11/21/2018

Chapter 11 Mini Case

Situation

Part I: Input Data

Scenario: Base Case

Equipment cost $200,000 Key Outputs: NPV = $62,593

Shipping charge $10,000 IRR = 20.1%

Installation charge $30,000 MIRR = 16.0%

Annual Depreciation Expense

Depreciable Basis = Equipment + Freight + Installation

Depreciable Basis = $240,000

Depreciation rate 0.3333 0.4445 0.1481 0.0741

Depreciation expense $79,992.00 $106,680.00 $35,544.00 $17,784.00

Shrieves Casting Company is considering adding a new line to its product mix, and the capital budgeting analysis is being conducted by

Sidney Johnson, a recently graduated MBA. The production line would be set up in unused space in Shrieves’ main plant. The machinery’s

invoice price would be approximately $200,000, another $10,000 in shipping charges would be required, and it would cost an additional

$30,000 to install the equipment. The machinery has an economic life of 4 years, and Shrieves has obtained a special tax ruling that places

the equipment in the MACRS 3-year class. The machinery is expected to have a salvage value of $25,000 after 4 years of use.

average project (r), is 10%.

a. Define “incremental cash flow.” Answer: See Chapter 11 Mini Case Show

(2.) Suppose the firm had spent $100,000 last year to rehabilitate the production line site. Should this be included in the analysis?

Explain. Answer: See Chapter 11 Mini Case Show

(1.) Should you subtract interest expense or dividends when calculating project cash flow? Answer: See Chapter 11 Mini Case Show

(3.) Now assume that the plant space could be leased out to another firm at $25,000 per year. Should this be included in the analysis?

If so, how? Answer: See Chapter 11 Mini Case Show

considered in the analysis? If so, how? Answer: See Chapter 11 Mini Case Show

b. Disregard the assumptions in Part a. What is Shrieves’ depreciable basis? What are the annual

depreciation expenses?

c. Calculate the annual sales revenues and costs (other than depreciation). Why is it important to include inflation when estimating cash

flows? See answer to part d.

Economic Life 4PI = 1.24

Salvage Value $25,000 Payback = 2.76

Tax Rate 25% Discounted Payback = 3.30

Cost of Capital 10%

Units Sold 1,000

Sales Price Per Unit $200

Incremental Cost Per Unit $100

Inflation rate 3%

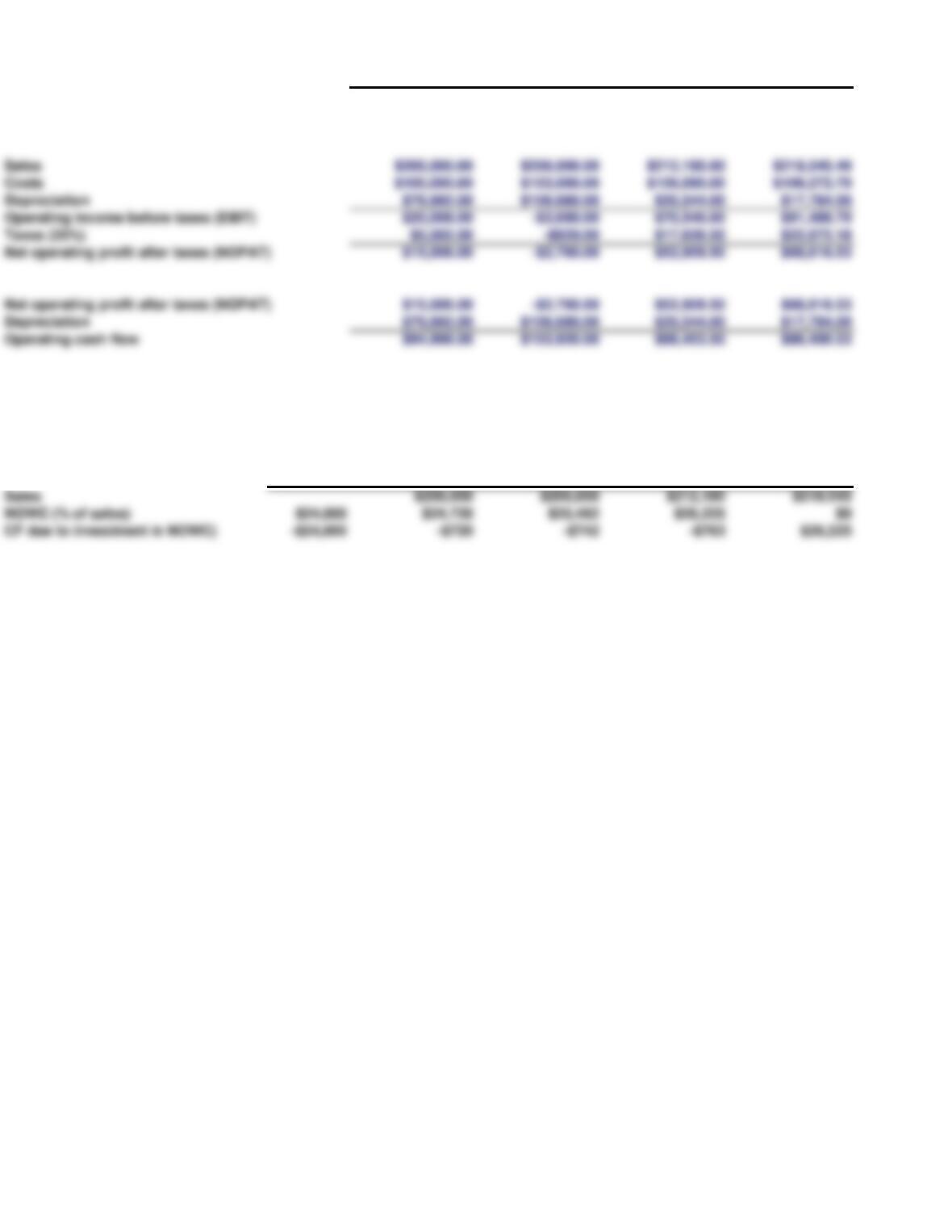

Annual Operating Cash Flows

Year 1 Year 2 Year 3 Year 4

Units 1,000 1,000 1,000 1,000

Unit price $200.00 $206.00 $212.18 $218.55

Unit cost $100.00 $103.00 $106.09 $109.27

Annual Cash Flows due to Investments in Net Working Capital

Year 0 Year 1 Year 2 Year 3 Year 4

NOWC (% of sales) $24,000 $24,720 $25,462 $26,225 $0

CF due to investment in NOWC) -$24,000 -$720 -$742 -$763 $26,225

d. Calculate annual net operating profit after sales (NOPAT).

e. Estimate the required net operating working capital (NOWC) for each year, and the cash flow due to investments in net working capital.

Depreciation $79,992.00 $106,680.00 $35,544.00 $17,784.00

Operating income before taxes (EBIT) $20,008.00 -$3,680.00 $70,546.00 $91,488.70

Taxes (25%) $5,002.00 -$920.00 $17,636.50 $22,872.18

Net operating profit after taxes (NOPAT) $15,006.00 -$2,760.00 $52,909.50 $68,616.53

Net operating profit after taxes (NOPAT) $15,006.00 -$2,760.00 $52,909.50 $68,616.53

Operating cash flow $94,998.00 $103,920.00 $88,453.50 $86,400.53

f. Calculate the after-tax salvage cash flow.

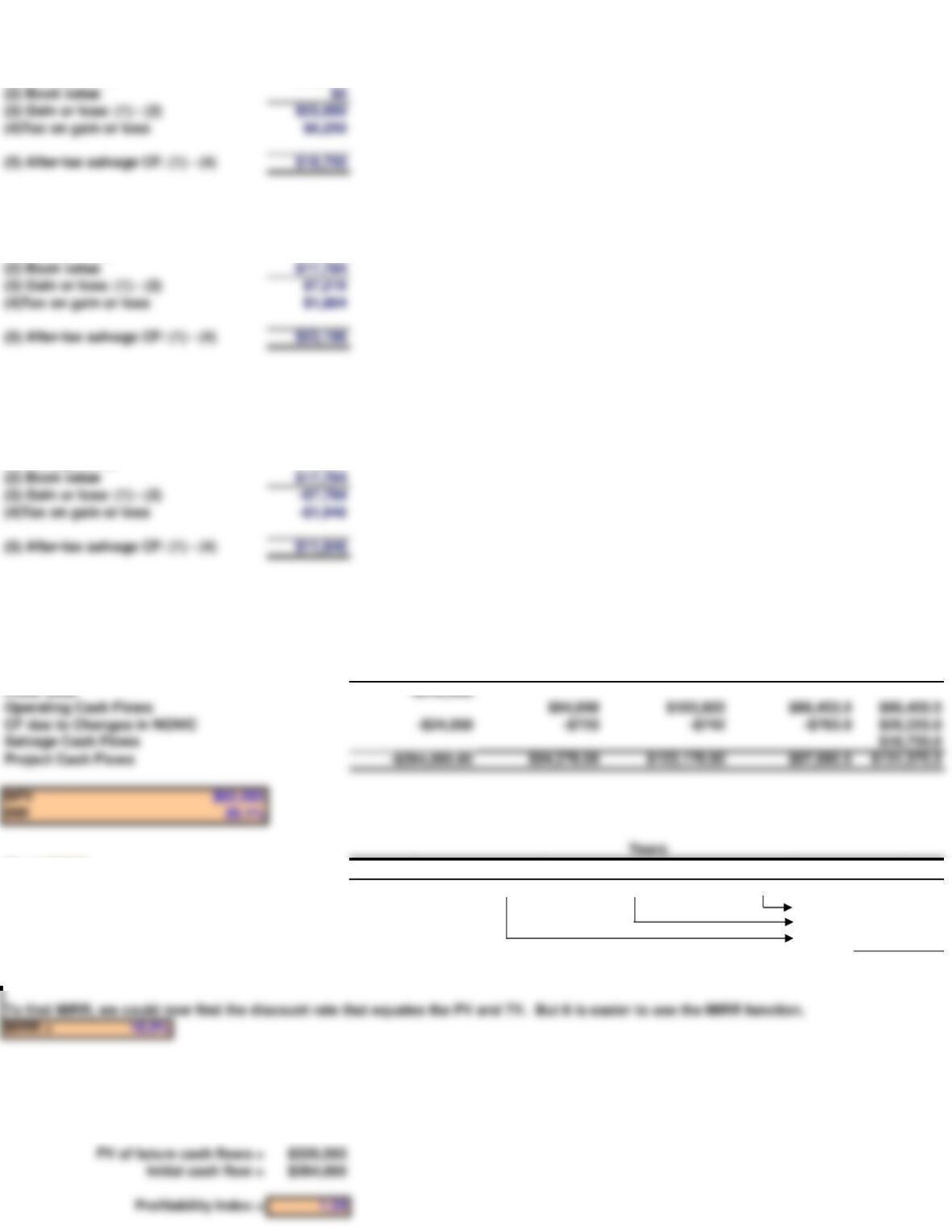

After-tax Salvage Value

(1) Salvage value $25,000

If the project lasts only 3 years and the salvage value is $25,000, what is the after-tax salvage cash flow?

(1) Salvage value $25,000

(2) Book value $17,784

(3) Gain or loss: (1) – (2) $7,216

(4)Tax on gain or loss $1,804

If the project lasts 3 year and the salvage value is $10,000, what is the after-tax salvage cash flow?

(1) Salvage value $10,000

(2) Book value $17,784

(3) Gain or loss: (1) – (2) -$7,784

(4)Tax on gain or loss -$1,946

Operating Cash Flows

Year 0 Year 1 Year 2 Year 3 Year 4

Initial Cost -$240,000

Operating Cash Flows $94,998 $103,920 $88,453.5 $86,400.5

CF due to Changes in NOWC -$24,000 -$720 -$742 -$763.0 $26,225.0

Find MIRR 0 1 2 3 4

Net Cash Flows -264,000 94,278 103,178 87,690.5 131,375.5

96,459.6

124,845.4

125,484.0

PV= -264,000 TV = 478,164.5

Find the Profitability Index (PI)

The profitability index is the present value of future cash flows divided by initial cost.

g. Calculate the net cash flows for each year. Based on these cash flows and the average project cost of capital, what are the project’s NPV,

IRR, MIRR, PI, payback, and discounted payback? Do these indicators suggest that the project should be undertaken?

(2) Book value $0

(3) Gain or loss: (1) – (2) $25,000

(4)Tax on gain or loss $6,250

Find Payback

0 1 2 3 4

Cash Flow -$264,000 $94,278 $103,178 $87,691 $131,376

Find Discounted Payback

0 1 2 3 4

Cash Flow -$264,000 $94,278 $103,178 $87,691 $131,376

Years

Years

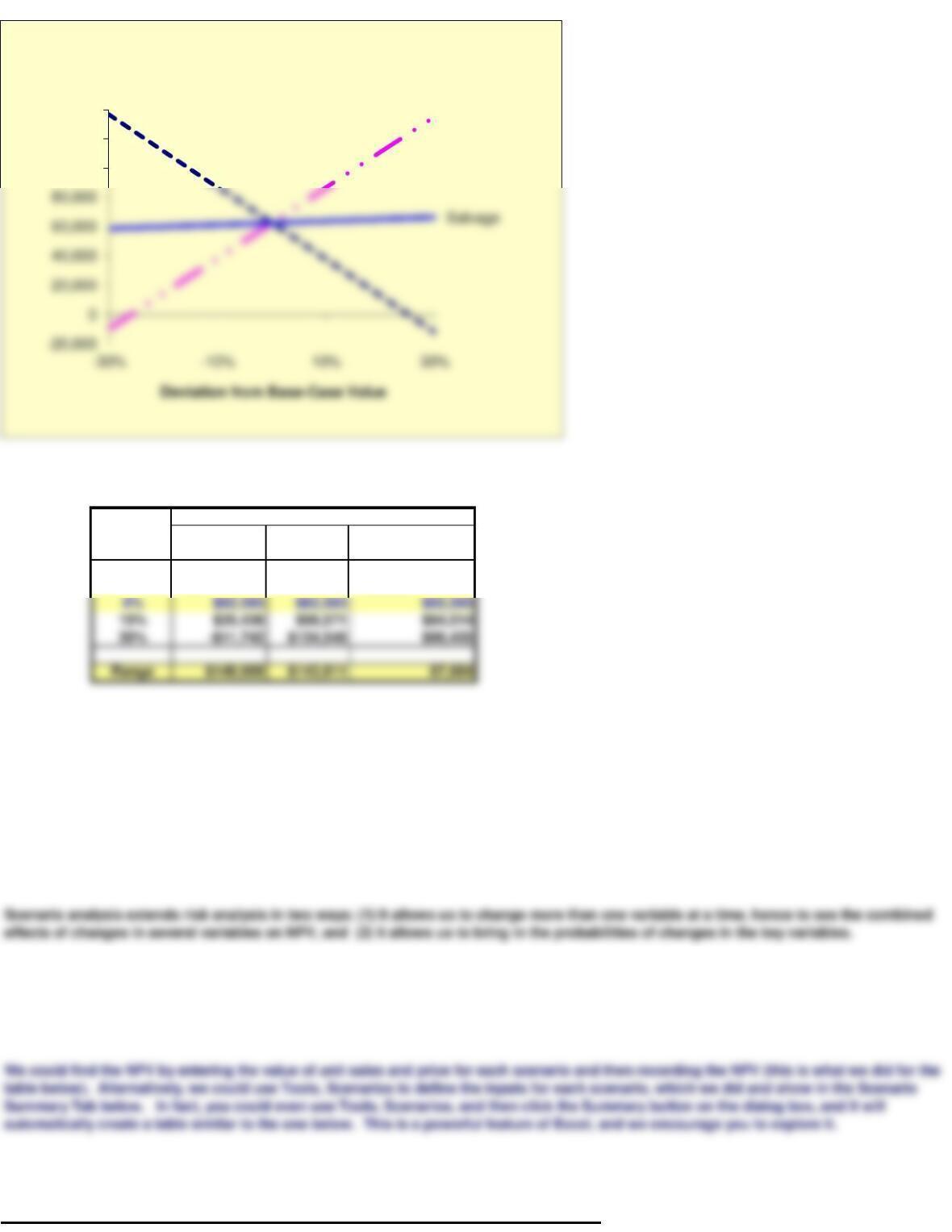

% Deviation % Deviation % Deviation

from Base cost NPV from Base units NPV from Base Salv. NPV

We summarize the data tables and show the sensitivity analysis graph below:

1st YEAR UNIT SALES

SALVAGE

j. (1.) What is sensitivity analysis? Answer: See Chapter 11 Mini Case Show

discuss the results.

(3.) How is each type of risk used in the capital budgeting process? Answer: See Chapter 11 Mini Case Show

Incremental Costs

Here we use an Excel “Data Table” to find the NPVs for changes in unit sales, salvage value, and WACC holding other things constant–

changing one variable at a time. This produces the sensitivity analys as shown below.

(2.) How is each of these risk types measured, and how do they relate to one another? Answer: See Chapter 11 Mini Case Show

h. What does the term ”risk” mean in the context of capital budgeting; to what extent can risk be quantified; and when risk is quantified, is

the quantification based primarily on statistical analysis of historical data or on subjective, judgmental estimates?

i. (1.) What are the three types of risk that are relevant in capital budgeting? Answer: See Chapter 11 Mini Case Show

Deviation NPV Deviation from Base Case

from

Base Case Cost per unit Units Sold Salvage

-30% $136,927 -$9,363 $58,751

-15% $99,760 $26,615 $60,672

Scenario Analysis

Probability Unit Sales Unit Price NPV

Scenario

(2.) What is the worst-case NPV? The best-case NPV?

(3.) Use the worst-, most likely, and best-case NPVs and probabilities of occurrence to find the project’s expected NPV, standard

deviation, and coefficient of variation.

Squared Deviation

times Probability

(3.) What is the primary weakness of sensitivity analysis? What is its primary usefulness? Answer: See Chapter 11 Mini Case Show

k. Assume that Sidney Johnson is confident of her estimates of all the variables that affect the project’s cash flows except unit sales and

sales price: If product acceptance is poor, unit sales would be only 800 units a year and the unit price would only be $160; a strong

consumer response would produce sales of 1,200 units and a unit price of $240. Sidney believes that there is a 25% chance of poor

acceptance, a 25% chance of excellent acceptance, and a 50% chance of average acceptance (the base case).

(1.) What is scenario analysis?

Cost per unit Units Sold

100,000

120,000

140,000

NPV ($)

Sensitivity Analysis

25% 1,200 $240 $227,595

(2.) Shrieves typically adds or subtracts 3 percentage points to the overall cost of capital to adjust for risk. Should the new line be

accepted?

(3.) Are there any subjective risk factors that should be considered before the final decision is made? Answer: See Chapter 11 Mini Case

Show

m. (1.) Assume that Shrieves’ average project has a coefficient of variation in the range of 0.2 to 0.4. Would the new line be classified as

high risk, average risk, or low risk? What type of risk is being measured here? Answer: See Chapter 11 Mini Case Show

Best Case

l. Are there problems with scenario analysis? Define simulation analysis, and discuss its principal advantages and disadvantages.

Answer: See Chapter 11 Mini Case Show. Also, see the worksheet this file for an application of simulation analysis to this project analysis.

$6,025,613,876.98

50% 1,000 $200 $62,593

$4,606,631,706.48