CHAPTER 11 CASE C-1

CHAPTER 12

THE FAMA-FRENCH MULTI-FACTOR

MODEL AND MUTUAL FUND RETURNS

NOTE: The example below shows the results for returns between October 2010 and September 2015.

The actual answer to the case will change based on current market conditions.

1. For a large-company stock fund, we would expect the beta for the market risk premium to be near one

since large company returns account for a large part of the total market return on a market-value basis.

2.

Fidelity Magellan:

Regression Statistics

Multiple R

0.976262394

R Square

0.953088261

Square

0.950575133

Standard Error

0.008714563

Observations

Regression

Residual

Total

Intercept

SMB

HML

Adjusted R

CHAPTER 11 CASE C-2

Fidelity Low-Priced Stock Fund:

Regression Statistics

Multiple R

0.97094

R Square

0.94273

Adjusted R

Coefficients

Standard

Error

t Stat

P-value

Intercept

0.00065

0.00119

0.54383

0.58871

0.95742

0.03530

0.00000

SMB

0.11224

0.05711

1.96550

0.05432

HML

0.09351

0.06283

1.48837

0.14226

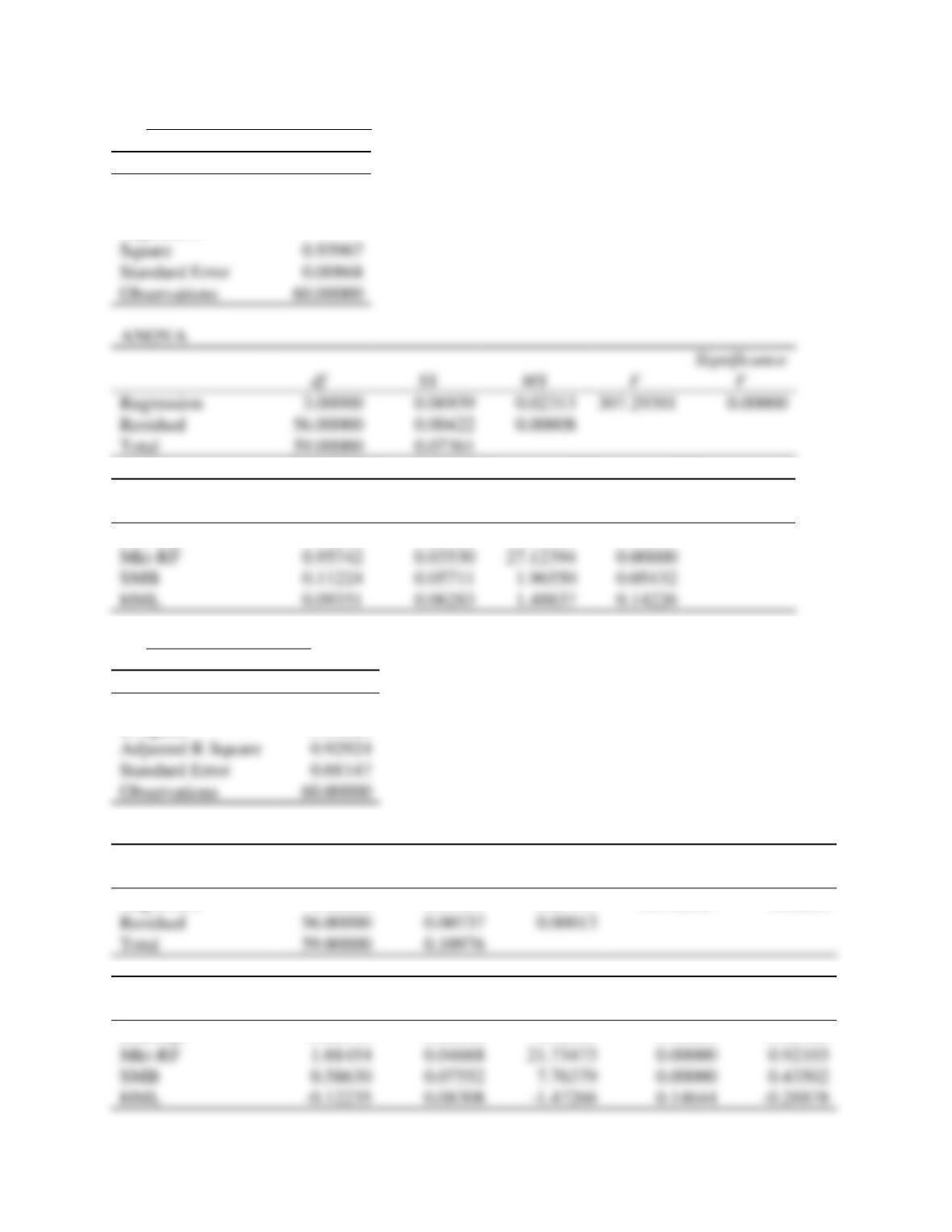

Baron Small Cap Fund:

Regression Statistics

Multiple R

0.96584

R Square

0.93284

Adjusted R Square

0.92924

Standard Error

0.01147

Observations

ANOVA

df

SS

MS

F

Significance

F

Regression

3.00000

0.10239

0.03413

259.28367

0.00000

Residual

0.00737

0.00013

Total

0.10976

Coefficients

Standard

Error

t Stat

P-value

Lower 95%

Intercept

-0.00147

0.00158

-0.92967

0.35653

-0.00463

1.01454

0.04668

0.00000

0.92103

SMB

0.58630

0.07552

7.76379

0.00000

0.43502

HML

-0.12235

0.08308

-1.47266

0.14644

-0.28878

Square

0.93967

Standard Error

0.00868

Observations

ANOVA

Regression

3.00000

0.06939

0.02313

Residual

0.00422

0.00008

Total

0.07361

CHAPTER 11 CASE C-3

4. If the market is efficient, all assets should have an alpha of zero. In this case, none of the three funds

5. Once adjusting for risk, we cannot say any of these three funds performed better since all three alphas