161

Chapter 11

Optimal Portfolio Choice and the Capital

Asset Pricing Model

11–1. You are considering how to invest part of your retirement savings. You have decided to put

$200,000 into three stocks: 50% of the money in GoldFinger (currently $25/share), 25% of the

money in Moosehead (currently $80/share), and the remainder in Venture Associates (currently

$2/share). If GoldFinger stock goes up to $30/share, Moosehead stock drops to $60/share, and

Venture Associates stock rises to $3 per share,

a. What is the new value of the portfolio?

b. What return did the portfolio earn?

c. If you don’t buy or sell shares after the price change, what are your new portfolio weights?

a. Let

i

n

be the number of share in stock I, then

200,000 0.5 4,000

25

G

n´

= =

11–2. You own three stocks: 600 shares of Apple Computer, 10,000 shares of Cisco Systems, and 5000

shares of Colgate-Palmolive. The current share prices and expected returns of Apple, Cisco, and

Colgate-Palmolive are, respectively, $500, $20, $100 and 12%, 10%, 8%.

a. What are the portfolio weights of the three stocks in your portfolio?

b. What is the expected return of your portfolio?

c. Suppose the price of Apple stock goes up by $25, Cisco rises by $5, and Colgate-Palmolive

falls by $13. What are the new portfolio weights?

d. Assuming the stocks’ expected returns remain the same, what is the expected return of the

portfolio at the new prices?

New

New

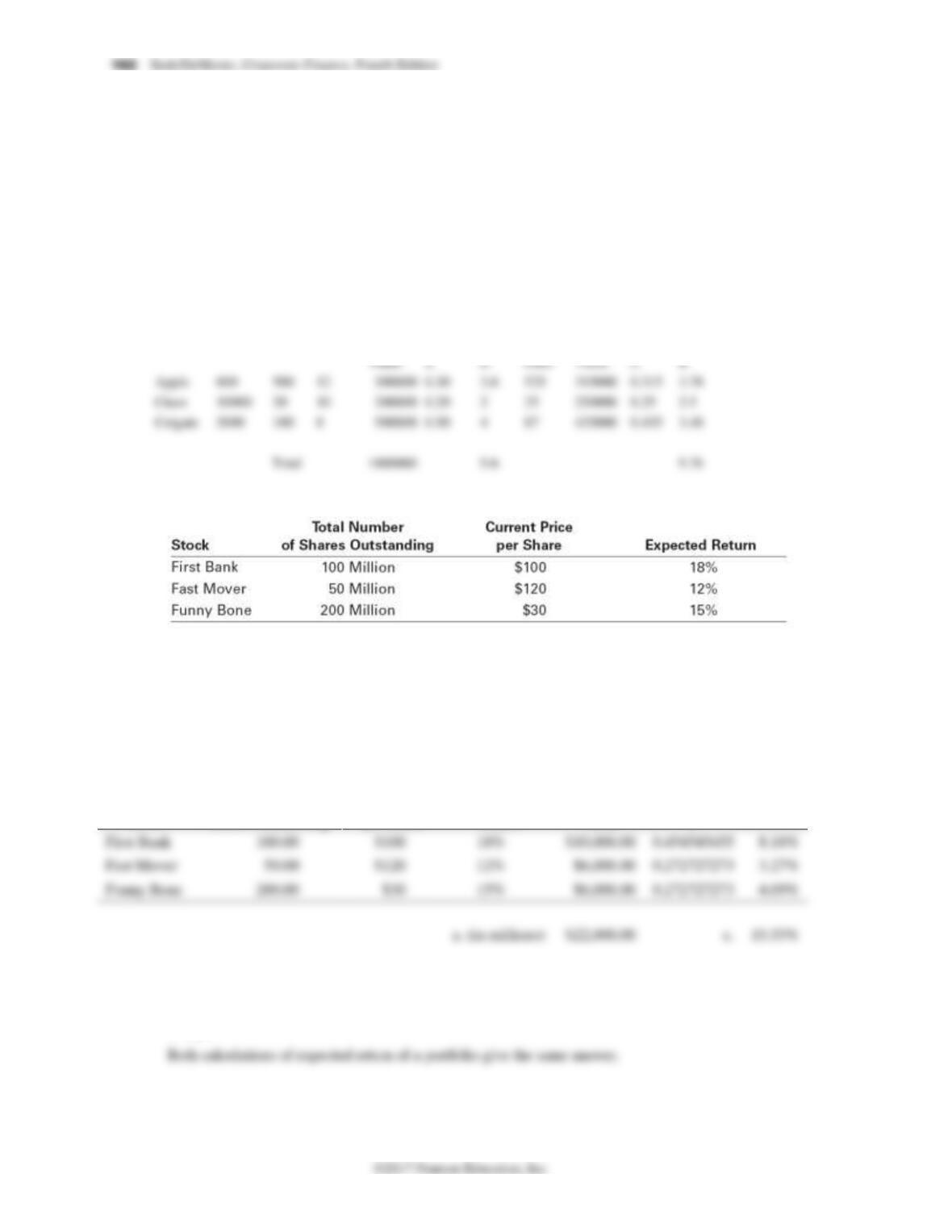

11–3. Consider a world that only consists of the three stocks shown in the following table:

a. Calculate the total value of all shares outstanding currently.

b. What fraction of the total value outstanding does each stock make up?

c. You hold the market portfolio, that is, you have picked portfolio weights equal to the answer

to part b (that is, each stock’s weight is equal to its contribution to the fraction of the total

value of all stocks). What is the expected return of your portfolio?

Stock

Total Number of

Shares Outstanding

Current Price

per Share

Expected

Return

Value

b.

11–4. There are two ways to calculate the expected return of a portfolio: either calculate the expected

return using the value and dividend stream of the portfolio as a whole, or calculate the weighted

average of the expected returns of the individual stocks that make up the portfolio. Which return

is higher?

11–5. Using the data in the following table, estimate (a) the average return and volatility for each stock,

(b) the covariance between the stocks, and (c) the correlation between these two stocks.

a.

10 20 5 5 2 9 3.5%

6

A

R

– + + – + +

= =

c.

Covariance

Correlation SD(R )SD(R )

=

164 Berk/DeMarzo, Corporate Finance, Fourth Edition

11–6. Use the data in Problem 5, consider a portfolio that maintains a 50% weight on stock A and a

50% weight on stock B.

a. What is the return each year of this portfolio?

b. Based on your results from part a, compute the average return and volatility of the portfolio.

c. Show that (i) the average return of the portfolio is equal to the average of the average

returns of the two stocks, and (ii) the volatility of the portfolio equals the same result as from

the calculation in Eq. 11.9.

d. Explain why the portfolio has a lower volatility than the average volatility of the two stocks.

a, b, and c. See table below.

11–7. Using your estimates from Problem 5, calculate the volatility (standard deviation) of a portfolio

that is 70% invested in stock A and 30% invested in stock B.

11–8. Using the data from Table 11.3, what is the covariance between the stocks of Alaska Air and

Southwest Airlines?

11–9. Suppose two stocks have a correlation of 1. If the first stock has an above average return this

year, what is the probability that the second stock will have an above average return?

11-10. Arbor Systems and Gencore stocks both have a volatility of 40%. Compute the volatility of a

portfolio with 50% invested in each stock if the correlation between the stocks is (a) + 1, (b) 0.50,

(c) 0, (d) −0.50, and (e) −1.0. In which cases is the volatility lower than that of the original stocks?

stock vol 40%

11-11. Suppose Wesley Publishing’s stock has a volatility of 60%, while Addison Printing’s stock has a

volatility of 30%. If the correlation between these stocks is 25%, what is the volatility of the

following portfolios of Addison and Wesley: (a) 100% Addison, (b) 75% Addison and 25%

Wesley, and (c) 50% Addison and 50% Wesley.

Vol Corr

Wesley 60% 25%

11-12. Suppose Avon and Nova stocks have volatilities of 50% and 25%, respectively, and they are

perfectly negatively correlated. What portfolio of these two stocks has zero risk?

11-13. Suppose Tex stock has a volatility of 40%, and Mex stock has a volatility of 20%. If Tex and Mex

are uncorrelated,

a. What portfolio of the two stocks has the same volatility as Mex alone?

b. What portfolio of the two stocks has the smallest possible volatility?

Vol Corr

Tex 40% 0%

Portfolio

x_tex x_mex Vol

0% 100% 20.00%

11–14. Using the data in Table 11.1,

a. Compute the annual returns for a portfolio with 25% invested in North Air, 25% invested in

West Air, and 50% invested in Tex Oil.

b. What is the lowest annual return for your portfolio in part a? How does it compare with the

lowest annual return of the individual stocks or portfolios in Table 11.1

166 Berk/DeMarzo, Corporate Finance, Fourth Edition

a.

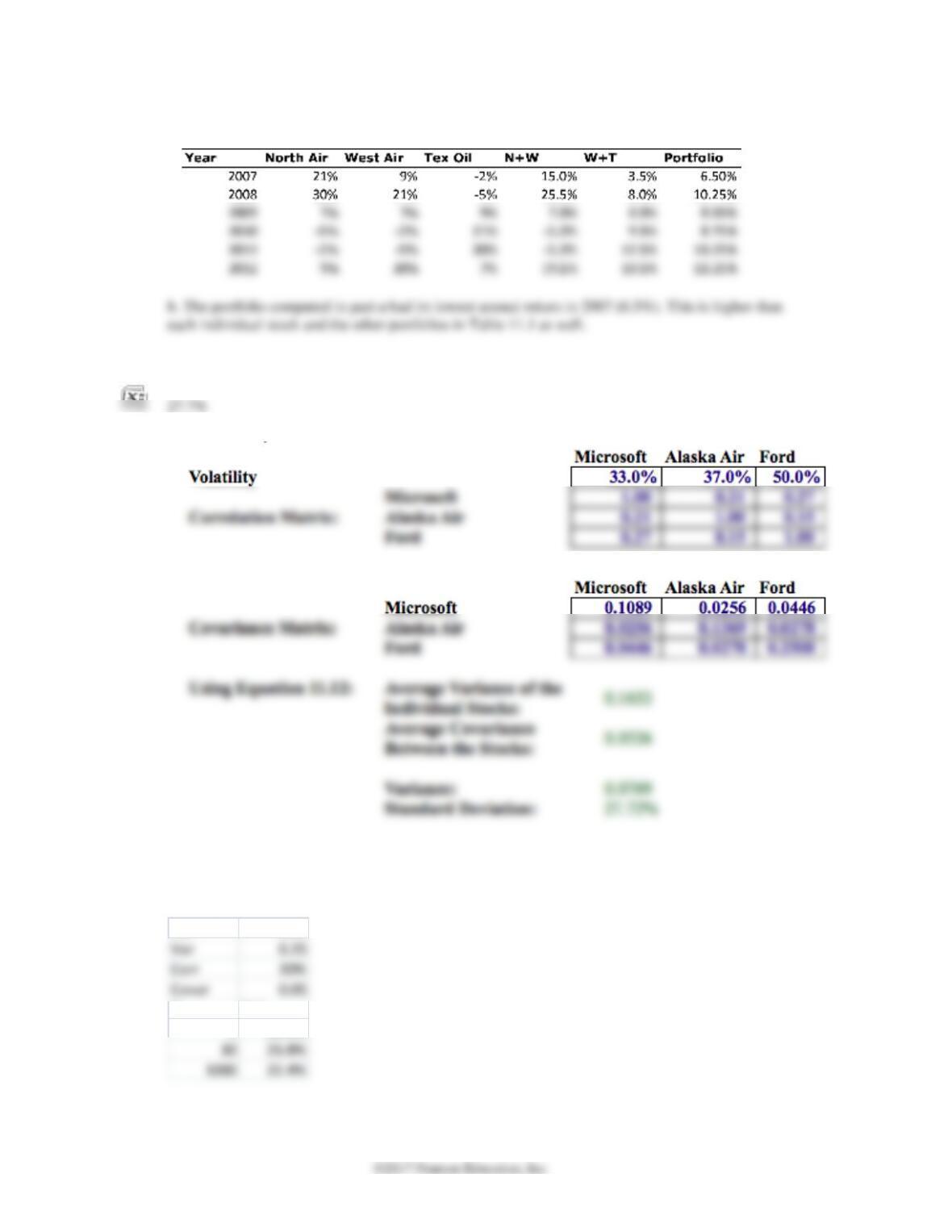

11–15. Using the data from Table 11.3, what is volatility of an equally weighted portfolio of Microsoft,

Alaska Air, and Ford Motor stock?

11–16. Suppose that the average stock has a volatility of 50%, and that the correlation between pairs of

stocks is 20%. Estimate the volatility of an equally weighted portfolio with (a) 1 stock, (b) 30

stocks, (c) 1000 stocks.

Vol 50%

N Vol

1 50.0%

Chapter 11/Optimal Portfolio Choice and the Capital Asset Pricing Model 167

11–17. What is the volatility (standard deviation) of an equally weighted portfolio of stocks within an

industry in which the stocks have a volatility of 50% and a correlation of 40% as the portfolio

becomes arbitrarily large?

11–18. Consider an equally weighted portfolio of stocks in which each stock has a volatility of 40%, and

the correlation between each pair of stocks is 20%.

a. What is the volatility of the portfolio as the number of stocks becomes arbitrarily large?

b. What is the average correlation of each stock with this large portfolio?

11–19. Stock A has a volatility of 65% and a correlation of 10% with your current portfolio. Stock B

has a volatility of 30% and a correlation of 25% with your current portfolio. You currently hold

both stocks. Which will increase the volatility of your portfolio: (i) selling a small amount of

stock B and investing the proceeds in stock A, or (ii) selling a small amount of stock A and

investing the proceeds in stock B?

11–20. You currently hold a portfolio of three stocks, Delta, Gamma, and Omega. Delta has a volatility

of 60%, Gamma has a volatility of 30%, and Omega has a volatility of 20%. Suppose you invest

50% of your money in Delta, and 25% each in Gamma and Omega.

a. What is the highest possible volatility of your portfolio?

b. If your portfolio has the volatility in (a), what can you conclude about the correlation

between Delta and Omega?

11–21. Suppose Ford Motor stock has an expected return of 20% and a volatility of 40%, and Molson

Coors Brewing has an expected return of 10% and a volatility of 30%. If the two stocks are

uncorrelated,

a. What is the expected return and volatility of an equally weighted portfolio of the two stocks?

b. Given your answer to (a), is investing all of your money in Molson Coors stock an efficient

portfolio of these two stocks?

c. Is investing all of your money in Ford Motor an efficient portfolio of these two stocks?

168 Berk/DeMarzo, Corporate Finance, Fourth Edition

a.

A B Corr

ER 20% 10%

11–22. Suppose Intel’s stock has an expected return of 26% and a volatility of 50%, while Coca-Cola’s

has an expected return of 6% and volatility of 25%. If these two stocks were perfectly negatively

correlated (i.e., their correlation coefficient is −1),

a. Calculate the portfolio weights that remove all risk.

b. If there are no arbitrage opportunities, what is the risk-free rate of interest in this economy?

a. If the two stocks are perfectly correlated negatively, they fluctuate due to the same risks, but in

opposite directions. Because Intel is twice as volatile as Coke, we will need to hold twice as much

Coke stock as Intel in order to offset Intel’s risk. That is, our portfolio should be 2/3 Coke and 1/3

Intel.

We can check this using Eq. 11.9.

11–23. Calculate (a) the expected return and (b) the volatility (standard deviation) of a portfolio that is

equally invested in Johnson & Johnson’s and Walgreen’s stock.

In this case, the portfolio weights are xj = xw = 0.50. From Eq. 11.3,

Chapter 11/Optimal Portfolio Choice and the Capital Asset Pricing Model 169

We can use Eq. 11.9.

11–24. For the portfolio in Problem 23, if the correlation between Johnson & Johnson’s and Walgreen’s

stock were to increase,

a. Would the expected return of the portfolio rise or fall?

b. Would the volatility of the portfolio rise or fall?

11–25. Calculate (a) the expected return and (b) the volatility (standard deviation) of a portfolio that

consists of a long position of $10,000 in Johnson & Johnson and a short position of $2000 in

Walgreen’s.

11-26. Using the same data as for Problem 23, calculate the expected return and the volatility (standard

deviation) of a portfolio consisting of Johnson & Johnson’s and Walgreen’s stocks using a wide

range of portfolio weights. Plot the expected return as a function of the portfolio volatility. Using

your graph, identify the range of Johnson & Johnson’s portfolio weights that yield efficient

combinations of the two stocks, rounded to the nearest percentage point.

170 Berk/DeMarzo, Corporate Finance, Fourth Edition

x(J&J) x(Walgreen) SD ER

-50% 150% 29.30% 11.50%

-30% 130% 25.38% 10.90%

70% 30% 13.82% 7.90%

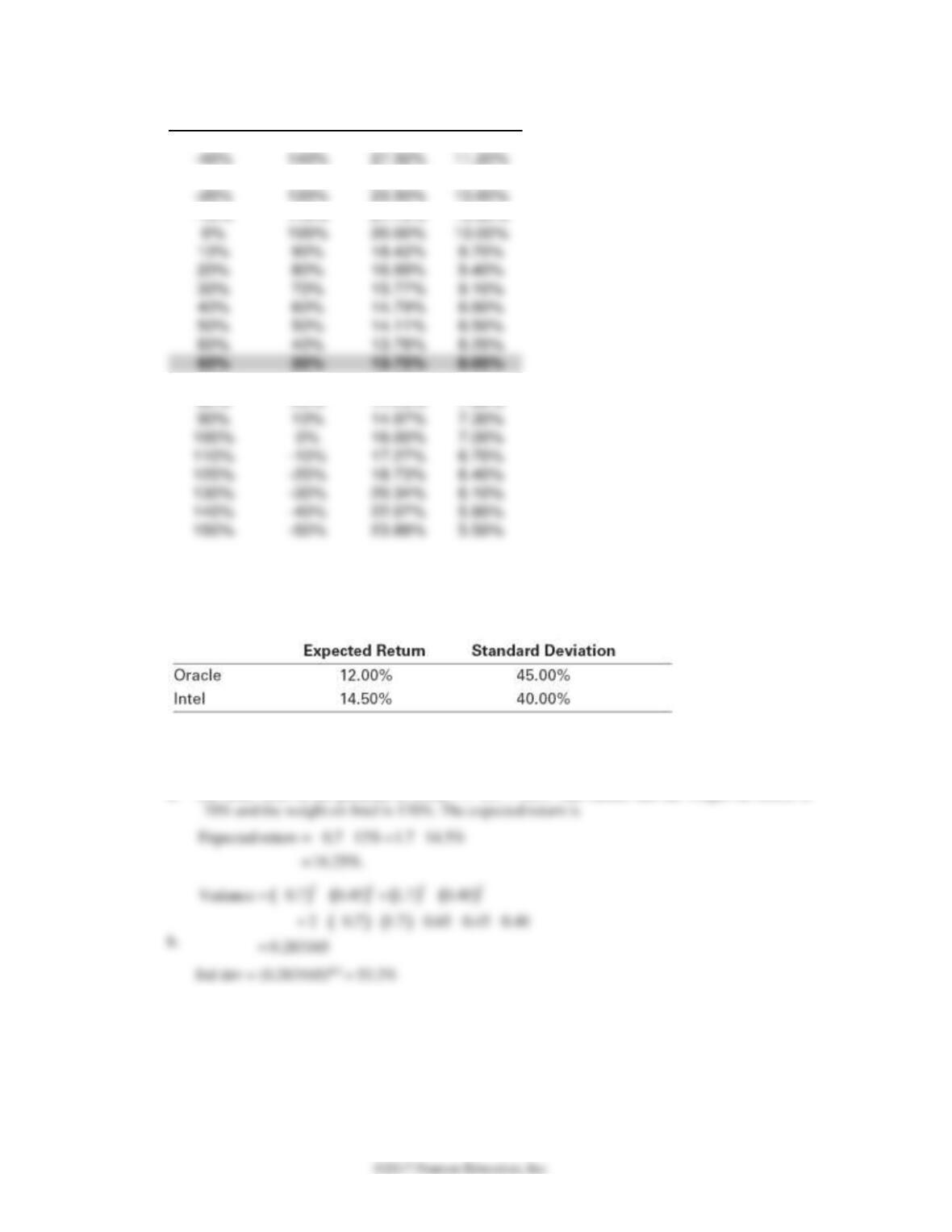

11–27. A hedge fund has created a portfolio using just two stocks. It has shorted $35,000,000 worth of

Oracle stock and has purchased $85,000,000 of Intel stock. The correlation between Oracle’s and

Intel’s returns is 0.65. The expected returns and standard deviations of the two stocks are given

in the table below:

a. What is the expected return of the hedge fund’s portfolio?

b. What is the standard deviation of the hedge fund’s portfolio?

a. The total value of the portfolio is $50m = (–$35 + $85). This means that the weight on Oracle is

11–28. Consider the portfolio in Problem 27. Suppose the correlation between Intel and Oracle’s stock

increases, but nothing else changes. Would the portfolio be more or less risky with this change?

Chapter 11/Optimal Portfolio Choice and the Capital Asset Pricing Model 171

If the correlation increased to 0.8, for example, the variance is

11–29. Fred holds a portfolio with a 30% volatility. He decides to short sell a small amount of stock with

a 40% volatility and use the proceeds to invest more in his portfolio. If this transaction reduces

the risk of his portfolio, what is the minimum possible correlation between the stock he shorted

and his original portfolio?

From Eq. 11.13, for a small transaction size, short selling A and investing in P changes risk according

11–30. Suppose Target’s stock has an expected return of 20% and a volatility of 40%, Hershey’s stock

has an expected return of 12% and a volatility of 30%, and these two stocks are uncorrelated.

a. What is the expected return and volatility of an equally weighted portfolio of the two stocks?

Consider a new stock with an expected return of 16% and a volatility of 30%. Suppose this new

stock is uncorrelated with Target’s and Hershey’s stock.

b. Is holding this stock alone attractive compared to holding the portfolio in (a)?

c. Can you improve upon your portfolio in (a) by adding this new stock to your portfolio?

Explain.

a.

A B Corr

ER 20% 12%

11–31. You have $10,000 to invest. You decide to invest $20,000 in Google and short sell $10,000 worth

of Yahoo! Google’s expected return is 15% with a volatility of 30% and Yahoo!’s expected

return is 12% with a volatility of 25%. The stocks have a correlation of 0.9. What is the expected

return and volatility of the portfolio?

11–32. You expect HGH stock to have a 20% return next year and a 30% volatility. You have $25,000 to

invest, but plan to invest a total of $50,000 in HGH, raising the additional $25,000 by shorting

either KBH or LWI stock. Both KBH and LWI have an expected return of 10% and a volatility

of 20%. If KBH has a correlation of +0.5 with HGH, and LWI has a correlation of −0.50 with

HGH, which stock should you short?

11–33. Suppose you have $100,000 in cash, and you decide to borrow another $15,000 at a 4% interest

rate to invest in the stock market. You invest the entire $115,000 in a portfolio J with a 15%

expected return and a 25% volatility.

a. What is the expected return and volatility (standard deviation) of your investment?

b. What is your realized return if J goes up 25% over the year?

c. What return do you realize if J falls by 20% over the year?

11–34. You have $100,000 to invest. You choose to put $150,000 into the market by borrowing $50,000.

a. If the risk-free interest rate is 5% and the market expected return is 10%, what is the

expected return of your investment?

b. If the market volatility is 15%, what is the volatility of your investment?

11–35. You currently have $100,000 invested in a portfolio that has an expected return of 12% and a

volatility of 8%. Suppose the risk-free rate is 5%, and there is another portfolio that has an

expected return of 20% and a volatility of 12%.

a. What portfolio has a higher expected return than your portfolio but with the same

volatility?

b. What portfolio has a lower volatility than your portfolio but with the same expected return?

Invest an amount x in the other portfolio and the expected return and volatility are

E[Rx]=rf+x(E[RO]–rf)=5% +x(20% –5%)

SD(Rx)=x SD(RO)=x(12%).

11–36. Assume the risk-free rate is 4%. You are a financial advisor, and must choose one of the funds

below to recommend to each of your clients. Whichever fund you recommend, your clients will

then combine it with risk-free borrowing and lending depending on their desired level of risk.

Which fund would you recommend without knowing your client’s risk preference?

11–37. Assume all investors want to hold a portfolio that, for a given level of volatility, has the

maximum possible expected return. Explain why, when a risk-free asset exists, all investors will

choose to hold the same portfolio of risky stocks.

11–38. In addition to risk-free securities, you are currently invested in the Tanglewood Fund, a broad–

based fund of stocks and other securities with an expected return of 12% and a volatility of 25%.

Currently, the risk-free rate of interest is 4%. Your broker suggests that you add a venture

capital fund to your current portfolio. The venture capital fund has an expected return of 20%, a

volatility of 80%, and a correlation of 0.2 with the Tanglewood Fund. Calculate the required

return and use it to decide whether you should add the venture capital fund to your portfolio.

11–39. You have noticed a market investment opportunity that, given your current portfolio, has an

expected return that exceeds your required return. What can you conclude about your current

portfolio?

11–40. The Optima Mutual Fund has an expected return of 20% and a volatility of 20%. Optima claims

that no other portfolio offers a higher Sharpe ratio. Suppose this claim is true, and the risk-free

interest rate is 5%.

a. What is Optima’s Sharpe Ratio?

b. If eBay’s stock has a volatility of 40% and an expected return of 11%, what must be its

correlation with the Optima Fund?

c. If the SubOptima Fund has a correlation of 80% with the Optima Fund what is the Sharpe

ratio of the SubOptima Fund?

11–41. You are currently only invested in the Natasha Fund (aside from risk-free securities). It has an

expected return of 14% with a volatility of 20%. Currently, the risk-free rate of interest is 3.8%.

Your broker suggests that you add Hannah Corporation to your portfolio. Hannah Corporation

has an expected return of 20%, a volatility of 60%, and a correlation of 0 with the Natasha Fund.

a. Is your broker right?

b. You follow your broker’s advice and make a substantial investment in Hannah stock so that,

considering only your risky investments, 60% is in the Natasha Fund and 40% is in Hannah

stock. When you tell your finance professor about your investment, he says that you made a

mistake and should reduce your investment in Hannah. Is your finance professor right?

c. You decide to follow your finance professor’s advice and reduce your exposure to Hannah.

Now Hannah represents 15% of your risky portfolio, with the rest in the Natasha fund. Is

this the correct amount of Hannah stock to hold?

Initial Portfolio

60-40 Portfolio

85-15 Portfolio

Natasha Fund

Expected Return

0.14

0.14

0.14

Expected Return

0.2

0.2

0.2

Volatility

0.6

0.6

0.6

Risk-Free Rate

0.038

0.038

0.038

Portfolio weight in Hannah

0

0.4

0.15

Expected Return of Portfolio

0.14

0.164

0.149

Volatility of Portfolio

0.2

11–42. Calculate the Sharpe ratio of each of the three portfolios in Problem 39. What portfolio weight in

Hannah stock maximizes the Sharpe ratio?

Initial Portfolio

60-40 Portfolio

85-15 Portfolio

Natasha Fund

Expected Return

0.14

0.14

0.14

Hannah Stock

Expected Return

0.2

0.2

0.2

0.6

0.6

0.6

Risk-Free Rate

0.038

0.038

0.038

Portfolio weight in Hannah

0

0.4

0.15

Expected Return of Portfolio

0.14

0.164

0.149

Volatility of Portfolio

0.2

Sharpe Ratio

0.51

0.09002

The Sharpe Ratio is maximized at 15% in Hannah Stock.

11–43. Returning to Problem 38, assume you follow your broker’s advice and put 50% of your money in

the venture fund.

a. What is the Sharpe ratio of the Tanglewood Fund?

b. What is the Sharpe ratio of your new portfolio?

c. What is the optimal fraction of your wealth to invest in the venture fund? (Hint:Use Excel

Initial Portfolio

50-50 Split

Tanglewood Fund

Expected Return

0.12

0.12

Volatility

0.25

0.25

0.25

Venture Fund

Expected Return

0.2

0.2

0.8

0.8

Risk-Free Rate

0.04

0.04

Portfolio weight in Hannah

0

0.5

Expected Return of Portfolio

0.12

0.16

Volatility of Portfolio

0.25

0.25

Sharpe Ratio

0.32

0.0656

176 Berk/DeMarzo, Corporate Finance, Fourth Edition

The Sharpe Ratio is maximized at 12% in the venture fund.

Weight in venture fund

Expected Return

Volatility

Sharpe Ratio

0

0.12

0.25

0.32

Part a

0.01

0.1208

0.249223293

0.324207256

0.02

0.1216

0.248694592

0.328113287

0.03

0.1224

0.248415479

0.331702358

0.04

0.1232

0.248386795

0.334961446

0.05

0.124

0.248608628

0.337880469

0.06

0.1248

0.249080308

0.340452445

0.07

0.1256

0.24980042

0.342673563

0.08

0.1264

0.250766824

0.344543184

0.09

0.1272

0.251976685

0.346063763

0.11

0.1288

0.25511223

0.348082097

0.12

0.1296

0.257029181

0.34859855

0.13

0.1304

0.25917224

0.348802788

Part c

0.14

0.1312

0.261535848

0.348709366

0.15

0.132

0.264114085

0.348334319

0.16

0.1328

0.266900731

0.347694814

0.17

0.1336

0.269889329

0.346808821

0.18

0.1344

0.27307325

0.34569479

0.19

0.1352

0.276445745

0.34437137

0.2

0.136

0.28

0.342857143

0.21

0.1368

0.283729184

0.341170403

0.22

0.1376

0.287626494

0.339328963

0.23

0.1384

0.29168519

0.337350004

0.24

0.1392

0.295898631

0.335249945

0.25

0.14

0.300260304

0.333044358

0.26

0.1408

0.304763843

0.330747896

0.27

0.1416

0.309403054

0.328374263

0.28

0.1424

0.314171927

0.325936187

0.29

0.1432

0.319064649

0.323445422

0.3

0.144

0.324075608

0.31

0.1448

0.329199408

0.318348082

0.32

0.1456

0.33443086

0.315760334

0.33

0.1464

0.339764992

0.313157631

0.34

0.1472

0.345197045

0.31054727

0.35

0.148

0.350722469

0.307935789

0.36

0.1488

0.356336919

0.305329013

0.37

0.1496

0.362036255

0.302732112

0.38

0.1504

0.36781653

0.300149642

0.39

0.1512

0.373673989

0.297585605

0.4

0.152

0.379605058

0.295043487

0.41

0.1528

0.385606341

0.29252631

0.42

0.1536

0.39167461

0.290036671

0.43

0.1544

0.3978068

0.287576784

0.44

0.1552

0.404

0.285148515

0.45

0.156

0.410251447

0.282753421

Chapter 11/Optimal Portfolio Choice and the Capital Asset Pricing Model 177

Weight in venture fund

Expected Return

Volatility

Sharpe Ratio

0.46

0.1568

0.416558519

0.280392777

0.47

0.1576

0.422918727

0.278067611

0.48

0.1584

0.42932971

0.275778725

0.49

0.1592

0.435789227

0.273526725

0.5

0.16

0.44229515

0.271312041

Part b

0.51

0.1608

0.448845463

0.269134947

0.52

0.1616

0.45543825

0.26699558

0.53

0.1624

0.462071694

0.264893958

0.54

0.1632

0.468744067

0.262829994

0.55

0.164

0.475453731

0.260803506

0.56

0.1648

0.482199129

0.258814238

0.57

0.1656

0.488978783

0.256861861

0.58

0.1664

0.495791287

0.254945989

0.59

0.1672

0.502635305

0.253066187

0.6

0.168

0.509509568

0.251221975

0.61

0.1688

0.516412868

0.24941284

0.62

0.1696

0.523344055

0.247638239

0.63

0.1704

0.530302037

0.245897604

0.64

0.1712

0.537285771

0.244190349

0.65

0.172

0.544294268

0.242515874

0.66

0.1728

0.551326582

0.240873566

0.67

0.1736

0.558381814

0.239262807

0.68

0.1744

0.565459106

0.237682971

0.69

0.1752

0.572557639

0.236133431

11–44. When the CAPM correctly prices risk, the market portfolio is an efficient portfolio. Explain why.

11–45. A big pharmaceutical company, DRIg, has just announced a potential cure for cancer. The stock

price increased from $5 to $100 in one day. A friend calls to tell you that he owns DRIg. You

proudly reply that you do too. Since you have been friends for some time, you know that he holds

the market, as do you, and so you both are invested in this stock. Both of you care only about

expected return and volatility. The risk-free rate is 3%, quoted as an APR based on a 365-day

year. DRIg made up 0.2% of the market portfolio before the news announcement.

a. On the announcement, your overall wealth went up by 1% (assume all other price changes

canceled out so that without DRIg, the market return would have been zero). How is your

wealth invested?

b. Your friend’s wealth went up by 2%. How is he invested?

11–46. Your investment portfolio consists of $15,000 invested in only one stock—Microsoft. Suppose the

risk-free rate is 5%, Microsoft stock has an expected return of 12% and a volatility of 40%, and

the market portfolio has an expected return of 10% and a volatility of 18%. Under the CAPM

assumptions,

a. What alternative investment has the lowest possible volatility while having the same

expected return as Microsoft? What is the volatility of this investment?

b. What investment has the highest possible expected return while having the same volatility as

Microsoft? What is the expected return of this investment?

a. Under the CAPM assumptions, the market is efficient; that is, a leveraged position in the market

has the highest expected return of any portfolio for a given volatility and the lowest volatility for a

given expected return. By holding a leveraged position in the market portfolio, you can achieve an

expected return of

b. A leveraged portion in the market has volatility

h

11–47. Suppose you group all the stocks in the world into two mutually exclusive portfolios (each stock

is in only one portfolio): growth stocks and value stocks. Suppose the two portfolios have equal

size (in terms of total value), a correlation of 0.5, and the following characteristics:

The risk-free rate is 2%.

a. What is the expected return and volatility of the market portfolio (which is a 50–50

combination of the two portfolios)?

Chapter 11/Optimal Portfolio Choice and the Capital Asset Pricing Model 179

b. Does the CAPM hold in this economy? (Hint: Is the market portfolio efficient?)

11–48. Suppose the risk-free return is 4% and the market portfolio has an expected return of 10% and

a volatility of 16%. Merck & Co. (Ticker: MRK) stock has a 20% volatility and a correlation

with the market of 0.06.

a. What is Merck’s beta with respect to the market?

b. Under the CAPM assumptions, what is its expected return?

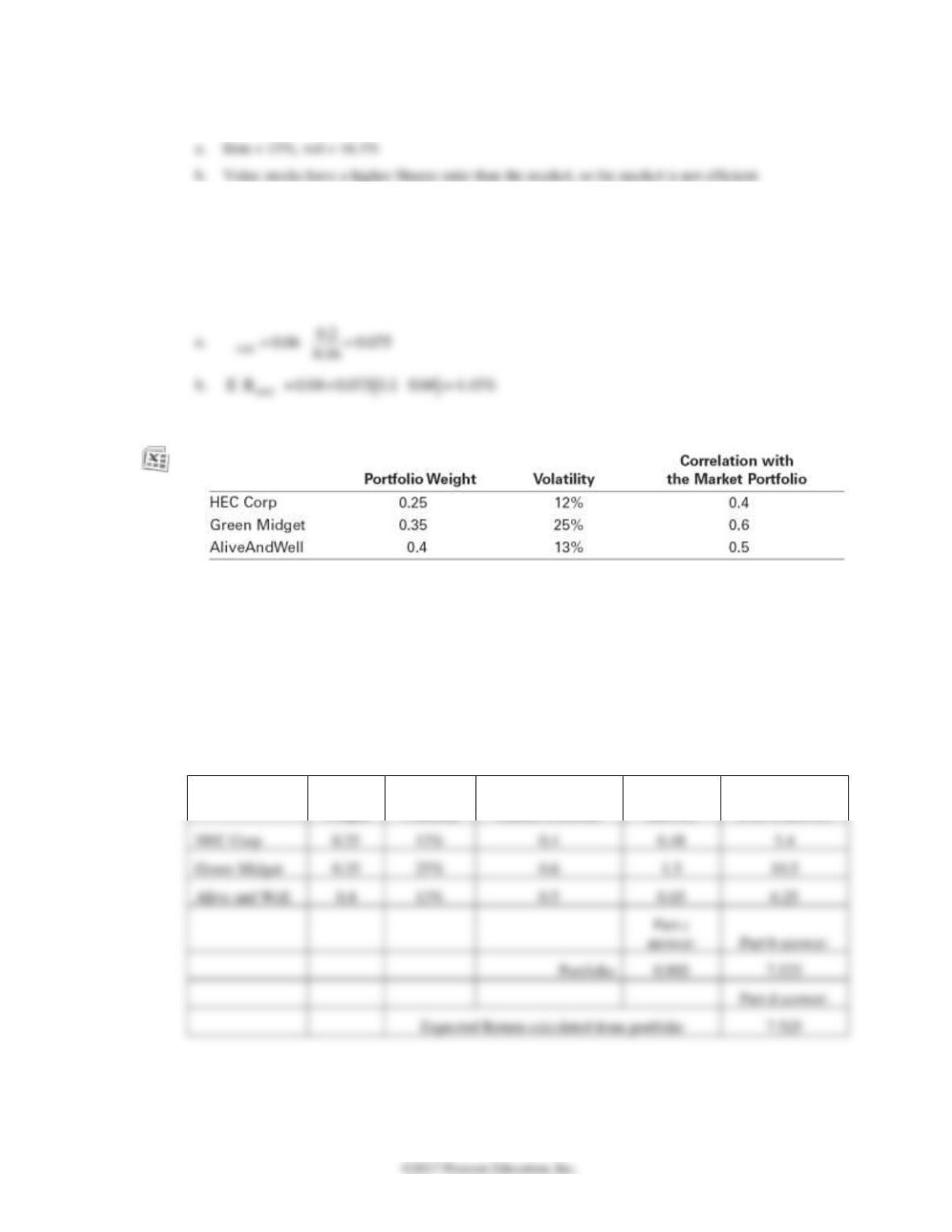

11–49. Consider a portfolio consisting of the following three stocks:

The volatility of the market portfolio is 10% and it has an expected return of 8%. The risk-free

rate is 3%.

a. Compute the beta and expected return of each stock.

b. Using your answer from part a, calculate the expected return of the portfolio.

c. What is the beta of the portfolio?

d. Using your answer from part c, calculate the expected return of the portfolio and verify that

it matches your answer to part b.

Portfolio

Weight

Volatility

Correlation with the

Market Portfolio

Beta (Part a

answer)

Expected Return

(Part a answer)

11–50. Suppose Autodesk stock has a beta of 2.16, whereas Costco stock has a beta of 0.69. If the risk–

free interest rate is 4% and the expected return of the market portfolio is 10%, what is the

expected return of a portfolio that consists of 60% Autodesk stock and 40% Costco stock,

according to the CAPM?

11–51. What is the risk premium of a zero-beta stock? Does this mean you can lower the volatility of a

portfolio without changing the expected return by substituting out any zero-beta stock in a

portfolio and replacing it with the risk-free asset?