Chapter 6: Managing Cash Flow

105

2018

2019

Accounts payable

300

400

Bank loan

150

250

Accrued liabilities

100

150

Total current liabilities

550

800

Retained earnings

1,850

2,450

Total liabilities and equity

3,400

4,500

A. Using yearend data, calculate the inventory-to-sale conversion period, the sale-to-cash

conversion period, and the purchase-to-payment conversion period for 2018 and 2019.

Note: because inventories, accounts receivable, accounts payable, and accrued liabilities

are not available for 2017, averages of these accounts cannot be calculated for 2018. So

for 2018 versus 2019 comparative purposes, we use yearend data for these accounts.

Inventory-to-Sale Conversion Period = (Yearend Inventories) / (COGS / 365)

2018: 1450 / (2250 / 365) = 1450/6.1644 = 235.22

2019: 2000 / (2700 / 365) = 2000/7.3973 = 270.37

Note: the calculation for 2019 using average receivables would be:

Sale-to-Cash Conversion Period = (Average Receivables) / (Net Sales / 365)

2019: [(500 + 800) / 2] / (4500 / 365) = 650/12.3288 = 52.72

B. Determine the cash conversion cycle for each year and discuss the changes that took

place, if any.

Chapter 6: Managing Cash Flow

106

Cash Conversion Cycle = Inventory-to-Sale Conversion Period + Sale-to-Cash

Conversion Period – Purchase-to-Payment Conversion Period

SPREADSHEET EXERCISES/PROBLEMS

[Note: The following activities are for students with spreadsheet software skills.]

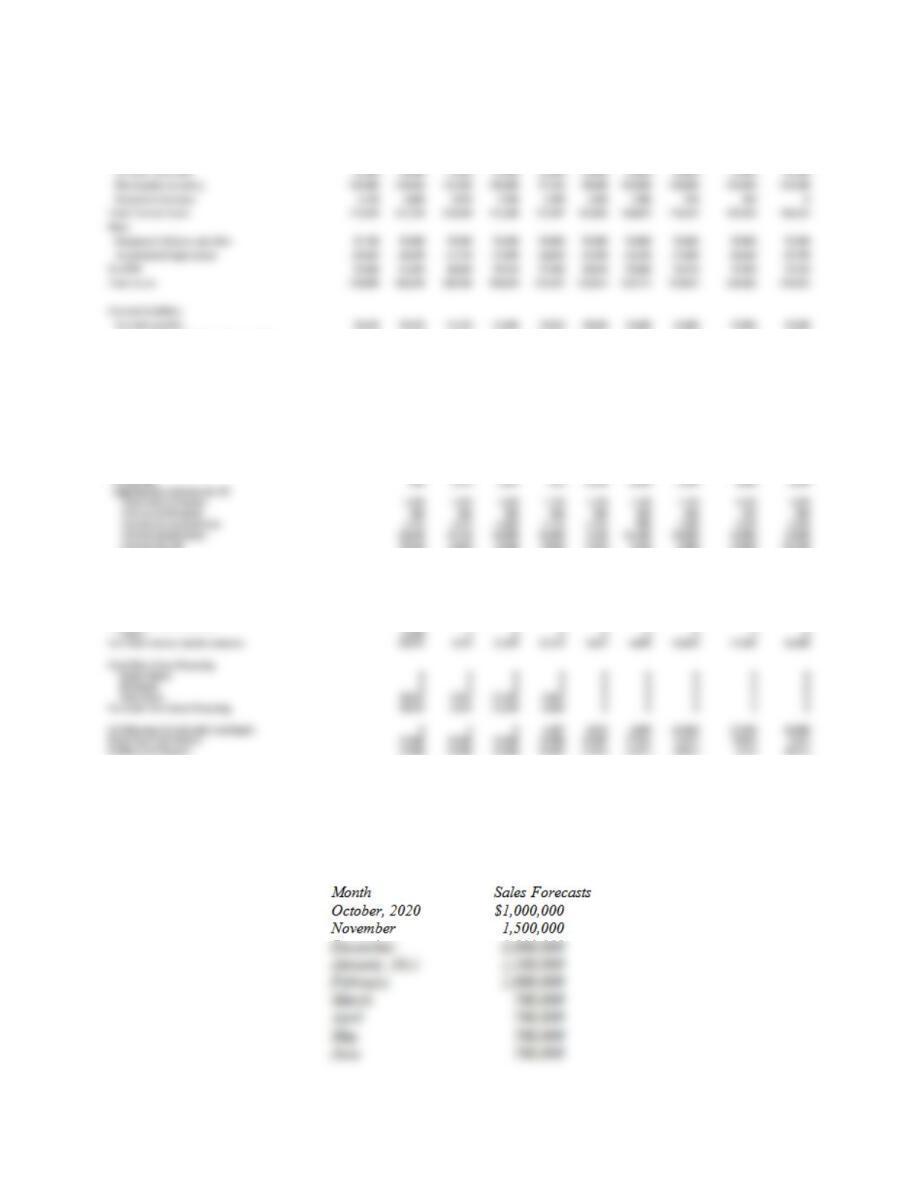

11. Short-term financial planning for the PDC Company was described during the early part of

this chapter. Refer to the PDC Company’s projected monthly operating schedules in Table 6.2.

PDC’s monthly sales for the remainder of 2020 are expected to be:

September $80,000

October $100,000

B. Prepare cash budgets for each of the last four months of 2020 for the PDC Company

and describe how the forecast affects the end of month cash balances.

See spreadsheet solution below.

C. Prepare the PDC Company’s projected monthly income statements for the August

through December period.

Chapter 6: Managing Cash Flow

107

E. Prepare the PDC Company’s projected monthly statements of cash flow for the August

through December period.

See spreadsheet solution below.

March April May June July Aug. Sept. Oct. Nov. Dec. Jan.

Schedule 1: Sales Forecast 92,000 115,000 184,000 138,000 115,000 92,000 80,000 100,000 130,000 160,000 100,000

Credit sales, 40% 36,800 46,000 73,600 55,200 46,000 36,800 32,000 40,000 52,000 64,000

Cash sales, 60% 55,200 69,000 110,400 82,800 69,000 55,200 48,000 60,000 78,000 96,000

Schedule 4: Disbursements for Purchases

50% of last month’s purchases 38,640 59,570 51,520 41,860 33,810 28,840 33,600 43,400 53,900

50% of this month’s purchases 59,570 51,520 41,860 33,810 28,840 33,600 43,400 53,900 39,200

Disbursements for merchandise 98,210 111,090 93,380 75,670 62,650 62,440 77,000 97,300 93,100

Chapter 6: Managing Cash Flow

108

Cash Budget April May June July Aug. Sept. Oct. Nov. Dec.

Beginning cash balance 23,000 23,000 23,000 23,000 29,487 37,562 32,672 18,822 5,422

Cash receipts

Collections from customers 105,800 156,400 156,400 124,200 101,200 84,800 92,000 118,000 148,000

Total cash available for needs, before fin. 128,800 179,400 179,400 147,200 130,687 122,362 124,672 136,822 153,422

Total cash needed 159,735 176,065 157,780 133,745 116,125 112,690 128,850 154,400 156,200

Excess of total cash -30,935 3,335 21,620 13,455 14,562 9,672 -4,178 -17,578 -2,778

Financing

New Borrowing 30,935 0 0 0 0 0 0 0 0

Repayments 2,871 21,199 6,865 0 0 0 0 0

Loan balance 30,935 28,064 6,865 0 0 0 0 0 0

Interest 0 464 421 103 0 0 0 0 0

Total effects of financing 30,935 -3,335 -21,620 -6,968 0 0 0 0 0

Cash balance 23,000 23,000 23,000 29,487 37,562 32,672 18,822 5,422 20,222

Budgeted Income Statements

Sales 92,000 115,000 184,000 138,000 115,000 92,000 80,000 100,000 130,000 160,000

COGS -64,400 -80,500 -128,800 -96,600 -80,500 -64,400 -56,000 -70,000 -91,000 -112,000

Gross Margin 27,600 34,500 55,200 41,400 34,500 27,600 24,000 30,000 39,000 48,000

Chapter 6: Managing Cash Flow

109

12. Artero Corporation, discussed in Problem 7, is a retailer of toy products. The firm’s

management team recently extended the monthly sales forecasts that were prepared for the

last three months of 2020 for an additional 6 months in 2021. These forecasts were

presented to Swen Artero, the firm’s president, as follows.

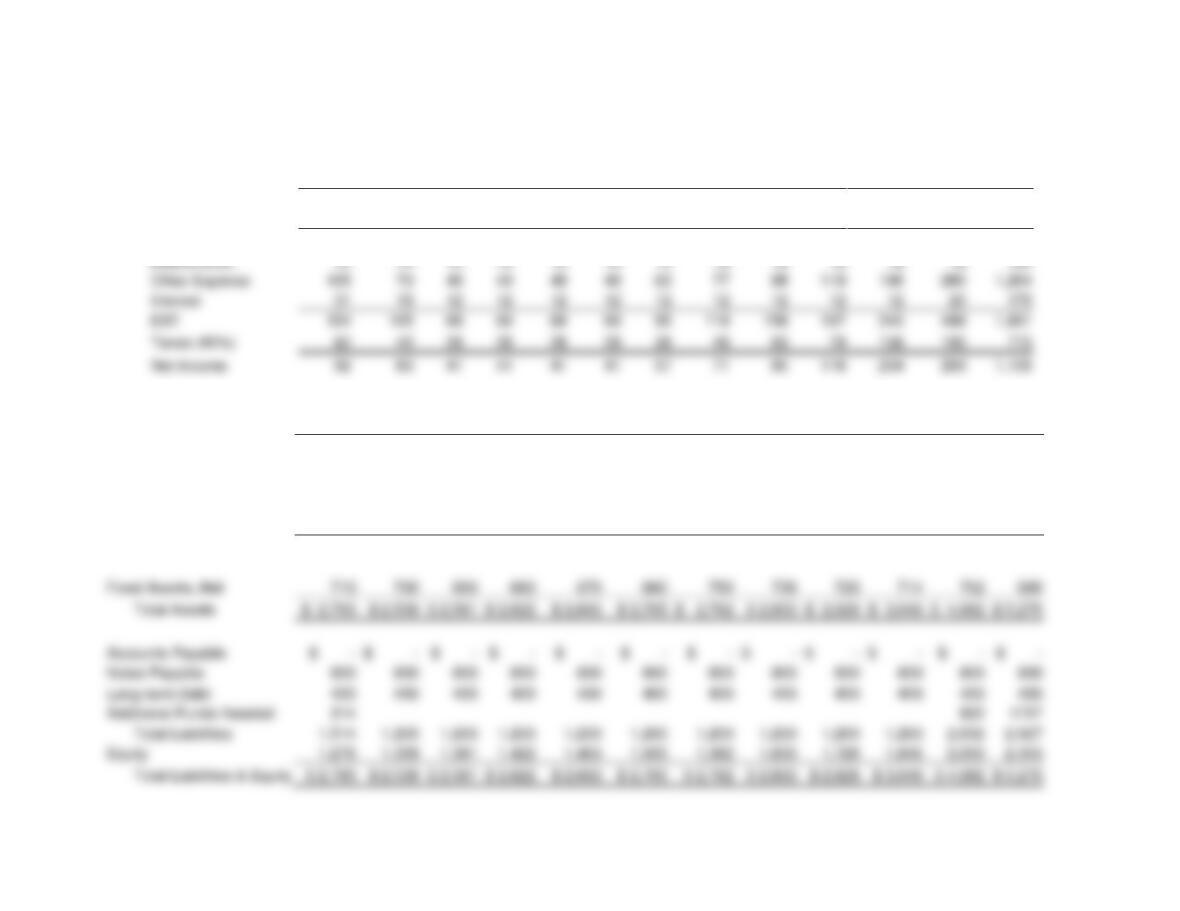

Balance Sheets

Current Assets:

Cash 23,000 23,000 23,000 23,000 29,487 37,562 32,672 18,822 5,422 20,222

Accrued wages and commissions payable 9,775 11,500 16,675 13,225 11,500 9,775 8,875 10,375 12,625 14,875

Loan 0 30,935 28,064 6,865 0 0 0 0 0 0

Total Current Liabilities 48,415 102,005 96,259 61,950 45,310 38,615 42,475 53,775 66,525 54,075

Owner’s equity 181,585 181,125 187,101 188,520 187,957 185,197 181,237 179,277 180,317 184,357

Total equities 230,000 283,130 283,360 250,470 233,267 223,812 223,712 233,052 246,842 238,432

Accounting Statement of Cash Flows

Cash Flows From Activities

Net Income -460 5,976 1,419 -563 -2,760 -3,960 -1,960 1,040 4,040

Adjustments to Net Inc for CF

Decrease in Prepaids 460 460 460 460 460 460 460 460 460

Increase in Accrued Liab. 1,725 5,175 -3,450 -1,725 -1,725 -900 1,500 2,250 2,250

Decrease in Inventory -38,640 25,760 12,880 12,880 6,720 -11,200 -16,800 -16,800 33,600

Decrease in A/P 20,930 -8,050 -9,660 -8,050 -4,970 4,760 9,800 10,500 -14,700

Increase in A/R -9,200 -27,600 18,400 9,200 9,200 4,800 -8,000 -12,000 -12,000

Decrease in Def. Inc. Tax 0 0 0 0 0 0 0 0 0

Total Adjustments -23,575 -3,105 19,780 13,915 10,835 -930 -11,890 -14,440 10,760

Net Cash Flow From Opps (Acct.) -24,035 2,871 21,199 13,352 8,075 -4,890 -13,850 -13,400 14,800

Cash Flows From Investing

Capex -6,900 0 0 0 0 0 0 0 0

Net Cash Used by Ops/Investments -30,935 2,871 21,199 13,352 8,075 -4,890 -13,850 -13,400 14,800

Cash Flows from Financing

Equity Issues 0 0 0 0 0 0 0 0 0

Dividends 0 0 0 0 0 0 0 0 0

Debt Issues 30,935 -2,871 -21,199 -6,865 0 0 0 0 0

Net Cash Flows from Financing 30,935 -2,871 -21,199 -6,865 0 0 0 0 0

Net Decrease in Cash and Cash Equiv. 0 0 0 6,487 8,075 -4,890 -13,850 -13,400 14,800

Beginning Cash Balance 23,000 23,000 23,000 23,000 29,487 37,562 32,672 18,822 5,422

Ending Cash Balance 23,000 23,000 23,000 29,487 37,562 32,672 18,822 5,422 20,222

Chapter 6: Managing Cash Flow

110

A. Use the income statement related data and the balance sheet information from Problem 7

to prepare monthly income statements, balance sheets, and statements of cash flow for

October through December of 2020. What is the maximum amount of bank borrowing

that would be needed?

Artero Corporation

Income Statement

(Thousands of Dollars)

Sept. 2020

Oct. 2020

Nov. 2020

Dec. 2020

Sales

$ 700

$ 1,000

$ 1,500

$ 3,000

Cost of Goods Sold

560

800

1,200

2,400

Gross Margin

140

200

300

600

Depreciation

Other Expense

105

210

Interest

108

170

362

Taxes (40%)

145

Net Income

102

217

Balance Sheet

(Thousands of Dollars)

Sept.30, 20

Oct.31, 20

Nov. 30, 20

Dec. 31, 20

Cash

$ 50

$ 80

$ 80

$ 80

Accounts Receivable

700

1,000

1,500

3,000

Inventories

500

500

500

500

Total Currents Assets

1,250

1,580

2,080

3,580

Fixed Assets, Net

750

730

720

Total Assets

Accounts Payable

Notes Payable

800

800

800

400

400

400

400

Additional Funds Needed

643

Equity

800

967

1,184

Total Liabilities & Equity

Statement of Cash Flow

(Thousands of Dollars)

Chapter 6: Managing Cash Flow

111

10/31/2020

11/30/2020

12/31/2020

Cash Flow From Operations

Net Income

$ 65

$ 102

$ 217

+ Depreciation

10

10

10

– Increase In A/R

300

500

1,500

– Increase In Inventory

0

0

0

Cash Flow from Investing

0

0

0

Cash Flow from Financing

0

0

0

Total Cash Flow

Required Balance

80

80

80

Additional Funds Needed

255

388

1,273

Cumulative Funds Needed

255

643

1,916

Ending Cash Balance

80

80

80

As shown in both Balance Sheet and Statement of Cash Flow, $1,916,000 was needed to

support the projected sales in the coming three months.

B. Prepare monthly income statements, balance sheets, and statements of cash flow for the

Chapter 6: Managing Cash Flow

112

Artero Corporation Pro Forma Statements 2021

Income Statement (Thousands of Dollars)

Jan. 15

Feb. 15

Mar. 15

Apr. 15

May. 15

June. 15

July. 15

Aug. 15

Sep. 15

Oct. 15

Nov. 15

Dec. 15

2021

Sales

$1,500

$ 1,000

$ 700

$ 700

$ 700

$ 700

$ 900

$ 1,100

$ 1,400

$ 1,700

$ 2,800

$ 4,000

$ 17,200

Cost of Goods Sold

1,200

800

560

560

560

560

720

880

1,120

1,360

2,240

3,200

$ 13,760

Gross Margin

300

200

140

140

140

140

180

220

280

340

560

800

3,440

Depreciation

10

10

10

10

10

10

10

12

12

12

12

12

130

Other Expense

105

70

49

49

49

49

63

77

98

119

196

280

1,204

Interest

31

15

12

12

12

12

12

12

12

12

12

20

175

154

105

69

69

69

69

95

119

158

197

340

488

1,931

Taxes (40%)

62

42

28

28

28

28

38

48

63

79

136

195

773

Net Income

92

63

41

41

41

41

57

71

95

118

204

293

1,159

Balance Sheet 2021 (Thousands of Dollars)

Jan. 15

Feb. 15

Mar. 15

Apr. 15

May. 15

June. 15

July. 15

Aug. 15

Sep. 15

Oct. 15

Nov.15

Dec. 15

Cash Required

$ 80

$ 80

$ 80

$ 80

$ 80

$ 80

$ 80

$ 80

$ 80

$ 80

$ 80

$ 80

Cash Surplus

259

611

662

713

765

532

415

222

52

Total Cash

339

691

742

793

845

612

495

302

132

80

80

Accounts Receivable

1,500

1,000

700

700

700

700

900

1,100

1,400

1,700

2,800

4,000

Inventories

500

500

500

500

500

500

500

500

500

500

500

500

Total Currents Assets

2,080

1,839

1,891

1,942

1,993

2,045

2,012

2,095

2,202

2,332

3,380

4,580

Fixed Assets, Net

710

700

690

680

670

660

750

738

726

714

702

690

Total Assets

$ 2,790

$ 2,539

$ 2,581

$ 2,622

$ 2,762

$ 2,833

$ 2,928

$ 3,046

$ 4,082

$ 5,270

Accounts Payable

Notes Payable

800

800

800

800

800

800

800

800

800

800

800

800

400

400

400

400

400

400

400

400

400

400

400

400

Additional Funds Needed

314

832

1727

Total Liabilities

1,514

1,200

1,200

1,200

1,200

1,200

1,200

1,200

1,200

1,200

2,032

2,927

Chapter 6: Managing Cash Flow

113

Statement of Cash Flow (Thousands of Dollars)

1/31/21

2/28/21

3/31/21

4/30/21

5/31/21

6/30/21

7/31/21

8/31/21

9/30/21

10/31/21

11/30/21

12/31/21

Cash Flow From Operations

Net Income

$ 92

$ 63

$ 41

$ 41

$ 41

$ 41

$ 57

$ 71

$ 95

$ 118

$ 204

$ 293

+ Depreciation

10

10

10

10

10

10

10

12

12

12

12

12

– Increase In A/R

–1,500

–500

–300

0

0

0

200

200

300

300

1,100

1,200

– Increase In Inventory

0

0

0

0

0

0

0

0

0

0

0

0

Cash Flow From

573

351

51

51

51

Cash Flow from Investing

0

0

0

0

0

0

0

0

0

0

0

Cash Flow from Financing

0

0

0

0

0

0

0

0

0

0

0

0

Total Cash Flow

573

351

51

51

51

Beginning Cash Balance

80

80

80

80

80

80

80

80

80

80

80

80

Required Balance

80

80

80

80

80

80

80

80

80

80

80

80

Additional Funds Needed

573

351

51

51

51

Cumulative Funds Needed

0

0

0

0

0

0

0

0

0

832

1,727

Cash Surplus

259

611

662

713

765

532

415

222

52

Ending Total Cash

80

339

691

742

793

845

612

495

302

132

80

80

As shown on the company’s balance sheet and statement of cash flow, started from February of 2021, the cash surplus account

increased monthly through the first-half of the year (with a peak in June). This indicated that the positive cash flow from operations in

January and through much of February were used to repay the $1.9 million additional bank borrowing needed during the last three

months of 2020, and the borrowing will be paid off by February of 2021.

Chapter 6: Managing Cash Flow

114

C. Based on your financial statement projections for the first six months of 2021, indicate

whether new bank borrowing will be needed.

13. Artero Corporation, discussed in Problems 7 and 12, is a retailer of toy products. This is a

continuation of Problem 12. The firm’s management team recently extended the monthly sales

forecasts through the last six months of 2021. Artero expects to spend $100,000 on fixed assets

in July 2021 and depreciation charges will increase to $12,000 per month beginning in August

2021.

A. Prepare monthly income statements, balance sheets, and statements of cash flow for the last

six months of 2021.

B. Based on your financial statement projections for the last six months of 2021 indicate (1)

whether new bank borrowing will be needed to finance the seasonal sales pattern and (2) if a

loan is needed, when does the need start occurring and what is the maximum amount

needed?

C. Assume that sales are forecasted for the first three months of 2022 as follows: January = $3

million, February = $2 million, and March = $1 million. Will Artero be able to pay off any

bank borrowing that is needed in 2021? Based on your analyses, what type(s), if any, of bank

loan(s) are needed in 2021?

Artero Corporation

Pro Forma Income Statement 2022 (Thousands of Dollars)

Jan 2022

Feb 2022

Mar.2022

Chapter 6: Managing Cash Flow

115

Depreciation

12

12

12

Other Expense

210

70

Interest

297

12

106

Taxes (40%)

42.4

Net Income

63.6

Pro Forma Balance Sheet (Thousands of Dollars)

Jan. 2022

Feb. 2022

Mar. 2022

Cash required

80

80

80

Cash Surplus

645

1720

Accounts Receivable

3000

2000

1000

Inventories

500

500

500

Total Currents Assets

3580

3225

3300

Fixed Assets, Net

678

666

654

Total Assets

4258

3891

3954

Accounts Payable

Notes Payable

800

800

800

400

400

400

Additional Funds Needed

506

Total Liabilities

1706

1200

1200

Equity

2552

2691

2754

Total Liabilities & Equity

4258

3891

3954

As indicated above in the projected 2022 pro forma statement, Artero will be able to pay off all

borrowing of $1,727,000 in December, 2021 by February of 2022. A surplus cash of $645,000

will also appear in February of 2022. In this case, short-term borrowing will be sufficient for

Artero to obtain all of the additional funds needed in 2021.

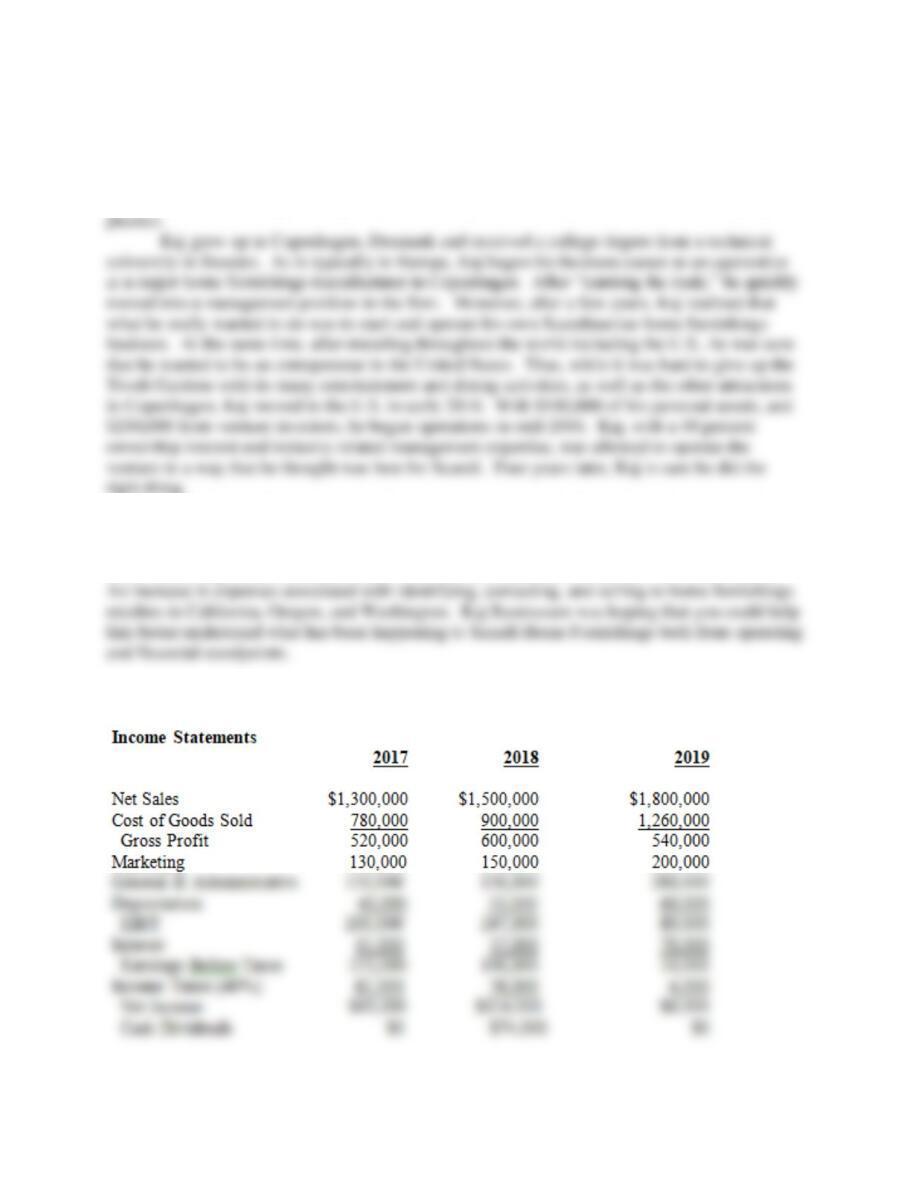

MINI CASE: SCANDI HOME FURNISHINGS, INC.

Kaj Rasmussen founded Scandi Home Furnishings as a corporation during mid-2016. Sales

during the first full year (2017) of operation reached $1.3 million. Sales increased by 15 percent

in 2018 and another 20 percent in 2019. However, profits after increasing in 2018 over 2017 fell

Chapter 6: Managing Cash Flow

116

allure of Scandinavian home furnishings. Some say that the inspiration for the Scandinavian

design can be traced to the “elegant curves” of art nouveau from which designers were able to

produce aesthetically pleasing, structurally strong modern furniture. Danish furnishings and the

home furnishings produced by the other Scandinavian countries—Sweden, Norway, and

Finland—are made using wood (primarily oak, maple, and ash), aluminum, steel, and high-grade

right thing.

Following are the three years of income statements and balance sheets for the Scandi

Home Furnishings Corporation. Kaj has felt that in order to maintain a competitive advantage

that he would need to continue to expand sales. After first concentrating on selling Scandinavian

home furnishings in the northeast in 2017 and 2018, he decided to enter the west coast market.

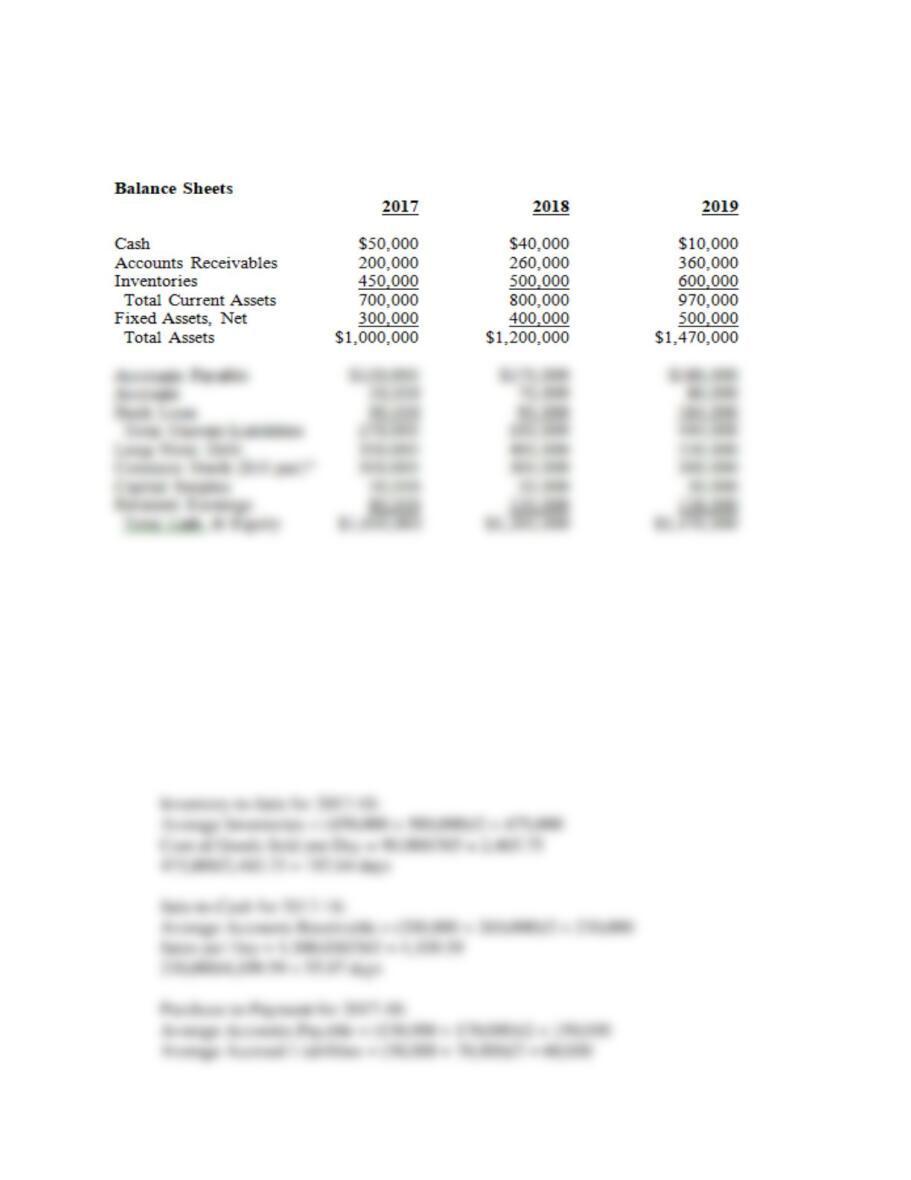

SCANDI HOME FURNISHINGS, INC.

Chapter 6: Managing Cash Flow

117

SCANDI HOME FURNISHINGS, INC.

Note: 30,000 shares of common stock were issued to Kaj Rasmussen and the venture investors

when Scandi Home Furnishings was incorporated in mid-2016.

A. An analysis of the cash conversion cycle should also help Kaj understand what has been

happening to the operations of Scandi. Prepare an analysis of the average conversion

periods for the three components of the cash conversion cycle for 2017-2018 and 2018-

2019. Explain was has happened in terms of each component of the cycle.

Ratios are based on the current year’s income statement amounts and average amounts

(past year and current year) for balance sheet items.

Chapter 6: Managing Cash Flow

118

Purchase-to-Payment for 2018-19:

Average Accounts Payable = (170,000 + 180,000)/2 = 175,000

Average Accrued Liabilities = (70,000 + 80,000)/2 = 75,000

175,000 + 75,000 = 250,000

Cost of Goods Sold per Day = 1,260,000/365 = 3,452.05

250,000/3,452.05 = 72.42 days

Cash Conversion Cycle (in Days):

2017-18 2018-19 Change

Inventory-to-Sale 192.64 159.33 Better

Sale-to-Cash 55.97 62.86 Worse

Purchase-to-Payment (85.17) (72.42) Worse

Cash Conversion Cycle 163.44 149.77 Better

B. Kaj has been able to obtain some industry ratio data from the home furnishings industry

trade association of which he is a member. The industry association collects proprietary

Chapter 6: Managing Cash Flow

119

Conversion Periods (in Days):

Scandi

Scandi Corporation Industry Compared to

2017-18 2018-19 Average Industry

Inventory-to-Sale 192.64 159.33 200 Better

Sale-to-Cash 55.97 62.86 60 Worse