1

2

3

4

5

6

7

8

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

40

41

42

43

44

45

46

47

48

49

50

51

62

63

64

65

66

67

68

69

70

77

78

Tax Rate 25% 25%

79

80

A B C D E F G H I J K L

11/21/2018

Situation

Input Data

Percent Financed

with debt, wdrd

0% 0.0%

20% 8.0%

30% 8.5%

40% 10.0%

50% 12.0%

F = $200 QRevenues

Fixed Costs

Total Costs

P = $15 0$0 $200 $200

V = $10 80 $1,200 $200 $1,000

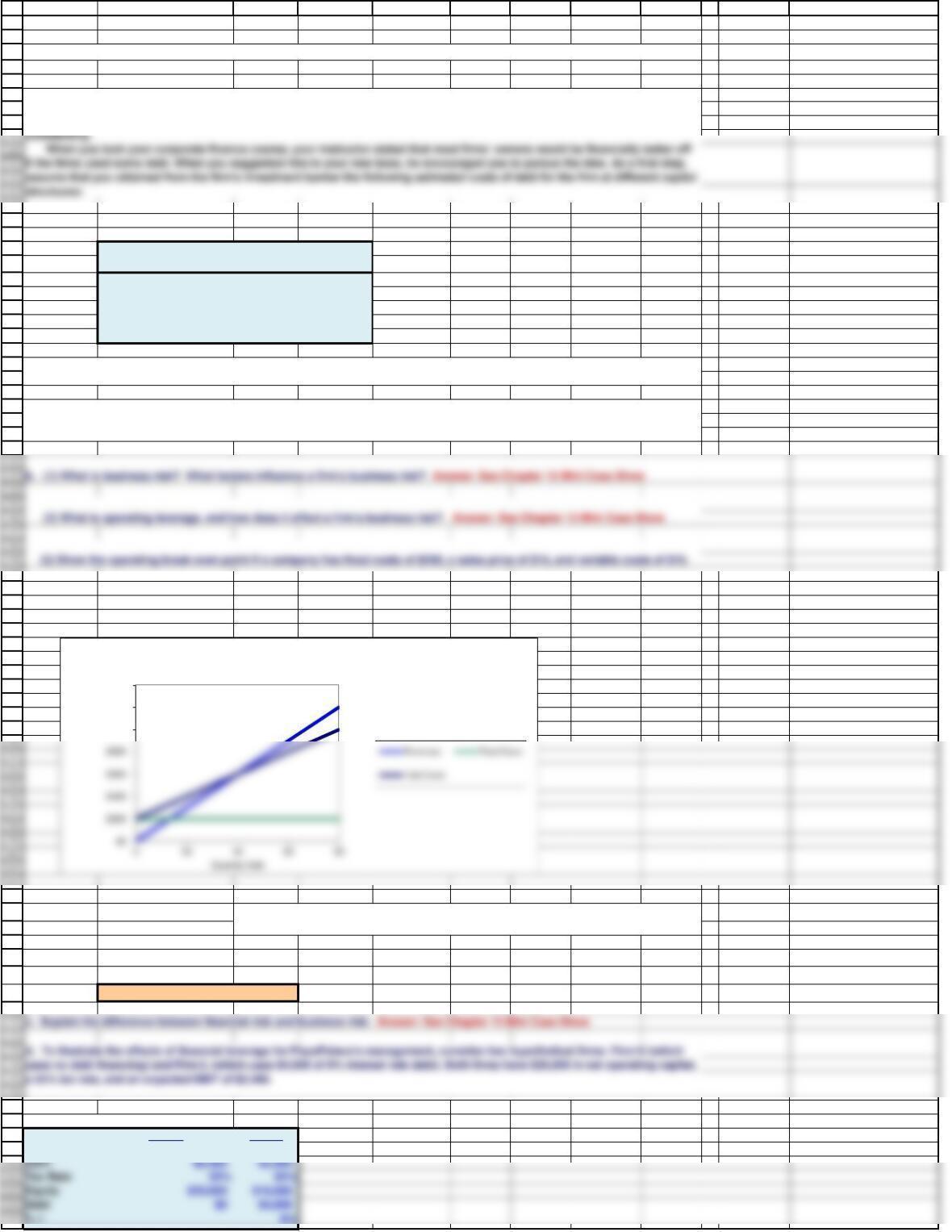

Q BE = FC / (P – VC)

Q BE = F÷(P – VC)

Q BE = $200 ÷$15.00 – $10.00

Q BE = 40 Units.

Two Hypothetical Firms

Firm U Firm L

Capital $20,000 $20,000

Chapter 15. Mini Case

If the company were to recapitalize, debt would be issued, and the funds received would be used to repurchase stock.

a. Using the free cash flow valuation model, show the only avenues by which capital structure can affect value.. Answer: See

Chapter 15 Mini Case Show

In words, the quantity at which a firm breaks even is found as the difference between

Price and Variable costs divided by Fixed costs.

Assume you have just been hired as a business manager of PizzaPalace, a regional pizza restaurant chain. The company’s EBIT

was $120 million last year and is not expected to grow. Pizza Palace is in the 25% state-plus-federal tax bracket, the risk-free rate

is 6 percent, and the market risk premium is 6 percent. The firm is currently financed with all equity and it has 10 million shares

$1,000

$1,200

$1,400

Operating Leverage

86

87

88

89

90

91

92

97

98

99

100

101

108

109

110

111

112

113

114

115

116

117

127

128

129

130

131

132

133

139

140

141

142

143

h. With the above points in mind, now consider the optimal capital structure for PizzaPalace.

g. What does does the empirical evidence say about capital structure theory? What are the implications for managers?

149

150

151

152

153

154

155

156

157

158

159

160

167

168

169

170

A B C D E F G H I J K L

Impact of Leverage

Firm U Firm L Distribution to Investors

EBIT $2,400 $2,400

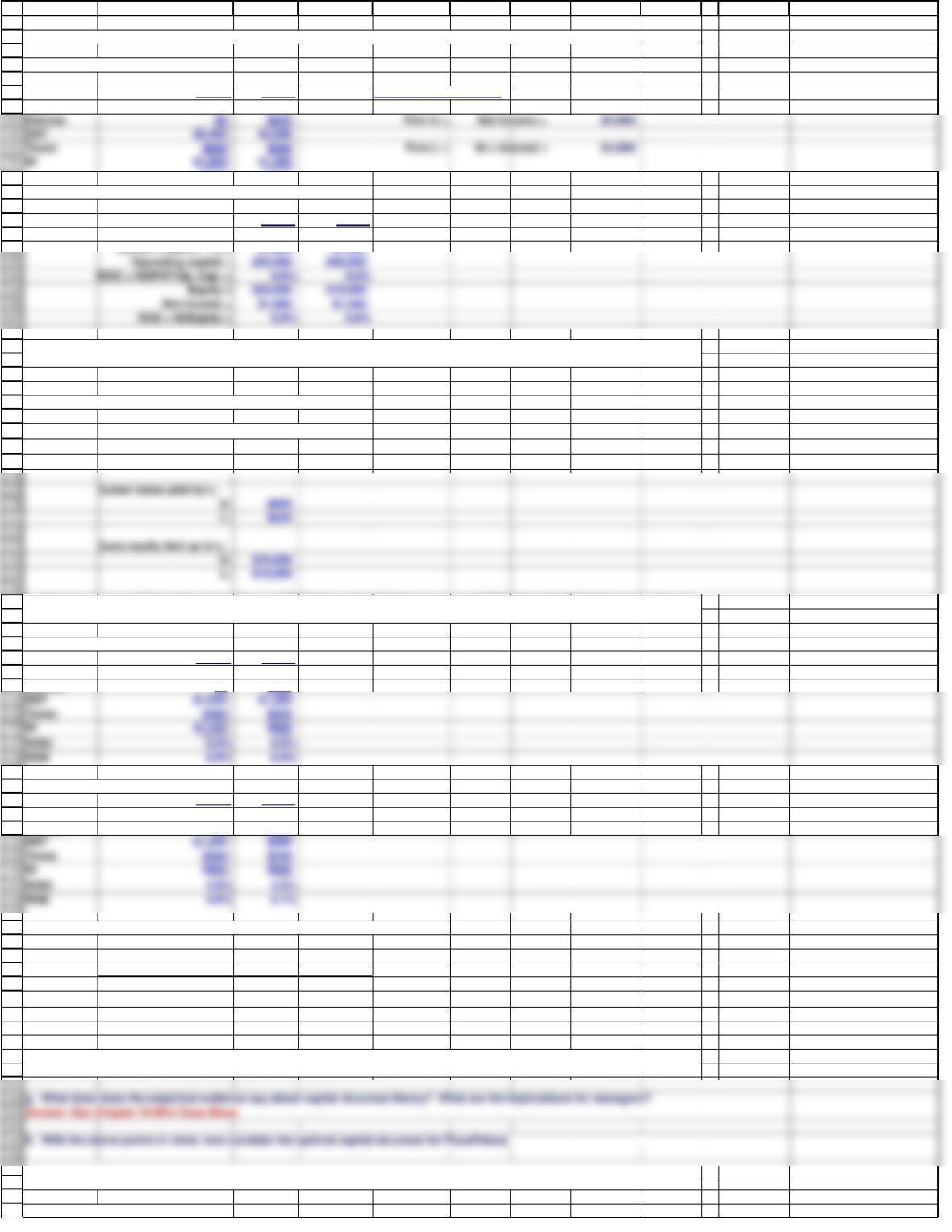

(2) Calculate NOPAT, ROIC, and ROE for both firms.

xFirm U Firm L

EBIT = $2,400 $2,400

(4) Why did leverage increase ROE in this example?

More total dollars paid to L’s investors:

U: NI = $1,800

L: NI + Int = $1,880

If EBIT = $1,200:

Firm U Firm L

EBIT $1,600 $1,600

Interest $0 $320

If EBIT = $1,600:

Firm U Firm L

EBIT $1,200 $1,200

Interest $0 $320

Leverage only adds value if ROIC is greater than the after-tax cost of debt.

EBIT EBIT EBIT

$2,400 $1,600 $1,200

ROIC 9.0% 6.0% 4.5%

rd(1-T) 6.0% 6.0% 6.0%

ROE 9.8% 6.0% 4.1%

Data for Recapitalization

f. What does capital structure theory attempt to do? What lessons can be learned from capital structure theory? Be sure to

address the MM models. Answer: See Chapter 15 Mini Case Show

e. What happens to ROE for Firm U and Firm L if EBIT falls to $1,600? What happens if EBIT falls to $1,200? What is the after-tax

cost of debt? What does this imply about the impact of leverage on risk and return?

(1) Construct partial income statements, which start with EBIT, for the two firms.

(1) For each capital structure under consideration, calculate the levered beta, the cost of equity, and the WACC.

(3) What does this example illustrate about the impact of financial leverage on ROE? Answer: See Chapter 15 Mini Case Show

Interest $0 $320 Firm U = $1,800

171

172

173

179

180

181

182

183

184

185

186

187

188

189

191

193

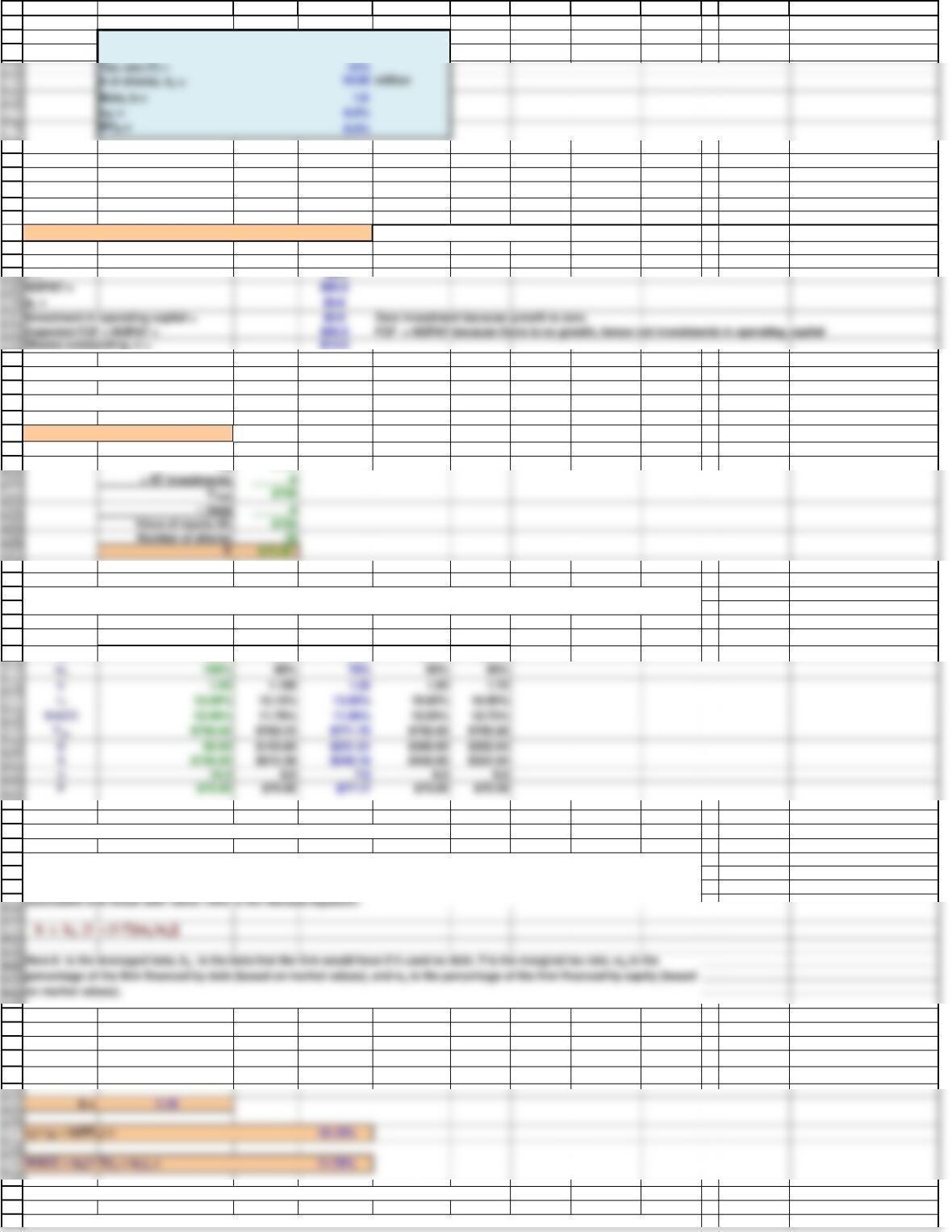

T = 25%

NOPAT = $90.0

gL = $0.0

Investment in operating capital = $0.0 Zero investment because growth is zero.

Expected FCF = NOPAT = $90.0 FCF = NOPAT because there is no growth, hence not investments in operating capital

Shares outstanding, n = $10.0

ws100% 80% 70% 60% 50%

rs12.00% 13.13% 13.93% 15.00% 16.50%

194

195

196

197

198

199

200

201

208

209

210

211

212

213

214

224

225

226

227

228

235

236

associated with those debt ratios. Here is the Hamada equation:

229

230

rs= rRF + b(RPM) = 13.13%

238

239

240

241

242

243

250

251

252

253

A B C D E F G H I J K L

EBIT = $120 million

gL = 0%

Beta, b = 1.0

rRF = 6.0%

RPM = 6.0%

WACC = rs= rRF + b(RPM) = 12.00% WACC = rs because there is not debt

EBIT = $120.0

Current Valuation

Vop = [FCF(1+gL)]/(WACC-gL)

Vop = $750.00

Vop $750

wd0% 20% 30% 40% 50%

rd0.0% 8.0% 8.5% 10.0% 12.0%

Estimating the Cost of Equity for Different Capital Structures

For example:

wd = 20%

ws = 80%

The betas, cost of equity, and WACC at each debt level are shown in the table above.

Investment bankers provided estimates of the cost of debt for different capital structures, as shown below. Other rows are

explained below the table.

(2) Now calculate the corporate value, the value of the debt that will be issued, and the resulting market value of equity.

Hamada developed his equation by merging the CAPM with the Modigliani-Miller model. We use the model to determine beta at

different amount of financial leverage, and then use the betas associated with different debt ratios to find the cost of equity

Tax rate (T) = 25%