Answers and Solutions: 15 – 1

Chapter 15

Capital Structure Decisions

ANSWERS TO END-OF-CHAPTER QUESTIONS

15-1 a. Capital structure is the manner in which a firm’s assets are financed; that is, the right–

hand side of the balance sheet. Capital structure is normally expressed as the

percentage of each type of capital used by the firm—debt, preferred stock, and common

equity. Business risk is the risk inherent in the operations of the firm, prior to the

financing decision. Thus, business risk is the uncertainty inherent in a total risk sense,

b. Operating leverage is the extent to which fixed costs are used in a firm’s operations. If

a high percentage of a firm’s total costs are fixed costs, then the firm is said to have a

high degree of operating leverage. Operating leverage is a measure of one element of

business risk, but does not include the second major element, sales variability.

c. Reserve borrowing capacity exists when a firm uses less debt under “normal”

conditions than called for by the tradeoff theory. This allows the firm some flexibility

to use debt in the future when additional capital is needed.

15-2 Business risk refers to the uncertainty inherent in projections of future ROIC = ROEU.

15-4 Operating leverage affects EBIT and, through EBIT, EPS. Financial leverage has no effect

on EBIT—it only affects EPS, given EBIT.

15-5 If sales tend to fluctuate widely, then cash flows and the ability to service fixed charges

will also vary. Such a firm is said to have high business risk. Consequently, there is a

15-6 Public utilities place greater emphasis on long-term debt because they have more stable

sales and profits as well as more fixed assets. Also, utilities have fixed assets which can

15-7 EBIT depends on sales and operating costs. Interest is deducted from EBIT. At high debt

levels, firms lose business, employees worry, and operations are not continuous because of

financing difficulties. Thus, financial leverage can influence sales and costs, and hence

EBIT, if excessive leverage is used.

15-8 The tax benefits from debt increase linearly, which causes a continuous increase in the

15-9 If equity is viewed as an option on the total value of the firm with a strike price equal to

the face value of debt then the equity value should be affected by risk in the same way that

an option is affected by risk. An option is worth more if the underlying asset is more risky,

Answers and Solutions: 15 – 3

SOLUTIONS TO END-OF-CHAPTER PROBLEMS

15-1 QBE = F/(P – V) = $500,000/($75 – $50) = 20,000.

15-2 If wd = 0.21, then ws = 1 – 0.21 = 0.79. So D/S = wd/we = 0.21/0.79.

15-3 If the company had no debt, its required return would be:

rs,U = rRF + bU x RPM = 5.5% + 1.0(6%) = 11.5%.

15-4 With zero debt, the MM model is: VL = VU:

VL = VU = $50 billion.

15-5 VL = VU + TD= $400 + 0.25($100) = $425 billion.

15-7 SPost = (1 – wd)(VopNew) = (1 – 0.4)($500) = $300 million.

15-8 SPost = (1 – wd)(VopNew) = (1 – 1/3)($900) = $600 million.

PPost = (VopNew – Dold)/nprior = ($900 – 0)/30 = $30

Answers and Solutions: 15 – 4

15-10 a. Here are the steps involved:

(1) Determine the variable cost per unit at present, V:

(3) Determine the incremental profit:

Profit = $1,350,000 – $500,000 = $850,000.

(4) Estimate the approximate rate of return on new investment:

b. The change would increase the breakeven point:

Old: QBE =

VP

F

−

=

000,50$000,100$

000,000,2$

−

= 40 units.

Answers and Solutions: 15 – 5

c. It is impossible to state unequivocally whether the new situation would have more or

less business risk than the old one. We would need information on both the sales

probability distribution and the uncertainty about variable input cost in order to make

this determination. However, since a higher breakeven point, other things held

constant, is more risky. Also the percentage of fixed costs increases:

15-11 a. Original value of the firm (D = $0):

Original free cash flow:

FCF = NOPAT = EBIT(1-T) since no growth = $600,000(1-0.25) = $450,000

Answers and Solutions: 15 – 6

b. Using its target capital structure of 30% debt:

With financial leverage (wd=30%):

WACC = wd rd(1-T) + wcers

= (0.3)(7%)(1-0.25) + (0.7)(12%) = 9.975%.

c. The stock price after the debt is issued but before shares are purchased, PPrior:

PPrior = (Vop + ST investments – Debt)/nPrior

= (Vop + New Debt – (Old debt + New Debt)/nPrior

= (Vop – Old debt)/nPrior

= ($4,511,278.195 – $0)/200,000 =$22.5564

Answers and Solutions: 15 – 7

15-12 a. Present situation (50% debt):

WACC = wd rd(1-T) + wcers

= (0.5)(10%)(1-0.15) + (0.5)(14%) = 11.25%.

15-13 a. BEA’s unlevered beta is bU=b/(1+ (1-T)(D/S))=1.0/(1+(1-0.25)(20/80)) = 0.8421.

b. b = bU (1 + (1-T)(D/S)).

At 40 percent debt: bL = 0.8421 (1 + 0.75(40%/60%)) = 1.2632.

rS = 6 + 1.2632(4) = 11.0528%

Answers and Solutions: 15 – 8

15-14 Tax rate = 25% rRF = 5.0%

bU = 0.8 rM – rRF = 6.0%

From data given in the problem and table we can develop the following table:

wd

ws

D/S

rd

rd(1 – T)

Levered

betaa

rsb

WACCc

Notes:

a These beta estimates were calculated using the Hamada equation,

b = bU[1 + (1 – T)(D/S)].

b These rs estimates were calculated using the CAPM, rs = rRF + (rM – rRF)b.

Answers and Solutions: 15 – 9

15-15 a. The inputs to the Black and Scholes option pricing model are P = 100, X = 50, rRF =

6%, = 50%, and t = 10 years. Given these inputs, the value of a call option is

calculated as:

)][N(dXe)]P[N(dV 2

t-r

1RF

−=

=

3.29 [0.8669]2e5[0.9656] )2(06.0– =−

million

b. The debt must therefore be worth 5-3.29 = $1.71 million. Its yield is

%1.881.0171.1/0.2 ==−

.

Answers and Solutions: 15 – 10

SOLUTIONS TO SPREADSHEET PROBLEMS

15-16 The detailed solution for the problem is available in the file Ch15 P16 Build a Model

Solutions.xlsx on the textbook’s Web site.

15-17 The detailed solution for the problem is available in the file Ch15 P17 Build a Model

Solution.xlsx on the textbook’s Web site.

Mini Case: 15 – 11

MINI CASE

Assume you have just been hired as a business manager of PizzaPalace, a regional pizza

restaurant chain. The company’s EBIT was $120 million last year and is not expected to

grow. Pizza Palace is in the 25% state-plus-federal tax bracket, the risk-free rate is 6

percent, and the market risk premium is 6 percent. The firm is currently financed with all

equity and it has 10 million shares outstanding.

When you took your corporate finance course, your instructor stated that most

firms’ owners would be financially better off if the firms used some debt. When you

suggested this to your new boss, he encouraged you to pursue the idea. If the company were

to recapitalize, debt would be issued, and the funds received would be used to repurchase

stock. As a first step, assume that you obtained from the firm’s investment banker the

following estimated costs of debt for the firm at different capital structures:

Percent Financed with Debt

wd rd

0% —

20 8.0%

30 8.5

40 10.0

50 12.0

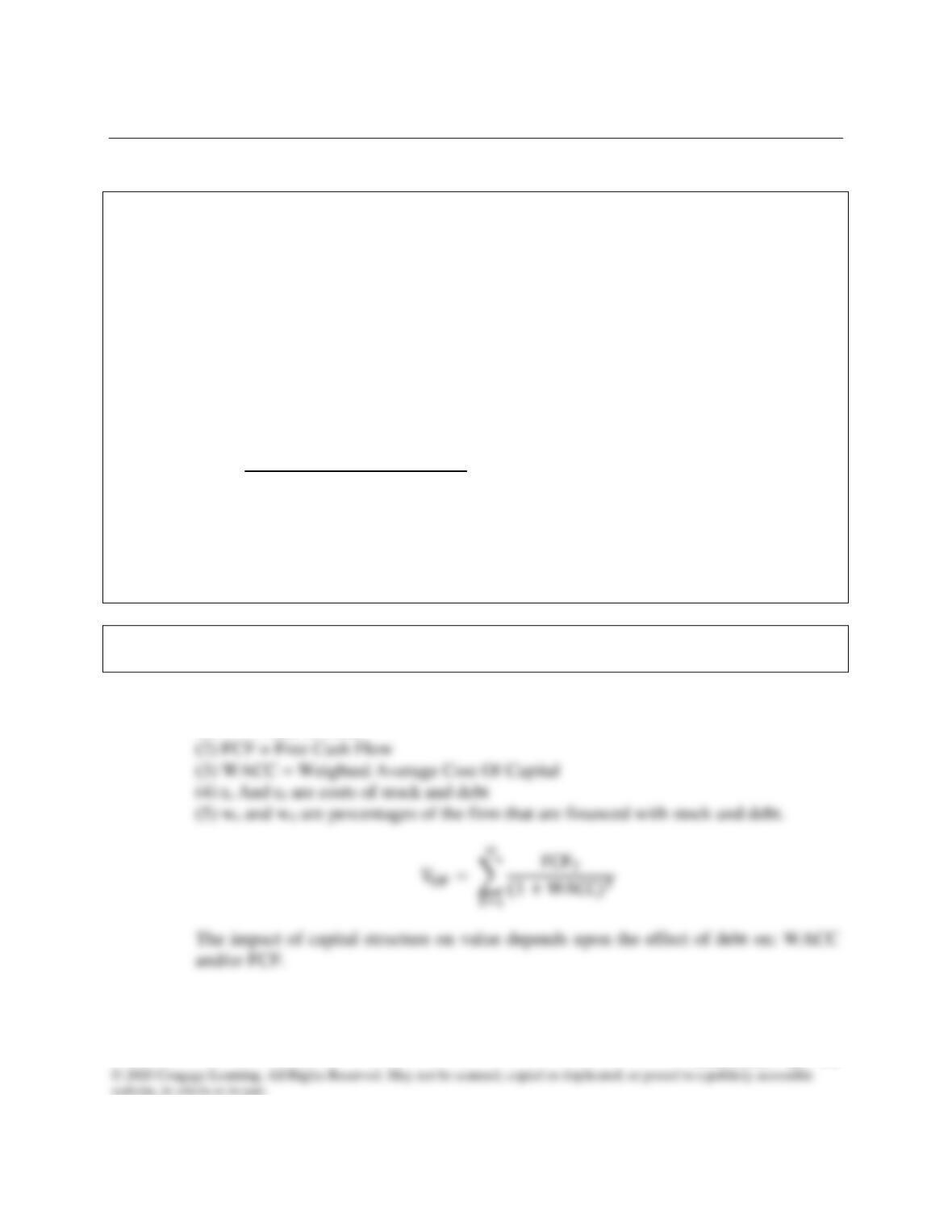

a. Using the free cash flow valuation model, show the only avenues by which capital

structure can affect value.

Answer: The basic definitions are:

(1) V = Value of Firm

Mini Case: 15 – 12

b. (1) What is business risk? What factors influence a firm’s business risk?

Answer: Business risk is uncertainty about EBIT. Factors that influence business risk include:

b. (2) What is operating leverage, and how does it affect a firm’s business risk? Show

the operating break even point if a company has fixed costs of $200, a sales price

of $15, and variables costs of $10.

Answer: Operating leverage is the change in EBIT caused by a change in quantity sold. The

c. Explain the difference between financial risk and business risk.

Answer: Business risk increases the uncertainty in future EBIT. It depends on business factors

Mini Case: 15 – 13

d. To illustrate the effects of financial leverage for PizzaPalace’s management,

consider two hypothetical firms: Firm U (which uses no debt financing) and Firm

L (which uses $4,000 of 8% interest rate debt). Both firms have $20,000 in net

operating capital, a 25% tax rate, and an expected EBIT of $2,400.

d. 1. Construct partial income statements, which start with EBIT, for the two firms.

Answer: Partial Income Statements:

d. 2. Calculate NOPAT, ROIC, and ROE for both firms.

Answer:

Firm U

Firm L

EBIT =

$2,400

$2,400

$1,800

$1,800

$1,800

$1,560

d. 3. What does this example illustrate about the impact of financial leverage on ROE?

Answer:

1. ROIC wasn’t affected by financial leverage.

Mini Case: 15 – 14

d. 4. Why did leverage increase ROE in this example?

Answer:

1. More total dollars paid to L’s investors:

a. U: NI = $1,800.

e. What happens to ROE for Firm U and Firm L if EBIT falls to $1,600? What

happens if EBIT falls to $1,200? What is the after-tax cost of debt? What does this

imply about the impact of leverage on risk and return?

Answer:

x

Firm U

Firm L

EBIT

$1,600

$1,600

Interest

EBT

$1,600

$1,280

Taxes

$1,200

ROIC

ROE

EBIT

Interest

EBT

Taxes

ROIC

ROE

Mini Case: 15 – 15

f. What does capital structure theory attempt to do? What lessons can be learned

from capital structure theory? Be sure to address the MM models.

Answer: MM theory begins with the assumption of zero taxes. MM prove, under a very

restrictive set of assumptions, that a firm’s value is unaffected by its financing mix:

VL = VU.

Mini Case: 15 – 16

One agency problem is that managers can use corporate funds for non-value

maximizing purposes. The use of financial leverage bonds “free cash flow,” and

forces discipline on managers to avoid perks and non-value adding acquisitions.

A second agency problem is the potential for “underinvestment”. Debt increases risk

of financial distress. Therefore, managers may avoid risky projects even if they have

positive NPVs.