Mini Case: 15 – 17

g. What does the empirical evidence say about capital structure theory? What are

the implications for managers?

Answer: Tax benefits are important. At the optimal capital structure, $1 debt adds about $0.10

to $0.20 to value on average. For the average firm financed with 25% to 30% debt,

this adds about 3% to 6% to the total value. However, these results were based on

periods prior to the TCJA and may now overstate the value added by debt.

After big stock price run ups, the debt ratio falls, but firms tend to issue equity

instead of debt. This is inconsistent with the trade-off model, inconsistent with the

pecking order theory, but is consistent with the windows of opportunity hypothesis.

Many firms, especially those with growth options and asymmetric information

problems, tend to maintain excess borrowing capacity.

Mini Case: 15 – 18

h. With the above points in mind, now consider the optimal capital structure for

PizzaPalace.

h. (1) For each capital structure under consideration, calculate the levered beta, the cost

of equity, and the WACC.

Answer: MM theory implies that beta changes with leverage. bu is the beta of a firm when it

has no debt (the unlevered beta). Hamada’s equation provides the beta of a levered

firm: bL = bU [1 + (1 – T)(D/S)]. For example, to find the cost of equity for wd = 20%,

we first use Hamada’s equation to find beta:

Mini Case: 15 – 19

h. (2) Now calculate the corporate value.

Answer: For example, suppose that wd = 20% is:

FCF = NOPAT – Investments in operating capital

= EBIT(1 − T) – Investments in operating capital

= $120(1 – 0.25) – $0 = $90.

Repeating this for all capital structures gives the following table:

wd

0%

20%

30%

40%

50%

i. Describe the recapitalization process and apply it to PizzaPalace. Calculate the

resulting the value of the debt that will be issued, the resulting market value of

equity, the price per share, the number of shares repurchased, and the remaining

shares. Considering only the capital structures under analysis, what is

PizzaPalace’s optimal capital structure?

Answer:

The situation before the recap is:

Before

Debt

Vop

$750.00

$750.00

$750.00

$750.00

$750.00

Mini Case: 15 – 21

Before Debt

After Debt,

Before Rep.

Vop

$750.00

$769.23

$153.85

VTotal

$750.00

$923.08

$153.85

$750.00

$769.23

$750.00

$769.23

$750.00

$769.23

Notice that the stock price increases and the wealth of shareholders increases.

The repurchase itself will not change the stock price. If investors thought that the

repurchase would increase the stock price, they would all purchase stock the day

before, which would drive up its price. If investors thought that the repurchase would

decrease the stock price, they would all sell short the stock the day before, which

would drive down the stock price.

Mini Case: 15 – 22

Before

Debt

After

Debt,

Before

Rep.

After Rep.

Vop

$750.00

$769.23

$769.23

$153.85

$750.00

$923.08

$769.23

$153.85

$153.85

$750.00

$769.23

$615.38

$750.00

$769.23

$615.38

$153.85

$750.00

$769.23

$769.23

Notice that the value of the equity declines as more debt is issued, because debt is

used to repurchase stock. But the total wealth of shareholders is the value of stock

after the recap plus the cash received in repurchase, and this total is not changed by

the repurchase.

Mini Case: 15 – 23

There are some shortcuts we can take to find the values of S, P, and n after the

repurchase:

We apply these relationships for each possible capital structure:

wd

0%

20%

30%

40%

50%

rd

0.0%

8.0%

8.5%

10.0%

12.0%

ws

100%

80%

70%

60%

50%

b

D

The optimal capital structure is for wd = 30%. This gives the highest corporate value,

the lowest WACC, and the highest stock price per share. But notice that wd = 20% is

very similar to the optimal solution; in other words, the optimal range is pretty flat.

j. Liu Industries is a highly levered firm. Suppose there is a large probability that

Liu will default on its debt. The value of Liu’s operations is $4 million. The firm’s

debt consists of 1–year, zero coupon bonds with a face value of $2 million. Liu’s

volatility, σ, is 0.60 and the risk-free rate rRF is 6%. Because Liu’s debt is risky, its

equity is like a call option and can be valued with the Black-Scholes Option Pricing

Model (OPM). (See Chapter 8 for details of the OPM.)

j. (1) What are the values of Liu’s stock and debt? What is the yield on the debt?

Answer: Liu’s equity can be considered as a call option on the total value of l with an exercise

price of $2 million, and an expiration date in one year. If the value of Liu’s operations

is less than $2 million in a year, then Liu’s management will not be able to make its

required payment on the debt, and the firm will be bankrupt. The debtholders will take

Mini Case: 15 – 25

j. (2) What are the values of Liu’s stock and debt for volatilities of 0.40 and 0.80? What

are yields on the debt?

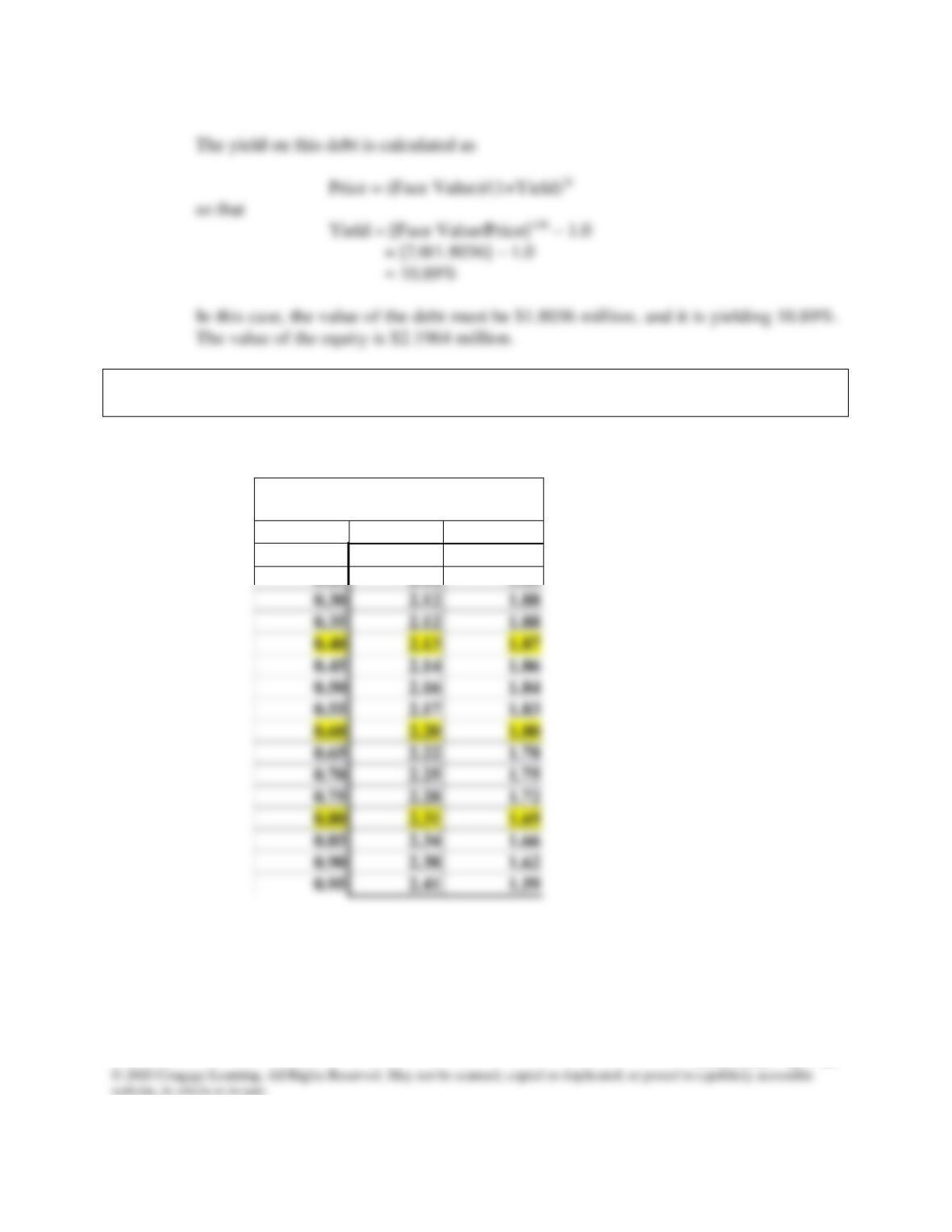

Answer: The mini case model shows the calculations for the table below.

Value of Stock and Debt

for Different Volatilities

Volatility

Equity

Debt

0.20

2.12

1.88

0.25

2.12

1.88

0.30

2.12

1.88

0.35

2.12

1.88

0.45

2.14

1.86

0.50

2.16

1.84

0.55

2.17

1.83

0.60

2.20

1.80

0.65

2.22

1.78

0.70

2.25

1.75

0.75

2.28

1.72

0.80

2.31

1.69

0.85

2.34

1.66

0.90

2.38

1.62

0.95

2.41

1.59

Mini Case: 15 – 26

j. (3) What incentives might the manager of Liu have if she understands the

relationship between equity value and volatility? What might debtholders do in

response?

Answer: The value of the equity increases as the volatility increases—and the value of the debt

decreases as well. A manager who knows this may choose to invest the proceeds from

k. How do companies manage the maturity structure of their debt?

Answer: Factors that influence the decision to issue long-term bonds rather than short-term debt:

Mini Case: 15 – 27

SOLUTIONS TO END–OF-WEB EXTENSION PROBLEMS

15B-1 a. Since the call premium is 11 percent, the total premium is 0.11($40,000,000) =

$4,400,000. However, this is a tax deductible expense, so the relevant after-tax cost is

$4,400,000(1 – T) = $4,400,000(0.75) = $3,300,000.

c. The flotation costs on the old issue were 0.06($40,000,000) = $2,400,000. These costs

were deferred and are being amortized over the 25-year life of the issue, and hence

$2,400,000/25 = $96,000 are being expensed each year, or $48,000 each 6 months.

d. The net after-tax initial cash outlay is shown below:

Old issue call premium from part a: $3,300,000

New issue flotation cost from part b: 1,600,000

Tax savings on old issue flotation costs from part c: (480,000)

Net cash outlay $4,420,000

Mini Case: 15 – 28

f. The interest on the old issue is 0.11($40,000,000) = $4,400,000 annually, or $2,200,000

semiannually. Since interest payments are tax deductible, the after-tax semiannual

g.

Semiannual Flotation Cost Tax Effects:

Semiannual tax savings on new flotation: $10,000

Tax benefits lost on old flotation: (12,000)

Net amortization tax effects ($ 2,000)

The cash flows are based on contractual obligations, and hence have about the same

amount of risk as the firm’s debt. Further, the cash flows are already net of taxes. Thus,

the appropriate interest rate is GST’s after-tax cost of debt. (The source of the cash to

fund the net investment outlay also influences the discount rate, but most firms use debt

Mini Case: 15 – 29

h.

PV of net benefits from part g: $10,355,418

Initial cash flow from part d: −$4,420,000

Refunding NPV $5,935,418

The decision to refund now rather than wait till later is much more difficult than

finding the NPV of refunding now. If interest rates were expected to fall, and hence

Mini Case: 15 – 30

15B-2 a. Investment outlay required to refund the issue (all figures after-tax):

Call premium on the old bond

−$6,750,000

Flotation costs on new issue

−$5,000,000

−$10,989,583

Annual lost tax savings from old-issue flotation

−$41,667

Net flotation cost tax savings

Interest on old bond

$6,750,000

Interest on new bond

−$5,625,000

Net interest savings

$1,125,000

b. The company should consider what interest rates might be next year. If there is a high

probability that rates will drop below the current rate, it may be more advantageous to

refund later versus now. If there is a high probability that rates will increase, the firm

should act now to refund the old issue. Also, the company should consider how much

ill will is created with investors if the issue is called. If Mullet is highly dependent on

a small group of investors, it would want to avoid future difficulty in obtaining

Mini Case: 15 – 31

SOLUTIONS TO WEB EXTENSION SPREADSHEET PROBLEMS

15B-3 The detailed solution for the spreadsheet problem, Solution for Ch15 Web15B P03 Build

a Model.xlsx, is available on the textbook’s Web site.