ANSWERS TO END-OF-CHAPTER QUESTIONS

10-1 a. Capital budgeting is the whole process of analyzing projects and deciding whether they

should be included in the capital budget. This process is of fundamental importance to

the success or failure of the firm as the fixed asset investment decisions chart the course

of a company for many years into the future. The payback, or payback period, is the

number of years it takes a firm to recover its project investment. Payback may be

money. NPV is the present value of the project’s expected future cash flows (both

inflows and outflows), discounted at the appropriate cost of capital. NPV is a direct

measure of the value of the project to shareholders. The internal rate of return (IRR) is

the discount rate that equates the present value of the expected future cash inflows and

outflows. IRR measures the rate of return on a project, but it assumes that all cash

Chapter 10

The Basics of Capital Budgeting: Evaluating Cash

Flows

Answers and Solutions: 10 – 2

that at that point their NPVs are equal.

f. Capital projects with nonnormal cash flows have a large cash outflow either sometime

during or at the end of their lives. A common problem encountered when evaluating

projects with nonnormal cash flows is multiple IRRs. A project has normal cash flows

if one or more cash outflows (costs) are followed by a series of cash inflows.

their engineering lives and therefore it may be best to terminate a project prior to its

potential life. The economic life is the number of years a project should be operated to

maximize its NPV, and is often less than the maximum potential life. Capital rationing

occurs when a firm’s management limits its capital expenditures to an amount less than

would be required to fund the optimal capital budget. The equivalent annual annuity

10-2 Projects requiring greater investments or that have greater risk should be given detailed

analysis the capital budgeting process.

10-3 The NPV is obtained by discounting future cash flows, and the discounting process actually

10-4 This question is related to Question 10-3 and the same rationale applies. With regard to

the second part of the question, the answer is no; the IRR rankings are constant and

independent of the firm’s cost of capital.

10-5 Generally, the failure to employ common-life analysis in such situations will bias the NPV

against the shorter project because it “gets no credit” for profits beyond its initial life, even

though it could possibly be “renewed” and thus provide additional NPV.

Answers and Solutions: 10 – 4

SOLUTIONS TO END-OF-CHAPTER PROBLEMS

10-1 NPV = -$40,000 + $9,000[(1/I) – (1/(I × (1 + I)N)]

solve for NPV = $2,409.77.

10-2 Financial calculator solution: Input CF0 = -40000, CF1-7 = 9000, and then solve for IRR =

12.84%.

10-3 MIRR: PV Costs = $40000.

FV Inflows:

Answers and Solutions: 10 – 5

10-4 PV = $9,000[(1/I) – (1/(I × (1 + I)N)]

= $9,000[(1/0.11) – (1/(0.11 × (1 + 0.11)7)]

= $42,410.

10-5 Since the cash flows are a constant $9,000, calculate the payback period as:

$40,000/$9,000 = 4.44, so the payback is about 4 years.

10-6 The project’s discounted payback period is calculated as follows:

Year

Annual CF

Discounted CF

(@11%)

Cumulative

Discounted CF

0

-40,000

-40,000.00

1

2

3

4

5

6

Answers and Solutions: 10 – 6

10-7 a. Project A: Using a financial calculator, enter the following:

CF0 = -15000000

CF1 = 5000000

CF2 = 10000000

CF3 = 20000000

b. Using the data for Project A, enter the cash flows into a financial calculator and solve

for IRRA = 43.97%. The IRR is independent of the WACC, so IRR doesn’t change

when the WACC changes.

10-8 Truck:

NPV = -$17,100 + $5,100(PVIFA14%,5)

= -$17,100 + $5,100(3.4331) = -$17,100 + $17,509

= $409. (Accept)

Answers and Solutions: 10 – 7

MIRR: PV Costs = $17,100.

Pulley:

NPV = -$22,430 + $7,500(3.4331) = -$22,430 + $25,748

= $3,318. (Accept)

Financial calculator: Input the appropriate cash flows into the cash flow register, input

I/YR = 14, and then solve for NPV = $3,318.

Answers and Solutions: 10 – 8

FV Inflows:

PV FV

0 1 2 3 4 5

| | | | | |

7,500 7,500 7,500 7,500 7,500

8,550

10-9 Electric-powered:

NPVE = -$22,000 + $6,290[(1/i) – (1/(i × (1 + i)n)]

= -$22,000 + $6,290[(1/0.12) – (1/(0.12 × (1 + 0.12)6)]

= -$22,000 + $6,290(4.1114) = -$22,000 + $25,861 = $3,861.

Financial calculator: Input the appropriate cash flows into the cash flow register, input

I/YR = 12, and then solve for NPV = $3,861.

14%

10-10 Financial calculator solution, NPV:

Project S

Inputs 5 12 3000 0

Inputs 5 12 7400 0

Output = -26,675.34

NPVL = $26,675.34 – $25,000 = $1,675.34.

Financial calculator solution, IRR:

Input CF0 = -10000, CF1 = 3000, Nj = 5, IRRS = ? IRRS = 15.24%.

Input CF0 = -25000, CF1 = 7400, Nj = 5, IRRL = ? IRRL = 14.67%.

N

I/YR

FV

PMT

PV

N

I/YR

FV

PMT

PV

Answers and Solutions: 10 – 10

Project L

Inputs 5 12 0 7400

Output = -47,011.07

PV costsL = $25,000.

FV inflowsL = $47,011.07.

N

I/YR

FV

PMT

PV

N

I/YR

FV

PMT

PV

Answers and Solutions: 10 – 11

10-11 Because both projects are the same size you can just calculate each project’s MIRR and

choose the project with the higher MIRR. (Remember, MIRR gives conflicting results

from NPV when there are scale differences between the projects.)

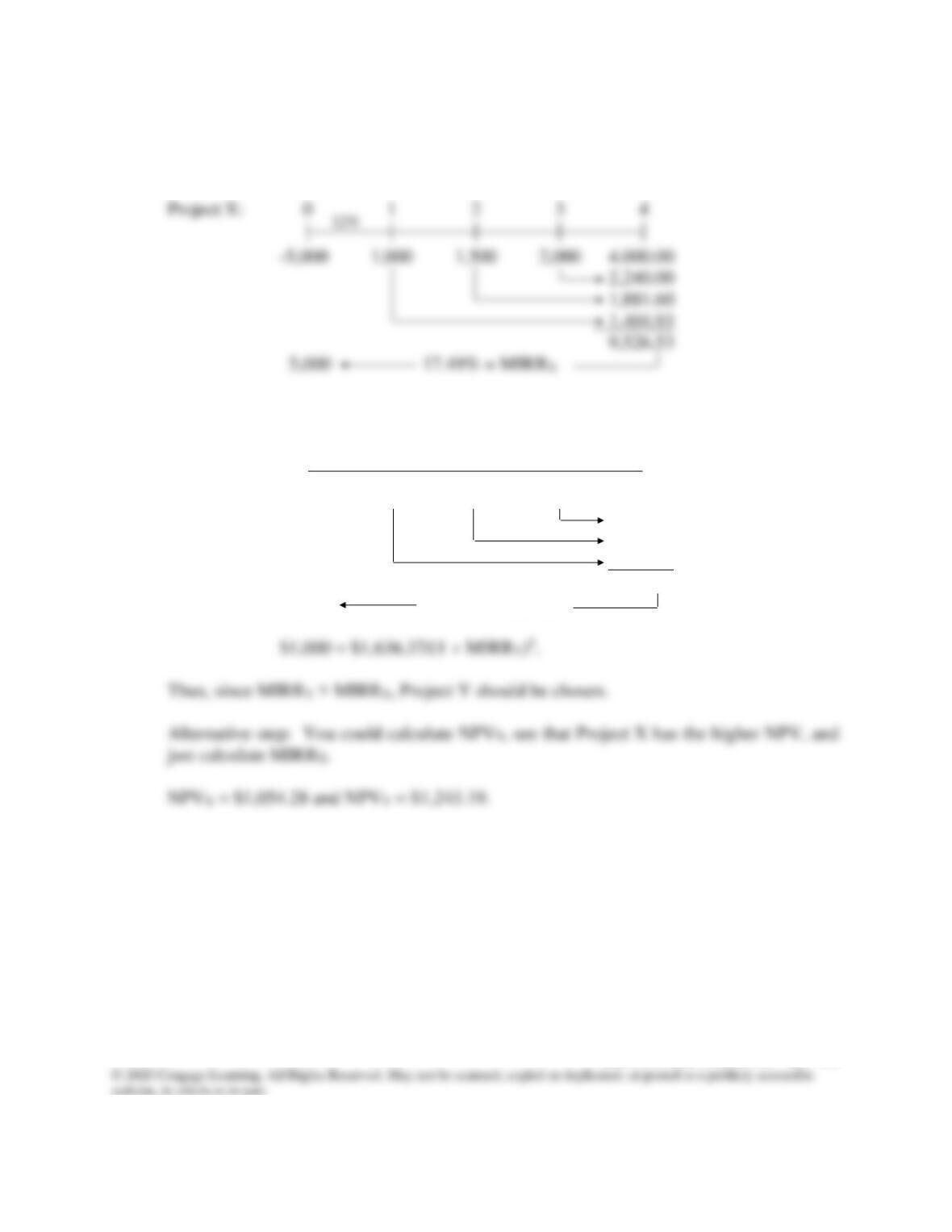

12%

$5,000 = $9,529/(1 + MIRRX)4.

Project Y: 0 1 2 3 4

| | | | |

-5,000 4,500 1,500 1,000 500.00

1,120.00

1,881.60

6,322.18

9,823.78

5,000 18.39% = MIRRY

12%

Answers and Solutions: 10 – 12

10-12 a. Purchase price $ 900,000

Installation 165,000

Initial outlay $1,065,000

CF0 = -1065000; CF1-5 = 350000; I/YR = 14; NPV = ?

NPV = $136,578; IRR = 19.22%.

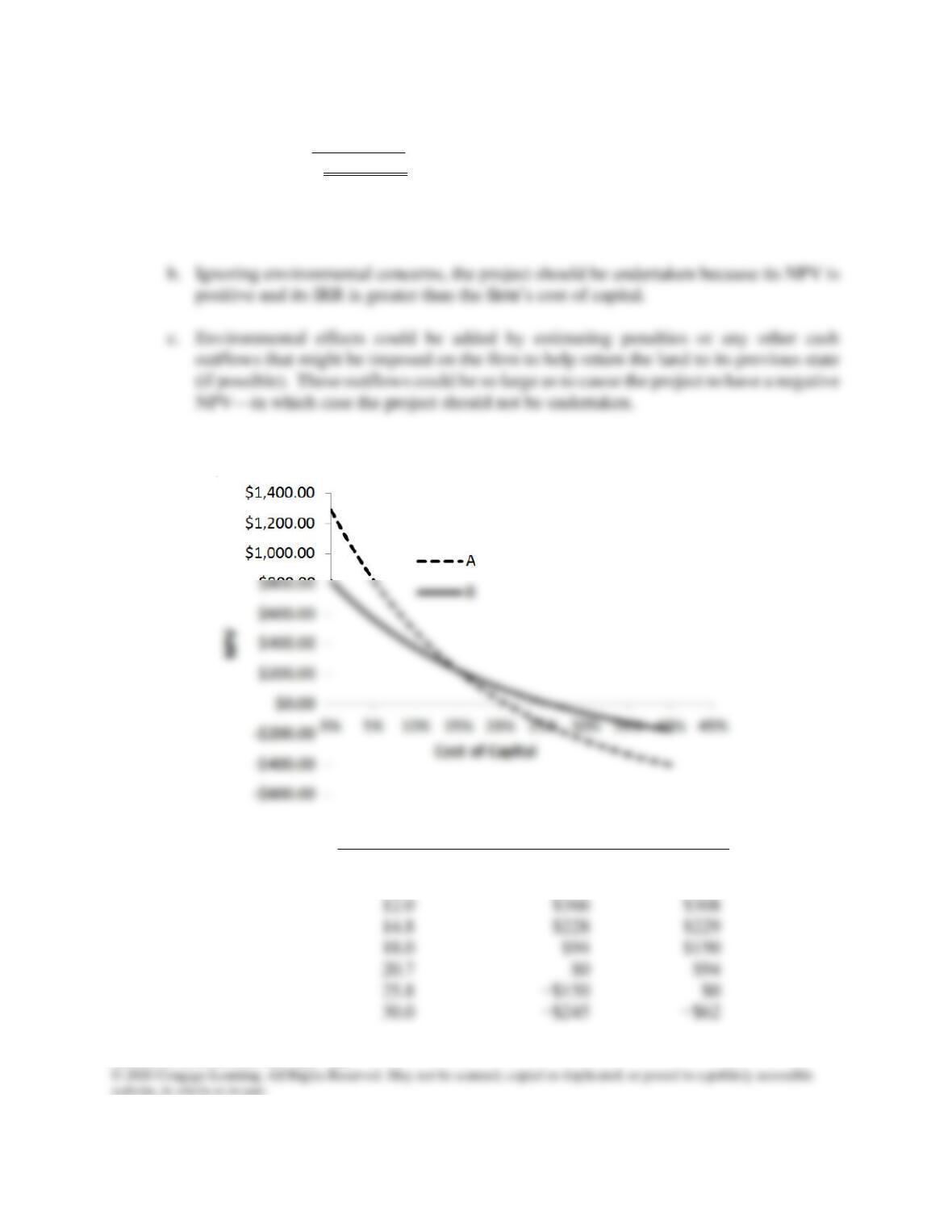

10-13 a.

r

NPVA

NPVB

0.0%

$1,288

$820

10.0

$479

$372

14.8

$228

$229

18.0

$150

20.7

25.8

30.0

Answers and Solutions: 10 – 13

b. IRRA = 20.7%; IRRB = 25.8%.

c. At r = 10%, Project A has the greater NPV, specifically $478.83 as compared to Project

B’s NPV of $372.37. Thus, Project A would be selected. At r = 17%, Project B has

an NPV of $173.70 which is higher than Project A’s NPV of $133.76. Thus, choose

Project B if r = 17%.

Here is the MIRR for Project B when r = 10%:

PV costs = 600.

TV of inflows: Financial calculator settings are N = 7, I/YR = 10, PV = 0, PMT = 210,

and solve for FV = -1992.3059.

Answers and Solutions: 10 – 14

e. To find the crossover rate, construct a Project ∆ which is the difference in the two

projects’ cash flows:

Year

Project ∆ = CFA – CFB

0

$250

1

−738

2

−429

3

−360

4

890

5

610

6

780

7

−535

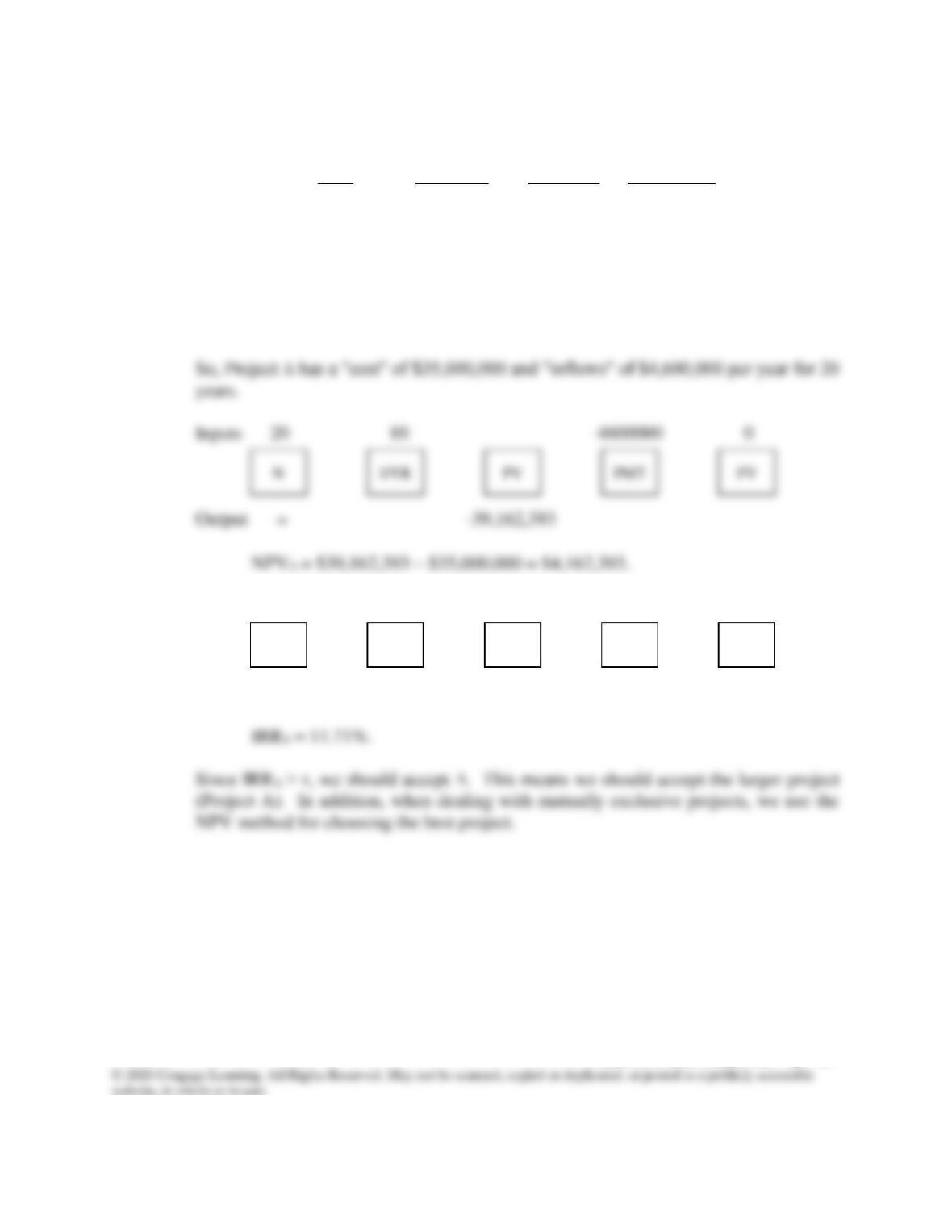

10-14 a. Incremental Cash

Year Plan B Plan A Flow (B – A)

0 ($10,000,000) ($10,000,000) $ 0

1 1,750,000 12,000,000 (10,250,000)

2-20 1,750,0000 0 1,750,000

Answers and Solutions: 10 – 15

b. If the firm could invest the incremental $10,250,000 at a return of 16.07%, it would

receive cash flows of $1,750,000. If we set up an amortization schedule, we would

find that payments of $1,750,000 per year for 19 years would amortize a loan of

$10,250,000 at 16.0665%.

d. See graph. If the cost of capital is less than 16.07%, then Plan B should be accepted;

if r > 16.07%, then Plan A is preferred.

N P V ( M i l l i o n s o f D o l l a r s )

B

25

20

15

Answers and Solutions: 10 – 16

10-15 a. Financial calculator solution:

Plan A

Inputs 20 10 8000000 0

Output = -68,108,510

NPVA = $68,108,510 – $50,000,000 = $18,108,510.

Plan A

Inputs 20 -50000000 8000000 0

Output = 15.03

IRRA = 15.03%.

N

I/YR

FV

PMT

PV

N

I/YR

FV

PMT

PV

N

I/YR

FV

PMT

PV

Answers and Solutions: 10 – 17

b. If the company takes Plan A rather than B, its cash flows will be (in millions of dollars):

Cash Flows Cash Flows Project ∆

Year from A from B Cash Flows

0 ($50) ($15.0) ($35.0)

1 8 3.4 4.6

2 8 3.4 4.6

– – – –

– – – –

– – – –

20 8 3.4 4.6

Inputs 20 -35000000 4600000 0

Output = 11.71

N

I/YR

FV

PMT

PV

Answers and Solutions: 10 – 18

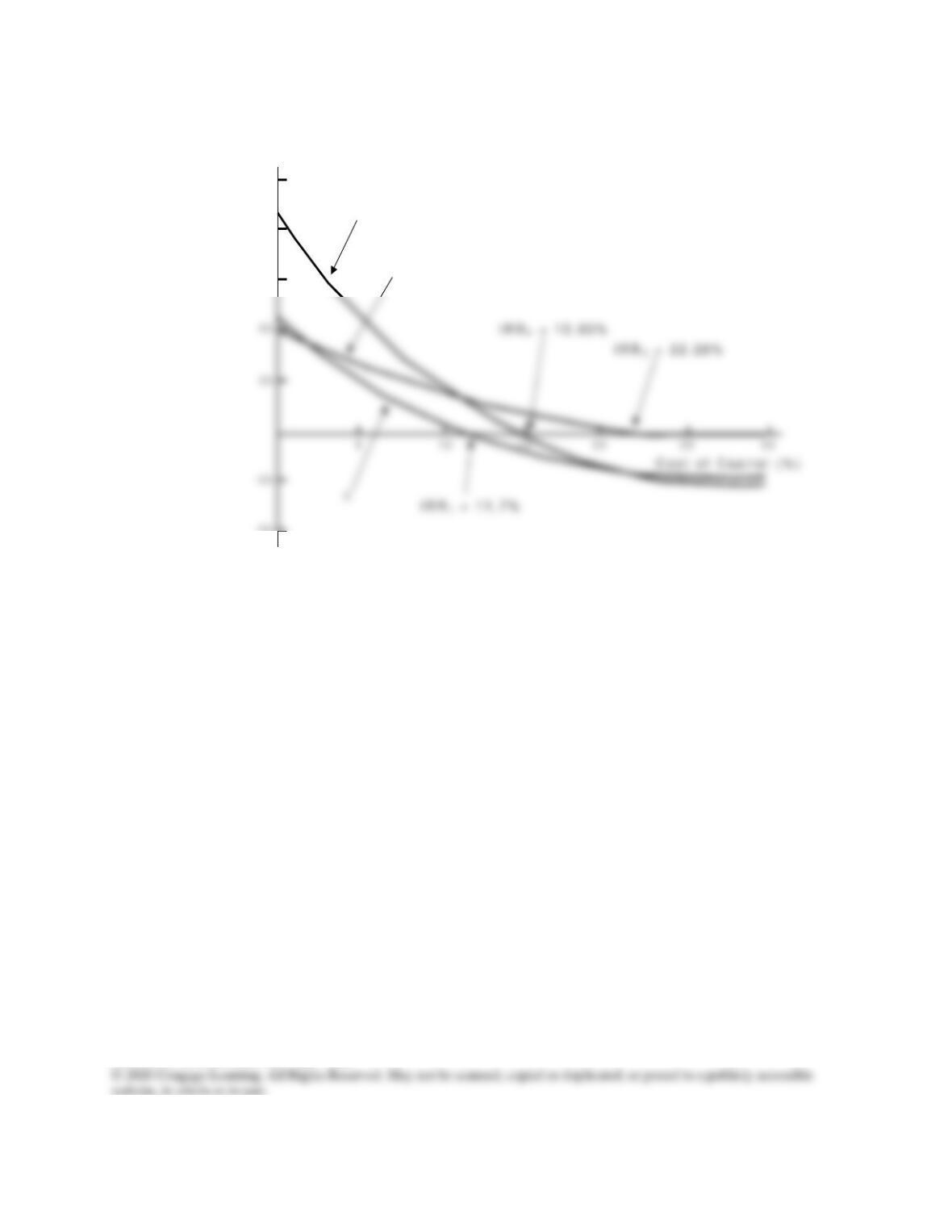

c.

N P V ( M i l l i o n s o f D o l l a r s )

C r o s s o v e r R a t e = 1 1 . 7 %

A

B

1 2 5

1 0 0

75

– 5 0

Answers and Solutions: 10 – 19

10-16 Plane A: Expected life = 5 years; Cost = $100 million; NCF = $30 million;

COC = 12%.

12%

Enter these values into the cash flow register: CF0 = -100; CF1-4 = 30; CF5 = -70; CF6-

10 = 30. Then enter I/YR = 12, and press the NPV key to get NPVA = $12.764 million.

0 1 2 3 4 5 6 7 8 9 10

B: | | | | | | | | | | |

-132 25 25 25 25 25 25 25 25 25 25

Enter these cash flows into the cash flow register, along with the interest rate, and press

the NPV key to get NPVB = $9.256 million.

Project A is the better project and will increase the company’s value by $12.764

million.

12%

10-17 0 1 2 3 4 5 6 7 8

A: | | | | | | | | |

-10 4 4 4 4 4 4 4 4

-10

-6

Machine A’s simple NPV is calculated as follows: Enter CF0 = -10 and CF1-4 = 4. Then

enter I/YR = 10, and press the NPV key to get NPVA = $2.679 million. However, this

10%

-15 3.5 3.5 3.5 3.5 3.5 3.5 3.5 3.5

For Machine B’s NPV, enter these cash flows into the cash flow register, along with

the interest rate, and press the NPV key to get NPVB = $3.672 ≈ $3.67 million.

Machine A is the better project and will increase the company’s value by $4.51 million.

10%