181

Chapter 12

Estimating the Cost of Capital

12–1. Suppose Pepsico’s stock has a beta of 0.57. If the risk-free rate is 3% and the expected return of

the market portfolio is 8%, what is Pepsico’s equity cost of capital?

12–2. Suppose the market portfolio has an expected return of 10% and a volatility of 20%, while

Microsoft’s stock has a volatility of 30%.

a. Given its higher volatility, should we expect Microsoft to have an equity cost of capital that is

higher than 10%?

b. What would have to be true for Microsoft’s equity cost of capital to be equal to 10%?

12–3. Aluminum maker Alcoa has a beta of about 2.0, whereas Hormel Foods has a beta of 0.45. If the

expected excess return of the marker portfolio is 5%, which of these firms has a higher equity

cost of capital, and how much higher is it?

12–4. Suppose all possible investment opportunities in the world are limited to the five stocks listed in

the table below. What does the market portfolio consist of (what are the portfolio weights)?

182 Berk/DeMarzo, Corporate Finance, Fourth Edition

Stock

Portfolio Weight

12–5. Using the data in Problem 4, suppose you are holding a market portfolio, and have invested

$12,000 in Stock C.

a. How much have you invested in Stock A?

b. How many shares of Stock B do you hold?

c. If the price of Stock C suddenly drops to $4 per share, what trades would you need to make

to maintain a market portfolio?

12–6. Suppose Best Buy stock is trading for $30 per share for a total market cap of $9 billion, and Walt

Disney has 1.65 billion shares outstanding. If you hold the market portfolio, and as part of it hold

100 shares of Best Buy, how many shares of Walt Disney do you hold?

12–7. Standard and Poor’s also publishes the S&P Equal Weight Index, which is an equally weighted

version of the S&P 500.

a. To maintain a portfolio that tracks this index, what trades would need to be made in

response to daily price changes?

b. Is this index suitable as a market proxy?

12–8. Suppose that in place of the S&P 500, you wanted to use a broader market portfolio of all U.S.

stocks and bonds as the market proxy. Could you use the same estimate for the market risk

premium when applying the CAPM? If not, how would you estimate the correct risk premium to

use?

12–9. From the start of 1999 to the start of 2009, the S&P 500 had a negative return. Does this mean

the market risk premium we should have used in the CAPM was negative?

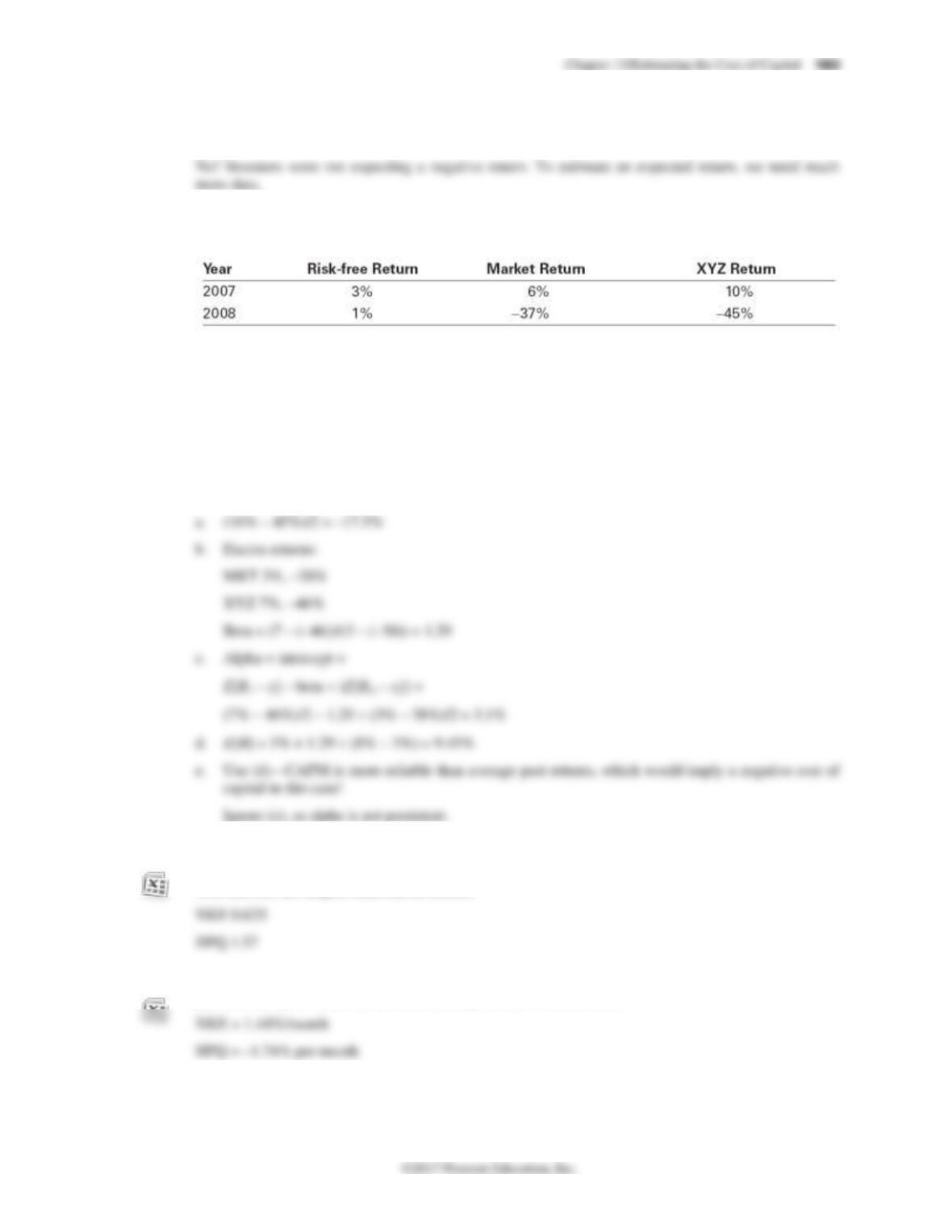

12-10. You need to estimate the equity cost of capital for XYZ Corp. You have the following data

available regarding past returns:

a. What was XYZ’s average historical return?

b. Compute the market’s and XYZ’s excess returns for each year. Estimate XYZ’s beta.

c. Estimate XYZ’s historical alpha.

d. Suppose the current risk-free rate is 3%, and you expect the market’s return to be 8%. Use

the CAPM to estimate an expected return for XYZ Corp.’s stock.

e. Would you base your estimate of XYZ’s equity cost of capital on your answer in part (a) or

in part (d)? How does your answer to part (c) affect your estimate? Explain.

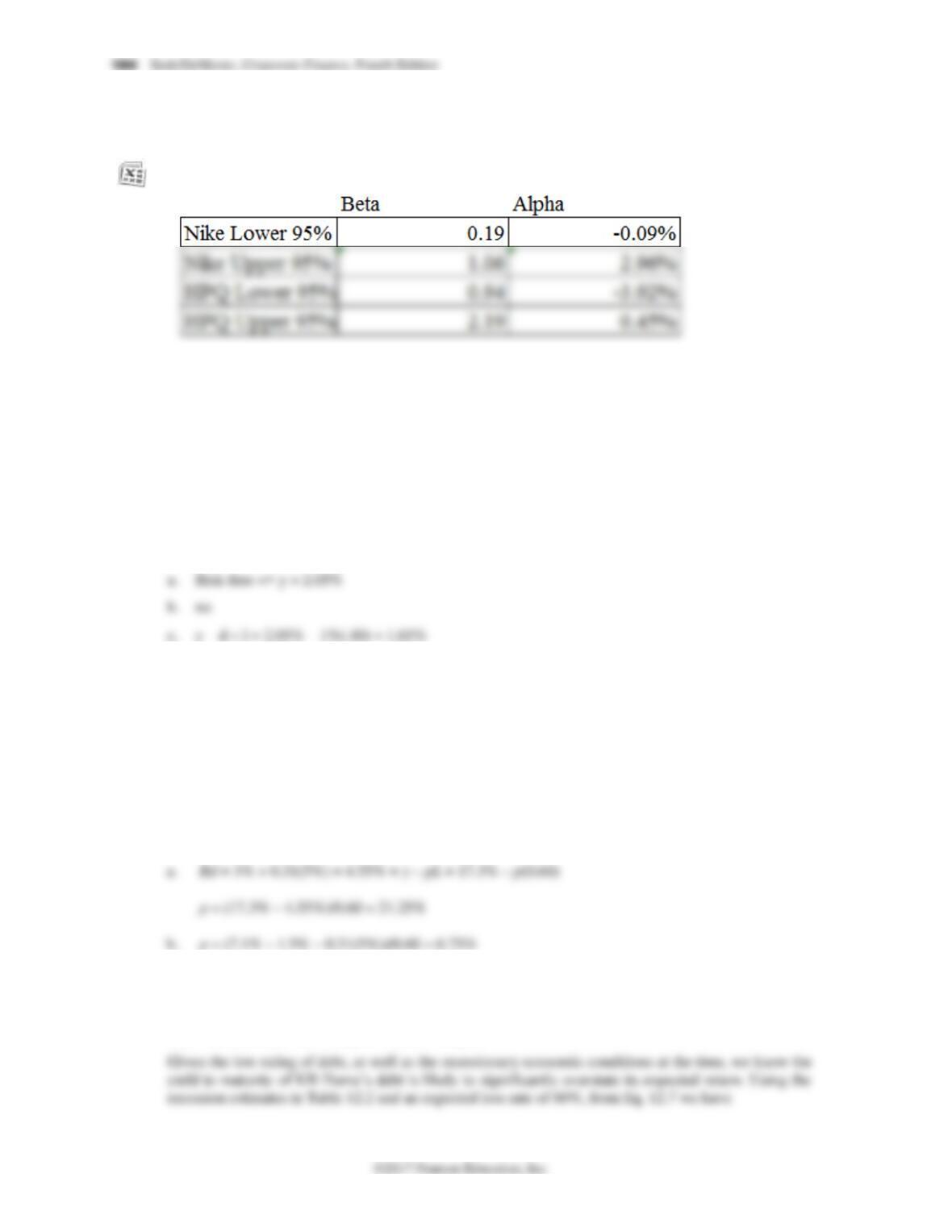

12-11. Go to Chapter Resources on MyFinanceLab and use the data in the spreadsheet provided to

estimate the beta of Nike and HPQ stock based on their monthly returns from 2011–2015. (Hint:

You can use the slope() function in Excel.)

12-12. Using the same data as in Problem 11, estimate the alpha of Nike and HPQ stock, expressed as %

per month. (Hint: You can use the intercept() function in Excel.)

12-13. Using the same data as in Problem 11, estimate the 95% confidence interval for the alpha and

beta of Nike and HPQ stock using Excel’s regression tool (from the data analysis menu) or the

linest() function.

12-14. In mid-2012, Ralston Purina had AA-rated, 10-year bonds outstanding with a yield to maturity

of 2.05%.

a. What is the highest expected return these bonds could have?

b. At the time, similar maturity Treasuries have a yield of 1.5%. Could these bonds actually

have an expected return equal to your answer in part (a)?

c. If you believe Ralston Purina’s bonds have 1% chance of default per year, and that expected

loss rate in the event of default is 40%, what is your estimate of the expected return for these

bonds?

12-15. In mid-2009, Rite Aid had CCC-rated, 6-year bonds outstanding with a yield to maturity of

17.3%. At the time, similar maturity Treasuries had a yield of 3%. Suppose the market risk

premium is 5% and you believe Rite Aid’s bonds have a beta of 0.31. The expected loss rate of

these bonds in the event of default is 60%.

a. What annual probability of default would be consistent with the yield to maturity of these

bonds in mid-2009?

b. In mid-2015, Rite-Aid’s bonds had a yield of 7.1%, while similar maturity Treasuries had a

yield of 1.5%. What probability of default would you estimate now?

12-16. During the recession in mid-2009, homebuilder KB Home had outstanding 6-year bonds with a

yield to maturity of 8.5% and a BB rating. If corresponding risk-free rates were 3%, and the

market risk premium was 5%, estimate the expected return of KB Home’s debt using two

different methods. How do your results compare?

Chapter 12/Estimating the Cost of Capital 185

12-17. The Dunley Corp. plans to issue 5-year bonds. It believes the bonds will have a BBB rating.

Suppose AAA bonds with the same maturity have a 4% yield. Assume the market risk premium

is 5% and use the data in Table 12.2 and Table 12.3.

a. Estimate the yield Dunley will have to pay, assuming an expected 60% loss rate in the event

of default during average economic times. What spread over AAA bonds will it have to pay?

b. Estimate the yield Dunley would have to pay if it were a recession, assuming the expected

loss rate is 80% at that time, but the beta of debt and market risk premium are the same as

in average economic times. What is Dunley’s spread over AAA now?

c. In fact, one might expect risk premia and betas to increase in recessions. Redo part (b)

assuming that the market risk premium and the beta of debt both increase by 20%; that is,

they equal 1.2 times their value in recessions.

12-18. Your firm is planning to invest in an automated packaging plant. Harburtin Industries is an all–

equity firm that specializes in this business. Suppose Harburtin’s equity beta is 0.85, the risk–free

rate is 4%, and the market risk premium is 5%. If your firm’s project is all equity financed,

estimate its cost of capital.

12-19. Consider the setting of Problem 18. You decided to look for other comparables to reduce

estimation error in your cost of capital estimate. You find a second firm, Thurbinar Design,

which is also engaged in a similar line of business. Thurbinar has a stock price of $20 per share,

186 Berk/DeMarzo, Corporate Finance, Fourth Edition

with 15 million shares outstanding. It also has $100 million in outstanding debt, with a yield on

the debt of 4.5%. Thurbinar’s equity beta is 1.00.

a. Assume Thurbinar’s debt has a beta of zero. Estimate Thurbinar’s unlevered beta. Use the

unlevered beta and the CAPM to estimate Thurbinar’s unlevered cost of capital.

b. Estimate Thurbinar’s equity cost of capital using the CAPM. Then assume its debt cost of

capital equals its yield, and using these results, estimate Thurbinar’s unlevered cost of

capital.

c. Explain the difference between your estimate in part (a) and part (b).

d. You decide to average your results in part (a) and part (b), and then average this result with

your estimate from Problem 17. What is your estimate for the cost of capital of your firm’s

project?

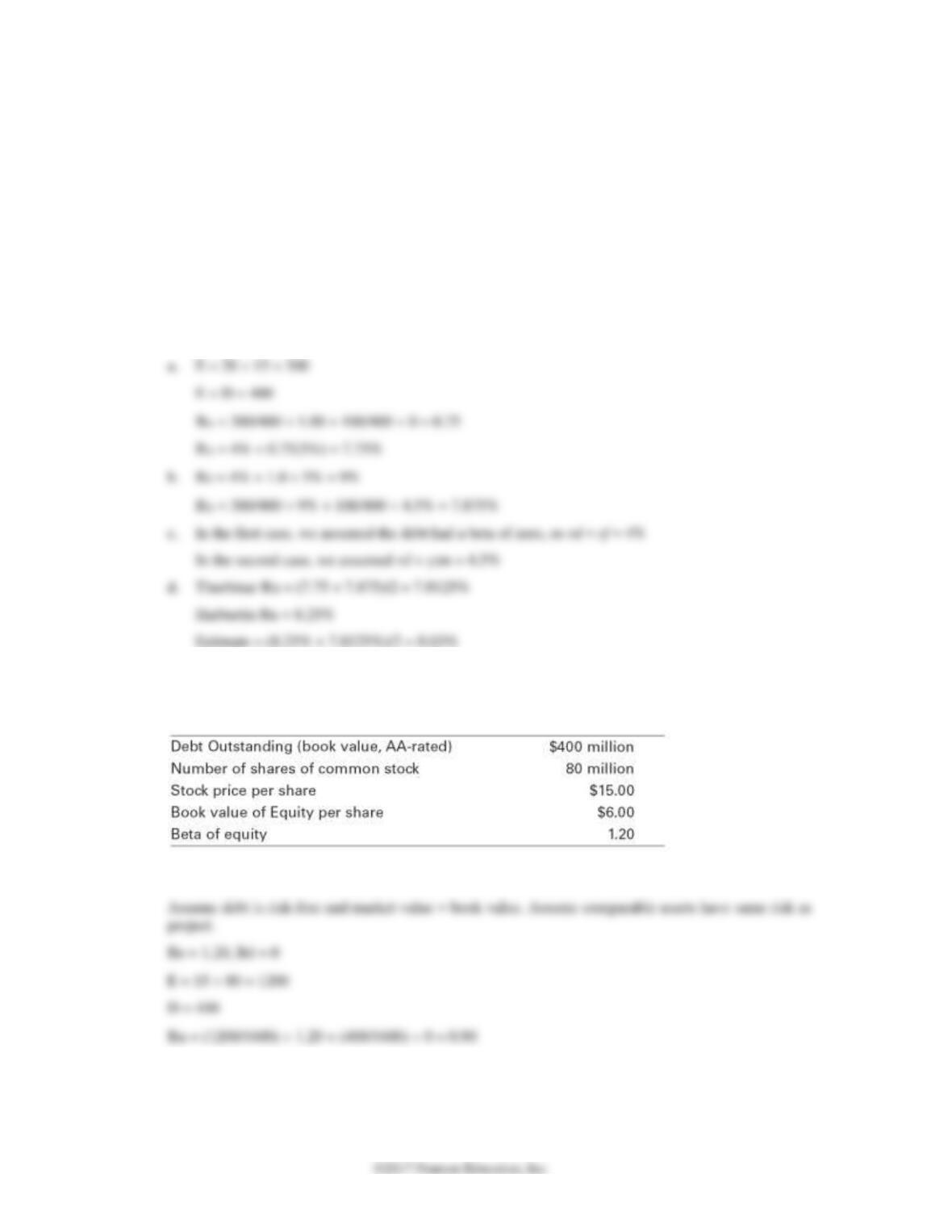

12-20. IDX Tech is looking to expand its investment in advanced security systems. The project will be

financed with equity. You are trying to assess the value of the investment, and must estimate its

cost of capital. You find the following data for a publicly traded firm in the same line of business:

What is your estimate of the project’s beta? What assumptions do you need to make?

12-21. In mid-2015, Cisco Systems had a market capitalization of $130 billion. It had A-rated debt of

$25 billion as well as cash and short-term investments of $60 billion, and its estimated equity

beta at the time was 1.11.

Chapter 12/Estimating the Cost of Capital 187

a. What is Cisco’s enterprise value?

b. Assuming Cisco’s debt has a beta of zero, estimate the beta of Cisco’s underlying business

enterprise.

12-22. Consider the following airline industry data from mid-2009:

Company Name

Market

Capitalization

($mm)

Total Enterprise

Value ($mm)

Equity Beta

Debt Ratings

Delta Air Lines (DAL)

4,938.5

17,026.5

2.04

BB

Southwest Airlines (LUV)

4,896.8

6,372.8

0.966

A/BBB

JetBlue Airways (JBLU)

1,245.5

3,833.5

1.91

B/CCC

Continental Airlines (CAL)

1,124.0

4,414.0

1.99

B

a. Use the estimates in Table 12.3 to estimate the debt beta for each firm (use an average if

multiple ratings are listed).

b. Estimate the asset beta for each firm.

c. What is the average asset beta for the industry, based on these firms?

Company Name

Ma rket Capita li zati on

($ mm)

Tota l En te r prise

Valu e ($ mm) 2 Year Beta

Debt

Rati ngs Deb t beta asset beta

12-23. Weston Enterprises is an all-equity firm with three divisions. The soft drink division has an asset

beta of 0.60, expects to generate free cash flow of $50 million this year, and anticipates a 3%

perpetual growth rate. The industrial chemicals division has an asset beta of 1.20, expects to

generate free cash flow of $70 million this year, and anticipates a 2% perpetual growth rate.

Suppose the risk-free rate is 4% and the market risk premium is 5%.

a. Estimate the value of each division.

b. Estimate Weston’s current equity beta and cost of capital. Is this cost of capital useful for

valuing Weston’s projects? How is Weston’s equity beta likely to change over time?

a. Soft drink

188 Berk/DeMarzo, Corporate Finance, Fourth Edition

b. Weston Beta (portfolio)

12-24. Harrison Holdings, Inc. (HHI) is publicly traded, with a current share price of $32 per share.

HHI has 20 million shares outstanding, as well as $64 million in debt. The founder of HHI, Harry

Harrison, made his fortune in the fast food business. He sold off part of his fast-food empire, and

purchased a professional hockey team. HHI’s only assets are the hockey team, together with

50% of the outstanding shares of Harry’s Hotdogs restaurant chain. Harry’s Hotdogs (HDG) has

a market capitalization of $850 million, and an enterprise value of $1.05 billion. After a little

research, you find that the average asset beta of other fast-food restaurant chains is 0.75. You

also find that the debt of HHI and HDG is highly rated, and so you decide to estimate the beta of

both firms’ debt as zero. Finally, you do a regression analysis on HHI’s historical stock returns

in comparison to the S&P 500, and estimate an equity beta of 1.33. Given this information,

estimate the beta of HHI’s investment in the hockey team.

12-25. Your company operates a steel plant. On average, revenues from the plant are $30 million per

year. All of the plants costs are variable costs and are consistently 80% of revenues, including

energy costs associated with powering the plant, which represent one quarter of the plant’s costs,

or an average of $6 million per year. Suppose the plant has an asset beta of 1.25, the risk-free

rate is 4%, and the market risk premium is 5%. The tax rate is 40%, and there are no other

costs.

a. Estimate the value of the plant today assuming no growth.

b. Suppose you enter a long–term contract which will supply all of the plant’s energy needs for

a fixed cost of $3 million per year (before tax). What is the value of the plant if you take this

contract?

c. How would taking the contract in (b) change the plant’s cost of capital? Explain.

Chapter 12/Estimating the Cost of Capital 189

12-26. Unida Systems has 40 million shares outstanding trading for $10 per share. In addition, Unida

has $100 million in outstanding debt. Suppose Unida’s equity cost of capital is 15%, its debt cost

of capital is 8%, and the corporate tax rate is 40%.

a. What is Unida’s unlevered cost of capital?

b. What is Unida’s after-tax debt cost of capital?

c. What is Unida’s weighted average cost of capital?

12-27. You would like to estimate the weighted average cost of capital for a new airline business. Based

on its industry asset beta, you have already estimated an unlevered cost of capital for the firm of

9%. However, the new business will be 25% debt financed, and you anticipate its debt cost of

capital will be 6%. If its corporate tax rate is 40%, what is your estimate of its WACC?