Chapter 10 Risk and Capital Budgeting

Chapter Overview

The Opening Focus looks at Hershey and how Deutsche Bank estimated the Weighted Average

Cost of Capital for this sweet giant. They found they had underestimated Hershey by nearly 4 per-

Opening Focus Discussion Questions:

1. How does WACC impact firm value? In other words, why does a minimum WACC maximize

firm value? How can shareholders use the WACC to choose an appropriate stock for their

portfolio?

2. How could Hershey further minimize its cost of capital? How easy would it be for the firm to

lower its cost of debt or equity or change the weights in the WACC to provide a lower cost of

capital?

This chapter concludes capital budgeting with:

10-1 Choosing the Right Discount Rate

10-4 Strategy and Capital Budgeting

Technology

1. Smart Practices Video. Beth Acton, former vice president and treasurer of Ford Motor Co.,

talks about the importance of the WACC calculation to Ford, since WACC is used in product

programs, capital investments and acquisition decisions.

3. Smart Concepts provide step-by-step explanations of scenario analysis and Monte Carlo

simulations.

5. Smart Practices Video. Pam Roberts, executive director of Corporate Services for Cummins

Inc., notes the difficulty in predicting future cash flow variables.

6. Smart Practices Video. Andy Bryant, executive vice president of finance and enterprise sys-

278 Instructor’s Manual

8. Smart Solutions provide a step-by-step solution for problem P10-3, looking at real firm’s op-

erating leverage.

Lecture Guide

This chapter brings together concepts from previous chapters. The Capital Asset Pricing

Model was previously introduced. Now, the CAPM required return can be a component of a com-

10-1 Choosing the Right Discount Rate

The discount rate must be a rate that compensates the investor for the project’s risk. Technical-

ly the discount rate should vary with the project since few projects have identical risk, but for sim-

plicity sake, use a rate for debt and a rate for equity.

• Note also that debt and equity do not have to be the only components of WACC. A firm

10-1a Cost of Equity

Marketing majors will appreciate the section on breakeven analysis which is used frequent-

ly in marketing decisions. With financial breakeven analysis, the firm looks at which strategy pro-

vides more income per shareholder, in the form of earnings per share. The firm looks at possible

A Simple Case

Carbonlite Inc. Cost of Equity

This example is a graphical representation of the differences between firms with differing degrees

of operating leverage. Note that the slope of the Carbonlite line is much steeper than the Fiber-

Chapter 10 Risk and Capital Budgeting 279

Figure 10.1 Risk Adjustments to Cash Flows and Discount Rates

Table 10.1 Financial Date for Carbonlite, Inc., and Fiberspeed Corp.

Figure 10.2 Operating Leverage for Carbonlite, Inc., and Fiberspeed Corp.

Table 10.2 The Effect of Financial Leverage on Shareholder Returns

10-1b The Weighted Average Cost of Capital

The appropriate discount rate for an all equity firm is the cost of equity. Many firms, how-

Table 10.3 Cash Distribution to Lox in a Box Investors

Finding WACC for Firms with Complex Capital Structures

While debt and equity are the most common components of WACC, some firms finance

10-1c The WACC, CAPM, and Taxes

Rules for Selecting an Appropriate Project Discount Rate

This section summarizes information on previous sections:

1.) If an all equity firm invests in an asset with similar risks to past assets, then the all

equity beta is the appropriate discount rate for NPV calculations.

Accounting for Taxes in Finding WACC

Note that the before tax cost of equity and preferred stock are the same as the after tax cost

280 Instructor’s Manual

10-2 A Closer Look at Risk

10-2a Break-Even Analysis

A firm must cover its variable and fixed costs in order to be profitable. A firm may want to

know how many units or how much in dollar sales is necessary for the firm to earn a profit. While

cash flows are central to capital budgeting problems, not accounting profits, a firm must ultimately

turn a profit, or it will not stay in business very long. While mathematically, this is an easy calcu-

Figure 10.3a : Break-Even for Carbonlite

In break-even analysis, take the firm’s fixed costs and then add variable costs to find total

costs. Variable costs include those costs that vary with the level of production, typically materials

and labor costs. Fixed costs include such expenses as executive salaries and overhead departments

Figure 10.3b: Break-Even Point for Fiberspeed

Carbonlite has higher fixed costs and a higher breakeven point than Fiberspeed. Notice

that Carbonlite’s total cost line has a flatter slope than Fiberspeed’s. This is because Fiberspeed is

10-2b Sensitivity Analysis

A sensitivity analysis is a very important part of any problem. You are never completely

sure of every input into a problem. It makes sense to show sensitivity to the variables you are least

Table 10.4: Sensitivity Analysis of the Gyroscope Skateboard Project

Chapter 10 Risk and Capital Budgeting 281

10-2c Scenario Analysis and Monte Carlo Simulation

10-2d Decision Trees

Fig. 10-4 Decision Trees for Odessa Investment

10-3 Real Options in Capital Budgeting

10.3a Why NPV May Not Always Give the Right Answer:

More and more managers are looking at real option valuation. More managers recognize that

there are options embedded in projects, and that it is appropriate to use option pricing to value the

projects. (You know that real option pricing is becoming more mainstream when firms like Dun

10-3b Types of Real Options

• Expansion options

Some examples of real options include:

10.3c The Surprising Link Between Risk and Real Option Values

We have seen in the past that if a project is more risky, then the required return should be

10-4 Strategy and Capital Budgeting

10-4a Competition and NPV

10-4b Strategic Thinking and Real Options

282 Instructor’s Manual

Risk and Capital Budgeting Summary

Experience and intuition also can count in a capital budgeting decision. If managers can dissect

Enrichment Exercise

1. Have students examine the latest opening of new WalMart stores and decide if the WACC

should be the same or different for each store (especially look at international projects).

2. Divide students into groups for the following exercise:

a. Half the students will represent the acquiring company

b. The other half will represent the target company.

Information for students representing the acquiring company

ABC company is developing a new technology. You represent XYZ company which is thinking of

Information for students representing the target company

ABC company is developing a new technology. You know that there is a 50% probability that the

Pair up groups and have them negotiate using the above information. Very likely, this will be a

very short negotiation. If the target company stands firm, and the bidder company correctly calcu-

Have the same groups negotiate with each other for the technology. Now the groups are much

more likely to reach agreement.

Chapter 10 Risk and Capital Budgeting 283

Answers to Concept Review Questions

1. The cost of equity is not appropriate to discount cash flows because it does not correctly reflect

2. Two firms could have very different equity betas if they have chosen differing capital struc-

tures. The firm using more debt financing will have a higher equity beta. Betas can also vary

3. If a firm is thinking of expanding its existing line of business, the WACC rather than the cost of

4. The cost of debt, rd, is generally less than the cost of equity, re, because debt is a less risky se-

curity. A naive application of the WACC formula might suggest that a firm could lower its cost

5. A project that reaches the breakeven point in terms of net income could potentially be bad for

6. In a project sensitivity analysis, the analysis is probably more sensitive to changes in the

growth rate of sales. Sales drive the cash flow analysis—many other variables are based on a

7. The assumptions that the airline would likely need to put into place in order to run a Monte

Carlo simulation on ticket prices for a new, nonstop flight between Atlanta and Tokyo might

284 Instructor’s Manual

8. The discount rate could vary as you move through a decision tree because parts of a project

9. A real world example of an expansion option would be the possibility of derivative products

after the first product was introduced. For example, suppose a company develops a new air-

10. Risk lowers the value of a project (higher discount rate, lower value), but increases the value of

an option. This is because as the risk becomes greater, more possibilities open up that the cash

11. Managers’ intuition is useful because you must be able to explain NPV. If you have a positive

Solutions to Self-Test Problems

ST10-1. A financial analyst for Quality Investments, a diversified investment fund, has gathered

the following information for the years 2012 and 2013 on two firms—A and B—that it is

considering adding to its portfolio. Of particular concern are the operating and financial

risks of each firm.

2012 2013 .

Firm A Firm B Firm A FirmB

Sales ($million) 10.7 13.9 11.6 14.6

EBIT ($million) 5.7 7.4 6.2 8.1

Assets ($million) 10.7 15.6

Debt ($million) 5.8 9.3

Interest ($million) 0.6 1.0

Equity ($million) 4.9 6.3

a. Use the data provided to assess the operating leverage of each firm (using 2012 as

the point of reference). Which firm has more operating leverage?

b. Use the data provided to assess the firms ROE (cash to equity/common stock equity)

assuming the firm’s Return on Assets is 10% and 20% in each case. Which firm has

more financial leverage?

c. Use your findings in parts a and b to compare and contrast the operating and finan-

cial risks of Firms A and B. Which firm is more risky? Explain.

Chapter 10 Risk and Capital Budgeting 285

A: a. ∆EBIT ∆Sales

Operating leverage = EBIT ÷ Sales

b. Firm A Firm B

When Return on Assets Equals 10%

Firm B has more financial leverage as demonstrated by the broader range of ROEs

it experiences when the return on assets moves from 10% to 20%. Note that Firm B’s

ROE is lower than Firm A’s at the 10% return on assets and its higher than Firm B’s

ROE at the 20% return on assets. Firm B’s ROE has greater variability—is more re-

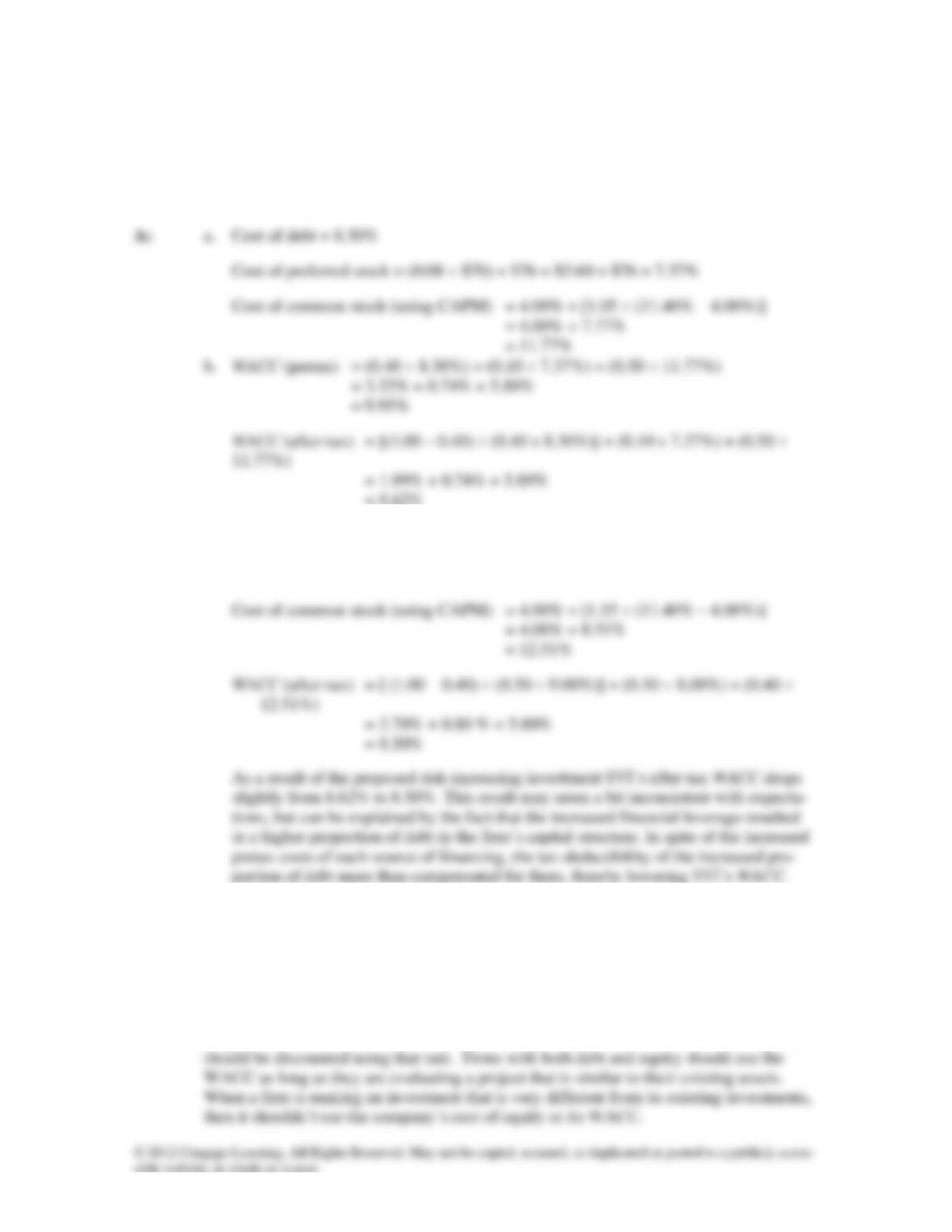

ST10-2. Sierra Vista Industries (SVI) wishes to estimate its cost of capital for use in analyzing

projects that are similar to those that already exist. The firm’s current capital structure in

terms of market value includes 40 percent debt, 10% preferred stock, and 50% common

stock. The firm’s debt has an average yield to maturity of 8.3%. Its preferred stock has a

$70 par value, an 8% dividend, and is currently selling for $76 per share. SVI’s beta is

1.05, the risk-free rate is 4%, and the return on the S&P 500 (the market proxy) is 11.4%.

CVI is in the 40% tax bracket.

a. What are SVI’s pretax costs of debt, preferred stock, and common stock?

b. Calculate SVI’s weighted average cost of capital (WACC) on both a pretax and after-

tax basis. Which WACC should SVI use when making investment decisions?

c. SVI is contemplating a major investment that is expected to increase both its operat-

ing and financial leverage. Its new capital structure will contain 50% debt, 10% pre-

ferred stock, and 40% common stock. As a result of the proposed investment, the

286 Instructor’s Manual

firm’s average yield to maturity on debt is expected to increase to 9%, the market

value of preferred stock is expected to fall to its $70 par value, and its beta is ex-

pected to rise to 1.15. What effect will this investment have on SVI’s WACC? Ex-

plain your finding.

= 8.62%

c. Cost of debt = 9.00%

Cost of preferred stock = (0.08 $70) ÷ $70 = $5.60 ÷ $70 = 8.00%

Answers to End-of-Chapter Questions

Q10-1. Explain when firms should discount projects using the cost of equity. When should they

use the WACC instead? When should they use neither?

A10-1. Only firms with no debt in their capital structure should use the cost of equity to discount

project cash flows, and only those projects that are very similar to a firm’s existing assets

Chapter 10 Risk and Capital Budgeting 287

Q10-2. If a firm takes actions that increase its operating leverage, we might expect to see an in-

crease in its equity beta. Why?

A10-2. Operating leverage makes a firm’s profits and cash flows more variable and more sensi-

Q10-3. Firm A and Firm B plan to raise $1 million to finance identical projects. Firm A finances

the project with 100% equity, while firm B uses a 50-50 mix of debt and equity. The in-

terest rate on the debt equals 7%. At what rate of return on the investment (i.e., assets)

will the rate of return on equity be the same for Firms A and B? (Hint: Think through

Table 10.2.)

Q10-4. Why do you think it is important to use the market values of debt and equity rather than

book values to calculate a firm’s WACC?

A10-4. Market values provide a better gauge of the true degree of leverage that a firm employs.

A personal finance analogy may help drive this point home. Suppose someone buys a

new home for $100,000, using $90,000 of borrowed money and $10,000 of personal

Q10-5. Assuming that there are no corporate income taxes, how can the costs of preferred stock

and debt be estimated?

A10-5. With no taxes, if you plug a firm’s asset beta into the CAPM equation the resulting rate

of return is the WACC. We can see this by starting with the equation for the WACC:

ED

D

r

ED

E

rWACC de +

+

+

=

288 Instructor’s Manual

Q10-6. What are the three main lessons learned with regard to choosing the right discount rate

for use in evaluating capital budgeting projects?

A10-6. 1. When an all-equity firm invests in an asset similar to its existing assets, the cost of

equity is the appropriate discount rate to use in NPV calculations.

Q10-7. How does the calculation of the after-tax WACC differ from that of the before-tax

WACC? Which method is typically applied in the United States? Why?

A10-7. The difference in calculating after-tax WACC is that companies are entitled to deduct

interest payments on their debt from the taxable income. This opportunity reduces the af-

Q10-8. In what sense could one argue that if managers make decisions using breakeven analysis,

they are not maximizing shareholder wealth? How can breakeven analysis be modified to

solve this problem?

A10-8. A problem with break-even analysis is that it uses accounting numbers – earnings before

interest and taxes and earnings per share. Accounting numbers can be manipulated, and

Q10-9. Explain the differences between sensitivity analysis and scenario analysis. Offer an ar-

A10-9. Sensitivity analysis looks at how changes in a single variable affect a project’s NPV.

Scenario analysis looks at how several changes occurring simultaneously affect the NPV.

Chapter 10 Risk and Capital Budgeting 289

Q10-10. In Chapter 9, we discussed how one might calculate the NPV of earning an MBA. Sup-

pose that you are asked to do a sensitivity analysis on the MBA decision. Which of the

following factors do you think would have a larger impact on the degree’s NPV?

A10-10. The factor least likely to affect the NPV of getting an MBA is your GPA. There are fair-

ly large starting salary differentials earned by graduates at different schools, and similar

Q10-11. Suppose you want to model the value an MBA degree with decision trees. What would

such a decision tree look like?

A10-11. The first part of the tree might indicate the initial choice to get an MBA or not. Subse-

Q10-12. If you decide to invest in an MBA, what is your follow-on investment option? What is

your abandonment option?

Q10-13. Your company is selling the mineral rights to several hundred acres of land it owns that

are believed to contain silver deposits. The current price of silver is $18 per ounce, but of

course, future prices are uncertain. Would you expect the mineral rights to sell for more

or less if investors believe that silver prices will be more volatile in the future than they

have been in the past? Explain.

A10-13. Rights would be more valuable if the price of silver is volatile. If the price is volatile,

Solutions to End-of-Chapter Problems

Choosing the Right Discount Rate

P10-1. Puritan Motors has a capital structure consisting almost entirely of equity.

a. If the beta of Puritan stock equals 1.6, the risk-free rate equals 6%, and the expected re-

turn on the market portfolio equals 11%, what is its cost of equity?