Answers and Solutions: 10 – 21

10-18 Cash flow time line for Machine 190-3:

0 1 2 3

| | | |

-190,000 87,000 87,000 87,000

Using a financial calculator, input the following data: CF0 = -190000; CF1-3 = 87000;

I/YR = 14; and solve for NPV190-3 = $11,982 (for 3 years).

Using a financial calculator, input the following data: CF0 = -360000; CF1-6 = 98300;

I/YR = 14; and solve for NPV360-6 = $22,256 (for 6 years).

EAA360-6: Using a financial calculator, input the following data:

N = 6; I/YR = 14; PV = -22256; and FV = 0. Solve for PMT = EAA =

$5,723.

14%

Answers and Solutions: 10 – 22

10-19 a. The project’s expected cash flows are as follows (in millions of dollars):

Time Net Cash Flow

0 ($ 4.4)

1 27.7

2 (25.0)

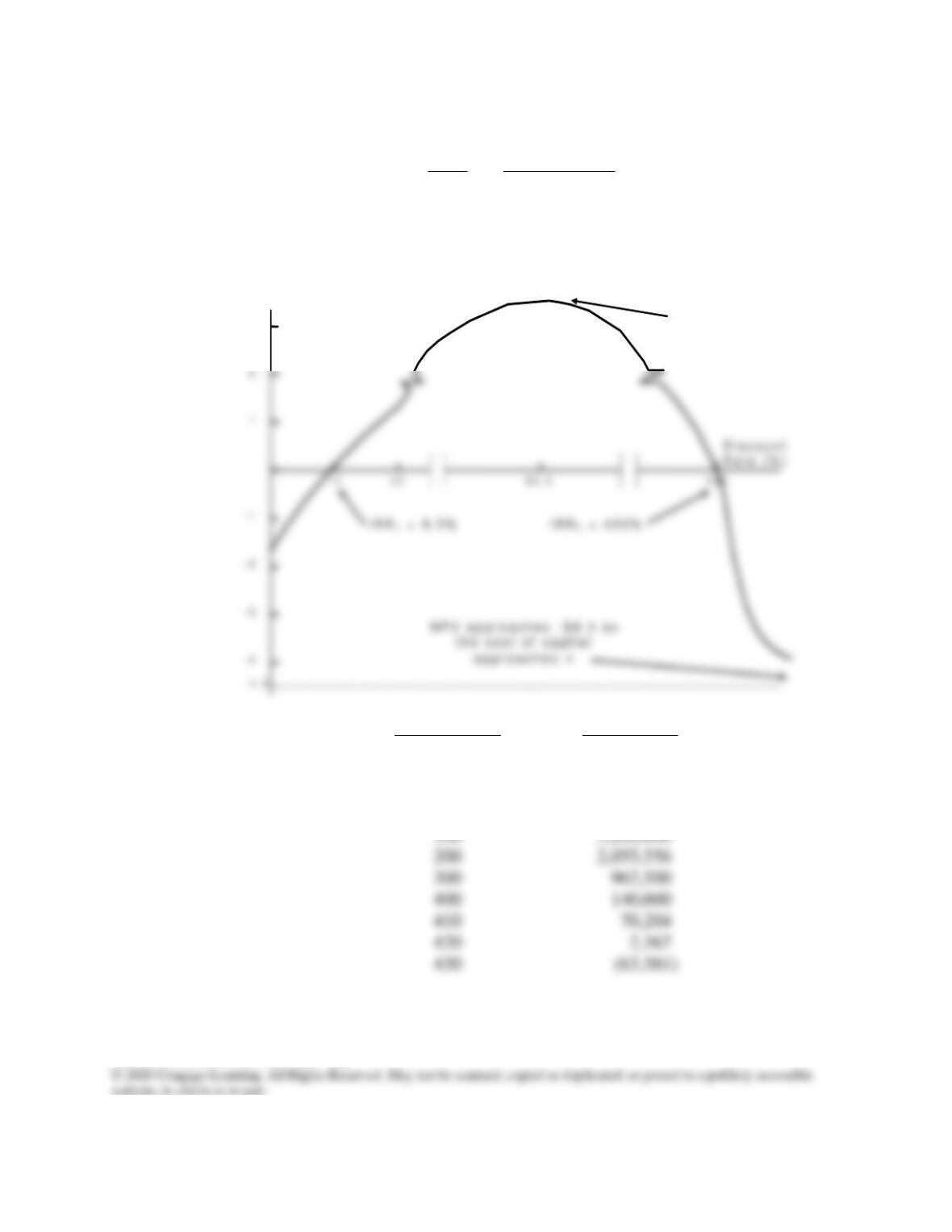

We can construct the following NPV profile:

Discount Rate NPV

0% ($1,700,000)

9 (29,156)

10 120,661

50 2,955,556

N P V ( M i l l i o n s o f D o l l a r s )

M a x i m u m

N P V a t 8 0 . 5 %

3

Answers and Solutions: 10 – 23

The table above was constructed using a financial calculator with the following inputs:

CF0 = -4400000, CF1 = 27700000, CF2 = –25000000, and I/YR = discount rate to solve

for the NPV.

d. Here is the MIRR for the project when r = 8%:

PV costs = $4,400,000 + $25,000,000/(1.08)2 = $25,833,470.51.

TV inflows = $27,700,000(1.08)1 = $29,916,000.00.

Now, MIRR is the discount rate that forces the PV of the TV of $29,916,000 over 2

years to equal $25,833,470.51:

MIRR = 7.61%.

At r = 14%, MIRR for the project is calculated as follows:

Answers and Solutions: 10 – 24

Now, MIRR is that discount rate which forces the PV of the TV of $31,578,000 over 2

years to equal $23,636,688.21:

10-20 a. The IRRs of the two alternatives are undefined. To calculate an IRR, the cash flow

stream must include both cash inflows and outflows.

b. The PV of costs for the conveyor system is ($911,067), while the PV of costs for the

forklift system is ($838,834). Thus, the forklift system is expected to be ($838,834) –

($911,067) = $72,233 less costly than the conveyor system, and hence the forklift

trucks should be used.

10-21 a. Payback A (cash flows in thousands):

Annual

Period Cash Flows Cumulative

0 ($25,000) ($25,000)

1 5,000 (20,000)

Answers and Solutions: 10 – 25

2 10,000 5,000

3 8,000 13,000

4 6,000 19,000

PaybackB = 1 + $5,000/$10,000 = 1.50 years.

b. Discounted Payback A (cash flows in thousands):

Period Cash Flows Cash Flows Cumulative

0 ($25,000) ($25,000.00) ($25,000.00)

1 20,000 18,181.82 (6,818.18)

2 10,000 8,264.46 1,446.28

3 8,000 6,010.52 7,456.80

4 6,000 4,098.08 11,554.88

Discounted PaybackB = 1 + $6,818.18/$8,264.46 = 1.825 years.

Answers and Solutions: 10 – 26

e. At a discount rate of 15%, NPVA = $8,207,071.

At a discount rate of 15%, NPVB = $8,643,390.

At a discount rate of 15%, Project B has the higher NPV; consequently, it should be

accepted.

f. Project ∆ =

cash flow registers being sure to enter 0 for CF0, then enter I/YR = 10, and

solve for NPV = $37,739,908.

Step 2: Calculate the FV of the cash inflow stream as follows:

Enter N = 4, I/YR = 10, PV = -37739908, and PMT = 0 to solve for FV =

$55,255,000.

Step 3: Calculate MIRRA as follows:

Enter N = 4, PV = -25000000, PMT = 0, and FV = 55255000 to solve for

I/YR = 21.93%.

Answers and Solutions: 10 – 27

Enter N = 4, I/YR = 10, PV = -36554880, and PMT = 0 to solve for FV =

$53,520,000.

Step 3: Calculate MIRRB as follows:

Enter N = 4, PV = -25000000, PMT = 0, and FV = 53520000 to solve for

I/YR = 20.96%.

10-22 a. NPV of termination after Year t:

NPV0 = -$22,500 + $22,500 = 0.

Using a financial calculator, input the following: CF0 = -22500, CF1 = 23750, and I/YR

= 10 to solve for NPV1 = –$909.09 ≈ -$909.

Using a financial calculator, input the following: CF0 = -22500, CF1 = 6250, CF2 =

20250, and I/YR = 10 to solve for NPV2 = –$82.64 ≈ -$83.

The firm should operate the truck for 3 years, NPV3 = $1,307.

b. No. Salvage possibilities could only raise NPV and IRR. The value of the firm is

maximized by terminating the project after Year 3.

Answers and Solutions: 10 – 28

SOLUTION TO SPREADSHEET PROBLEM

10-23 The detailed solution for the problem is available in the file Solution for Ch10 P23 Build

a Model.xlsx at the textbook’s Web site.

Mini Case: 12 – 29

MINI CASE

You have just graduated from the MBA program of a large university, and one of your

favorite courses was “Today’s Entrepreneurs.” In fact, you enjoyed it so much you have

decided you want to “be your own boss.” While you were in the master’s program, your

grandfather died and left you $1 million to do with as you please. You are not an inventor

and you do not have a trade skill that you can market; however, you have decided that you

would like to purchase at least one established franchise in the fast-foods area, maybe two (if

profitable). The problem is that you have never been one to stay with any project for too

long, so you figure that your time frame is three years. After three years you will sell off

your investment and go on to something else.

You have narrowed your selection down to two choices; (1) Franchise L, Lisa’s Soups,

Salads, & Stuff and (2) Franchise S, Sam’s Fabulous Fried Chicken. The net cash flows

shown below include the price you would receive for selling the franchise in Year 3 and the

forecast of how each franchise will do over the three–year period. Franchise L’s cash flows

will start off slowly but will increase rather quickly as people become more health conscious,

while Franchise S’s cash flows will start off high but will trail off as other chicken competitors

enter the marketplace and as people become more health conscious and avoid fried foods.

Franchise L serves breakfast and lunch, while Franchise S serves only dinner, so it is possible

for you to invest in both franchises. You see these franchises as perfect complements to one

another: You could attract both the lunch and dinner crowds and the health conscious and

not so health conscious crowds without the franchises directly competing against one

another.

Here are the net cash flows (in thousands of dollars):

Expected Net Cash Flows

Year Franchise L Franchise S

0 ($100) ($100)

1 10 70

2 60 50

3 80 20

Depreciation, salvage values, net working capital requirements, and tax effects are all

included in these cash flows.

You also have made subjective risk assessments of each franchise, and concluded that

both franchises have risk characteristics that require a return of 10%. You must now

determine whether one or both of the franchises should be accepted.

Mini Case: 12 – 30

a. What is capital budgeting?

Answer: Capital budgeting is the process of analyzing additions to fixed assets. Capital

budgeting is important because, more than anything else, fixed asset investment

decisions chart a company’s course for the future. Conceptually, the capital budgeting

b. What is the difference between independent and mutually exclusive projects?

Answer: Projects are independent if the cash flows of one are not affected by the acceptance of

the other. Conversely, two projects are mutually exclusive if acceptance of one impacts

c. 1. Define the term net present value (NPV). What is each franchise’s NPV?

Answer: The net present value (NPV) is simply the sum of the present values of a project’s cash

flows:

Mini Case: 12 – 31

c. 2. What is the rationale behind the NPV method? According to NPV, which

franchise or franchises should be accepted if they are independent? Mutually

exclusive?

Answer: The rationale behind the NPV method is straightforward: if a project has NPV = $0,

then the project generates exactly enough cash flows (1) to recover the cost of the

investment and (2) to enable investors to earn their required rates of return (the

c. 3. Would the NPVs change if the cost of capital changed?

Answer: The NPV of a project is dependent on the cost of capital used. Thus, if the cost of capital

d. 1. Define the term internal rate of return (IRR). What is each franchise’s IRR?

Answer: The internal rate of return (IRR) is the discount rate that forces the NPV of a project to

equal zero:

Mini Case: 12 – 33

d. 2. How is the IRR on a project related to the YTM on a bond? For example, suppose

the initial cost of a project is $100 and it has cash flows of $40 at Years 1, 2, and

3. What is its IRR? Use the Excel RATE function as though the project were a

bond.

Answer: The IRR is the discount rate that forces the PV of a project’s expected future cash flows

to equal the initial cash flow. This is analogous to a bond’s yield because a bond’s yield

d. 3. What is the logic behind the IRR method? According to IRR, which franchises

should be accepted if they are independent? Mutually exclusive?

Answer: IRR measures a project’s profitability in the rate of return sense: If a project’s IRR

equals its cost of capital, then its cash flows are just sufficient to provide investors with

Mini Case: 12 – 34

d. 4. Would the franchises’ IRRs change if the cost of capital changed?

Answer: IRRs are independent of the cost of capital. Therefore, neither IRRS nor IRRL would

e. 1. Draw NPV profiles for Franchises L and S. At what discount rate do the profiles

cross?

Answer: The NPV profiles are plotted in the figure below.