Answers and Solutions: 11 – 1

Chapter 11

Cash Flow Estimation and

Risk Analysis

ANSWERS TO END-OF-CHAPTER QUESTIONS

11-1 a. Project cash flow, which is the relevant cash flow for project analysis, represents the

actual flow of cash, which includes investments in capital and working capital, but does

not include interest expenses or noncash charges like depreciation (except to the extent

that depreciation affects taxes). In other words, project cash flow is the free cash flow

generated by the project. Accounting income, on the other hand, reports accounting data

as defined by Generally Accepted Accounting Principles (GAAP).

c. Net operating working capital changes are the increases in current operating assets

resulting from accepting a project less the resulting increases in current operating

liabilities, or accruals and accounts payable. A net operating working capital change

must be financed just as a firm must finance its increases in fixed assets. Salvage value

is the market value of an asset after its useful life. Salvage values and their tax effects

must be included in project cash flow estimation.

Answers and Solutions: 11 – 2

d. Stand-alone risk is the risk a project would have if it was held in isolation. Corporate

(within-firm) risk is the risk that a project contributes to a company after taking into

consideration the cash flows of the company’s other projects; because projects are not

perfectly correlated, corporate risk usually will be less than stand-alone risk. Market

(beta) risk is the risk that a company contributes to a well diversified portfolio.

f. A risk-adjusted discount rate incorporates the risk of the project’s cash flows. The cost

of capital to the firm reflects the average risk of the firm’s existing projects. Thus, new

projects that are riskier than existing projects should have a higher risk-adjusted discount

rate. Conversely, projects with less risk should have a lower risk-adjusted discount rate.

This adjustment process also applies to a firm’s divisions. Risk differences are difficult

to quantify, thus risk adjustments are often subjective in nature. A project’s cost of

capital is its risk-adjusted discount rate for that project.

Answers and Solutions: 11 – 3

11-2 Only cash can be spent or reinvested, and since accounting profits do not represent cash, they

are of less fundamental importance than cash flows for investment analysis. Recall that in

the stock valuation chapters we focused on dividends and free cash flows, which represent

cash flows, rather than on earnings per share, which represent accounting profits.

11-3 Since the cost of capital includes a premium for expected inflation, failure to adjust cash

11-4 Capital budgeting analysis should only include those cash flows which will be affected by

the decision. Sunk costs are unrecoverable and cannot be changed, so they have no bearing

11-5 When a firm takes on a new capital budgeting project, it typically must increase its

investment in receivables and inventories, over and above the increase in payables and

accruals, thus increasing its net operating working capital. Since this increase must be

financed, it is included as an outflow in Year 0 of the analysis. At the end of the project’s

life, inventories are depleted and receivables are collected. Thus, there is a decrease in

NOWC, which is treated as an inflow.

Answers and Solutions: 11 – 4

11-6 Scenario analysis analyzes a limited number of outcomes. Although the base case scenario

may be the most likely, or expected outcome, the bad and good scenarios are frequently worst

case and best case scenarios, that is, when everything goes bad together, or everything goes

11-7 The costs associated with financing are reflected in the weighted average cost of capital.

To include interest expense in the capital budgeting analysis would “double count” the cost

of debt financing.

11-8 Daily cash flows would be theoretically best, but they would be costly to estimate and

probably no more accurate than annual estimates because we simply cannot forecast

11-9 In replacement projects, the benefits are generally cost savings, although the new

machinery may also permit additional output. The data for replacement analysis are

generally easier to obtain than for new products, but the analysis itself is somewhat more

Answers and Solutions: 11 – 5

11-10 Stand-alone risk is the project’s risk if it is held as a lone asset. It disregards the fact that

it is but one asset within the firm’s portfolio of assets and that the firm is but one stock in

a typical investor’s portfolio of stocks. Stand-alone risk is measured by the variability of

11-11 It is often difficult to quantify market risk. On the other hand, we can usually get a good

idea of a project’s stand–alone risk, and that risk is normally correlated with market risk:

The higher the stand-alone risk, the higher the market risk is likely to be. Therefore, firms

tend to focus on stand-alone risk, then deal with corporate and market risk by making

subjective, judgmental modifications to the calculated stand-alone risk.

Answers and Solutions: 11 – 6

SOLUTIONS TO END-OF-CHAPTER PROBLEMS

11-1 a. Equipment $ 17,000,000

NWC Investment 5,000,000

Initial investment outlay $22,000,000

11-2 Operating Cash Flows: t = 1

Sales revenues $18,000,000

Operating costs 9,000,000

11-3 Equipment’s original cost $12,000,000

Depreciation (80%) 9,000,000

Book value $ 3,000,000

Answers and Solutions: 11 – 7

11-4 Cash outflow = $110,000.

Increase in annual after-tax cash flows: CF = $19,000.

11-5 a. The MACRS rates are 33.33%, 44.45%, 14.81%, and 7.41%. The first MACRS

depreciation expense is 33.33%($1,700,000) = $566,610. The others are calculated

similarly. The applicable depreciation values are as follows for the two scenarios:

Scenario 1 Scenario 2

Year (Straight Line) (MACRS)

1 $425,000 $566,610

2 425,000 755,650

3 425,000 251,770

4 425,000 125,970

CF0 = 0; CF1 = 35402.5; CF2 = 82662.5; CF3 = -43307.5; CF4 = -74757.5; and I/YR =

10. Solve for NPV = $16,902.26

So, all else equal the use of the accelerated depreciation method will result in a higher

NPV (by $16,902.26) than would the use of a straight-line depreciation method.

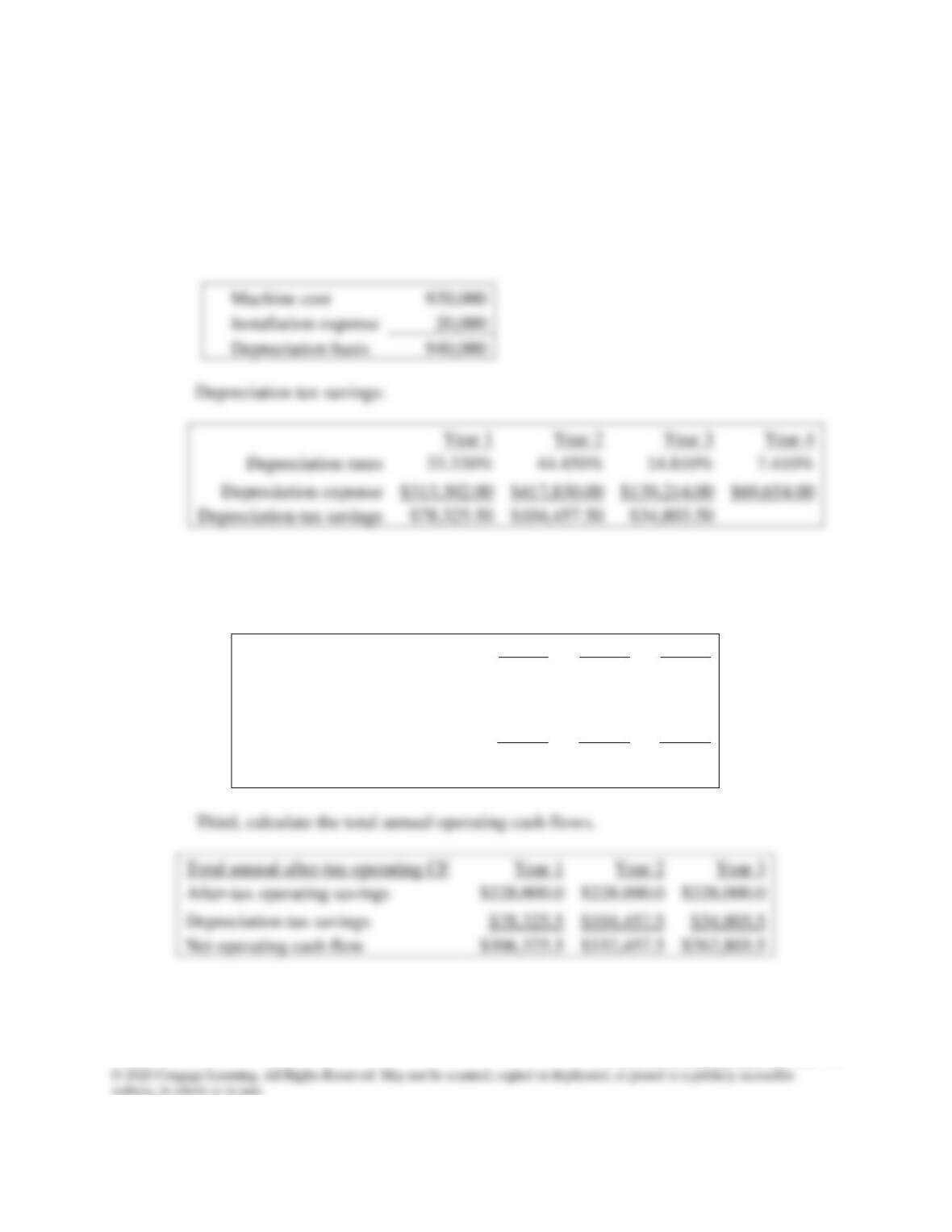

11-6 a. The net initial cash flow is:

Machine price

−$920,000

Installation cost

−$20,000

NWC required

−$15,500

Year 0 CF

−$955,500

Answers and Solutions: 11 – 9

b. The operating cash flows are:

First, calculate deprecation basis, annual depreciation expenses, and the annual tax

savings due to depreciation. The tax rate is 25%.

Basis:

$313,302.00

$417,830.00

$139,214.00

$69,654.00

$104,457.50

Second, calculate the after-tax operating savings.

Year 1

Year 2

Year 3

Before-tax operating savings

304,000

304,000

304,000

Tax on operating savings

76,000

76,000

76,000

After-tax operating savings

228,000

228,000

228,000

Total annual after-tax operating CF

After-tax operating savings

$228,000.0

$228,000.0

$228,000.0

Depreciation tax savings

$104,457.5

Net operating cash flow

$306,325.5

$332,457.5

$262,803.5

Answers and Solutions: 11 – 10

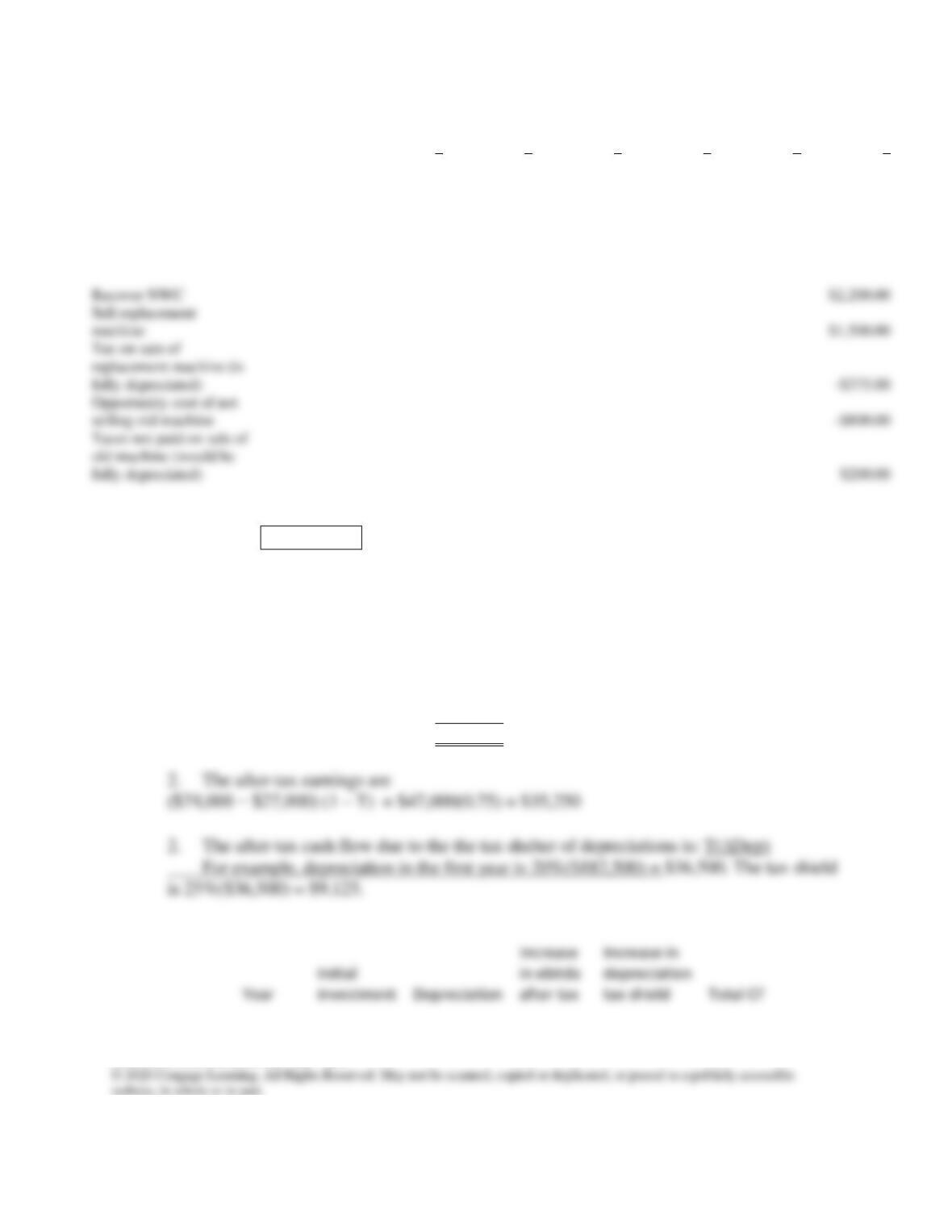

c. The additional Year-3 cash flows are:

First, find the remaining book value:

Salvage value calculation

Additional Year-3 CF

Depreciation basis

$940,000.0

Total depreciation expense in Years 1 through 3

$870,346.0

Remaining book value

$69,654.0

Salvage value

$500,000.0

Remaining book value

Salvage minus remaining book value

$430,346.0

Tax on gain

$107,586.5

Salvage value

$500,000.0

Tax on salvage gain

$107,586.5

NWC recovery

Additional Year-3 CF

$407,913.5

d. The cost of capital is 12%.

The total annual cash flows are:

Year 0

Year 1

Year 2

Year 3

Year 0 CF

-$955,500.0

Net operating CF

$306,325.5

$332,457.5

$262,803.5

Additional Year-3 CF

$407,913.5

Total CF

-$955,500.0

$306,325.5

$332,457.5

$670,717.0

11-7 The net cost is $89,000:

Basic price

$70,000.00

Modifications

$15,000.00

NWC increase

$4,000.00

Time 0 CF

$89,000.00

b. The operating cash flows follow:

Depreciation basis

$85,000.000

Depreciation expenses

$28,330.500

$12,588.500

Depreciation tax shield

After-tax savings

$18,750.000

$18,750.000

Operating cash flow

$21,897.125

Notes:

1. The after-tax cost savings is $25,000(1 – T) = $25,000(0.75) = $18,750.

2. The depreciation expense in each year is the depreciable basis, $85,000, times the

Answers and Solutions: 11 – 12

c. The additional end-of-project cash flow is $24,519:

Beginning Book Value

$85,000.00

$56,669.50

$18,887.00

Depreciation

$28,330.50

$37,782.50

$12,588.50

Ending Book Value

$56,669.50

$18,887.00

$6,298.50

Salvage value

$30,000.000

Book value

$6,298.500

Taxable profit

$23,701.500

Tax

A-T Salvage vaue

$24,074.625

Recover NWC

$4,000.000

Additional CF Year 3

$28,074.625

d. The project has an NPV of −$4,669.11. Thus, it should not be accepted.

Year

0

1

2

3

Time 0 CF

-$89,000.00

Operating cash flow

Additional CF Year 3

NPV

11-8 a.

Year1 sales = 1,000($138)$138,000

Year-1 costs = 1,000($105)105,000

Sales revenues at Year 1

$138,000.00

Costs at Year 1

$105,000.00

Pre-tax CF at Year 1

Tax

Year 1 after-tax CF

PV of future CFs

$275,000.00

Initial after-tax cost

$170,000.00

Answers and Solutions: 11 – 13

NPV

$105,000.00

Using the Year-1 price and theconstant growth formula , the present value of all of

the future cash flows is:

11-9 First determine the net cash flow at t = 0:

CF0 Calculation

Purchase Price

-$12,000.00

Sale of old machine

$4,150.00

Tax on sale

-$143.75

Net working capital

-$2,200.00

Total investment

-$10,193.75

Answers and Solutions: 11 – 14

Year

1

2

3

4

5

6

New depreciation

$2,400.00

$3,840.00

$2,304.00

$1,382.40

$1,382.40

$691.20

Old depreciation

$650.00

$650.00

$650.00

$650.00

$650.00

$325.00

Change in depreciation

$1,750.00

$3,190.00

$1,654.00

$732.40

$732.40

$366.20

Incremental Depr. Tax

savings

$437.50

$797.50

$413.50

$183.10

$183.10

$91.55

Recover NWC

$2,200.00

Sell replacement

machine

$1,500.00

selling old machine

$200.00

Total CFs

-$10,193.75

$3,362.50

$3,722.50

$3,338.50

$3,108.10

$3,108.10

$5,741.55

NPV

$3,544.60

11–10 1. Net investment at t = 0:

Cost of new machine $182,500

Net investment outlay (CF0) $182,500

Answers and Solutions: 11 – 15

0

$182,500

–

$182,500

1

$36,500

$35,250

$9,125

$44,375

2

$58,400

$35,250

$14,600

$49,850

3

$35,040

$35,250

$8,760

$44,010

4

$21,024

$35,250

$5,256

$40,506

5

$21,024

$35,250

$5,256

$40,506

6

$10,512

$35,250

$2,628

$37,878

7

$35,250

$35,250

8

$35,250

$35,250

11-11 E(NPV) = 0.05(-$70) + 0.20(-$25) + 0.50($12) + 0.20($20) + 0.05($30)

= -$3.5 + -$5.0 + $6.0 + $4.0 + $1.5

= $3.0 million.

Answers and Solutions: 11 – 16

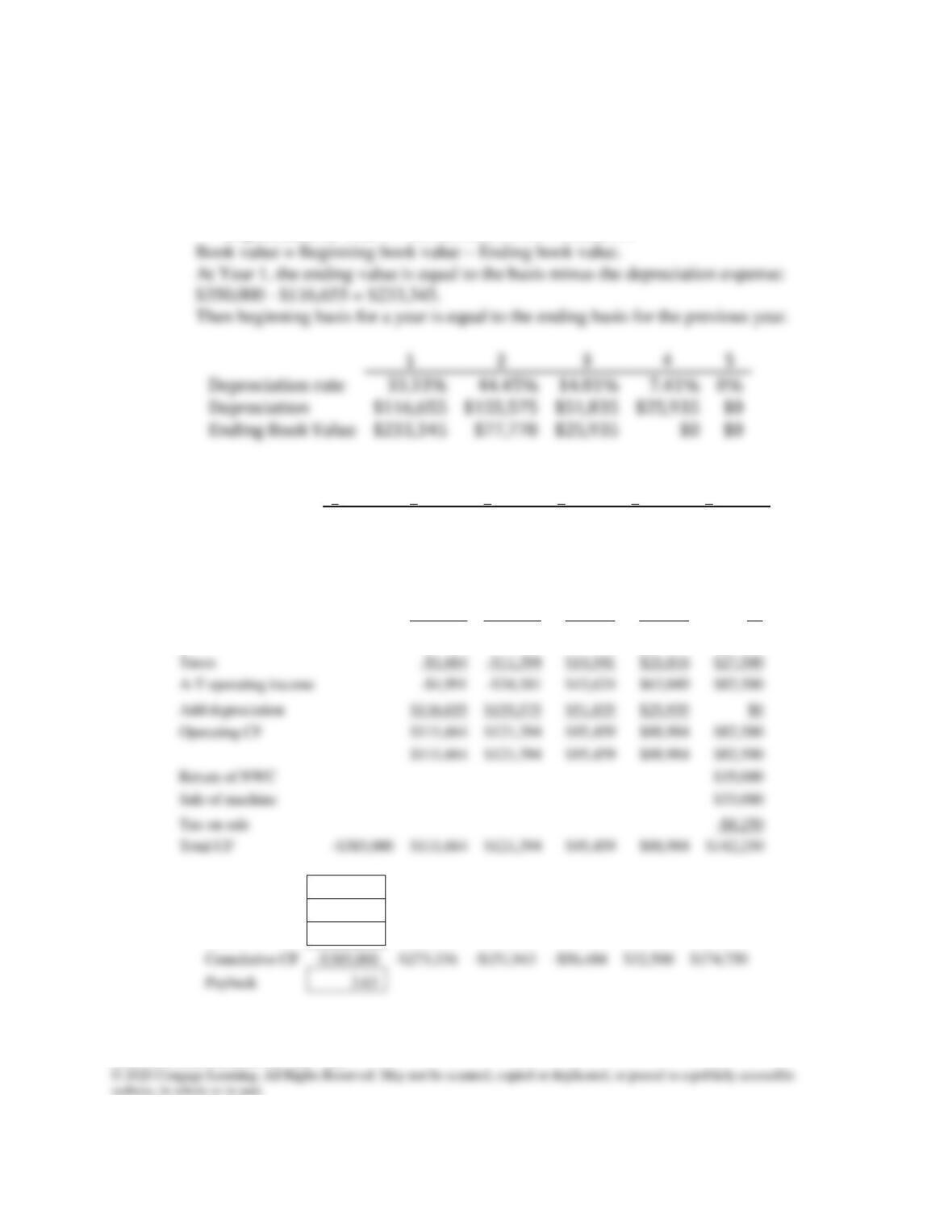

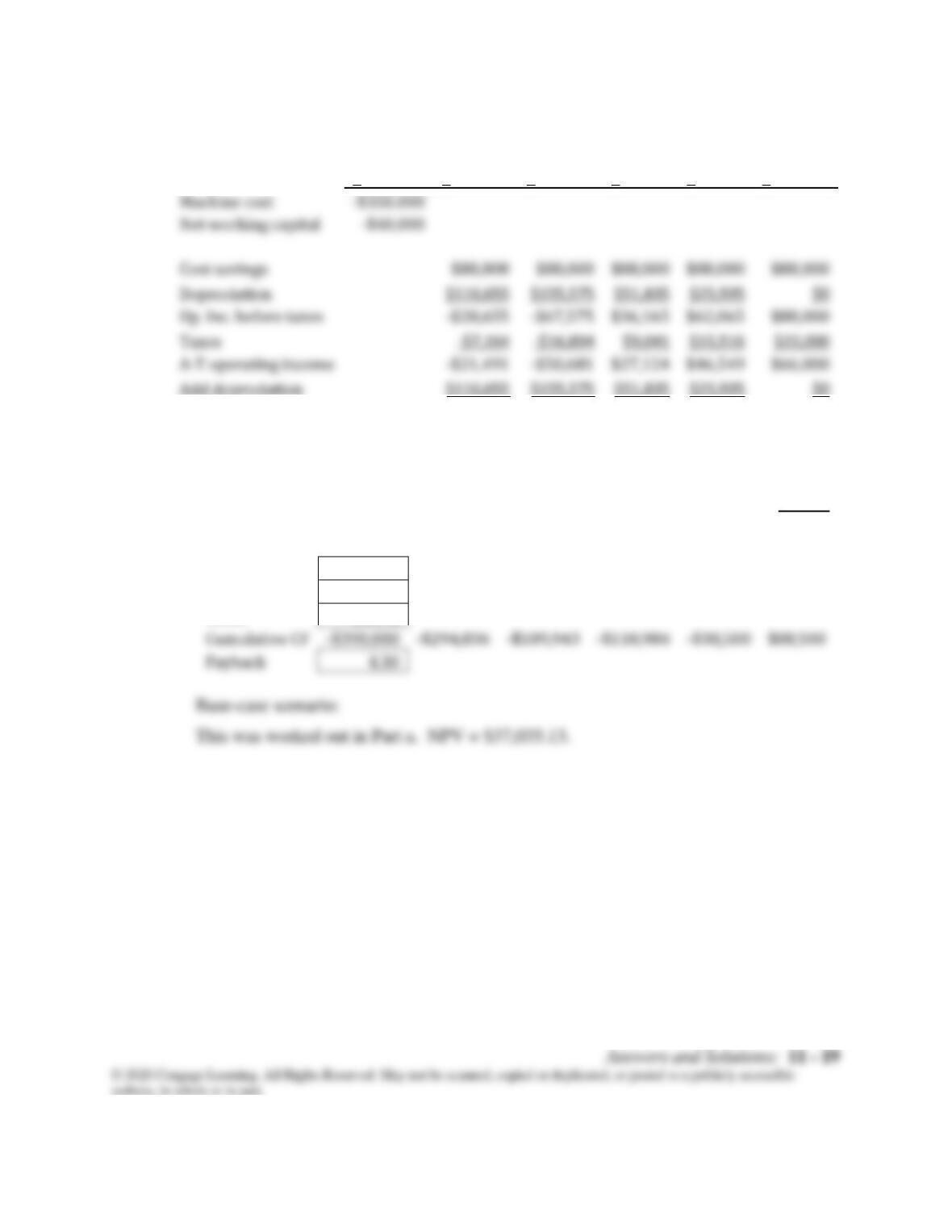

11-12 a. First, set up a depreciation schedule.

Depreciation basis = $350,000.

Depreciation = Basis(Depreciation rate)

For example, the depreciation in Year 1 is:

Depreciation in Year 1 = $350,000(0.3333) = $116,655.

0

1

2

3

4

5

Machine cost

-$350,000

Net working capital

-$35,000

Cost savings

$110,000

$110,000

$110,000

$110,000

$110,000

Depreciation

$116,655

$155,575

$51,835

$25,935

$0

Op. Inc. before taxes

-$6,655

-$45,575

$58,165

$84,065

$110,000

Taxes

-$1,664

-$11,394

$14,541

$21,016

$27,500

A-T operating income

-$4,991

-$34,181

$43,624

$63,049

$82,500

Add depreciation

$116,655

$155,575

$51,835

$25,935

$0

Operating CF

$111,664

$121,394

$95,459

$88,984

$82,500

$111,664

$121,394

$95,459

$88,984

$82,500

Return of NWC

$35,000

Sale of machine

$33,000

Tax on sale

-$8,250

Total CF

-$385,000

$111,664

$121,394

$95,459

$88,984

$142,250

NPV

$37,661

IRR

13.72%

MIRR

12.07%

Cumulative CF

-$385,000

-$273,336

-$151,943

-$56,484

$32,500

$174,750

Payback

Answers and Solutions: 11 – 17

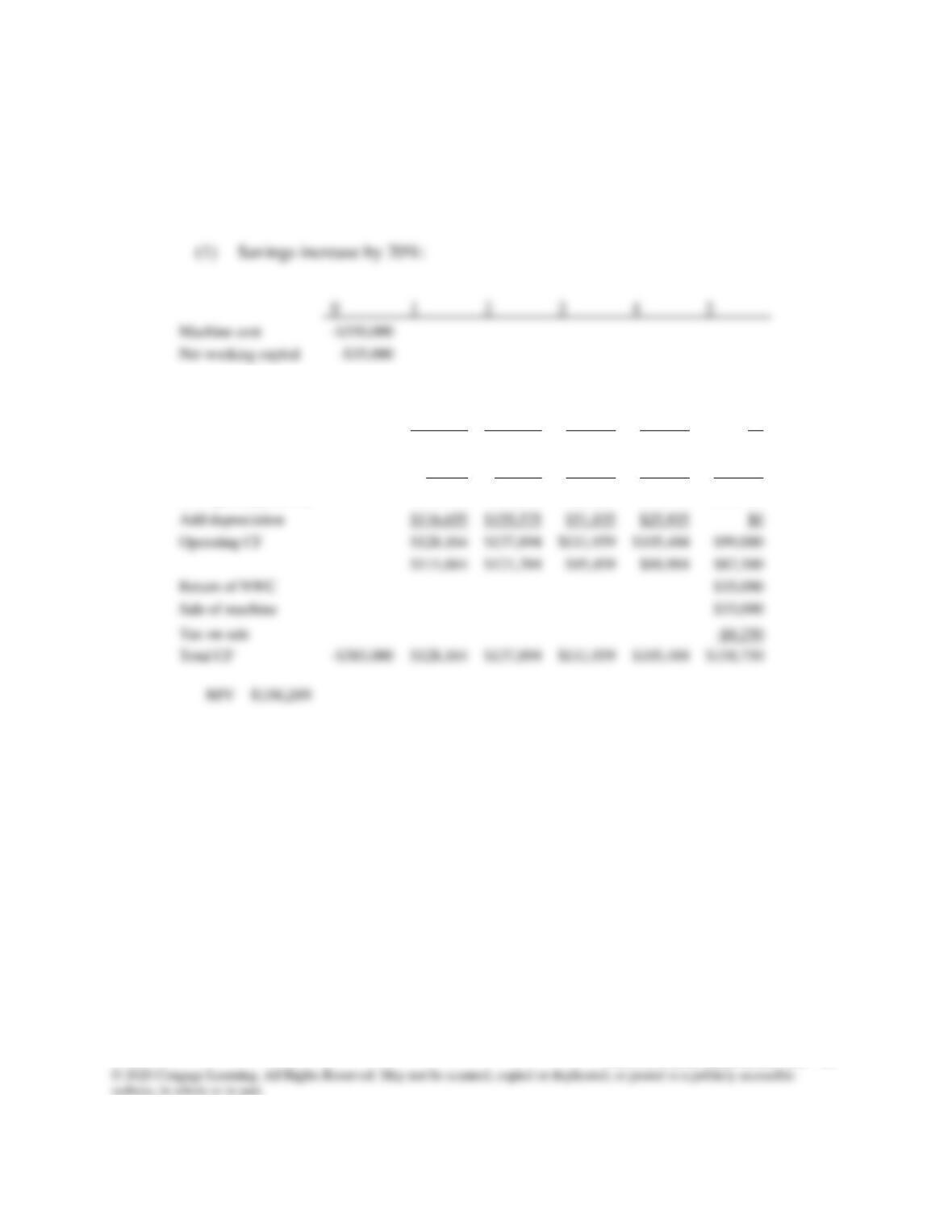

b. If savings increase by 20%, then savings will be (1.2)($110,000) = $132,000.

If savings decrease by 20%, then savings will be (0.8)($110,000) = $88,000.

0

1

2

3

4

5

Machine cost

-$350,000

Net working capital

-$35,000

Cost savings

$132,000

$132,000

$132,000

$132,000

$132,000

Depreciation

$116,655

$155,575

$51,835

$25,935

$0

Op. Inc. before taxes

$15,345

-$23,575

$80,165

$106,065

$132,000

Taxes

$3,836

-$5,894

$20,041

$26,516

$33,000

A-T operating income

$11,509

-$17,681

$60,124

$79,549

$99,000

Add depreciation

$116,655

$155,575

$51,835

$25,935

$0

Operating CF

$128,164

$137,894

$111,959

$105,484

$99,000

$111,664

$121,394

$95,459

$88,984

$82,500

Return of NWC

$35,000

Sale of machine

$33,000

Tax on sale

-$8,250

Total CF

-$385,000

$128,164

$137,894

$111,959

$105,484

$158,750

Answers and Solutions: 11 – 18

(2) Savings decrease by 20%:

0

1

2

3

4

5

Machine cost

-$350,000

Net working capital

-$35,000

Cost savings

$88,000

$88,000

$88,000

$88,000

$88,000

Depreciation

Op. Inc. before taxes

$36,165

$62,065

$88,000

Taxes

A-T operating income

$27,124

$46,549

$66,000

Add depreciation

Operating CF

$95,164

$104,894

$78,959

$72,484

$66,000

$111,664

$121,394

$95,459

$88,984

$82,500

Return of NWC

$35,000

Sale of machine

$33,000

Tax on sale

Total CF

-$385,000

$95,164

$104,894

$78,959

$72,484

$125,750

NPV –$24,887

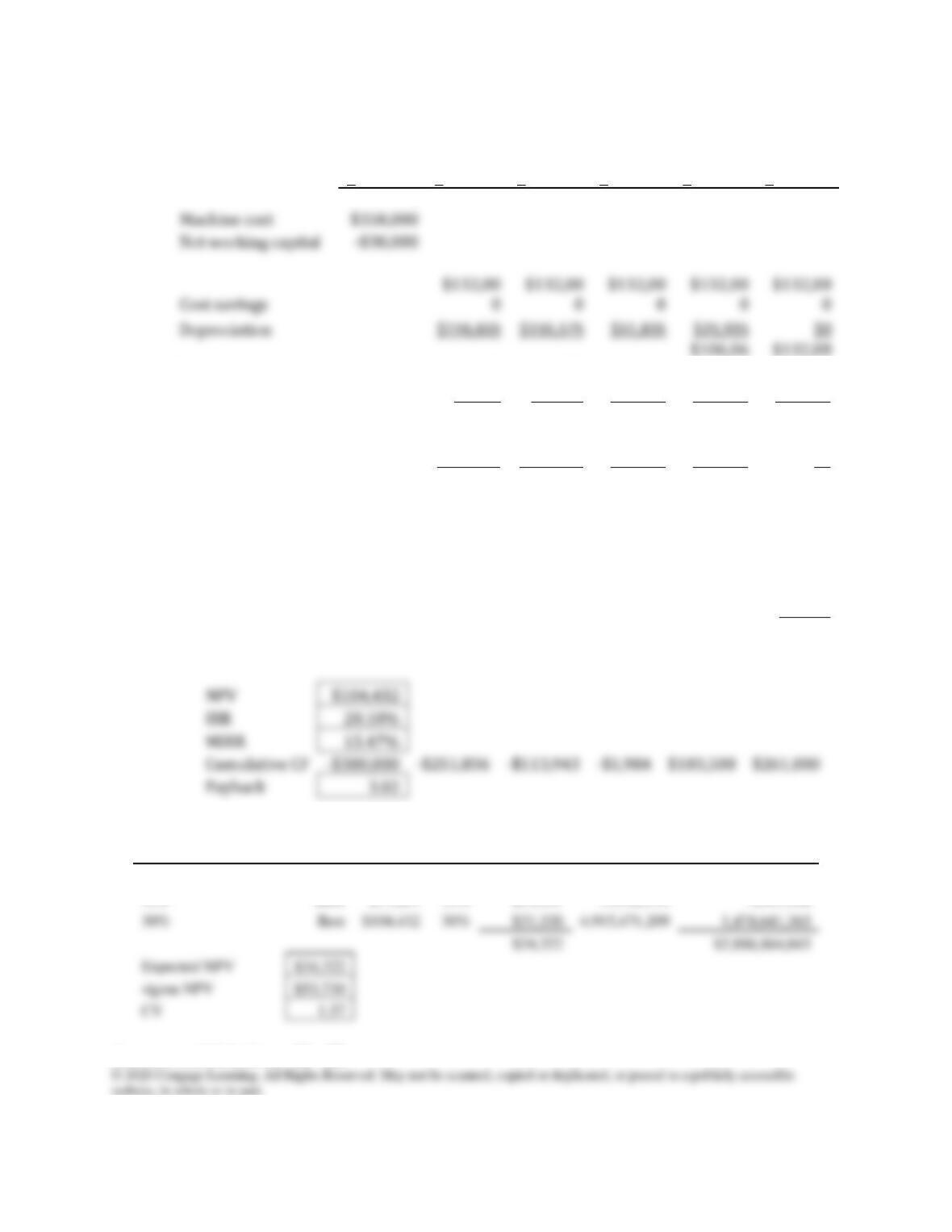

c. Worst-case scenario:

0

1

2

3

4

5

Machine cost

-$350,000

Net working capital

-$40,000

Cost savings

$88,000

$88,000

$88,000

$88,000

$88,000

Depreciation

Op. Inc. before taxes

$36,165

$62,065

$88,000

Taxes

-$7,164

A-T operating income

$27,124

$46,549

$66,000

Add depreciation

Operating CF

$95,164

$104,894

$78,959

$72,484

$66,000

$111,664

$121,394

$95,459

$88,984

$82,500

Return of NWC

$40,000

Sale of machine

$28,000

Tax on sale

-$7,000

Total CF

-$390,000

$95,164

$104,894

$78,959

$72,484

$127,000

NPV

-$29,111

IRR

7.08%

MIRR

8.31%

-$390,000

-$294,836

-$189,943

-$110,984

-$38,500

$88,500

Payback

Answers and Solutions: 11 – 20

Best-case scenario:

0

1

2

3

4

5

Machine cost

Net working capital

-$30,000

Cost savings

$132,00

0

$132,00

0

$132,00

0

$132,00

0

$132,00

0

Depreciation

$51,835

$25,935

$0

$106,06

$132,00

Op. Inc. before taxes

$15,345

-$23,575

$80,165

5

0

Taxes

$3,836

-$5,894

$20,041

$26,516

$33,000

A-T operating

income

$11,509

-$17,681

$60,124

$79,549

$99,000

Add depreciation

$116,655

$155,575

$51,835

$25,935

$0

Operating CF

$128,16

4

$137,89

4

$111,95

9

$105,48

4

$99,000

$111,66

4

$121,39

4

$95,459

$88,984

$82,500

Return of NWC

$30,000

Sale of machine

$38,000

Tax on sale

-$9,500

Total CF

–

$380,000

$128,16

4

$137,89

4

$111,95

9

$105,48

4

$157,50

0

NPV

IRR

MIRR

Cumulative CF

-$380,000

-$251,836

-$113,943

-$1,984

$103,500

$261,000

Scenario probabilities

NPV

Prob.

Prob x NPV

Dev. Squared

Prob(Dev. Squared)

35%

Worst

-$29,111

35%

-$10,189

4,023,775,752

1,408,321,513

35%

Base

$37,661

35%

$13,181

11,146,193

3,901,168

30%

30%

$31,330

4,915,471,209

1,474,641,363

$34,322

$2,886,864,043

Expected NPV

$34,322

sigma NPV

$53,730