Answers and Solutions: 12 – 1

Chapter 12

Corporate Valuation and Financial Planning

ANSWERS TO END-OF-CHAPTER QUESTIONS

12-1 a. The operating plan provides detailed implementation guidance designed to accomplish

corporate objectives. It details who is responsible for what particular function, and

when specific tasks are to be accomplished. The financial plan details the financial

aspects of the corporation’s operating plan.

b. Spontaneous liabilities are the first source of expansion capital as these accounts

payout ratio is calculated as dividends per share divided by earnings per share. The

less of its income a company distributes as dividends, the larger its addition to retained

earnings. Therefore, the firm’s need for external financing will be lower.

c. Additional funds needed (AFN) are those funds required from external sources to

increase the firm’s assets to support a sales increase. A sales increase will normally

require an increase in assets. However, some of this increase is usually offset by a

spontaneous increase in liabilities as well as by earnings retained in the firm. Those

funds that are required but not generated internally must be obtained from external

d. The forecasted financial statement approach using percent of sales develops a complete

set of financial statements that can be used to calculate projected EPS, free cash flow,

various other financial ratios, and a projected stock price. This approach first forecasts

sales, the required assets, the funds that will be spontaneously generated, and then net

income, dividends, and retained earnings.

Answers and Solutions: 12 – 3

12-2 Accounts payable, accrued wages, and accrued taxes increase spontaneously. Retained

earnings may or may not increase, depending on profitability and dividend payout policy.

12-3 The equation gives good forecasts of financial requirements if the ratios A0*/S and L0*/S,

the profit margin, and payout ratio are stable. This equation assumes that ratios are

12-4 The five key factors that impact a firm’s external financing requirements are: Sales growth,

capital intensity, spontaneous liabilities-to-sales ratio, profit margin, and payout ratio.

12-5 The self-supporting growth rate is the maximum rate a firm can achieve without having to

raise external capital. The self-supporting growth rate is calculated using the AFN

equation, setting AFN equal to zero, replacing the term ΔS with the term g × S0, and

replacing the term S1 with S0 × (1 + g). Once the AFN equation is rewritten with these

modifications, you can now solve for g. This “g” obtained is the firm’s self-supporting

growth rate.

SOLUTIONS TO END-OF-CHAPTER PROBLEMS

12-1 AFN = (A0*/S0)∆S – (L0*/S0)∆S – (PM)(S1)(1 – payout rate)

12-2 Cash/Sales = $100/$1,000 = 10.0%

AR/Sales = $200/$1,000 = 20.0%

Inventories/Sales = $200/$1,000 = 20.0%

12-3 AP/Sales = $1,000/$10,000 = 10%

Accruals/Sales = $1,000/$10,000 = 10%

Answers and Solutions: 12 – 5

12-4 S0 = $5,000,000; A0* = $2,500,000; CL = $700,000; NP = $300,000; AP = $500,000;

Accruals = $200,000; M = 7%; payout ratio = 80%; A0*/S0 = 0.50; L0* = (AP +

Accruals)/S0 = ($500,000 + $200,000)/$5,000,000 = 0.14.

12-5 a.

equity and

liab. Total

=

payable

Accounts

+

debt

term–Long

+

stock

Common

+

earnings

Retained

$2,170,000 = $560,000 + Long-term debt + $625,000 + $395,000

Long-term debt = $590,000.

Answers and Solutions: 12 – 6

2019

Forecast

basis is %

of 2019

Sales

Additions

(New

Financing and

ΔRE)

2020

Sales

$3.500,000

$4,725,000

Total assets

$2,170,000

0.62

$2,929,500

Current liabilities

$ 560,000

0.16

Preliminary long-term debt

$1,150,000

$1,346,000

Common stock

Retained earnings

$1,020,000

$1,344,937

Preliminary total liabilities and equity

$2,170,000

$2,690,937

Answers and Solutions: 12 – 7

12-6 Cash $ 100.00 2.0 = $ 200.00

Accounts receivable 200.00 2.0 = 400.00

Inventories 200.00 2.0 = 400.00

Net fixed assets* 500.00 1.0 = 500.00

Total assets $1,000.00 $1,500.00

*Capacity sales = Sales/0.5 = $1,000/0.5 = $2,000 with respect to existing fixed assets.

Target FA/S ratio = $500/$2,000 = 0.25.

Target FA = 0.25($2,000) = $500 = Required FA. Since the firm currently has $500 of

fixed assets, no new fixed assets will be required.

**Addition to RE = (M)(S1)(1 – Payout ratio) = 0.05($2,000)(0.4) = $40.

Answers and Solutions: 12 – 8

c.

Upton Computers

Pro Forma Balance Sheet

December 31, 2019

(Millions of Dollars)

2019

Forecast

Basis:

Percent of

forecasted

sales

Cash

$ 3.5

0.0100

Receivables

26.0

0.0743

Inventories

58.0

0.1657

Total current assets

$ 87.5

Net fixed assets

35.0

0.100

Total assets

Accounts payable

$ 9.0

0.0257

Notes payable

18.0

Line of credit

Accruals

8.5

0.0243

Total current liabilities

$ 35.5

Mortgage loan

Common stock

15.0

Retained earnings

66.0

Total liab. and equity

Forecasted sales = $420 million

Profit margin = M = $10.5/$350 = 3%.

Payout ratio = $4.2/$10.5 = 40%.

NI = Forecasted sales Profit margin = $350 1.2 0.03 = $12.6.

Dividends = NI(Payout ratio) = $12.6(40%) = $5.04.

Addition to RE = NI – DIV = $12.6 – $5.04 = $7.56.

Answers and Solutions: 12 – 9

Upton Computers

Pro Forma Balance Sheet

December 31, 2020

(Millions of Dollars)

2019

Forecast

Basis:

Percent of

forecasted

sales

Additions

2020 Pro

Forma

Financing

2020 Pro

Forma after

Financing

Cash

$ 3.5

0.0100

$ 4.20

$ 4.20

Receivables

26.0

0.0743

31.20

31.20

Inventories

58.0

0.1657

69.60

69.60

Total current assets

$ 87.5

$105.00

$105.00

Net fixed assets

35.0

0.100

42.00

42.00

Total assets

$122.5

$147.00

$147.00

Accounts payable

$ 9.0

0.0257

$ 10.80

$ 10.80

Notes payable

18.0

18.00

18.00

Line of credit

+13.44

Accruals

8.5

0.0243

10.20

10.20

Total current liabilities

$ 35.5

$ 39.00

$ 52.44

Mortgage loan

Common stock

15.0

15.00

15.00

Total liab. and equity

$122.5

$133.56

$147.00

Deficit =

$ 13.44

12-8

The first column shows the financial statement accounts and the method used for

projections. Projected sales are equal to the actual sales that grow at the specified growth

rate.

Answers and Solutions: 12 – 10

Income Statements (Thousands of Dollars)

Actual

Projected

Sales = $36,000(1.15)

$36,000

$41,400

Op. costs = ($34,000/$36,000)($41,400)

$34,000

$39,100

Earnings before interest and taxes

$2,000

$2,300

Interest = 10%($2,100 + $3,500)

$160

$560

Pre-tax earnings

$1,840

$1,740

Taxes = 25%(Pre-tax earnings)

$460

$435

Net income

$1,380

$1,305

Dividends = 40%(Net income)

$552

$522

Addition to retained earnings

$828

$783

Balance Sheets (Thousands of Dollars)

Actual

Cash= ($1,080/$36,000)($41,400)

$1,080

$1,242

Receivables= ($6,480/$36,000)($41,400)

$6,480

$7,452

Inventories= ($9,000/$36,000)($41,400)

$9,000

$10,350

Total current assets

$16,560

$19,044

Net fixed assets= ($12,600/$36,000)($41,400)

$12,600

$14,490

Total assets

$29,160

$33,534

Accounts payable= ($4,320/$36,000)($41,400)

$4,320

$4,968

Accruals= ($2,880/$36,000)($41,400)

$2,880

$3,312

Line of credit (see calculation below)

$2,511

Notes payable = carry over

$2,100

$2,100

Total current liabilities

$9,300

$12,891

Long-term bonds = carry over

$3,500

$3,500

Common stock = carry over

$3,500

$3,500

Retained earnings REActual + Add. to REProj.

$12,860

$13,643

Total liabilities and equity

$29,160

$33,534

Answers and Solutions: 12 – 11

a. What is the projected value for earnings before interest and taxes? $2,300.

b. What is the projected value for pre-tax earnings? $1,740.

c. What is the projected net income? $1,305.

d. What is the projected addition to retained earnings? $783.

e. What is the projected value of total current assets? $19,044.

f. What is the projected value of total assets? $33,534.

g. What is the projected sum of accounts payable, accruals, and notes payable? $10,380

h. What is the forecasted line of credit? $2,511.

12-9

Income Statements for

December 31 in Current and

Projected Years

Sales

Operating costs

x Proj. Sales

Interest

Taxes (25%)

Net income

Dividends

Addn. to RE

Answers and Solutions: 12 – 12

Cash

$160,000

4%

$176,000

Receivables

$360,000

9%

$396,000

Inventories

$720,000

$792,000

Total CA

$1,240,000

$1,364,000

Fixed assets

$4,000,000

$4,400,000

Total assets

$5,240,000

$5,764,000

Balance Sheet as of

December 31 in

Current and Projected

Accounts payable

$360,000

9%

$396,000

Line of credit

$0

TA – AP -Accr.-

LT bonds – stk –

RE

$98,000

Accruals

$200,000

5%

$220,000

Total CL

$560,000

$714,000

LT bonds

$1,000,000

Carry over

$1,000,000

Common stock

$1,100,000

Carry over

$1,100,000

$2,580,000

$2,950,000

Total L&E

$5,240,000

$5,764,000

Current RE

Answers and Solutions: 12 – 13

SOLUTION TO SPREADSHEET PROBLEMS

12-10 The detailed solution is available in the file Ch12 P10 Build a Model Solution.xlsx at the

textbook’s Web site.

12-11 The detailed solution for is available in the file Ch12 P11 Build a Model Solution.xlsx at

the textbook’s Web site.

Mini Case: 12- 14

MINI CASE

Hatfield Medical Supply’s stock price had been lagging its industry averages, so its

board of directors brought in a new CEO, Jaiden Lee. Lee had brought in Ashley Novak, a

finance MBA who had been working for a consulting company, to replace the old CFO, and

Lee asked Ashley to develop the financial planning section of the strategic plan. In her

previous job, Novak’s primary task had been to help clients develop financial forecasts, and

that was one reason Lee hired her.

Novak began as she always did, by comparing Hatfield’s financial ratios to the

industry averages. If any ratio was substandard, she discussed it with the responsible manager

to see what could be done to improve the situation. The following data shows Hatfield’s latest

financial statements plus some ratios and other data that Novak plans to use in her analysis.

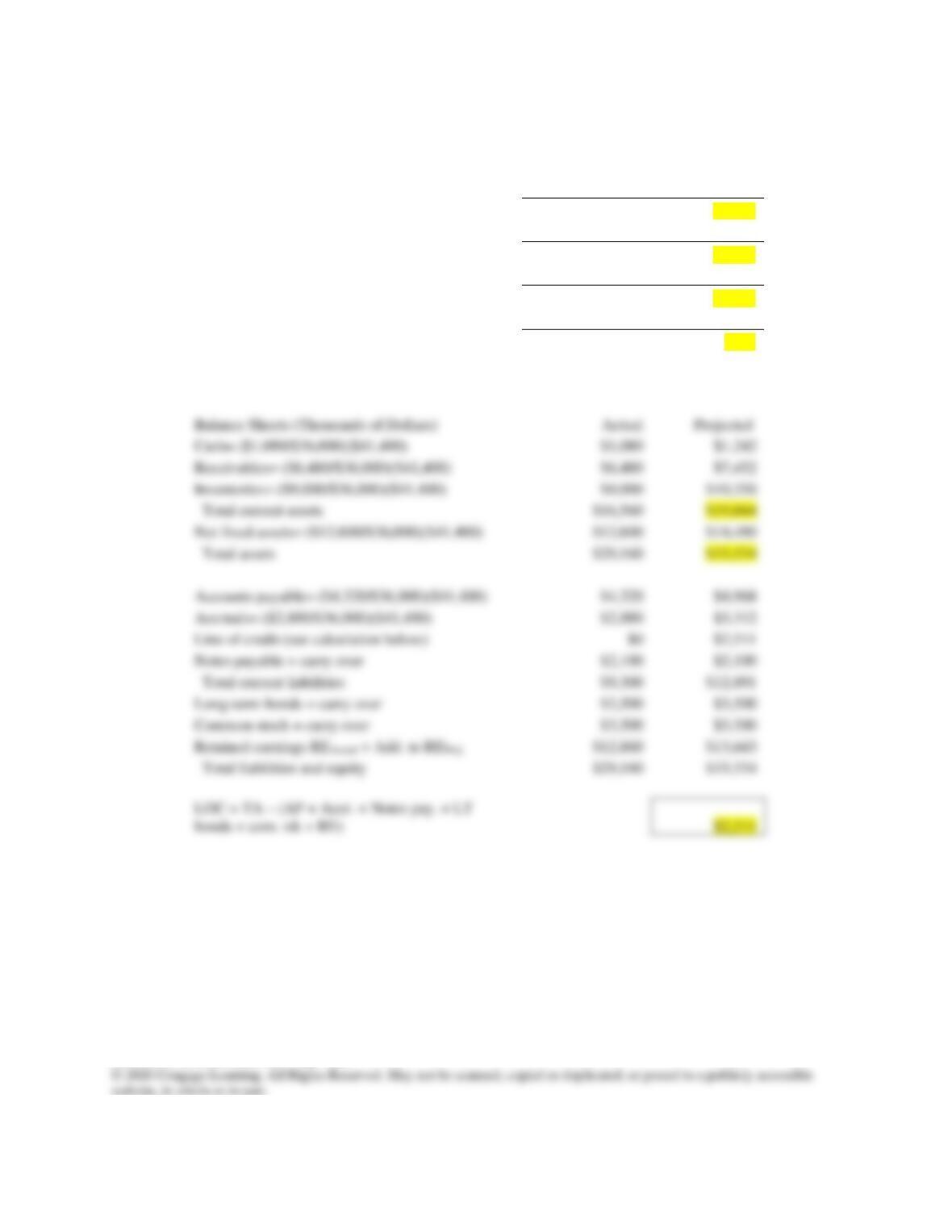

Hatfield Medical Supply (Millions of Dollars, Except per Share Data)

Balance Sheet,

12/31/2019

Income Statement, Year Ending

2019

Cash

$ 90

Sales

$9,000.9

Accounts receivable

1,260

Op costs (excl. depr.)

8,100.9

Inventories

1,440

Depreciation

360.0

Total CA

$2,790

EBIT

$540.0

Net fixed assets

3,600

Interest

144.0

Total assets

$6,390

Pre-tax earnings

$396.0

Taxes (25%)

Accts. pay. & accruals

$1,620

Net income

Line of credit

Total CL

$1,620

Long-term debt

1,800

Dividends

Total liabilities

$3,420

Additions to RE

Common stock

2,100

Common shares

Retained earnings

EPS

Total common equity.

$2,970

DPS

Total liab. & equity

$6,390

Ending stock price