CFIN6 – CHAPTER 13

INTEGRATIVE PROBLEM SOLUTION

a(1). Dividend policy is defined as the firm’s policy with regard to paying out earnings as dividends

versus retaining them for reinvestment in the firm. Dividend policy really involves two issues: (1)

the dollar amount of dividends to be paid out in the near future, say the next year, and (2) the

long-run policy regarding the average percentage of earnings to be paid out to stockholders.

a(2). Dividend irrelevance refers to the theory that investors are indifferent between dividends and capital

gains, making dividend policy irrelevant with regard to its effect on the value of the firm. On the

other hand, according to the dividend relevance theory, dividend policy can affect the value of a firm

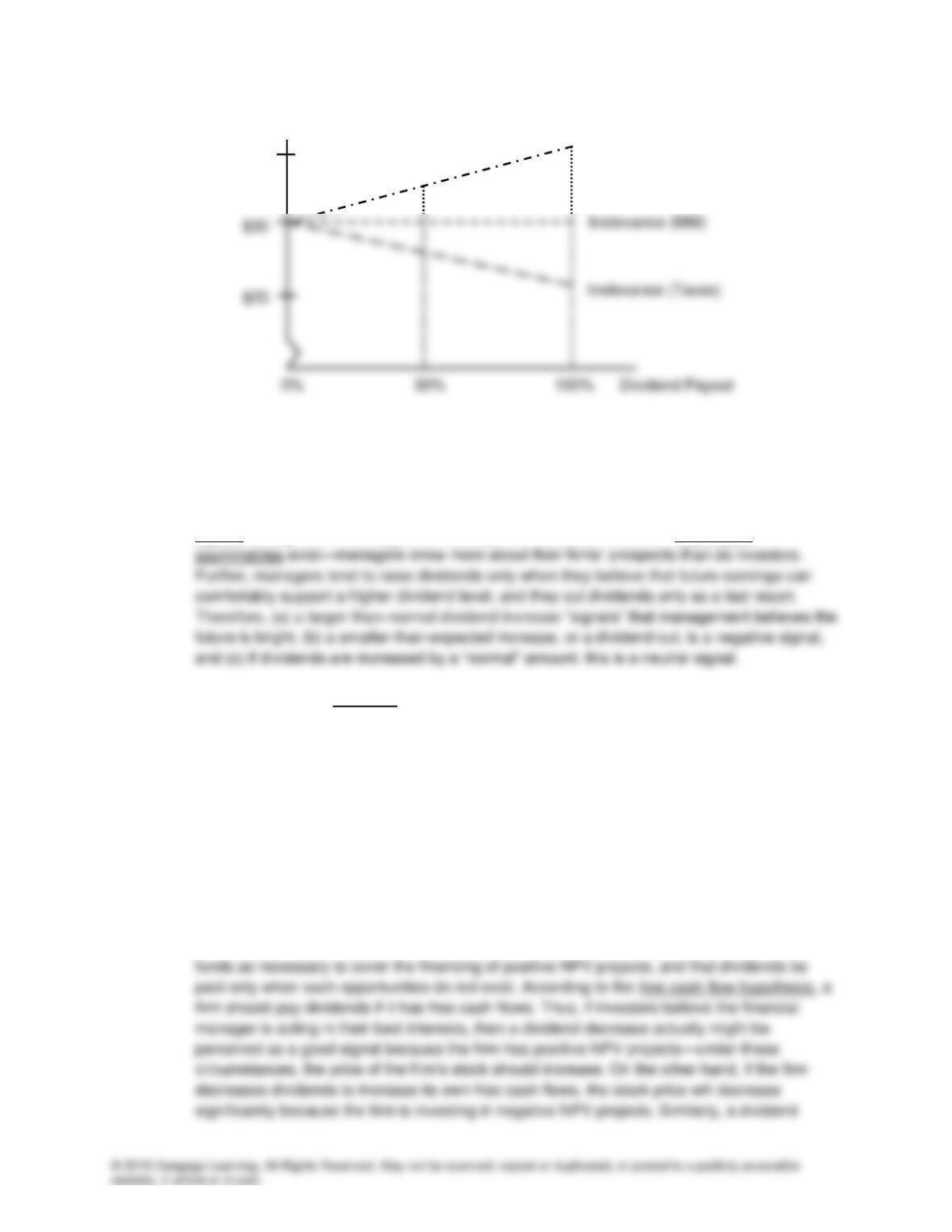

a(3). In the graph given here we plot stock price versus dividend policy (payout) under the dividend

relevance theory and dividend irrelevance when investors prefer current dividends (GL) and when

investors prefer to delay tax payments associated with their investment (taxes). It is assumed that a

zero percent payout produces a stock price of $30. If the dividend irrelevance theory (MM) is

correct, then the stock price will remain constant at $30 regardless of whether the firm retains all

Irrelevance (MM)

Irrelevance (Taxes)

b. (1) It has long been recognized that the announcement of a dividend increase often results in an

increase in the stock price, while an announcement of a dividend cut typically causes the

stock price to fall. One could argue that this observation supports the premise that investors

prefer dividends to capital gains. However, MM argued that dividend announcements are

signals through which management conveys information to investors. Information

(2) Different groups, or clienteles, of stockholders prefer different dividend payout policies. For

example, many retirees, pension funds, and university endowment funds are in a low (or

zero) tax bracket, and they have a need for current cash income. Therefore, this group of

stockholders might prefer high payout stocks. These investors could, of course, sell some of

their stock, but this would be inconvenient, transactions costs would be incurred, and the sale

might have to be made in a down market. Conversely, investors in their peak earnings years

who are in high tax brackets and who have no need for current cash income should prefer

low payout stocks.

(3) Investors expect financial managers to make decisions that help maximize the value of the

firm. If positive net present value capital budgeting projects are available for current

investment, the firm should invest in these projects. Thus, if investors want wealth

maximization, they should prefer the financial manager uses as much internally generated

Relevance (GL)

Price

$40

(4) Firms are aware of these “hypotheses” when selecting dividend policies. For example,

evidence indicates that most firms are very reluctant to cut dividends, even if they have to

borrow to make the payments. Likewise, firms generally increase dividends only when they

are sure operations can support the increase long into the future.

c(1). The following graph shows that the WACC as is WACC1 as long as only retained earnings

are used. Once new stock must be sold, the MCC rises to WACC2. The break point occurs at

a capital budget level equal to (net income/% equity) = $600,000/0.6 = $1 million. As a result,

if it strictly follows the residual dividend policy, ISI should retain $480,000 = $800,000(0.6) of

c(2). A change in investment opportunities would either increase or decrease the amount of equity

needed, hence in the residual dividend payout.

c(3). The primary advantage of the residual policy is that under it the firm makes maximum use of lower

cost retained earnings, thus minimizing flotation costs and hence the cost of capital. Also, whatever

negative signals are associated with stock issues would be avoided.

d. Three other dividend payment policies are (1) pay a stable, predictable dollar dividend, (2) pay out a

constant percentage of earnings, and (3) pay a low regular dividend plus an extra when funds are

available. Note: in virtually all cases, an annual dividend is set, but then paid in 4 quarterly

installments.

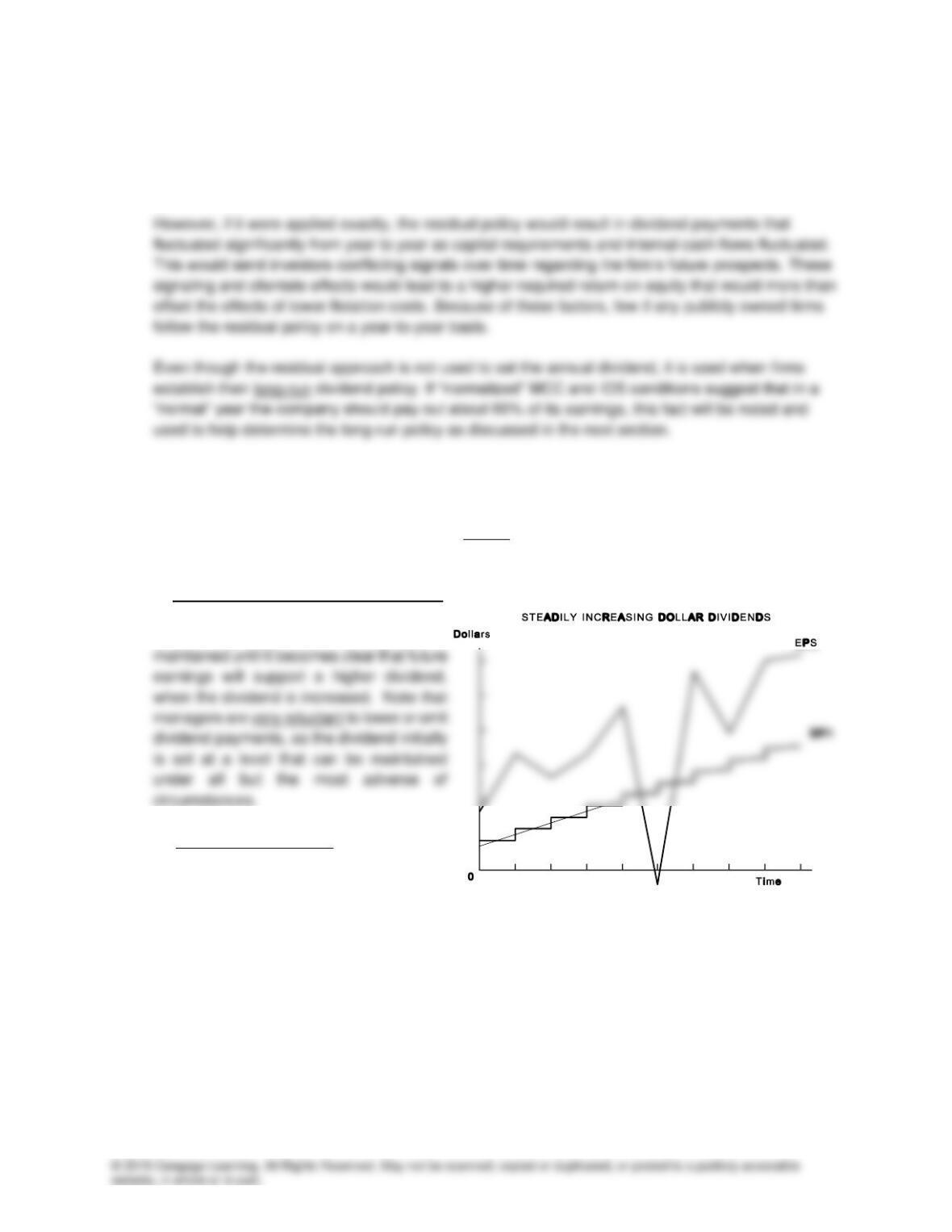

1. Stable, predictable dollar dividend policy.

Here the firm sets a specific annual dollar

dividend per share, and this payment is

2. Constant payout ratio. This policy is

followed when a firm sets a constant payout

ratio and then lets its dividend fluctuate with earnings.

3. Low regular plus extras policy. Here a

firm would set a constant or steadily

increasing payment policy as discussed

The constant payout ratio policy creates fluctuating dollar dividends, hence (1) sends mixed signals

about future earnings expectations and (2) is not appealing to many clienteles.

The low regular plus extras policy has advantages similar to the stable, predictable dollar dividend

policy, but, because the dollar amount is low, there is less risk that the firm will be forced into

undesirable actions just to meet the dividend payment. From an investor’s viewpoint, though, cash

flows are less dependable than under the stable, predictable dollar dividend policy.

Because of its disadvantages, few firms today follow the constant payout ratio policy. Low growth firms

with relatively stable, or steadily growing, earnings generally follow the stable, predictable dividend

policy. Cyclical firms with volatile earnings tend to use the low regular plus extras policy.

f. When it uses a stock dividend, a firm issues new shares in lieu of paying a cash dividend. For

example, in a 5% stock dividend, the holder of 100 shares would receive an additional 5 shares. In

a stock split, the number of shares outstanding is increased (or decreased in a reverse split) in an

action unrelated to a dividend payment. For example, in a 2-for-1 split, the number of shares

of higher earnings, then one would expect the price of the stock to adjust such that each investor’s

wealth remains unchanged. For example, a 2-for-1 split of a stock selling for $50 would result in the

stock price being cut in half, to $25.

It is hard to come up with a convincing rationale for small stock dividends, like 5percent or 10%. No

economic value is being created or distributed, yet stockholders have to bear the administrative

outside the $20 to $80 range, but most stay within it.

Another factor that might influence stock splits and dividends is the belief that they signal

management’s belief that the future is bright. If a firm’s management would be inclined to split the

stock or pay a stock dividend only if it anticipated improvements in earnings and dividends, then a

split/dividend action could provide a positive signal and thus boost the stock price. However, if

1. Distribute excess funds to stockholders. Firms sometimes use stock repurchases to distribute

funds that exceed capital budgeting needs in a particular year, especially when the price of

the stock is considered low (undervalued).

2. Adjust the firm’s capital structure. When a firm has more equity than its target capital

soon, it might buy back shares in the financial markets to ensure that sufficient shares are

available when the options are exercised.

4. Protect against a takeover attempt. A stock repurchase can be used to fend off a hostile

takeover attempt because (a) repurchasing stock increases demand in the stock markets,

The principal advantages of repurchases include:

1. A company can use a stock repurchase to distribute excess cash (free cash flows) without

increasing the amount of dividends that is paid during the year. Most firms are reluctant to

increase dividend payments unless management is confident that future operations can

the “dilution effect” associated with exercising the options.

4. Stockholders do not have to sell their shares to the company during a repurchase period.

Thus, those investors who need cash and don’t mind paying the taxes associated with selling

their stock will participate in the repurchase program; other stockholders will not.

The principal disadvantages of stock repurchases include:

1. The company might pay too much for stock that is repurchased. A firm that buys back

substantial amounts of its stock will bid up the per share price of the stock that remains

outstanding, perhaps to an artificially high level.