Chapter 10 CFIN6

Chapter 10 Solutions

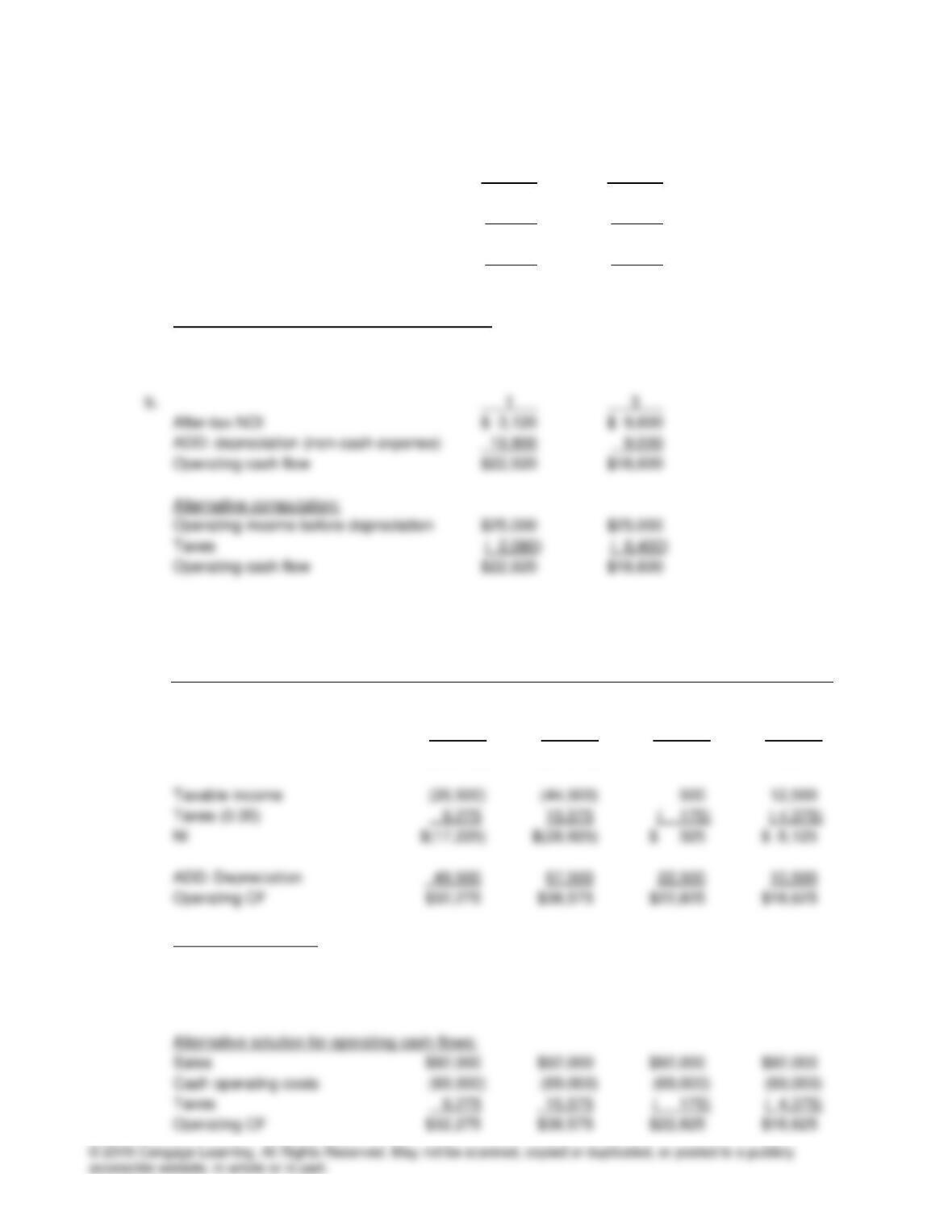

10-1 a. 1 3

Operating income before depreciation $25,000 $25,000

Depreciation* (19,800) ( 9,000)

NOI 5,200 16,000

Taxes (0.40) ( 2,080) ( 6,400)

After-tax NOI $ 3,120 $ 9,600

*Depreciation, based on MACRS 3-year class:

Depreciation in Year 1 = $60,000(0.33) = $19,800

Depreciation in Year 3 = $60,000(0.15) = $ 9,000

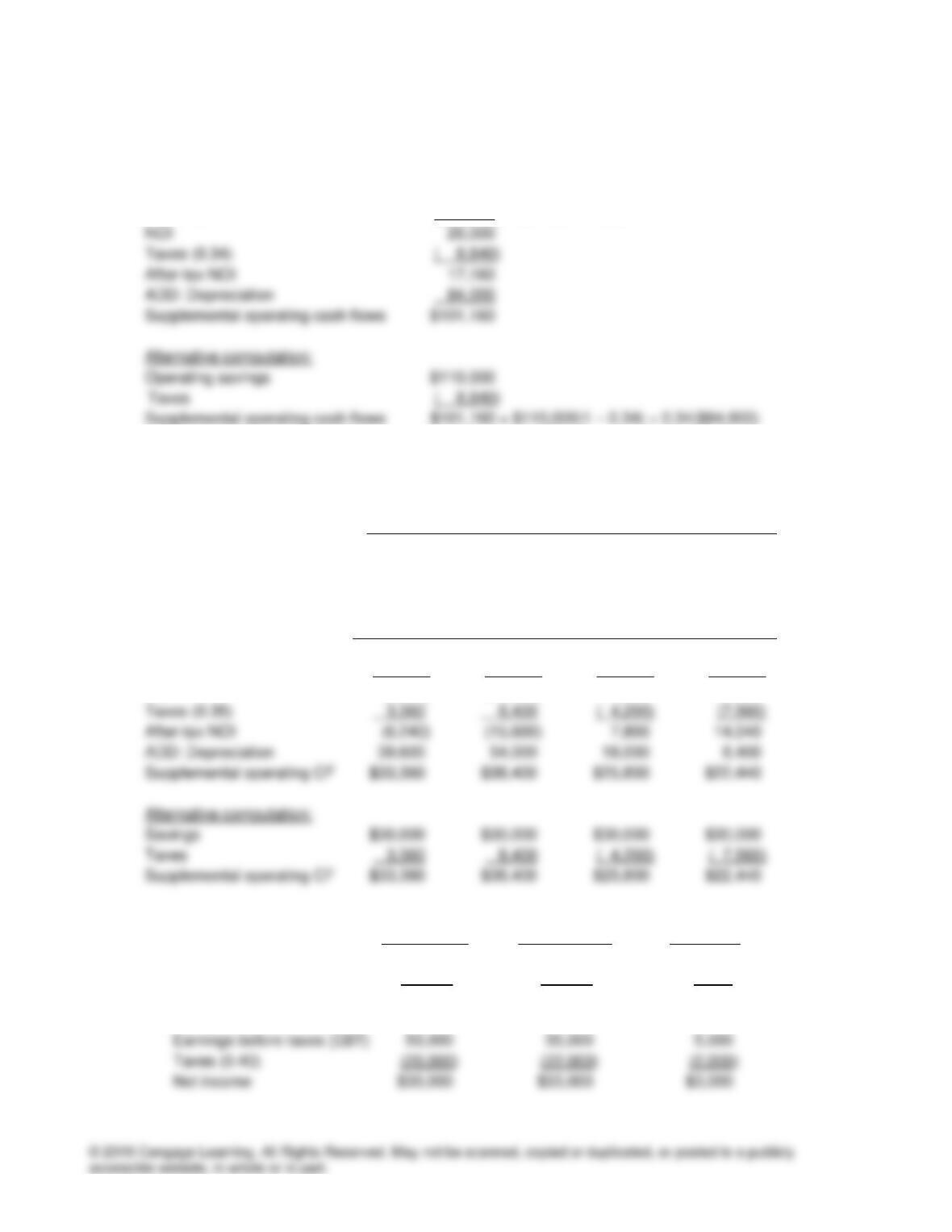

10-2 a & b

1 2 3 4

Sales $92,000 $92,000 $92,000 $92,000

Operating costs (0,75 x Sales) (69,000) (69,000) (69,000) (69,000)

Depreciation (49,500) (67,500) (22,500) (10,500)

NOI (26,500) (44,500) 500 12,500

Annual Depreciation:

Depreciable basis $150,000

Depreciation rates 0.33 0.45 0.15 0.07

Depreciation amount $49,500 $67,500 $22,500 $10,500

Chapter 10 CFIN6

10-3 Purchase price $(350,000)

Shipping cost ( 20,000)

Installation cost ( 50,000)

Depreciable basis $420,000

Year Depreciation: MACRS 3-year class

10-4 Purchase price $(500,000)

Shipping & installation costs ( 75,000)

Depreciable basis $575,000

Year Depreciation: MACRS 3-year class

1 $115,000 = $575,000 x 0.20

10-5 a. Purchase price $(214,000)

Installation ( 26,000)

Depreciable basis $(240,000)

Year Depreciation: MACRS 3-year class

1 $48,000 = $240,000 x 0.20

b. Selling price at the end of four years = $80,000

Book value at the end of four years = $240,000 – $48,000 – $76,800 – $45,600 – $28,800

= $40,800

Alternative computation of BV: Because 83 percent of the depreciable basis has been depreciated, 17

percent remains (0.17 = 1.00 – 0.20 – 0.32 – 0.19 – 0.12). Thus, the depreciable basis is $40,800 =

$240,000(0.17).

Chapter 10 CFIN6

10-6 Because the depreciation expense is the same each year, the supplemental operating cash flow will be the

same for every year.

Operating savings $110,000

Depreciation ( 84,000) = ($840,000 – $0)/10

10-7 Depreciable basis = $120,000

1 2 3 4

Percent depreciated 0.33 0.45 0.15 0.07

Depreciation $39,600 $54,000 $18,000 $8,400

1 2 3 4

Savings $30,000 $30,000 $30,000 $30,000

Depreciation (39,600) (54,000) (18,000) ( 8,400)

NOI (9,600) (24,000) 12,000 21,600

10-8 a. Old Machine New Machine Difference

NOI, excluding depreciation $90,000 $90,000 $ 0

Depreciation (40,000) (35,000) 5,000

NOI 50,000 55,000 5,000

Chapter 10 CFIN6

b. Old Machine New Machine Difference

Net income $30,000 $33,000 $3,000

Depreciation 40,000 35,000 (5,000)

Supplemental operating CF $70,000 $68,000 $(2,000)

10-9 Selling price = $102,000

Book value = $90,000

10–10 Selling price = $4,000

Book value = $6,000

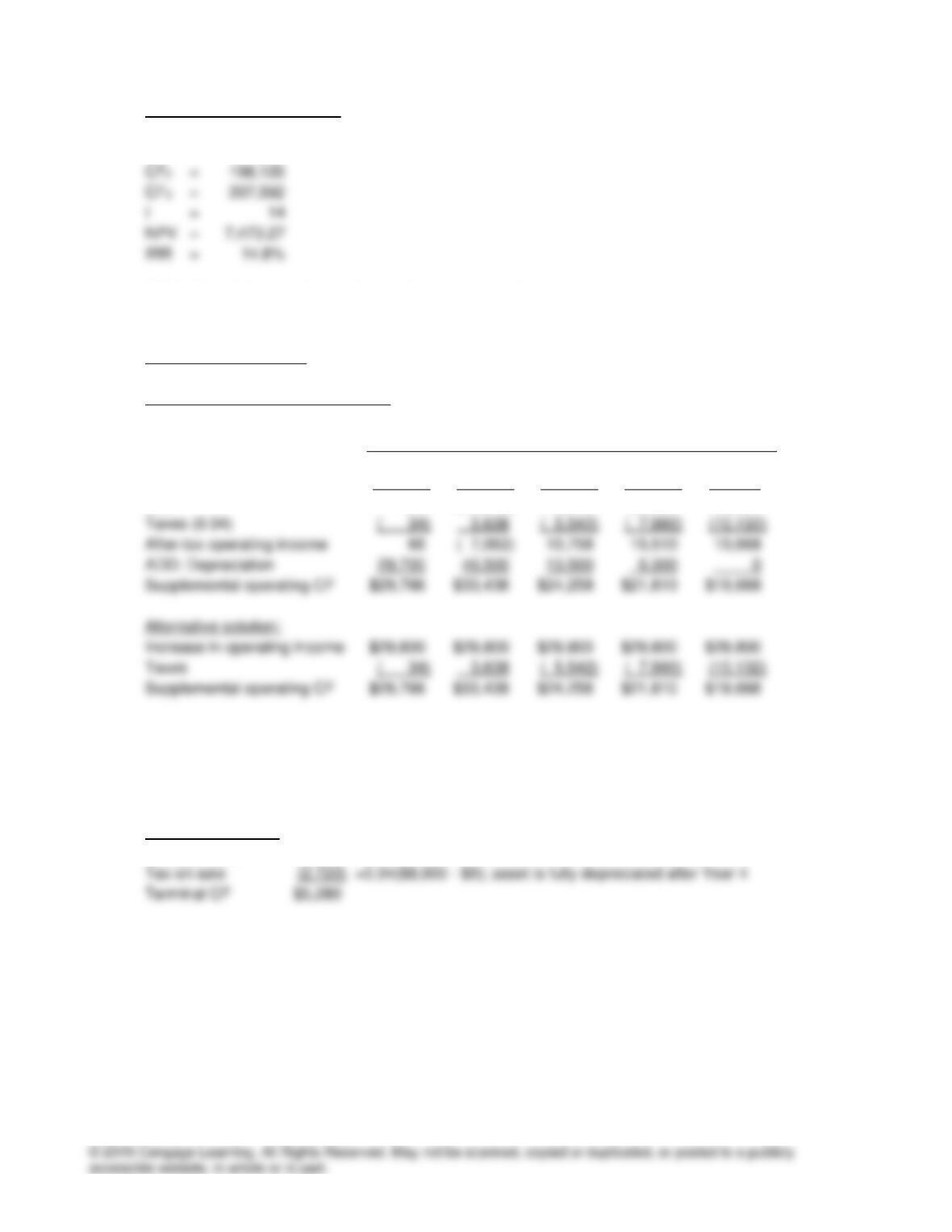

10–11 Initial investment outlay:

Purchase price $(432,000)

Installation ( 52,000)

Increase in net working capital ( 22,000)

Initial investment outlay $(506,000)

Chapter 10 CFIN6

Supplemental operating cash flows:

1 2 3

Savings $185,000 $185,000 $185,000

Depreciation (159,720) (217,800) ( 72,600)

NOI 25,280 ( 32,800) 112,400

Depreciation % 0.33 0.45 0.15

Depreciation = $484,000 x Deprec % $159,720 $217,800 $72,600

Alternative solution:

1 2 3

Savings $185,000 $185,000 $185,000

Taxes (0.40) ( 10,112) 13,120 ( 44,960)

Supplemental operating CF $174,888 $198,120 140,040

Terminal cash flow:

Selling price = $220,000

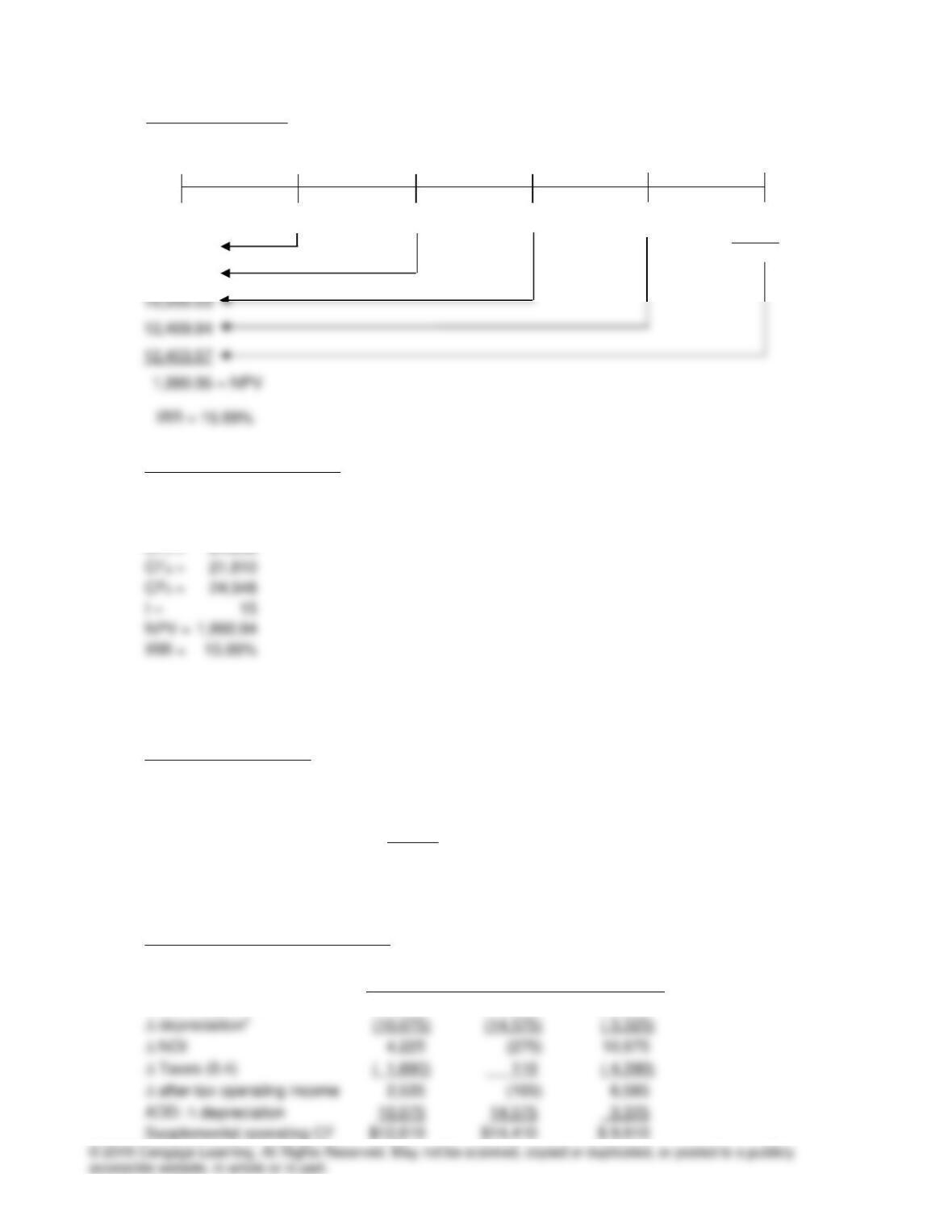

Cash flow timeline:

0 1 2 3

(506,000.00) 174,888 198,120 140,040

167,552

r = 14%

153,410.53

Chapter 10 CFIN6

Financial calculator solution:

CF0 = –506,000

CF1 = 174,888

NPV > 0, which means the setter should be purchased.

10–12 Initial investment outlay = Purchase price = $90,000

Supplemental operating cash flows:

1 2 3 4 5

Increase in operating income $29,800 $29,800 $29,800 $29,800 $29,800

Depreciation (29,700) (40,500) (13,500) ( 6,300) 0

NOI 100 (10,700) 16,300 23,500 29,800

Depreciable basis $90,000

Depreciation rates 0.33 0.45 0.15 0.07 0.00

Depreciation $29,700 $40,500 $13,500 $6,300 $0

Terminal cash flow:

Salvage value $8,000

Chapter 10 CFIN6

Financial calculator solution:

CF0 = -90,000

CF1 = 29,766

CF2 = 33,438

NPV > 0, which means the machine should be purchased.

10–13 Initial investment outlay:

Purchase price of new machine $(37,500)

Salvage of old machine 5,000

Tax on sale of old machine* 1,320

Initial investment outlay $(31,180)

*tax on sale of old machine = 0.4($5,000 – $8,300) = -$1.320, which represents a tax refund

Supplemental operating cash flows:

1 2 3

operating income $14,300 $14,300 $14,300

Cash Flow Timeline:

0 1 2 3 4 5

(90,000.00) 29,766 33,438 24,258 21,810 19,668

5,280

24,948

r = 15%

25,883.48

25,283.93

Chapter 10 CFIN6

Alternative solution:

Increase in operating income $14,300 $14,300 $14,300

Taxes ( 1,690) 110 ( 4,390)

Supplemental operating CF $12,610 $14,410 $ 9,910

Terminal cash flow:

Salvage value of new machine $6,000

Tax on sale of new machine (1,350) = 0.4($6,000 – $2,625)

Loss of sale of old machine (2,000)

Taxes on sale of old machine that are not paid 240 = 0.4($2,000 – $1,400)

Terminal cash flow $2,890

Cash Flow Timeline:

0 1 2 3

(31,180.00) 12,610 14,410 9,910

2,890

12,800

r = 11%

11,360.36

Chapter 10 CFIN6

Financial calculator solution:

CF0 = -31,180

CF1 = 12,610

CF2 = 14,410

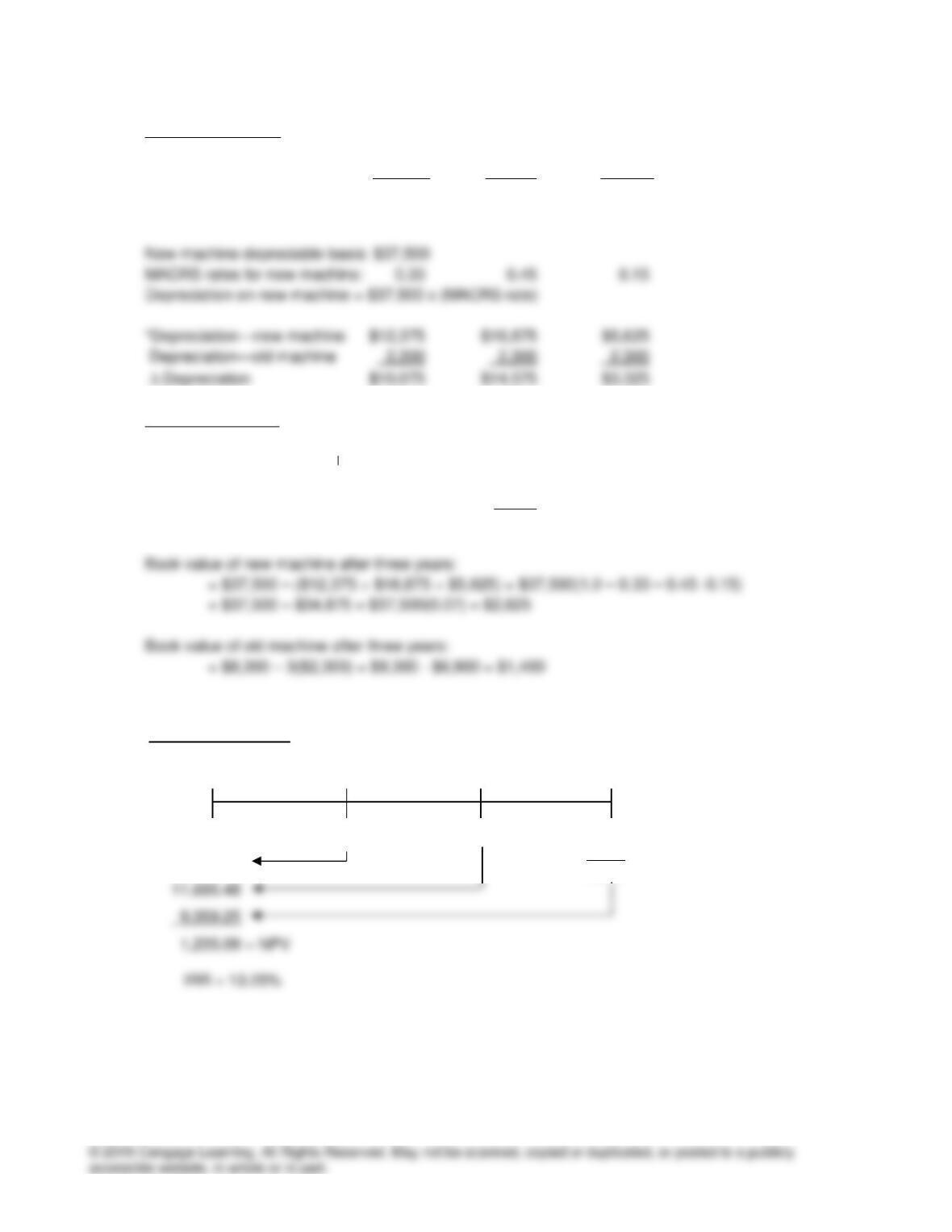

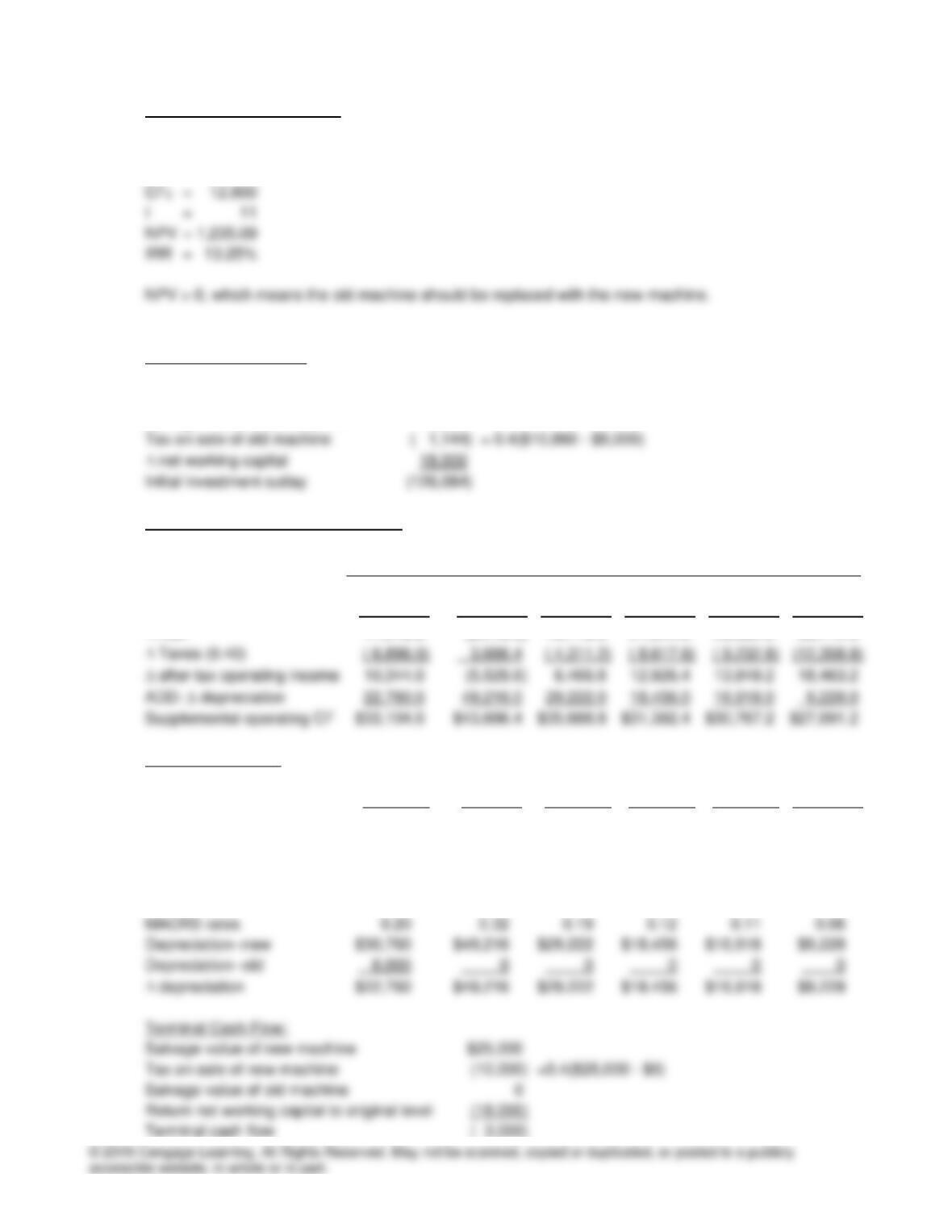

10–14 Initial investment outlay:

Purchase price $(153,800)

Salvage value of old machine 10,860

Supplemental Operating Cash Flows:

1 2 3 4 5 6

operating income $40,000.0 $40,000.0 $40,000.0 $40,000.0 $40,000.0 $40,000.0

depreciation (22,760.0) (49,216.0) (29,222.0) (18,456.0) (16,918.0) ( 9,228.0)

Alternative solution:

Increase in operating income 40,000.0 40,000.0 40,000.0 40,000.0 40,000.0 40,000.0

Taxes ( 6,896.0) 3,686.4 ( 4,311.2) ( 8,617.6) ( 9,232.8) (12,308.8)

Supplemental operating CF 33,104.0 43,686.4 35,688.8 31,382.4 30,767.2 27,691.2

Depreciable basis—new machine: $153,800

Chapter 10 CFIN6

Financial calculator solution:

CF0 = -126,084.0

CF1 = 33,104.0

CF2 = 43,686.4

CF3 = 35,688.8

NPV > 0, which means the old machine should be replaced with the new machine

10–15 r = 4% + (11% – 4%)(0.8) = 9.6%

17

(1.096)

1

NPV $6,250 $29,500

−

=−

IRR = 10.95%

Calculator solution: CF0 = –29,500, CF1 – CF7 = 6,250, I = 9.6; compute NPV = 1,332.53; IRR = 10.95%

Cash Flow Timeline:

IRR = 15.97%

0 1 2 3 4 5 6

(126,084.00) 33,104.0 43,686.4 35,688.8 31,382.4 30,767.2 27,691.2

( 3,000.0)

24,691.2

r = 12%

29,557.14

34,826.53

13,613.80 = NPV

Chapter 10 CFIN6

Alternative calculator solution using TVM keys: N = 7, PV = -29,500, PMT = 6,250, FV = 0; compute I/Y

= 10.95% = IRR

The new division should be added, because NPV > 0.

IRR = 10.75%

Calculator solution: CF0 = -405,000, CF1 – CF3 = 165,000, I = 10.8; compute NPV = -380.36; IRR =

10.75%

10–17 NPV Probability NPV x Probability

$31,500 0.20 $6,300

19,800 0.70 13,860

-20,100 0.10 -2,010

E(NPV) = $18,150

CV = 0.75 < 0.80, so the project should be purchased.

10–18 NPV Probability NPV x Probability

$185,400 0.25 $46,350

128,300 0.60 76,980

-77,600 0.15 -11,640

E(NPV) = $111,690

Chapter 10 CFIN6

2 = 0.25($185,400 – $111,690)2 + 0.60($128,300 – $111,690)2 +0.15(-$77,600 – $111,690)2

The project should not be purchased, because CV > 0.70.

10–19 Project IRR Risk Risk-Adjusted r Acceptable?

P 10.0% Low 9% = 11% – 2% Yes, IRR > r (risk-adjusted)

10–20 Project IRR Risk Risk-Adjusted r Acceptable?