219

Chapter 16

Financial Distress, Managerial Incentives,

and Information

16–1. Gladstone Corporation is about to launch a new product. Depending on the success of the new

product, Gladstone may have one of four values next year: $150 million, $135 million, $95

million, or $80 million. These outcomes are all equally likely, and this risk is diversifiable.

Gladstone will not make any payouts to investors during the year. Suppose the risk-free interest

rate is 5% and assume perfect capital markets.

a. What is the initial value of Gladstone’s equity without leverage?

Now suppose Gladstone has zero-coupon debt with a $100 million face value due next year.

b. What is the initial value of Gladstone’s debt?

c. What is the yield-to-maturity of the debt? What is its expected return?

d. What is the initial value of Gladstone’s equity? What is Gladstone’s total value with

leverage?

16–2. Baruk Industries has no cash and a debt obligation of $36 million that is now due. The market

value of Baruk’s assets is $81 million, and the firm has no other liabilities. Assume perfect capital

markets.

a. Suppose Baruk has 10 million shares outstanding. What is Baruk’s current share price?

b. How many new shares must Baruk issue to raise the capital needed to pay its debt

obligation?

c. After repaying the debt, what will Baruk’s share price be?

220 Berk/DeMarzo, Corporate Finance, Fourth Edition

16–3. When a firm defaults on its debt, debt holders often receive less than 50% of the amount they are

owed. Is the difference between the amount debt holders are owed and the amount they receive a

cost of bankruptcy?

16–4. Which type of firm is more likely to experience a loss of customers in the event of financial

distress:

a. Campbell Soup Company or Intuit, Inc. (a maker of accounting software)?

b. Allstate Corporation (an insurance company) or Adidas AG (maker of athletic footwear,

apparel, and sports equipment)?

16–5. Which type of asset is more likely to be liquidated for close to its full market value in the event of

financial distress:

a. An office building or a brand name?

b. Product inventory or raw materials?

c. Patent rights or engineering “know–how”?

16–6. Suppose Tefco Corp. has a value of $100 million if it continues to operate, but has outstanding

debt of $120 million that is now due. If the firm declares bankruptcy, bankruptcy costs will equal

$20 million, and the remaining $80 million will go to creditors. Instead of declaring bankruptcy,

management proposes to exchange the firm’s debt for a fraction of its equity in a workout. What

is the minimum fraction of the firm’s equity that management would need to offer to creditors

for the workout to be successful?

16–7. You have received two job offers. Firm A offers to pay you $85,000 per year for two years. Firm

B offers to pay you $90,000 for two years. Both jobs are equivalent. Suppose that firm A’s

contract is certain, but that firm B has a 50% chance of going bankrupt at the end of the year. In

that event, it will cancel your contract and pay you the lowest amount possible for you to not

quit. If you did quit, you expect you could find a new job paying $85,000 per year, but you would

be unemployed for 3 months while you search for it.

a. Say you took the job at firm B. What is the least firm B can pay you next year in order to

match what you would earn if you quit?

Chapter 16/Financial Distress, Managerial Incentives, and Information 221

b. Given your answer to part (b), and assuming your cost of capital is 5%, which offer pays you

a higher present value of your expected wage?

c. Based on this example, discuss one reason why firms with a higher risk of bankruptcy may

need to offer higher wages to attract employees.

16–8. As in Problem 1, Gladstone Corporation is about to launch a new product. Depending on the

success of the new product, Gladstone may have one of four values next year: $150 million, $135

million, $95 million, or $80 million. These outcomes are all equally likely, and this risk is

diversifiable. Suppose the risk-free interest rate is 5% and that, in the event of default, 25% of

the value of Gladstone’s assets will be lost to bankruptcy costs. (Ignore all other market

imperfections, such as taxes.)

a. What is the initial value of Gladstone’s equity without leverage?

Now suppose Gladstone has zero-coupon debt with a $100 million face value due next year.

b. What is the initial value of Gladstone’s debt?

c. What is the yield-to-maturity of the debt? What is its expected return?

d. What is the initial value of Gladstone’s equity? What is Gladstone’s total value with

leverage?

Suppose Gladstone has 10 million shares outstanding and no debt at the start of the year.

e. If Gladstone does not issue debt, what is its share price?

f. If Gladstone issues debt of $100 million due next year and uses the proceeds to repurchase

shares, what will its share price be? Why does your answer differ from that in part (e)?

16–9. Kohwe Corporation plans to issue equity to raise $50 million to finance a new investment. After

making the investment, Kohwe expects to earn free cash flows of $10 million each year. Kohwe

currently has 5 million shares outstanding, and it has no other assets or opportunities. Suppose

the appropriate discount rate for Kohwe’s future free cash flows is 8%, and the only capital

market imperfections are corporate taxes and financial distress costs.

a. What is the NPV of Kohwe’s investment?

b. What is Kohwe’s share price today?

Suppose Kohwe borrows the $50 million instead. The firm will pay interest only on this loan each

year, and it will maintain an outstanding balance of $50 million on the loan. Suppose that

Kohwe’s corporate tax rate is 40%, and expected free cash flows are still $10 million each year.

c. What is Kohwe’s share price today if the investment is financed with debt?

Now suppose that with leverage, Kohwe’s expected free cash flows will decline to $9 million per

year due to reduced sales and other financial distress costs. Assume that the appropriate

discount rate for Kohwe’s future free cash flows is still 8%.

d. What is Kohwe’s share price today given the financial distress costs of leverage?

16-10. You work for a large car manufacturer that is currently financially healthy. Your manager feels

that the firm should take on more debt because it can thereby reduce the expense of car

warranties. To quote your manager, “If we go bankrupt, we don’t have to service the warranties.

We therefore have lower bankruptcy costs than most corporations, so we should use more debt.”

Is he right?

16-11. Facebook, Inc. has no debt. As Problem 21 in Chapter 15 makes clear, by issuing debt Facebook

can generate a very large tax shield potentially worth nearly $2 billion. Given Facebook’s

success, one would be hard pressed to argue that Facebook’s management are naïve and

unaware of this huge potential to create value. A more likely explanation is that issuing debt

would entail other costs. What might these costs be?

16-12. Hawar International is a shipping firm with a current share price of $5.50 and 10 million shares

outstanding. Suppose Hawar announces plans to lower its corporate taxes by borrowing $20

million and repurchasing shares.

a. With perfect capital markets, what will the share price be after this announcement?

Suppose that Hawar pays a corporate tax rate of 30%, and that shareholders expect the change

in debt to be permanent.

b. If the only imperfection is corporate taxes, what will the share price be after this

announcement?

c. Suppose the only imperfections are corporate taxes and financial distress costs. If the share

price rises to $5.75 after this announcement, what is the PV of financial distress costs Hawar

will incur as the result of this new debt?

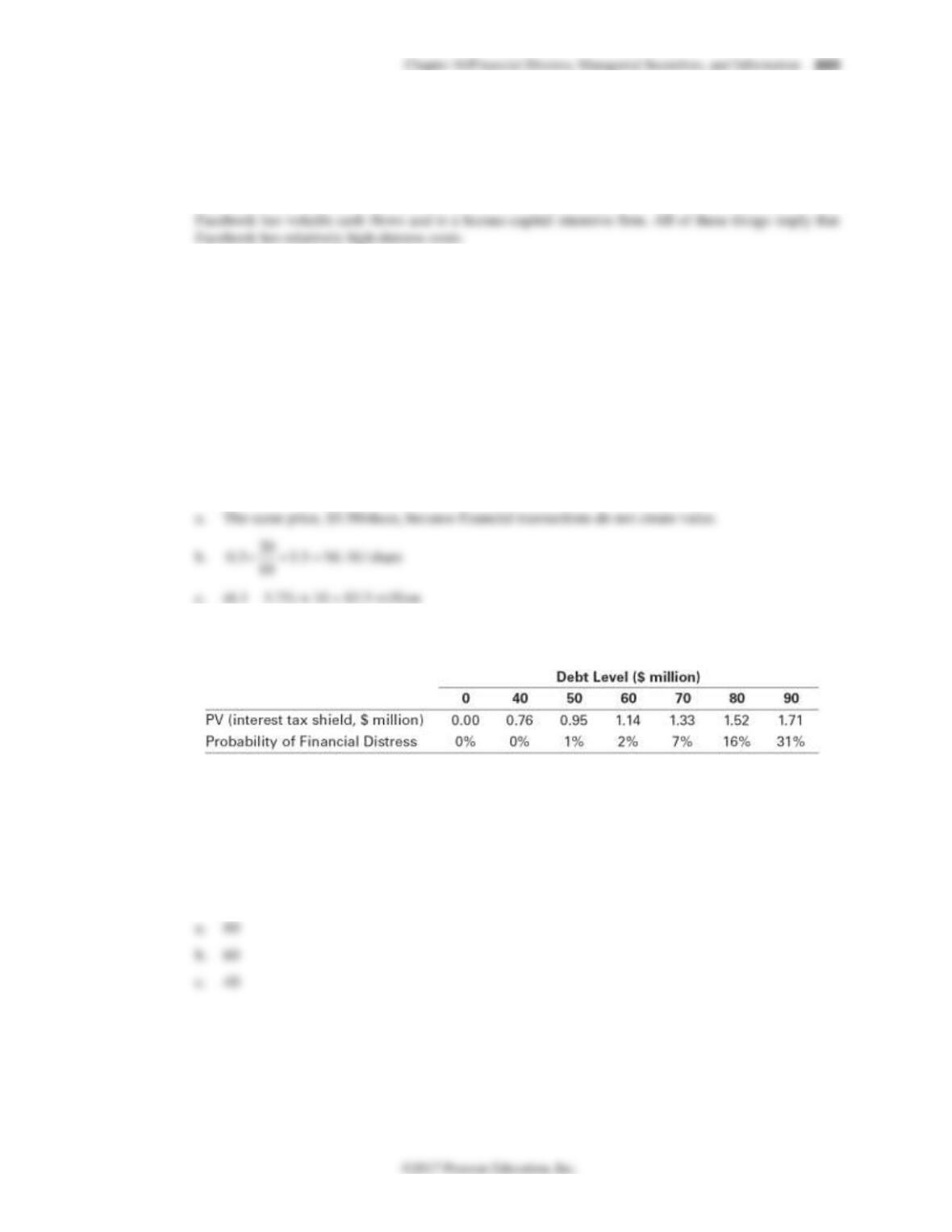

16-13. Your firm is considering issuing one-year debt, and has come up with the following estimates of

the value of the interest tax shield and the probability of distress for different levels of debt:

Suppose the firm has a beta of zero, so that the appropriate discount rate for financial distress

costs is the risk-free rate of 5%. Which level of debt above is optimal if, in the event of distress,

the firm will have distress costs equal to

a. $2 million?

b. $5 million?

c. $25 million?

224 Berk/DeMarzo, Corporate Finance, Fourth Edition

Tax

040 50 60 70 80 90 40%

PV(interest tax shield) 0.00 0.76 0.95 1.14 1.33 1.52 1.71 Vol

Prob(Financial Distress) 0% 0% 1% 2% 7% 16% 31% 20%

Debt Level ($ million)

16-14. Marpor Industries has no debt and expects to generate free cash flows of $16 million each year.

Marpor believes that if it permanently increases its level of debt to $40 million, the risk of

financial distress may cause it to lose some customers and receive less favorable terms from its

suppliers. As a result, Marpor’s expected free cash flows with debt will be only $15 million per

year. Suppose Marpor’s tax rate is 35%, the risk-free rate is 5%, the expected return of the

market is 15%, and the beta of Marpor’s free cash flows is 1.10 (with or without leverage).

a. Estimate Marpor’s value without leverage.

b. Estimate Marpor’s value with the new leverage.

16-15. Real estate purchases are often financed with at least 80% debt. Most corporations, however,

have less than 50% debt financing. Provide an explanation for this difference using the tradeoff

theory.

16-16. On May 14, 2008, General Motors paid a dividend of $0.25 per share. During the same quarter

GM lost a staggering $15.5 billion or $27.33 per share. Seven months later the company asked for

billions of dollars of government aid and ultimately declared bankruptcy just over a year later,

on June 1, 2009. At that point a share of GM was worth only a little more than a dollar.

a. If you ignore the possibility of a government bailout, the decision to pay a dividend given

how close the company was to financial distress is an example of what kind of cost?

b. What would your answer be if GM executives anticipated that there was a possibility of a

government bailout should the firm be forced to declare bankruptcy?

16-17. Dynron Corporation’s primary business is natural gas transportation using its vast gas pipeline

network. Dynron’s assets currently have a market value of $150 million. The firm is exploring

the possibility of raising $50 million by selling part of its pipeline network and investing the $50

million in a fiber-optic network to generate revenues by selling high-speed network bandwidth.

While this new investment is expected to increase profits, it will also substantially increase

Dynron’s risk. If Dynron is levered, would this investment be more or less attractive to equity

holders than if Dynron had no debt?

16-18. Consider a firm whose only asset is a plot of vacant land, and whose only liability is debt of $15

million due in one year. If left vacant, the land will be worth $10 million in one year.

Alternatively, the firm can develop the land at an upfront cost of $20 million. The developed land

will be worth $35 million in one year. Suppose the risk-free interest rate is 10%, assume all cash

flows are risk-free, and assume there are no taxes.

a. If the firm chooses not to develop the land, what is the value of the firm’s equity today?

What is the value of the debt today?

b. What is the NPV of developing the land?

c. Suppose the firm raises $20 million from equity holders to develop the land. If the firm

develops the land, what is the value of the firm’s equity today? What is the value of the

firm’s debt today?

d. Given your answer to part (c), would equity holders be willing to provide the $20 million

needed to develop the land?

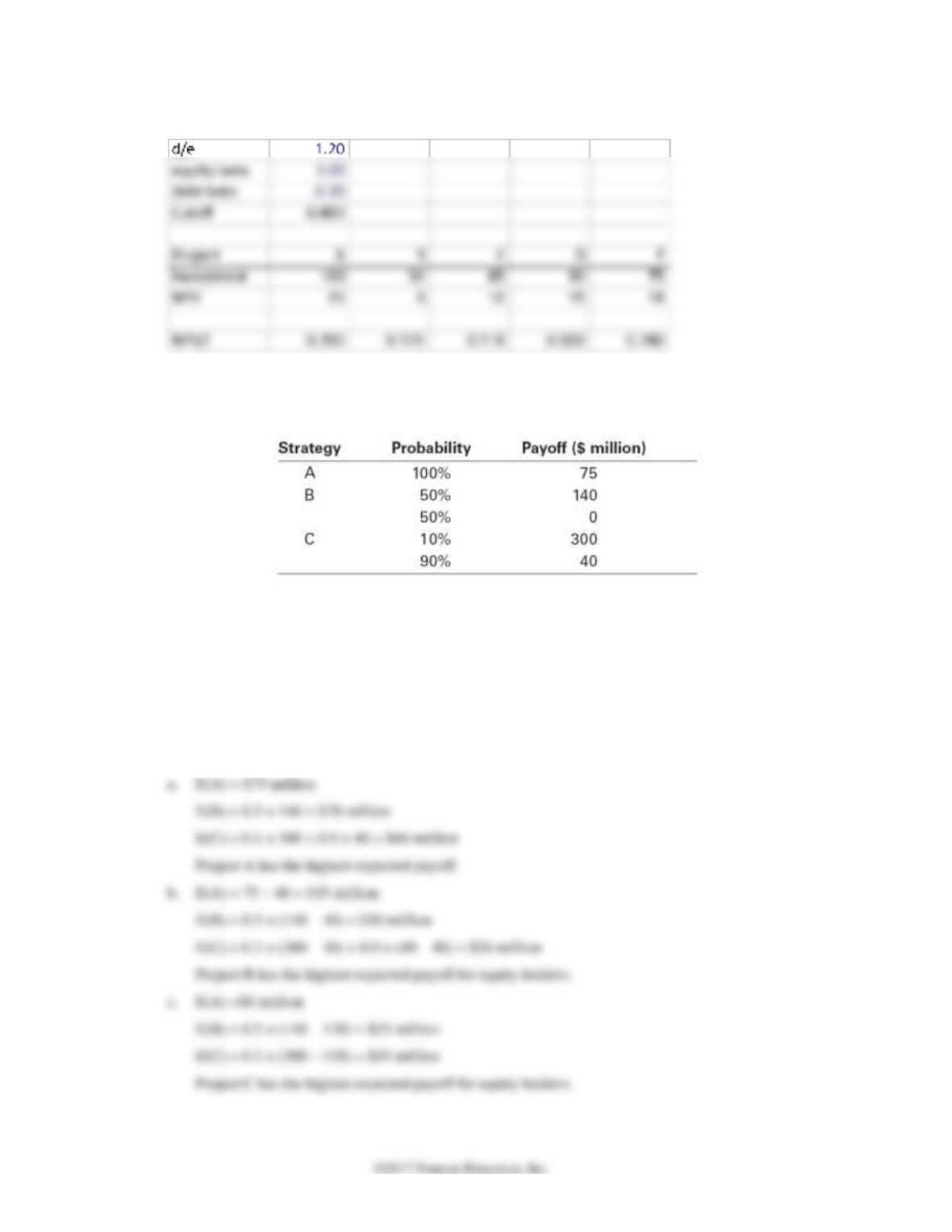

16-19. Sarvon Systems has a debt-equity ratio of 1.2, an equity beta of 2.0, and a debt beta of 0.30. It

currently is evaluating the following projects, none of which would change the firm’s volatility

(amounts in $ million):

a. Which project will equity holders agree to fund?

b. What is the cost to the firm of the debt overhang?

226 Berk/DeMarzo, Corporate Finance, Fourth Edition

b. Don’t take B&C = loss of 6 + 10 = 16 million

16-20. Zymase is a biotechnology start-up firm. Researchers at Zymase must choose one of three

different research strategies. The payoffs (after-tax) and their likelihood for each strategy are

shown below. The risk of each project is diversifiable.

a. Which project has the highest expected payoff?

b. Suppose Zymase has debt of $40 million due at the time of the project’s payoff. Which

project has the highest expected payoff for equity holders?

c. Suppose Zymase has debt of $110 million due at the time of the project’s payoff. Which

project has the highest expected payoff for equity holders?

d. If management chooses the strategy that maximizes the payoff to equity holders, what is the

expected agency cost to the firm from having $40 million in debt due? What is the expected

agency cost to the firm from having $110 million in debt due?

16-21. Petron Corporation’s management team is meeting to decide on a new corporate strategy. There

are four options, each with a different probability of success and total firm value in the event of

success, as shown below:

Strategy

A

B

C

D

Probability of Success

100%

80%

60%

40%

Firm Value if Successful (in $ million)

50

60

70

80

Assume that for each strategy, firm value is zero in the event of failure.

a. Which strategy has the highest expected payoff?

b. Suppose Petron’s management team will choose the strategy that leads to the highest

expected value of Petron’s equity. Which strategy will management choose if Petron

currently has

(i) No debt?

(ii) Debt with a face value of $20 million?

(iii) Debt with a face value of $40 million?

c. What agency cost of debt is illustrated in your answer to part (b)?

16-22. Consider the setting of Problem 21, and suppose Petron Corp. has debt with a face value of $40

million outstanding. For simplicity, assume all risk is idiosyncratic, the risk-free interest rate is

zero, and there are no taxes.

a. What is the expected value of equity, assuming Petron will choose the strategy that

maximizes the value of its equity? What is the total expected value of the firm?

b. Suppose Petron issues equity and buys back its debt, reducing the debt’s face value to $5

million. If it does so, what strategy will it choose after the transaction? Will the total value

of the firm increase?

c. Suppose you are a debt holder, deciding whether to sell your debt back to the firm. If you

expect the firm to reduce its debt to $5 million, what price would you demand to sell your

debt?

d. Based on your answer to (c), how much will Petron need to raise from equity holders in

order to buy back the debt?

e. How much will equity holders gain or lose by recapitalizing to reduce leverage? How much

will debt holders gain or lose? Would you expect Petron’s management to choose to reduce

its leverage?

16-23. Consider the setting of Problems 21 and 22, and suppose Petron Corp. must pay a 25% tax rate

on the amount of the final payoff that is paid to equity holders. It pays no tax on payments to, or

capital raised from, debt holders.

a. Which strategy will Petron choose with no debt? Which will it choose with a face value of

$10 million, $30 million, or $50 million in debt? (Assume management maximizes the value

of equity, and in the case of ties, will choose the safer strategy.)

b. Given your answer to (a), show that the total combined value of Petron’s equity and debt is

maximized with a face value of $30 million in debt.

c. Show that if Petron has $30 million in debt outstanding, shareholders can gain by increasing

the face value of debt to $50 million, even though this will reduce the total value of the firm.

d. Show that if Petron has $50 million in debt outstanding, shareholders will lose by buying

back debt to reduce the face value of debt to $30 million, even though that will increase the

total value of the firm.

a. The table shows value of equity for different debt levels and strategy choices. Optimal strategies

are highlighted:

b. The total value of the firm in each case is:

Debt Face Value

10

30

50

80

0

Debt Value

10

24

30

32

0

Equity Value

30

18

9

0

Firm Value

40

42

39

32

16–24. You own your own firm, and you want to raise $30 million to fund an expansion. Currently, you

own 100% of the firm’s equity, and the firm has no debt. To raise the $30 million solely through

equity, you will need to sell two-thirds of the firm. However, you would prefer to maintain at

least a 50% equity stake in the firm to retain control.

a. If you borrow $20 million, what fraction of the equity will you need to sell to raise the

remaining $10 million? (Assume perfect capital markets.)

b. What is the smallest amount you can borrow to raise the $30 million without giving up

control? (Assume perfect capital markets.)

( )

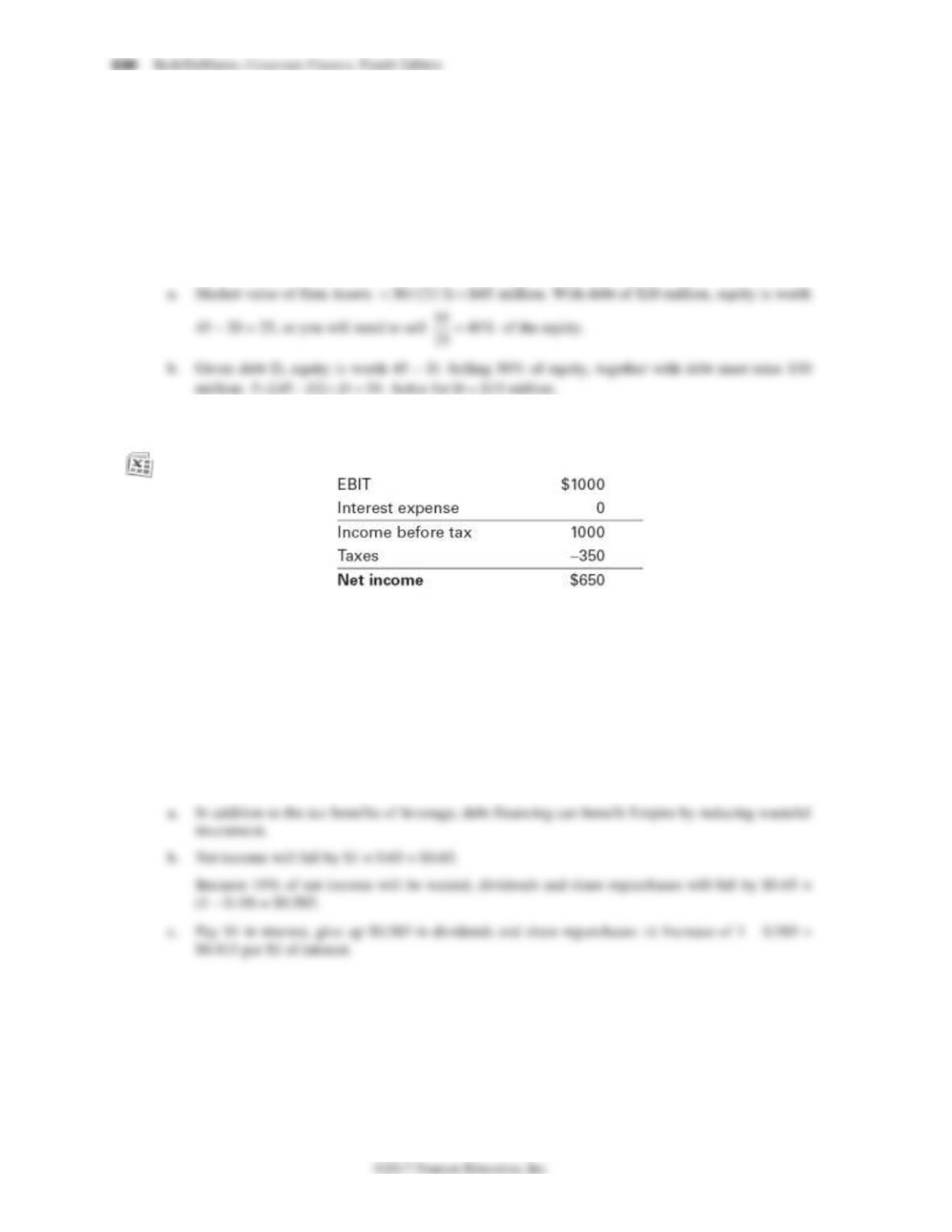

16–25. Empire Industries forecasts net income this coming year as shown below (in thousands of

dollars):

Approximately $200,000 of Empire’s earnings will be needed to make new, positive-NPV

investments. Unfortunately, Empire’s managers are expected to waste 10% of its net income on

needless perks, pet projects, and other expenditures that do not contribute to the firm. All

remaining income will be returned to shareholders through dividends and share repurchases.

a. What are the two benefits of debt financing for Empire?

b. By how much would each $1 of interest expense reduce Empire’s dividend and share

repurchases?

c. What is the increase in the total funds Empire will pay to investors for each $1 of interest

expense?

Chapter 16/Financial Distress, Managerial Incentives, and Information 231

16–26. Ralston Enterprises has assets that will have a market value in one year as follows:

That is, there is a 1% chance the assets will be worth $70 million, a 6% chance the assets will be

worth $80 million, and so on. Suppose the CEO is contemplating a decision that will benefit her

personally but will reduce the value of the firm’s assets by $10 million. The CEO is likely to

proceed with this decision unless it substantially increases the firm’s risk of bankruptcy.

a. If Ralston has debt due of $75 million in one year, the CEO’s decision will increase the

probability of bankruptcy by what percentage?

b. What level of debt provides the CEO with the biggest incentive not to proceed with the

decision?

16–27. Although the major benefit of debt financing is easy to observe—the tax shield—many of the

indirect costs of debt financing can be quite subtle and difficult to observe. Describe some of

16–28. If it is managed efficiently, Remel Inc. will have assets with a market value of $50 million, $100

million, or $150 million next year, with each outcome being equally likely. However, managers

may engage in wasteful empire building, which will reduce the firm’s market value by $5 million

in all cases. Managers may also increase the risk of the firm, changing the probability of each

outcome to 50%, 10%, and 40%, respectively.

a. What is the expected value of Remel’s assets if it is run efficiently?

Suppose managers will engage in empire building unless that behavior increases the likelihood of

bankruptcy. They will choose the risk of the firm to maximize the expected payoff to equity

holders.

b. Suppose Remel has debt due in one year as shown below. For each case, indicate whether

managers will engage in empire building, and whether they will increase risk. What is the

expected value of Remel’s assets in each case?

i. $44 million

ii. $49 million

iii. $90 million

iv. $99 million

c. Suppose the tax savings from the debt, after including investor taxes, is equal to 10% of the

expected payoff of the debt. The proceeds from the debt, as well as the value of any tax

savings, will be paid out to shareholders immediately as a dividend when the debt is issued.

Which debt level in part (b) is optimal for Remel?

232 Berk/DeMarzo, Corporate Finance, Fourth Edition

16–29. Which of the following industries have low optimal debt levels according to the trade-off theory?

Which have high optimal levels of debt?

a. Tobacco firms

b. Accounting firms

c. Mature restaurant chains

d. Lumber companies

e. Cell phone manufacturers

16–30 According to the managerial entrenchment theory, managers choose capital structures so as to

preserve their control of the firm. On the one hand, debt is costly for managers because they risk

losing control in the event of default. On the other hand, if they do not take advantage of the tax

shield provided by debt, they risk losing control through a hostile takeover.

Suppose a firm expects to generate free cash flows of $90 million per year, and the discount rate

for these cash flows is 10%. The firm pays a tax rate of 40%. A raider is poised to take over the

firm and finance it with $750 million in permanent debt. The raider will generate the same free

cash flows, and the takeover attempt will be successful if the raider can offer a premium of 20%

over the current value of the firm. According to the managerial entrenchment hypothesis, what

level of permanent debt will the firm choose?

0.10

Chapter 16/Financial Distress, Managerial Incentives, and Information 233

16–31. Info Systems Technology (IST) manufactures microprocessor chips for use in appliances and

other applications. IST has no debt and 100 million shares outstanding. The correct price for

these shares is either $14.50 or $12.50 per share. Investors view both possibilities as equally

likely, so the shares currently trade for $13.50.

IST must raise $500 million to build a new production facility. Because the firm would suffer a

large loss of both customers and engineering talent in the event of financial distress, managers

believe that if IST borrows the $500 million, the present value of financial distress costs will

exceed any tax benefits by $20 million. At the same time, because investors believe that managers

know the correct share price, IST faces a lemons problem if it attempts to raise the $500 million

by issuing equity.

a. Suppose that if IST issues equity, the share price will remain at $13.50. To maximize the

long-term share price of the firm once its true value is known, would managers choose to

issue equity or borrow the $500 million if

i. They know the correct value of the shares is $12.50?

ii. They know the correct value of the shares is $14.50?

b. Given your answer to part (a), what should investors conclude if IST issues equity? What

will happen to the share price?

c. Given your answer to part (a), what should investors conclude if IST issues debt? What will

happen to the share price in that case?

d. How would your answers change if there were no distress costs, but only tax benefits of

leverage?

234 Berk/DeMarzo, Corporate Finance, Fourth Edition

16–32. During the Internet boom of the late 1990s, the stock prices of many Internet firms soared to

extreme heights. As CEO of such a firm, if you believed your stock was significantly overvalued,

would using your stock to acquire non-Internet stocks be a wise idea, even if you had to pay a

small premium over their fair market value to make the acquisition?

16–33. “We R Toys” (WRT) is considering expanding into new geographic markets. The expansion will

have the same business risk as WRT’s existing assets. The expansion will require an initial

investment of $50 million and is expected to generate perpetual EBIT of $20 million per year.

After the initial investment, future capital expenditures are expected to equal depreciation, and

no further additions to net working capital are anticipated.

WRT’s existing capital structure is composed of $500 million in equity and $300 million in debt

(market values), with 10 million equity shares outstanding. The unlevered cost of capital is 10%,

and WRT’s debt is risk free with an interest rate of 4%. The corporate tax rate is 35%, and

there are no personal taxes.

a. WRT initially proposes to fund the expansion by issuing equity. If investors were not

expecting this expansion, and if they share WRT’s view of the expansion’s profitability, what

will the share price be once the firm announces the expansion plan?

b. Suppose investors think that the EBIT from WRT’s expansion will be only $4 million. What

will the share price be in this case? How many shares will the firm need to issue?

c. Suppose WRT issues equity as in part (b). Shortly after the issue, new information emerges

that convinces investors that management was, in fact, correct regarding the cash flows from

the expansion. What will the share price be now? Why does it differ from that found in part

(a)?

d. Suppose WRT instead finances the expansion with a $50 million issue of permanent risk-free

debt. If WRT undertakes the expansion using debt, what is its new share price once the new

information comes out? Comparing your answer with that in part (c), what are the two

Chapter 16/Financial Distress, Managerial Incentives, and Information 235