CFIN6 – CHAPTER 15

INTEGRATIVE PROBLEMS SOLUTIONS

Integrative Problem 15-1

a. Because cash is a nonearning asset, the goal of cash management is to reduce the amount of cash

held to the minimum necessary to conduct business.

d. Sound working capital management requires an ample supply of cash so:

(1) A firm has sufficient cash to take trade discounts, discounts that suppliers offer customers for

e. A firm can synchronize its cash flows by arranging to bill customers and to pay their own bills on

regular “billing cycles” throughout the month. Synchronized cash flows reduce the cash balances,

decrease required bank loans, lower interest expenses, and boost profits.

f. SSP’s disbursement float is the amount of funds tied up in checks that have been written but are

still in process and have not yet been deducted from the store’s checking account balance by the

bank. SSP’s disbursement float is $50,000 and is calculated as 5 days x $10,000.

g. To speed up collections, a lockbox plan can be used. A firm arranges to have its customers send

payments to post office boxes in local areas. A local bank picks up the checks, has them cleared in

the local area, and then transfers the funds by wire to the company’s concentration bank. This is

not a practical solution for Smith because he only has one shop. To speed up his collections, he

needs to concentrate on recording them as soon as they come in each day and making a bank

deposit daily.

To slow down disbursements, many firms write checks on banks located in distant cities. Another

method would be to use drafts. A draft must be transmitted to the issuer, who approves it and

deposits funds to cover it, and then it can be collected. Again, neither of these methods is effective

for Smith; however, he can wait until the due date to pay his bills.

Some securities that are not suitable to hold as near-cash reserves are: U.S. Treasury notes and

bonds, corporate bonds, state and local government bonds, preferred stocks, common stocks of

other corporations, and the firm’s own common stock.

Integrative Problem 15-2

a. The variables that make up a firm’s credit policy are (1) credit standards, (2) credit terms, (3)

collection policy, and (4) monitoring function.

Credit terms refer to the conditions of the credit sale, including the length of time until payment is

due, whether a cash discount is available for early payment, and so on. If a firm offers a cash

discount for early payment, all else equal, the average balance of accounts receivable will decrease

if some customer take the cash discount—without the cash discount, these customers would wait

until the due date to make payment. If a firm increases the cash discount it offers, generally sales

will increase because the customers of competitors will be attracted to the new credit terms.

find (perhaps too late) that the cash flow pattern associated with collections of credit sales has

changed significantly.

b. ACP and DSO measure the same thing—the average length of time the firm must wait after making

a sale before receiving payment. DSO is the more preferred business nomenclature. Under the

current credit policy, the DSO is approximately 19 days:

c. Of the $3,600,000 in current sales 62.5 percent are affected by the discount. So,

DiscountsOld = 0.02 x $3,600,000 x 0.625 = $45,000

d. Analysis of the change:

Current Proposal

Annual amounts:

Sales $ 3,600,000 $ 4,000,000

Operating expenses (75%) $(2,700,000) $(3,000,000)

Cash discount $( 45,000) $( 87,000)

Required return, r 10% 10%

Daily amounts:

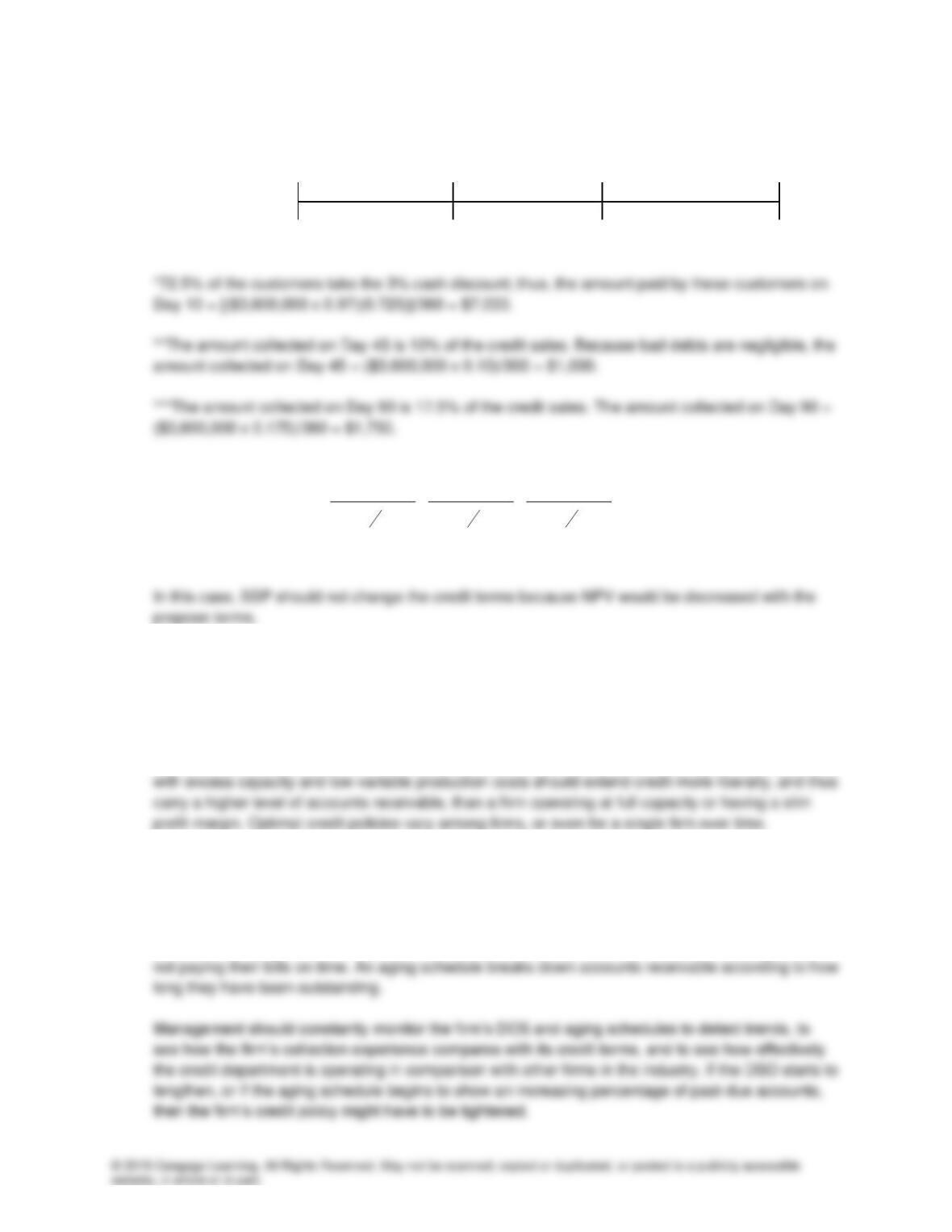

Current Policy:

(7,500) 6,125* 3,200** 550***

0

30

0.0278%

10

60

**The amount collected on Day 30 is 32% of the credit sales. Because bad debts are negligible, the

amount collected on Day 30 = [($3,600,000)(0.32)]/360 = ($10,000)0.32 = $3,200.

*** The amount collected on Day 60 is 5.5% of the credit sales. The amount collected on Day 60 =

[($3,600,000)(0.055)]/360 = ($10,000)0.055 = $550.

*72.5% of the customers take the 3% cash discount; thus, the amount paid by these customers on

Day 10 = [($4,000,000 x 0.97)(0.725)]/360 = $7,814.

**The amount collected on Day 45 is 10% of the credit sales. Because bad debts are negligible, the

amount collected on Day 45 = ($4,000,000 x 0.10)/360 = $1,111.

SSP should change the credit terms because NPV would be increased with the propose terms.

e. Current Proposal

Annual amounts:

Sales $ 3,600,000 $ 3,600,000

Operating expenses (75%) $(2,700,000) $(2,700,000)

Cash discount $( 45,000) $( 78,300)*

Required return, r 10% 10%

Proposed Policy:

(7,500) 7,033* 1,000** 1,750***

( ) ( ) ( )

Pr oposal 20 45 90

0.10 0.10 0.10

360 360 360

$7,033 $1,000 $1,750

NPV $(7,500) 1 1 1

$(7,500) $6,994 $988 $1,707 $2,289

= + + +

+ + +

= + + + =

g(1). To monitor a firm’s accounts receivable means to analyze the effectiveness of its credit policy in an

aggregate sense.

g(2). A firm would want to monitor its receivables because the optimal credit policy, and hence the

optimal level of accounts receivable, depends on the firm’s own unique operating conditions. A firm

g(3). The DSO and aging schedule can be used to monitor a firm’s accounts receivable. If the firm’s DSO

is higher than the industry average it means that the firm might have an excessive investment in

receivables (unless of course it is a case of excess capacity and low variable production costs, as

discussed earlier). Also, the firm’s DOS should be compared with the firm’s own credit policy. If the

firm’s DSO is longer than the maximum credit period, then the firm’s customers, on average, are

0

45

0.0278%

20

90

Integrative Problem 15-3

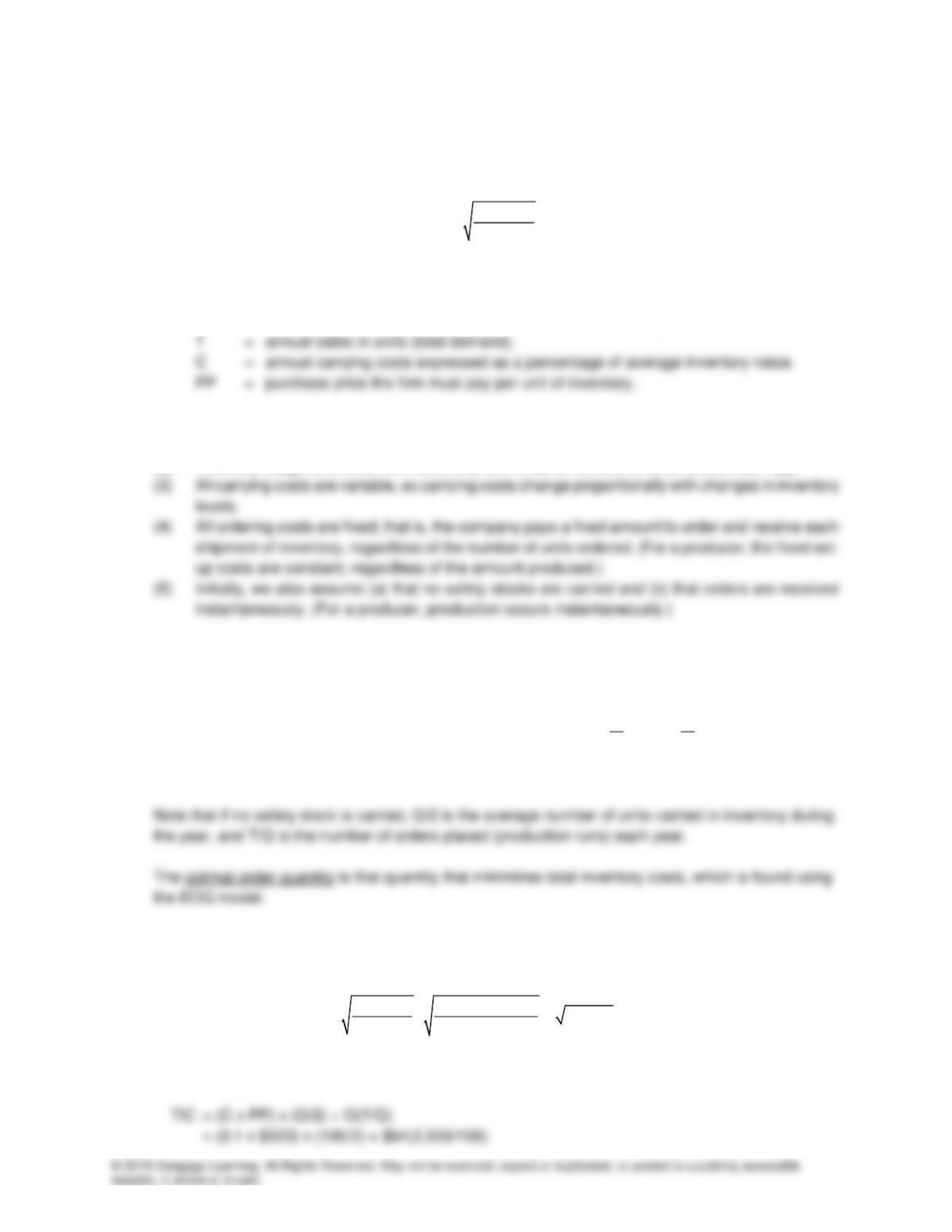

a. The EOQ model is written:

2 O T

EOQ = C PP

Where

EOQ = economic ordering quantity, or the optimum quantity to be ordered each time an order

is placed.

O = fixed costs of placing and receiving an order (set up cost per production run).

The standard form of the EOQ model requires the following assumptions:

(1) All values (a) are known with certainty and (b) are constant over time.

b. Under the assumptions listed above, total inventory costs (TIC) can be expressed as follows:

Total Total Total QT

Inventory = TIC = carrying + ordering = C PP + O

2Q

Costs costs costs

c. The EOQ and total inventory costs for the fly rods are:

2 O T 2 $64 2,500

EOQ = 10,000 = 100

C PP 0.1 $320

==

When 100 fly rods are ordered each time inventory is needed, total inventory costs equal:

d. 500 rods:

TIC = (C x PP) x (Q/2) + O(T/Q)

= (0.1 x $320) x (500/2) + $64(2,500/500)

= $32(250) + $64(5) = $8,000 + $320 = $8,320

Added cost = $8,320 – $3,200 = $5,120

Note the following points:

(1) At any order quantity other than EOQ = 100 units, total inventory costs are higher than they need

be.

(2) The added cost of not ordering the EOQ amount is not large if the quantity ordered is close to the

EOQ.

e. With an annual usage of 2,500 rods, SSP’s daily usage rate is 2,500/360 = 6.94 rods. If it takes three

days to receive an order, then SSP must order when its inventory of rods reaches 21 ≈ 6.94 x 3 days.

f. There are two ways to view the impact of safety stocks on total inventory costs. SSP’s total cost of

carrying the operating inventory is $3,200(see part c). Now the cost of carrying an additional 50 fly rods

is (C x PP)(Safety stock) = 0.1($320)(50) = $1,600. Thus, total inventory costs are increased by $1,600,

for a total of $3,200 + $1,600 = $4,800.

h(1). Just-In-Time (JIT) procedures are designed specifically to reduce inventories. If a JIT system were

put in place, it probably would obviate the need for using the EOQ model. The JIT system allows a

h(2). Air freight presumably would shorten delivery times and reduce the need for safety stocks. It might

or might not affect the EOQ.