnover 7.75 13.22

Total assets turnover 2.60 3.00

Profit margin on sales 2.07% 3.50%

Return on equity (ROE) 10.45% 21.00%

Payables deferral period 30.00 33.00

1

2

3

4

5

6

7

8

9

10

11

12

21

22

23

28

29

30

31

32

33

34

42

A B C D E F G H I J

11/23/2018

RR Industry

Current 1.75 2.25

Quick 0.92 1.16

TL/assets 58.76% 50.00%

Turnover of cash 16.67 22.22

Karen Johnson, CFO for Raucous Roasters (RR), a specialty coffee manufacturer, is rethinking her company’s working capital

policy in light of a recent scare she faced when RR’s corporate banker, citing a nationwide credit crunch, balked at renewing RR’s

line of credit. Had the line of credit not been renewed, RR would not have been able to make payroll, potentially forcing the

company out of business. Although the line of credit was ultimately renewed, the scare has forced Johnson to examine carefully

each component of RR’s working capital to make sure it is needed, with the goal of determining whether the line of credit can be

eliminated entirely. In addition to (possibly) freeing RR from the need for a line of credit, Johnson is well aware that reducing

working capital will improve free cash flow.

Chapter 16. Mini Case for Supply Chains and Working Capital Management

Johnson also knows that decisions about working capital cannot be made in a vacuum. For example, if inventories could be

lowered without adversely affecting operations, then less capital would be required, and free cash flow would increase. However,

1 of 4

Inventory conversion period

43

44

48

49

50

51

52

53

54

65

66

67

68

69

70

71

g. Does RR face any risks if it tightens its credit policy? See Ch16 Mini Case Show.

changed by RR? See Ch16 Mini Case Show.

80

81

82

83

84

85

86

A B C D E F G H I J

=Inventory / Daily COGS

=$55,000 / $1,627.40

d. Is there any reason to think that RR may be holding too much inventory? See Ch16 Mini Case Show.

Inventory conversion period

Inventory conversion period

e. If RR reduces its inventory without adversely affecting sales, what effect should this have on free cash flow: (1) in the short run

and (2) in the long run? See Ch16 Mini Case Show.

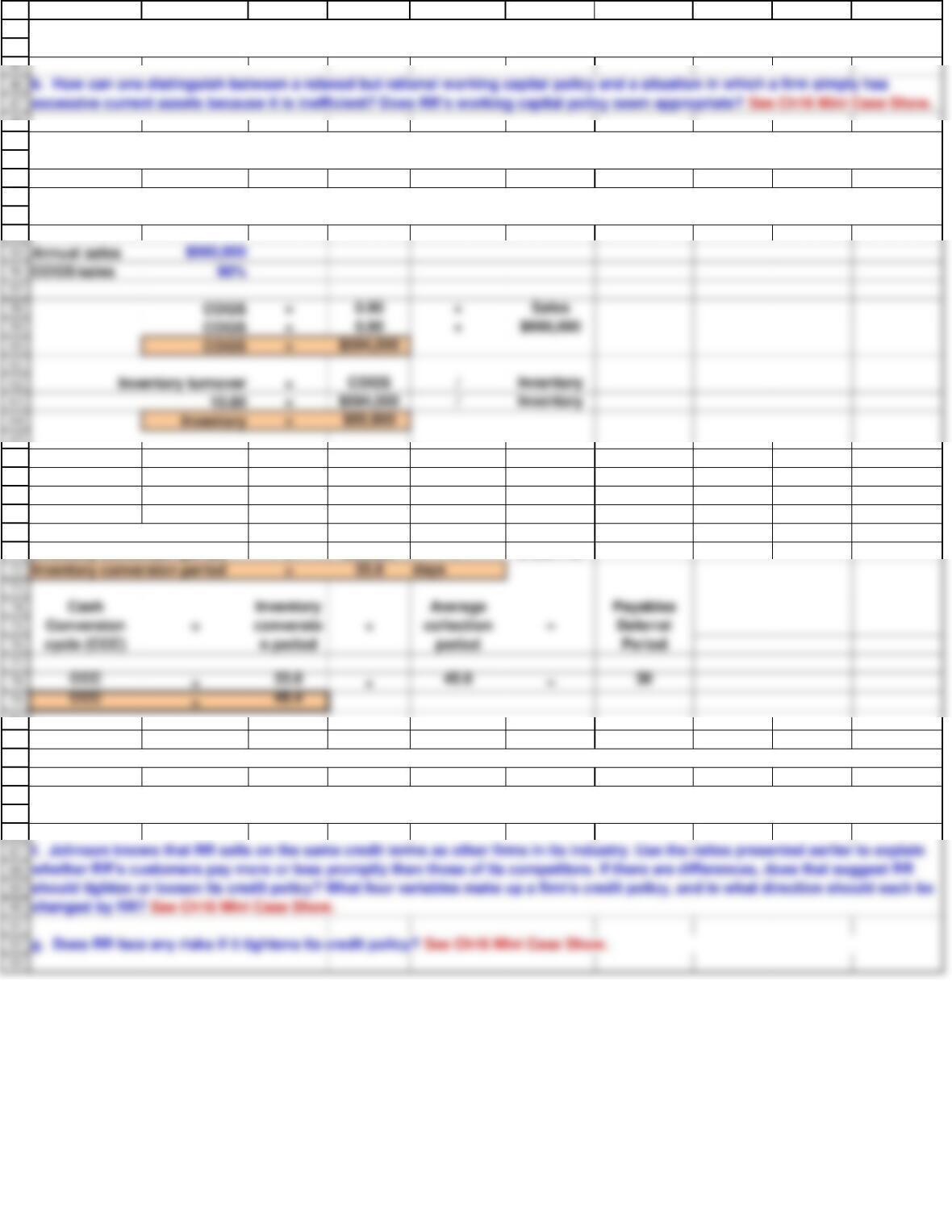

c. Calculate the firm’s cash conversion cycle given annual sales are $660,000 and cost of goods sold are 90% of sales. Assume a

365-day year.

First, determine the amount of inventory from the firm’s inventory turnover ratio. Then, calculate the inventory conversion period

from the data given in the problem.

a. Johnson plans to use the preceding ratios as the starting point for discussions with RR’s operating team. Based on the data,

does RR seem to be following a relaxed, moderate, or restricted current asset usage policy? See Ch16 Mini Case Show.

2 of 4

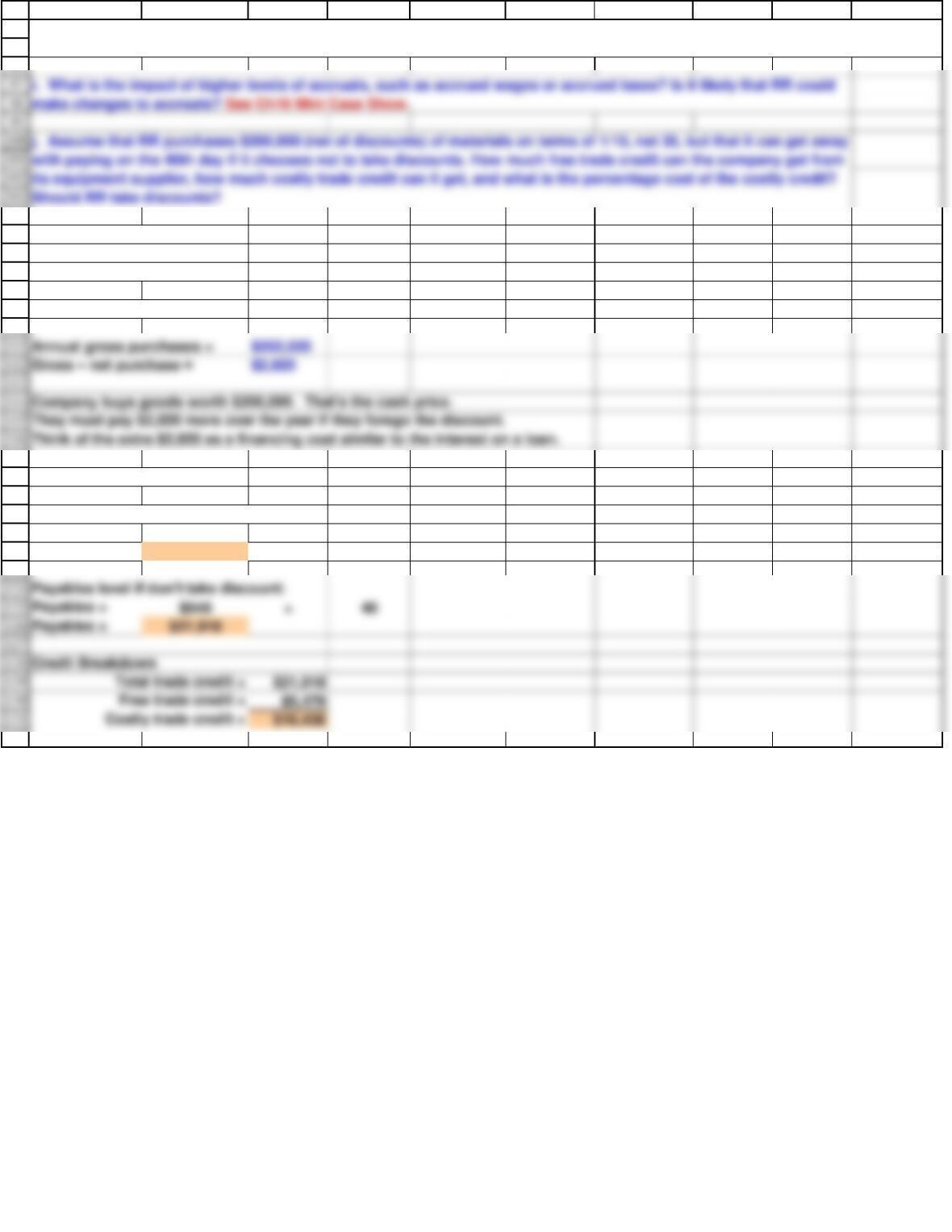

Annual gross purchases = $202,020

They must pay $2,020 more over the year if they forego the discount.

Think of the extra $2,020 as a financing cost similar to the interest on a loan.

Payables = $548 ×40

Payables = $21,918

Credit Breakdown

94

95

104

105

106

107

108

109

110

117

118

119

120

121

122

123

132

A B C D E F G H I J

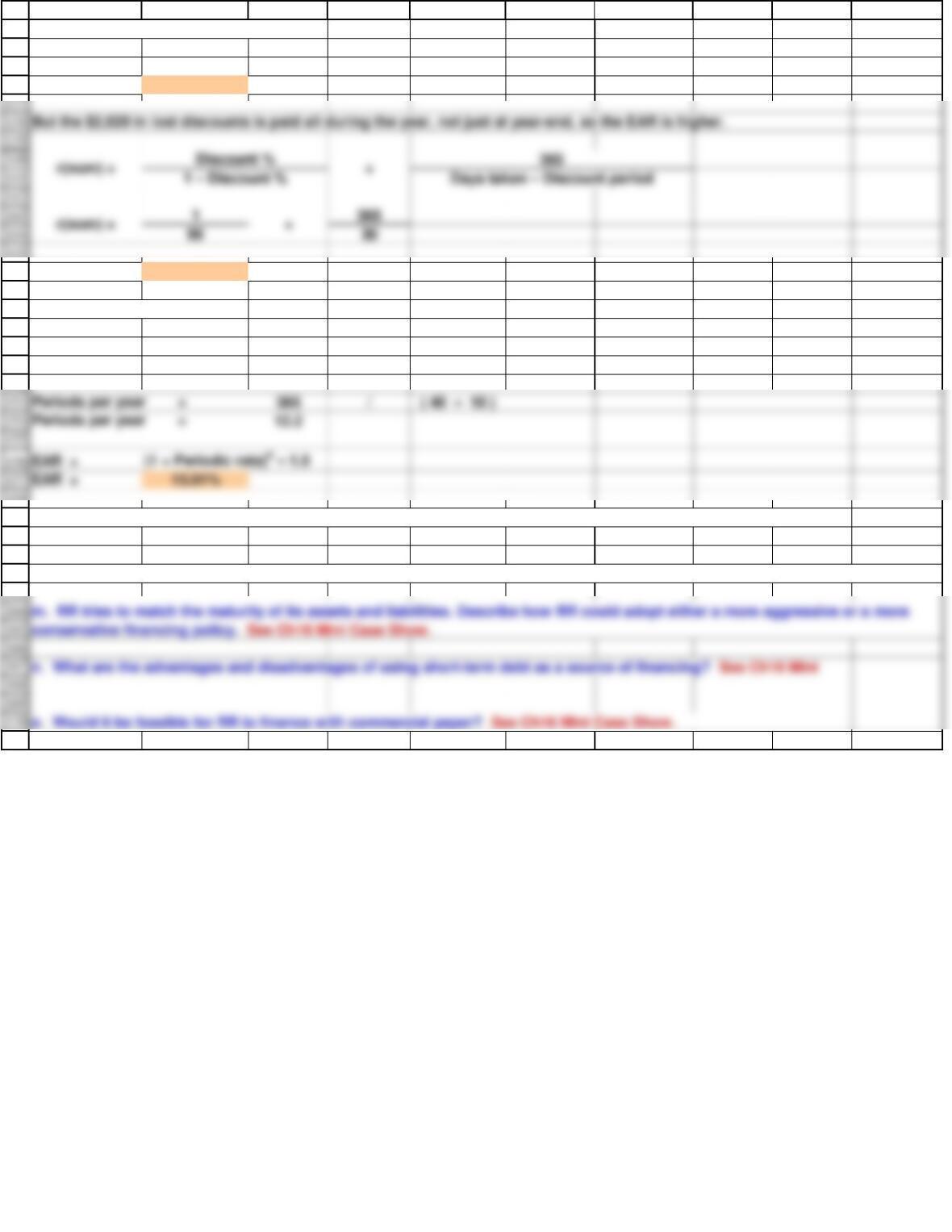

Terms: free credit period = 10 days.

“Official” credit period = 30 days.

Credit period taken = 40

Discount = 1%

Annual net purchases = $200,000

Net daily purchases = $548

Payables level if discount is taken:

Payables = $548 ×10

Payables = $5,479

h. If the company reduces its DSO without seriously affecting sales, what effect would this have on its free cash flows: (1) in the

short run and (2) in the long run? See Ch16 Mini Case Show.

3 of 4

i. What is the impact of higher levels of accruals, such as accrued wages or accrued taxes? Is it likely that RR could

EAR = 13.01%

167

o. Would it be feasible for RR to finance with commercial paper? See Ch16 Mini Case Show.

133

134

135

136

146

147

148

149

150

151

152

158

159

160

161

162

171

A B C D E F G H I J

Nominal cost of costly trade credit:

r(nom) = $2,020 / $16,438

r(nom) = 12.29%

r(nom) = 12.29%

Effective Annual Rate

Periodic rate = 1% /99%

Periodic rate = 1.01%

k. Cash doesn’t earn interest, so why would a company have a positive target cash balance? See Ch16 Mini Case

l. What might RR do to reduce its target cash balance without harming operations? See Ch16 Mini Case Show.

4 of 4