1

2

3

4

5

6

7

8

9

10

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

result of the NPV function.

A B C D E F G H I J K L M N O P Q R S

11/20/2018

Situation

Franchise S

Year (t) Franchise S Franchise L Year 0 1 2 3

0-$100 -$100 CF -100 70 50 20

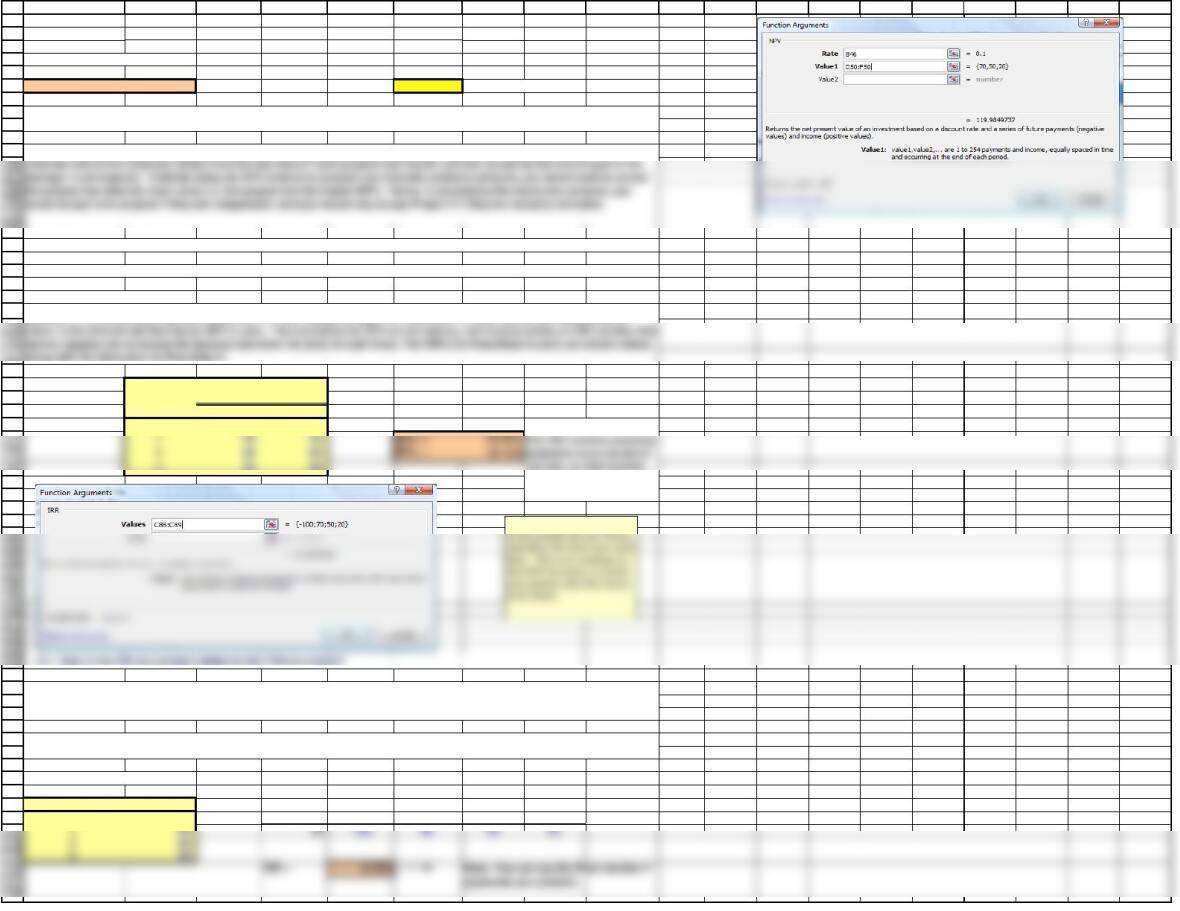

Net Present Value (NPV)

Depreciation, salvage values, net working capital requirements, and tax effects are all included in these cash flows.

You also have made subjective risk assessments of each franchise and concluded that both franchises have risk characteristics

that require a return of 10%. You must now determine whether one or both of the franchises should be accepted.

c. (1.) Define the term net present value (NPV). What is each franchise’s NPV?

To calculate the NPV, we find the present value of the individual cash flows and find the sum of those discounted cash flows.

This value represents the value the project add to shareholder wealth.

a. What is capital budgeting? Answer: See Chapter 10 Mini Case Show

b. What is the difference between independent and mutually exclusive projects? Answer: See Chapter 10 Mini Case Show

Chapter 10. Mini Case

Expected

Net Cash Flows

You have just graduated from the MBA program of a large university, and one of your favorite courses was “Today‘s

Entrepreneurs.” In fact, you enjoyed it so much you have decided you want to “be your own boss.” While you were in the

master’s program, your grandfather died and left you $1 million to do with as you please. You are not an inventor, and you do not

have a trade skill that you can market; however, you have decided that you would like to purchase at least one established

franchise in the fast-foods area, maybe two (if profitable). The problem is that you have never been one to stay with any project

for too long, so you figure that your time frame is three years. After three years you will go on to something else.

55

56

57

58

59

60

61

62

63

64

65

72

73

74

75

76

77

78

82

83

84

85

86

89

90

91

92

93

94

95

96

97

98

99

100

101

102

103

104

(2.) How is the IRR on a project related to the YTM on a bond?

105

106

107

108

109

110

111

112

113

114

115

116

117

118

119

120

121

122

A B C D E F G H I J K L M N O P Q R S

Franchise L

Time period: 0 1 2 3

Cash flow: -100 10 60 80

Disc. cash flow: -100 950 60

NPV(L) = $18.78 $18.78 = Uses NPV function.

Internal Rate of Return (IRR)

Year (t) Franchise S Franchise L

0-$100 -$100

320 80

Constant Cash Flows

Year (t) Cash Flow

0-$100 Year 0 1 2 3

The NPV method of capital budgeting dictates that all independent projects that have positive NPV should accepted. The

(3.) Would the NPVs change if the cost of capital changed? Answer: See Chapter 10 Mini Case Show

The internal rate of return is defined as the discount rate that equates the present value of a project’s cash inflows to its

outflows. It is the discount rate that forces the PV of the inflows to equal the initial cost. In other words, the internal rate of

d. (1.) Define the term internal rate of return (IRR). What is each franchise’s IRR?

net cash flows

(2.) What is the rationale behind the NPV method? According to NPV, which franchise or franchises should be accepted if they

are independent? Mutually exclusive?

Expected

does not have to be

adjusted.

The IRR is the discount rate that forces the PV of a project’s expected future cash flows to equal the initial cash flow. This is

analogous to a bond’s yield because a bond’s yield is the discount rate that forces the present value of a bonds coupons and

maturity value to equal the price of the bond.

Suppose the initial cost of a project is $100 and it has cash flows of $40 at Years 1, 2, and 3. What is its IRR? Use the Excel

RATE function as though the project were a bond.

Notice that for IRR you

66

67

68

69

70

71

would accept both projects if they are independent, and you would only accept Project S if they are mutually exclusive.

123

124

125

126

127

128

129

130

131

132

137

138

139

140

141

142

143

144

145

146

147

148

149

150

151

152

153

154

155

4% 31.32 4% 36.21

6% 27.33 6% 30.00

156

157

158

159

160

161

162

163

164

165

166

167

168

169

170

171

172

173

174

175

176

177

178

179

180

181

182

183

184

185

186

187

A B C D E F G H I J K L M N O P Q R S

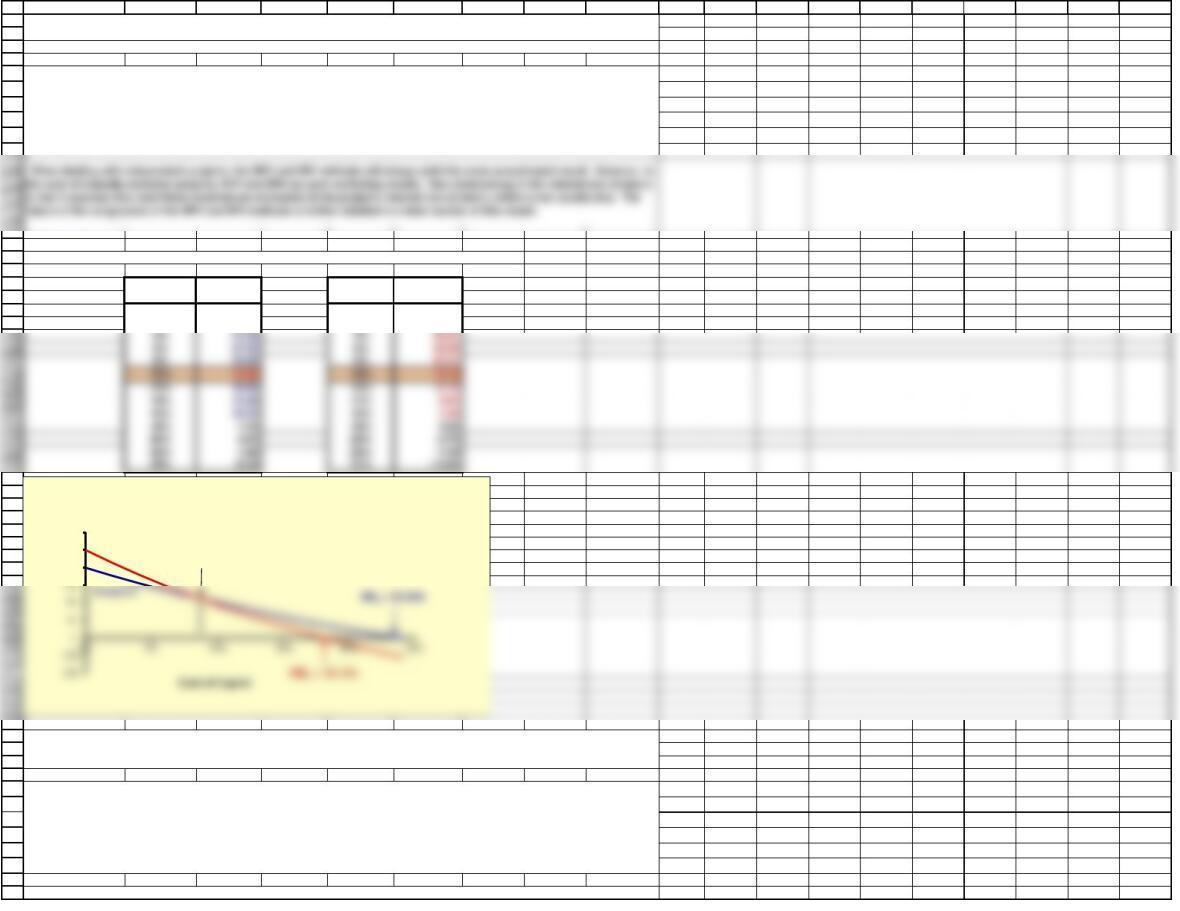

NPV Profiles

e. Draw NPV profiles for Franchises L and S. At what discount rate do the profiles cross?

Franchise S Franchise L

r$19.98 r$18.78

0% 40.00 0% 50.00

2% 35.53 2% 42.86

f. What is the underlying cause of ranking conflicts between NPV and IRR?

The IRR method of capital budgeting maintains that projects should be accepted if their IRR is greater than the cost of capital.

Strict adherence to the IRR method would further dictate that mutually exclusive projects should be chosen on the basis of the

greatest IRR. In this scenario, both franchises have IRRs that exceed the cost of capital (10%) and both should be accepted, if

they are independent. If, however, the franchises are mutually exclusive, we would choose Franchise S. Recall, that this was our

determination using the NPV method as well. The question that naturally arises is whether or not the NPV and IRR methods will

always arrive at the same conclusion.

Previously, we had discussed that in some instances the NPV and IRR methods can give conflicting results. First, we should

attempt to define what we see in this graph. Notice, that the two franchises’ profiles (S and L) intersect the X-axis at costs of

capital of 18.13% and 23.56%, respectively. Not coincidently, those are the IRRs of the franchises. If we think about the

definition of IRR, we remember that the internal rate of return is the cost of capital at which a project will have an NPV of zero.

Looking at our graph, it is a logical conclusion that the project IRR is defined as the point at which its profile intersects the

X-axis.

(4.) Would the franchises’ IRRs change if the cost of capital changed?

(2.) Look at your NPV profile graph without referring to the actual NPVs and IRRs. Which franchise or franchises should be

accepted if they are independent? Mutually exclusive? Explain. Are your answers correct at any cost of capital less than

23.6%?

(3.) What is the logic behind the IRR method? According to IRR, which franchises should be accepted if they are

independent?

40

50

60

NPV ($)

NPV Profile of Franchises S and L

Project L

Crossover

Rate = 8.7%

188

189

190

195

196

197

198

199

200

201

202

203

204

205

206

207

208

209

210

211

high values of t. (2) Long-term projects like L have most of their cash flows coming in the later years, when the discount penalty

is largest; hence, they are most severely impacted by high capital costs. (3) Therefore, Franchise L’s NPV profile is steeper than

212

213

214

215

216

217

218

219

220

221

222

223

224

225

226

229

230

232

233

234

235

236

237

238

239

240

242

244

245

246

247

249

A B C D E F G H I J K L M N O P Q R S

Cash Flow

Year (t) Franchise S Franchise L Differential

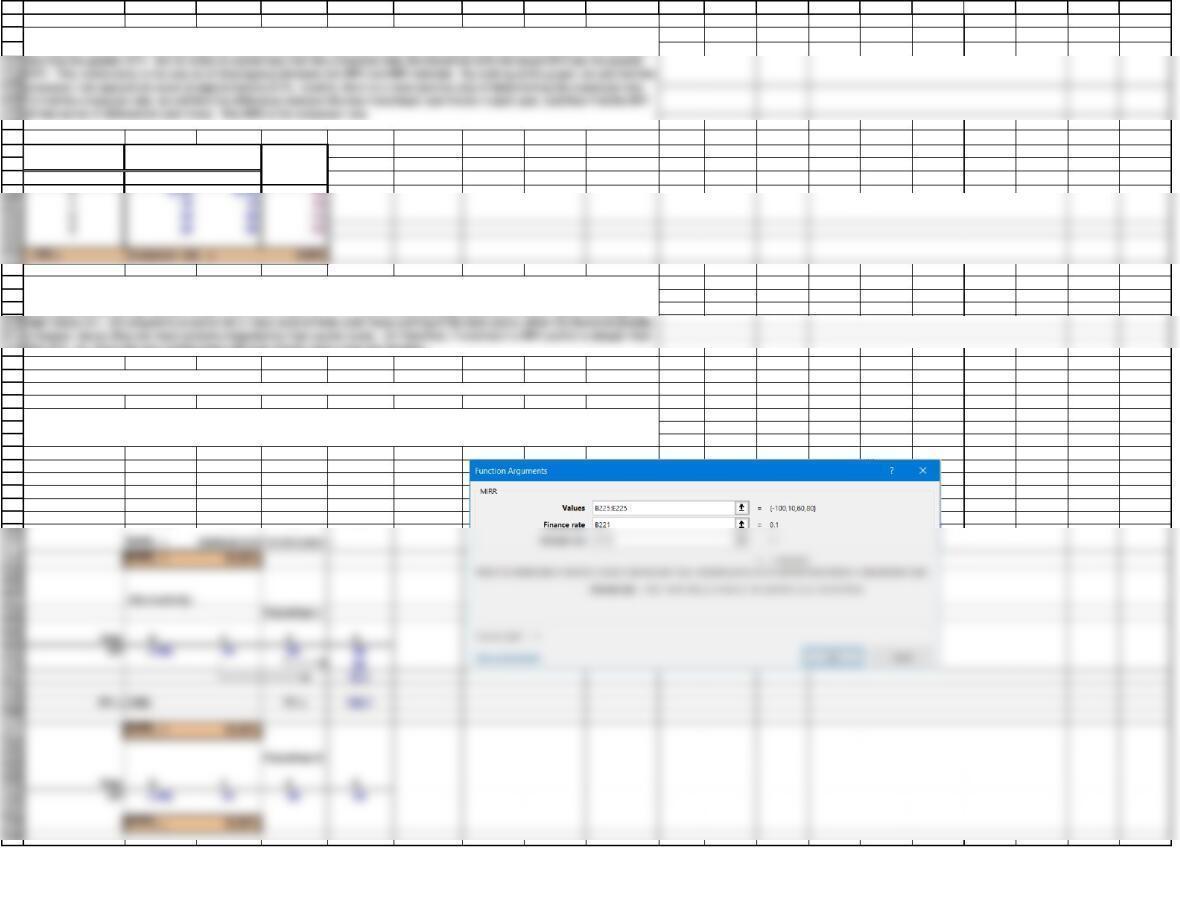

Modified Internal Rate of Return (MIRR)

WACC = 10%

Franchise L

Year 0 1 2 3

CF (100) 10 60 80

g. Define the term modified IRR (MIRR). Find the MIRRs for Franchises L and S.

Expected

Net Cash Flows

The intuition behind the relationship between the NPV profile and the crossover rate is as follows: (1) Distant cash flows are

heavily penalized by high discount rates–the denominator is (1 + r)t, and it increases geometrically; hence, it gets very large at

that of S. (4) Since the two profiles have different slopes, they cross one another.

Looking further at the NPV profiles, we see that the two franchises profiles intersect at a point we shall call the crossover rate.

We observe that at costs of capital greater than the crossover rate, the franchise with the greater IRR (Franchise S, in this case)

The modified internal rate of return is the discount rate that causes a project‘s cost (or cash outflows) to equal the present value

of the project’s terminal value. To find MIRR, use Excel’s MIRR function. Alternatively, calculate the PV of the outflows and the

FV of the inflows and then find the discount rate that equates the two.

250

251

252

253

254

255

256

268

269

270

271

272

273

274

275

276

277

278

279

280

281

282

283

284

285

286

287

288

289

Payback: 1.600

Payback: 1.600

290

291

292

293

294

295

296

297

298

299

300

301

302

303

304

305

306

307

308

309

310

311

312

313

314

315

Franchise S

Time period: 0 1 2 3

Cash flow: -100 70 50 20

Discounted payback period uses the project’s cost of capital to discount the expected cash flows. The calculation of discounted

payback period is identical to the calculation of regular payback period, except you must base the calculation on a new row of

cash flows discounted at r back to t = 0. Note that both projects have a cost of capital of 10%.

316

A B C D E F G H I J K L M N O P Q R S

PROFITABILITY INDEX

h. What does the profitability index (PI) measure? What are the PI’s for Franchises S and L?

Payback Period

Franchise S

Time period: 0 1 2 3

Cash flow: -100 70 50 20

Cumulative cash flow: -100 -30 20 40

Franchise L

Time period: 0 1 2 3

Cash flow: -100 10 60 80

Cumulative cash flow: -100 -90 -30 50

Payback: 2.375

Discounted Payback Period

Disc. cum. cash flow: -100 -36 520

The profitability index is the present value of all future cash flows divided by the intial cost. It measures the PV per dollar of

investment.

(3.) What is the difference between the regular and discounted payback periods?

The payback period is defined as the expected number of years required to recover the investment, and it was the first formal

method used to evaluate capital budgeting projects. First, we identify the year in which the cumulative cash inflows exceed the

initial cash outflows. That is the payback year. Then we take the previous year and add to it the fraction calculated as the

unrecovered balance at the end of that year divided by the following year’s cash flow. Generally speaking, the shorter the

payback period, the better the investment.

(2.) What is the rationale for the payback method? According to the payback criterion, which franchise or franchises should

be accepted if the firm’s maximum acceptable payback is 2 years, and if Franchise L and S are independent? If they are

mutually exclusive? Answer: See Chapter 12 Mini Case Show

Intermediate calculation to

257

260

261

262

265

266

267

i. (1.) What is the payback period? Find the paybacks for Franchises L and S.