CFIN6 – CHAPTER 14

INTEGRATIVE PROBLEM SOLUTION

Integrative Problem 14-1

a.

()

Inventory Inventory $1,000

Conversion 97.3 days

$3,700

Cost of goods sold per day

Period 360

= = =

Payables deferral period = 29 days (given in problem).

Cash conversion cycle = 111.5 days:

Cash Inventory Receivables Payables

Conversion Conversion Collection Deferral

Cycle Period Period Period

97.3 days 43.2 days – 29.0 days 111.5 days

= + −

= + =

(1) Industry average inventory conversion period = 360/5.4 = 66.7 days.

(2) Industry average receivables collection period = 30 days.

b. To focus on NYF’s current working capital policy, one should examine its DSO, its accounts receivable

turnover, its inventory turnover, its current ratio, and its quick ratio—which are all poor when compared

to the industry average ratios. NYF’s DSO is 44 percent higher than the industry average DSO. NYF’s

DSO should be compared to the terms on which the firm sells goods. This information has not been

pay off current obligations.

Finally, a review of these ratios suggests that NYF’s working capital policy is worse than that of the

average firm in its industry.

Integrative Problem 14-2

a. Short-term credit is any liability originally scheduled for payment within one year. The four major

sources of short-term credit are: accruals, accounts payable, commercial bank loans, and commercial

paper.

d(1). If Dellvoe’s gross purchases are $50,000 annually, then, with a 2 percent discount, its net purchases

are 0.98 ($50,000) = $49,000. If we assume a 360-day year, then net daily purchases are $49,000/360

= $136.11.

d(2). If the discount is taken, then Dellvoe must pay this supplier on Day 11 for purchases made on Day 1,

on Day 12 for purchases made on Day 2, and so on. Thus, in a steady state, Dellvoe will on average

have 10 days’ worth of purchases in payables, so,

Payables = 10($136.11) = $1,361.11.

d(3). To get $5,444.45 of costly trade credit Dellvoe must give up 0.02 ($50,000) = $1,000 in lost discounts

annually. Because the forgone discounts pay for $5,444.45 of credit, the APR is 18.37 percent:

$1,000

APR 0.1837 18.4%

$5,444.45

= =

Following is a formula that can be used to find the approximate cost rate of costly trade credit:

Note that (1) the formula gives the same cost rate as was calculated earlier, (2) the first term is the

periodic cost of the credit (Dellvoe spends $2 to get the use of $98), and (3) the second term is the

number of “savings periods” per year (Dellvoe delays payment for 50 – 10 = 40 days, and there are

360/40 = 9 40-day periods in a year.)

The effective annual rate is 19.94%:

m9

Discount % 0.02

EAR 1 + 1 = 1 + – 1 = 0.1994 = 19.94%

1 – Discount % 0.98

=−

e(1). With a simple interest loan, Dellvoe gets the full use of the $800,000 for a year, and then pays

0.09($800,000) = $72,000 in interest at the end of the term, along with the $800,000 principal

repayment. For a one-year simple interest loan, the simple rate, 9 percent, is also the effective annual

rate.

Effective rate = (1.04)2 – 1.0 = 0.0816 = 8.16%.

In general, the shorter the maturity (within a year), the higher the effective cost of a simple interest

loan.

$72,000

EAR 0.0989 9.9%

$728,000

= = =

Note that a formula also can be used for a one-year discount loan:

Finally, if Dellvoe needed the use of $800,000 for the year, then the face amount of the loan must be:

SIMPLE

Amount needed $800,000 $800,000

Principal $879,121

1 r 1 0.09 0.91

= = = =

−−

Then, the bank would discount the loan by 0.09($879,121) = $79,121, and the firm would receive the

needed $800,000.

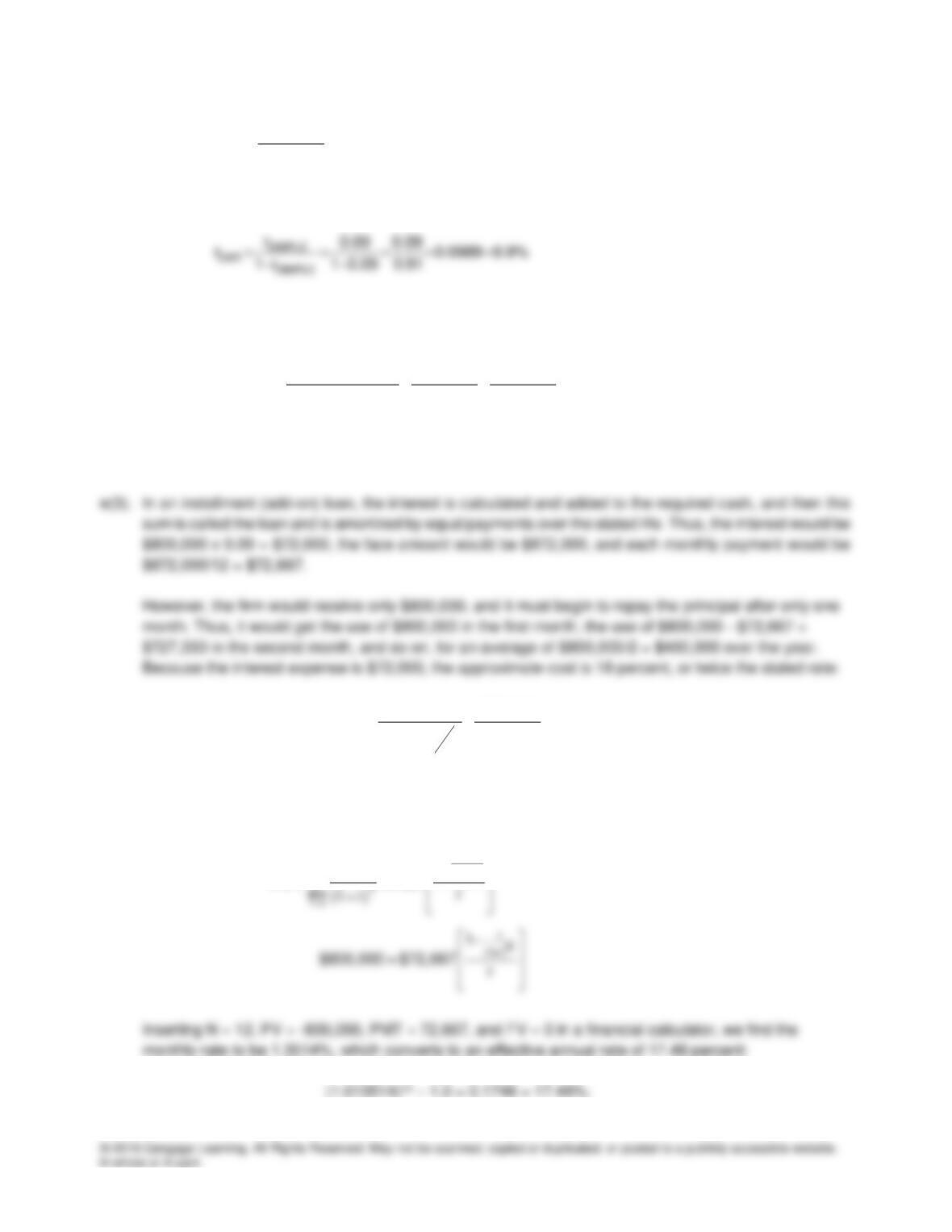

( )

Interest $72,000

Approximate cost 0.18 18.0%

Principal $400,000

2

= = = =

To find the exact effective annual rate, recognize that Dellvoe has received $800,000 and must make

monthly payments of $72,667:

1

NN

(1 r)

1

PMT

+

−

e(4). Dellvoe must obtain a loan of $1,000,000:

Amount needed $800,000 $800,000

Principal $1,000,000

1 Compensating balance 1 0.20 0.80

= = = =

−−

Thus, 0.2($1,000,000) = $200,000 must remain at the bank as a compensating balance; so the firm

only receives $800,000, and it must pay back the $1,000,000 plus 0.09($1,000,000) = $90,000 in

SIMPLE

EAR

r0.09 0.09

r 0.1125 11.25%

1 Compensating balance % 1 0.20 0.80

= = = = =

−−

e(5). If the loan is a discount loan, and also has a compensating balance requirement, then Dellvoe must

borrow $1,126,761:

Amount needed $800,000 $800,000

( )

SIMPLE

EAR

SIMPLE

r0.09 0.09

r 0.1268 12.68%

Compensating 1 0.09 0.20 0.71

1r balance %

= = = = =

−−

−−

e(6). (i) This formula can be used to determine the size of the required loan:

1 0.20 0.80

−

Note that the total cash in the account, after the $800,000 has been spent, will be $175,000 =

EAR $78,750

r 0.0984 9.84%

$800,000

= = =

Versus 11.25 percent if it had to borrow the entire amount of the compensating balance.

f. A secured loan is one backed by collateral, often inventories or receivables.

department and assume the risk of default on bad accounts. The cost of pledging receivables is less

expensive than factoring receivables. When receivables are pledged, the firm maintains its own credit

department and assumes the risk of default on bad accounts, rather than the bank (as in the case of

factoring).

h. The three forms of inventory financing discussed in the text are blanket liens, trust receipts, and

nonperishable. Warehouse financing can be done through a public warehouse or a field warehouse. If

the inventory is bulky and transportation to and from premises is expensive, then a field warehouse is

used rather than a public warehouse. Finally, the fixed costs of field warehousing arrangements are

relatively high, so this type of financing is not suitable for a very small firm.

i. Interest Commitment

Month Borrowings Charges* Fee**

January $925,000 $ 7,708 $ 63

Interest charges $16,458

Commitment fees 855

Total cost $17,313

Average three-month rate = Cost/(Average loan amount)

= $17,313/[($925,000 + $625,000 + $425,000)/3]

= $17,313/$658,333 = 0.0263