89

Chapter 6

MANAGING CASH FLOW

FOCUS

In this chapter, we focus on short-term financial planning involving projecting monthly financial

statements for one year or less. The availability of cash is what drives the entrepreneurial

venture. Inadequate cash often constrains the venture’s ability to grow, is a primary cause of

financial distress, and can result in bankruptcy even though the venture may be profitable in an

LEARNING OBJECTIVES

LO 6.1: Describe the types of financial planning needed at various stages in a venture’s life

cycle.

LO 6.2: Explain why cash is so important in early-stage ventures.

CHAPTER OUTLINE

6.1 FINANCIAL PLANNING THROUGHOUT THE VENTURE’S LIFE CYCLE

6.2 SURVIVING IN THE SHORT RUN

6.3 SHORT-TERM CASH-PLANNING TOOLS

6.4 PROJECTED MONTHLY FINANCIAL STATEMENTS

DISCUSSION QUESTIONS AND ANSWERS

1. What does short-term financial planning involve?

Short-term financial planning usually involves projecting monthly financial statements and

Chapter 6: Managing Cash Flow

90

2. Provide a description of the financing cost implications associated with a venture’s need for

additional funds.

The cost of obtaining additional funds may be explicit, such as additional interest expense

associated with debt. Interest expense shows up directly on the projected income statement

3. What is meant by a cash budget? Describe how a cash budget is prepared.

A cash budget is a financial tool showing the inflows and outflows of the firm’s cash balance

4. Besides the cash budget, what additional financial statements are projected monthly in

conjunction with short-term financial planning?

Additional statements that can be prepared on a monthly basis to provide a clear financial

1. What is meant by a venture’s operating cycle?

A venture’s operating cycle is the time it takes to purchase raw materials, assemble a product, book a

sale, and collect on it.

2. Describe the cash conversion cycle (C3).

3. What are the three components of the cash conversion cycle (C3)? How is each component

calculated?

The three components of the cash conversion cycle are inventory-to-sale conversion period, sales-to–

cash conversion period, and purchase-to-payment conversion period. The inventory-to–sale

4. Briefly explain how changes in the conversion times of the components of the C3 can be interpreted.

A lengthening of the inventory-to-sale conversion period indicates less efficient inventory

management. A lengthening of the sale-to–cash conversion period indicates less efficient collections

Chapter 6: Managing Cash Flow

91

9. From the Headlines – Sustainable Northwest: Describe Sustainable Northwest’s short-term

inflows and outflows of cash. What would you expect to be the main ingredients of each part

of the cash conversion cycle?

Sustainable Northwest is a nonprofit organization with a for-profit wholesale lumberyard

INTERNET ACTIVITIES

EXERCISES/PROBLEMS AND ANSWERS

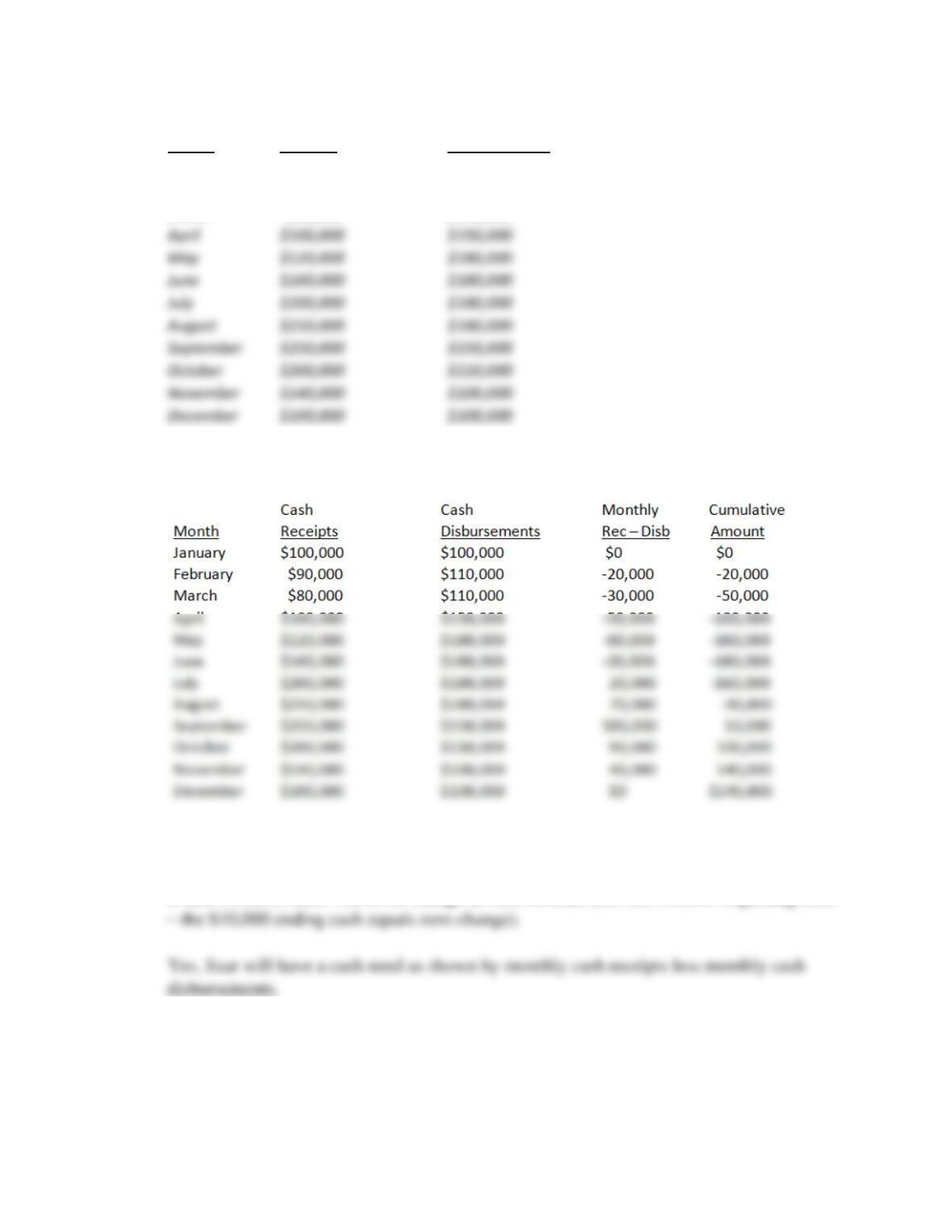

1. [Short-Term Financial Planning] The Itsar Products Company has made the following

monthly estimates of cash receipts and cash disbursements when preparing cash budgets for

the next twelve months. Itsar Products has beginning cash on hand of $10,000 and wants to

maintain this minimum cash level throughout the next year.

Chapter 6: Managing Cash Flow

92

Cash Cash

Month Receipts Disbursements

January $100,000 $100,000

February $90,000 $110,000

March $80,000 $110,000

A. Determine whether Itsar Products will have a cash need during the next year.

Note: the January beginning cash on hand is $10,000. Since the minimum end of cash

month

B. If Itsar Products has a cash need, indicate the month when the need will begin and

determine the month and amount when the maximum need will occur.

Chapter 6: Managing Cash Flow

93

A cash need will occur in February when $20,000 will be needed. The largest monthly

C. Determine whether the cash need (if any) can be repaid within the next year.

As previously noted, a cash need of $20,000 occurs in February and increases to a

maximum cumulative monthly cash need of $180,000 in June. The cumulative

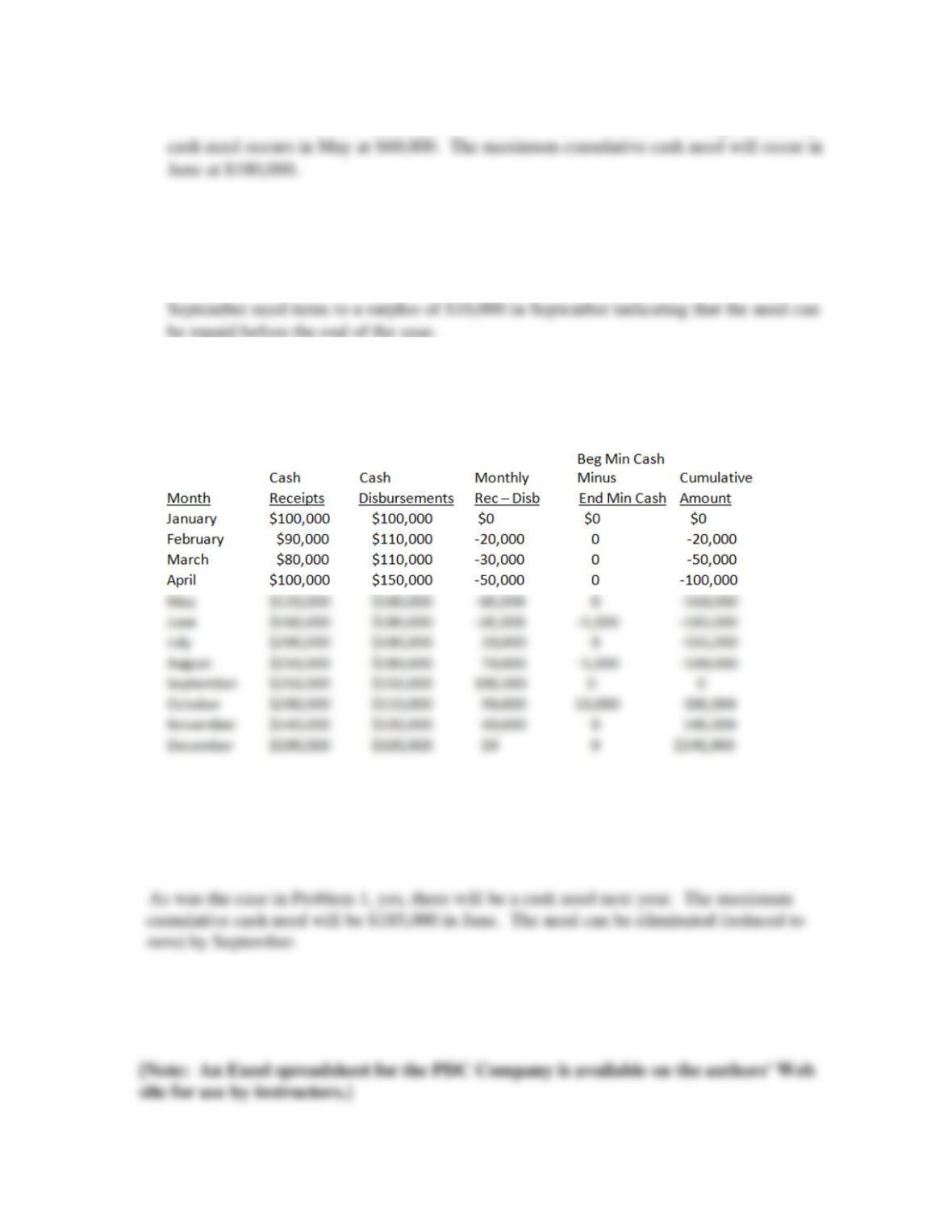

2. Rework Problem 1 assuming minimum cash on hand requirements are $10,000 a month

through May, increase to $15,000 in June and July, increase further to $20,000 in August

and September, and return to the $10,000 per month level beginning in October.

Note: Beginning cash on hand for January was $10,000. Since the target ending cash on

hand amount also was $10,000, there was no change in monthly cash on hand need. In

June, the beginning cash on hand was $10,000; however, the target ending cash on hand was

$15,000, which meant that an additional $5,000 ($10,000 – $15,000) was needed.

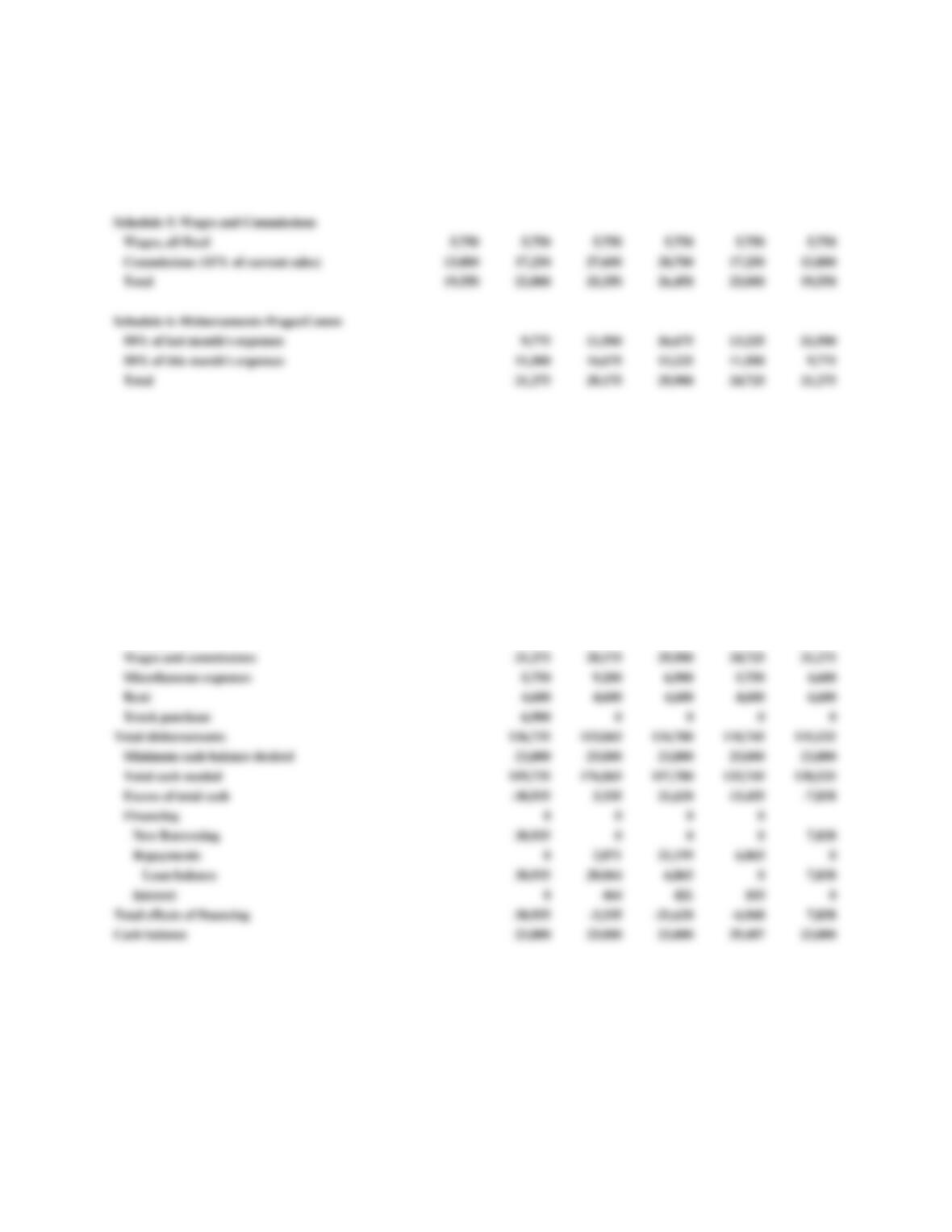

3. [Short-Term Financial Planning] The PDC Company was described during the early part of

this chapter. Refer to the PDC Company’s projected monthly operating schedules in Table

6.2. PDC’s sales are projected to be $80,000 in September 2020.

Chapter 6: Managing Cash Flow

94

A. Prepare PDC’s sales schedule, purchases schedule, and the wages schedule for August

2020.

See the spreadsheet solution for Problem 11. Here we are focusing just on projecting the

month of August.

Sales Schedule:

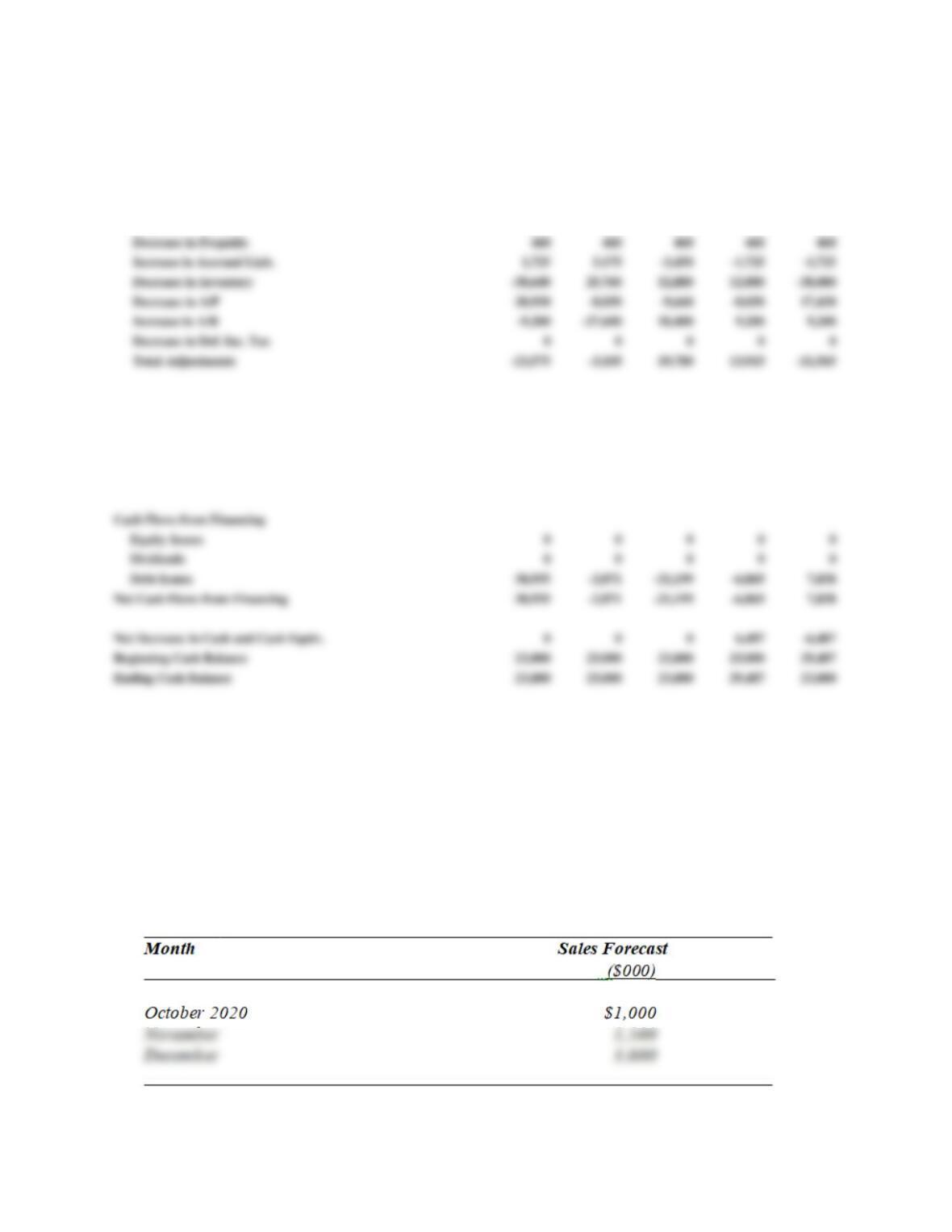

Schedule 1: Sales Forecast

Total inventory needed is $90,800 + $64,400 = $155,200

Schedule 3: Purchases

$155,200 total inventory needed minus $97,520 beginning inventory (i.e., ending

inventory from July) = $57,680 purchases

B. Prepare a cash budget for August 2020 for the PDC Company and describe how the

forecast affects the end-of-month cash balance.

See the spreadsheet solution for August provided in the comprehensive spreadsheet

4. [Short-Term Financial Planning] The PDC Company was described during the early

part of this chapter. Refer to the PDC Company’s projected monthly operating schedules

in Table 6.2. PDC’s sales are projected to be $80,000 in September 2020.

Chapter 6: Managing Cash Flow

95

A. Prepare the PDC Company’s projected income statement for August.

See the spreadsheet solution for August provided in the comprehensive spreadsheet

output provided in Problem 11.

C. Prepare the PDC Company’s projected statement of cash flow for August.

See the spreadsheet solution for August provided in the comprehensive spreadsheet

output provided in Problem 11.

5. [Short-Term Financial Planning] Rework Problem 3 based on the assumption that, because

of an unexpected order, the PDC Company’s sales are forecasted to be $160,000 for

September 2020.

March April May June July Aug. Sept.

Schedule 1: Sales Forecast 92,000 115,000 184,000 138,000 115,000 92,000 160,000

Credit sales, 40% 36,800 46,000 73,600 55,200 46,000 36,800

Cash sales, 60% 55,200 69,000 110,400 82,800 69,000 55,200

Chapter 6: Managing Cash Flow

96

Schedule 4: Disbursements for Purchases

50% of last month’s purchases 38,640 59,570 51,520 41,860 33,810

50% of this month’s purchases 59,570 51,520 41,860 33,810 51,240

Disbursements for merchandise 98,210 111,090 93,380 75,670 85,050

Cash Budget April May June July Aug.

Beginning cash balance 23,000 23,000 23,000 23,000 29,487

Cash receipts 0 0 0 0

Collections from customers 105,800 156,400 156,400 124,200 101,200

Total cash available for needs, before fin. 128,800 179,400 179,400 147,200 130,687

Cash disbursements: 0 0 0 0

Merchandise 98,210 111,090 93,380 75,670 85,050

Chapter 6: Managing Cash Flow

97

6. [Short-Term Financial Planning] Rework Problem 4 based on the assumption that, because

of an unexpected order, the PDC Company’s sales are forecasted to be $160,000 for

September 2020.

Budgeted Income Statements

Sales 92,000 115,000 184,000 138,000 115,000 92,000

COGS -64,400 -80,500 -128,800 -96,600 -80,500 -64,400

Gross Margin 27,600 34,500 55,200 41,400 34,500 27,600

Operating Expenses 0 0 0 0 0

Wages and commissions -19,550 -23,000 -33,350 -26,450 -23,000 -19,550

Balance Sheets

Current Assets:

Cash 23,000 23,000 23,000 23,000 29,487 23,000

Accounts receivable 36,800 46,000 73,600 55,200 46,000 36,800

Merchandise inventory 110,400 149,040 123,280 110,400 97,520 135,600

Current Liabilities

Accounts payable 38,640 59,570 51,520 41,860 33,810 51,240

Accrued wages and commissions payable 9,775 11,500 16,675 13,225 11,500 9,775

Loan 0 30,935 28,064 6,865 0 7,838

Chapter 6: Managing Cash Flow

98

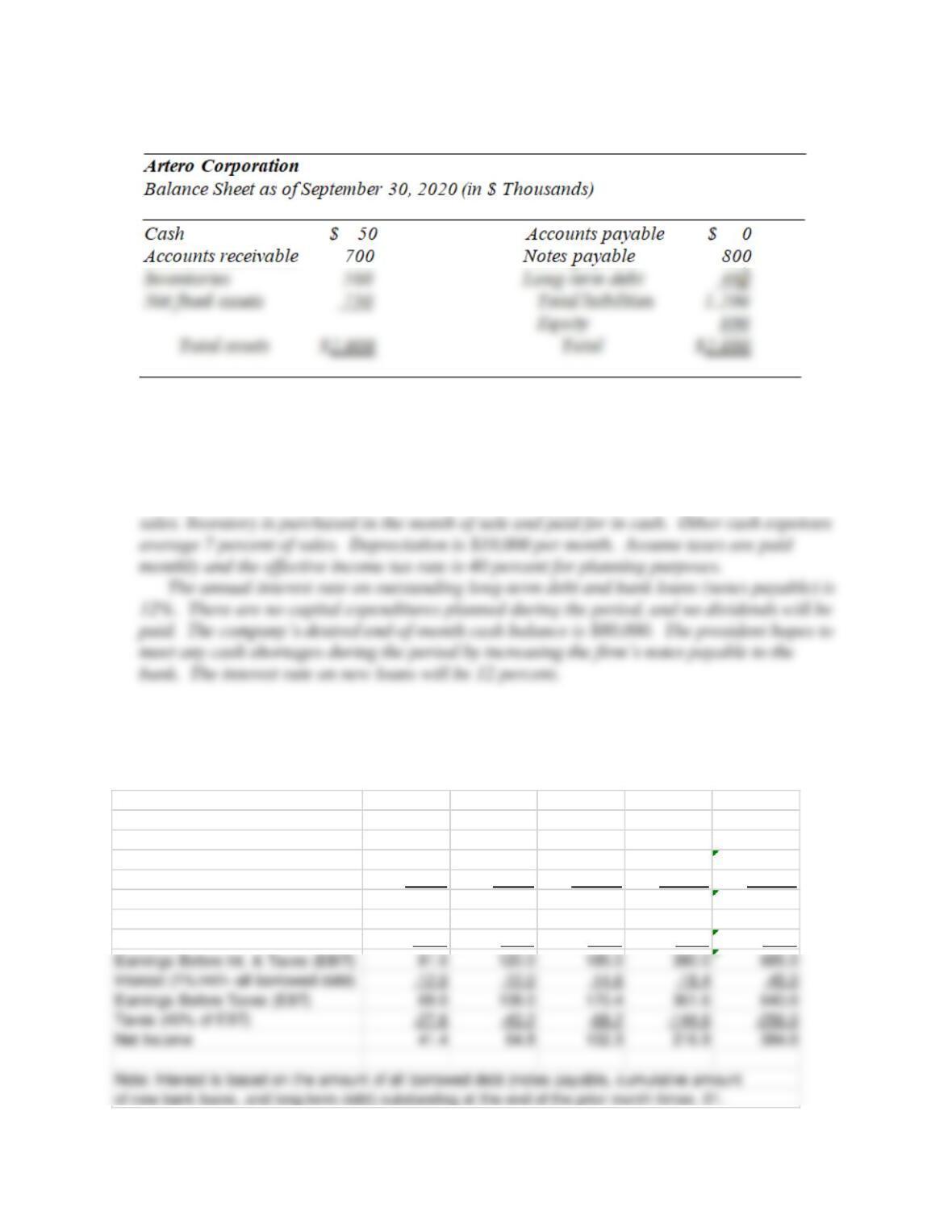

7. [Short-Term Financial Planning] Artero Corporation is a traditional toy products retailer

that recently also started an Internet-based subsidiary that sells toys online. A markup is

added on goods the company purchases from manufacturers for resale. Swen Artero, the

company president, is preparing for a meeting with Jennifer Brown, a loan officer with First

Banco Corporation, to review year end financing requirements. After discussions with the

company’s marketing manager, Rolf Eriksson, and finance manager, Lisa Erdinger, sales

over the last three months of 2020 are forecasted to be:

Accounting Statement of Cash Flows

Cash Flows From Activities

Net Income -460 5,976 1,419 -563 -2,760

Adjustments to Net Inc for CF

Depreciation Expense 1,150 1,150 1,150 1,150 1,150

Net Cash Flow From Opps (Acct.) -24,035 2,871 21,199 13,352 -14,325

Cash Flows From Investing

Capex -6,900 0 0 0 0

Net Cash Used by Ops/Investments -30,935 2,871 21,199 13,352 -14,325

Chapter 6: Managing Cash Flow

99

Artero’s balance sheet as of the end of September, 2020 was as follows.

All sales are made on credit terms of net 30 days and are collected the following month and

no bad debts are anticipated. The accounts receivable on the balance sheet at the end of

September thus will be collected in October. The October sales will be collected in

November, and so on. Inventory on hand represents a minimum operating level (or “safety”

stock), which the company intends to maintain. Cost of goods sold average 80 percent of

A. Prepare monthly pro forma income statements for October, November, and December,

and for the quarter ending December 31, 2020.

Artero Corporation Solution Quarter

Ch 6, Prob. 7 (In $ Thousands) Actual Projected Projected Projected Ending

Income Statements Sept. 2020 Oct. Nov. Dec. Dec. 2020

Sales 700.0 1000.0 1500.0 3000.0 5500.0

Cost of Goods Sold (80% of Sales) –560.0 –800.0 -1200.0 -2400.0 -4400.0

Gross Profit 140.0 200.0 300.0 600.0 1100.0

Other Expenses (7% of Sales) -49.0 –70.0 –105.0 –210.0 –385.0

Depreciation –10.0 -10.0 -10.0 -10.0 -30.0

Chapter 6: Managing Cash Flow

100

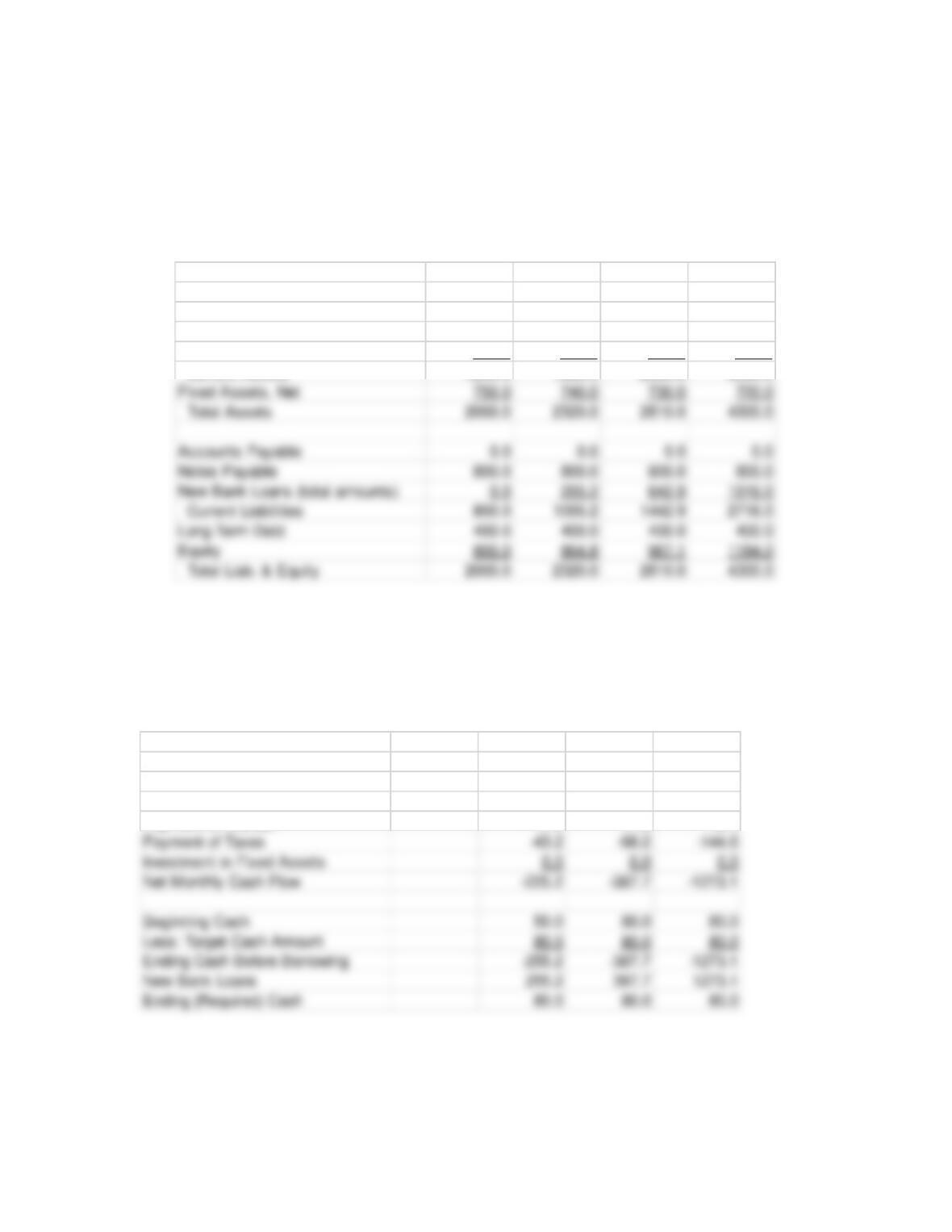

B. Prepare monthly pro forma balance sheets at the end of October, November, and

December, 2020.

C. Prepare both a monthly cash budget and pro forma statements of cash flows for October,

November, and December 2020.

Balance Sheets Sept. 2020 Oct. Nov. Dec.

Required Cash 50.0 80.0 80.0 80.0

Surplus Cash 0.0 0.0 0.0 0.0

Accounts Receivable 700.0 1000.0 1500.0 3000.0

Inventories 500.0 500.0 500.0 500.0

Cash Budget Sept. 2020 Oct. Nov. Dec.

Collection of Receivables 700.0 1000.0 1500.0

Purchases –800.0 -1200.0 -2400.0

Other Cash Costs (7% of Sales) –70.0 –105.0 –210.0

Chapter 6: Managing Cash Flow

101

D. Describe your findings and indicate the maximum amount of bank borrowing that is

needed.

Based on the financial projection above, a maximum of $1,916,000 is needed.

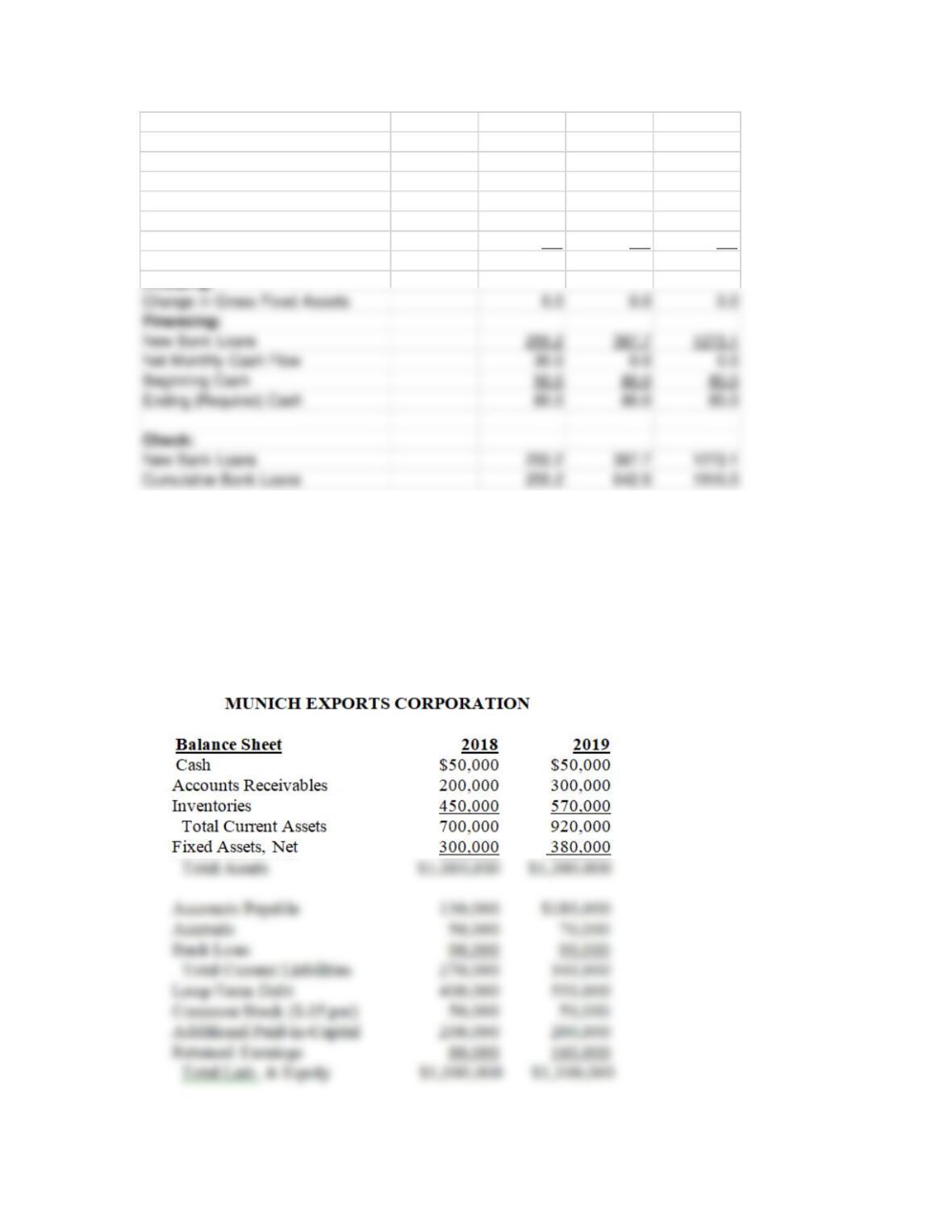

8. Cash Conversion Cycle] Two years of financial statement data for the Munich Export

Corporation are shown below.

Statement of Cash Flows Sept. 2020 Oct. Nov. Dec.

Operating:

Net Income 64.8 102.3 216.9

Depreciation 10.0 10.0 10.0

Change in Accts. Receivable –300.0 -500.0 –1500.0

Change in Inventories 0.0 0.0 0.0

Change in Accts. Payable 0.0 0.0 0.0

Cash Flow from Operations –225.2 -387.7 –1273.1

Chapter 6: Managing Cash Flow

102

A. Calculate the inventory-to-sale, sale-to-cash, and purchase-to-payment conversion

periods for Munich Exports for 2019.

Inventory-to-Sale Conversion Period = Average Inventories / (Cost of Goods Sold/365) =

[($450,000 + $570,000)/2]/$960,000/365 = $510,000/$2,630.14 = 193.91 days

B. Calculate the length of Munich Exports’ cash conversion cycle for 2019.

Cash Conversion Cycle = Inventory-to-Sale Conversion Period + Sale-to-Cash

9. [Cash Conversion Cycle] Castillo Products Company improved its operations from a net loss

in 2018 to a net profit in 2019. While the founders, Cindy and Rob Castillo, are happy about

these developments, they are concerned with trying to understand how long the firm takes to

Chapter 6: Managing Cash Flow

103

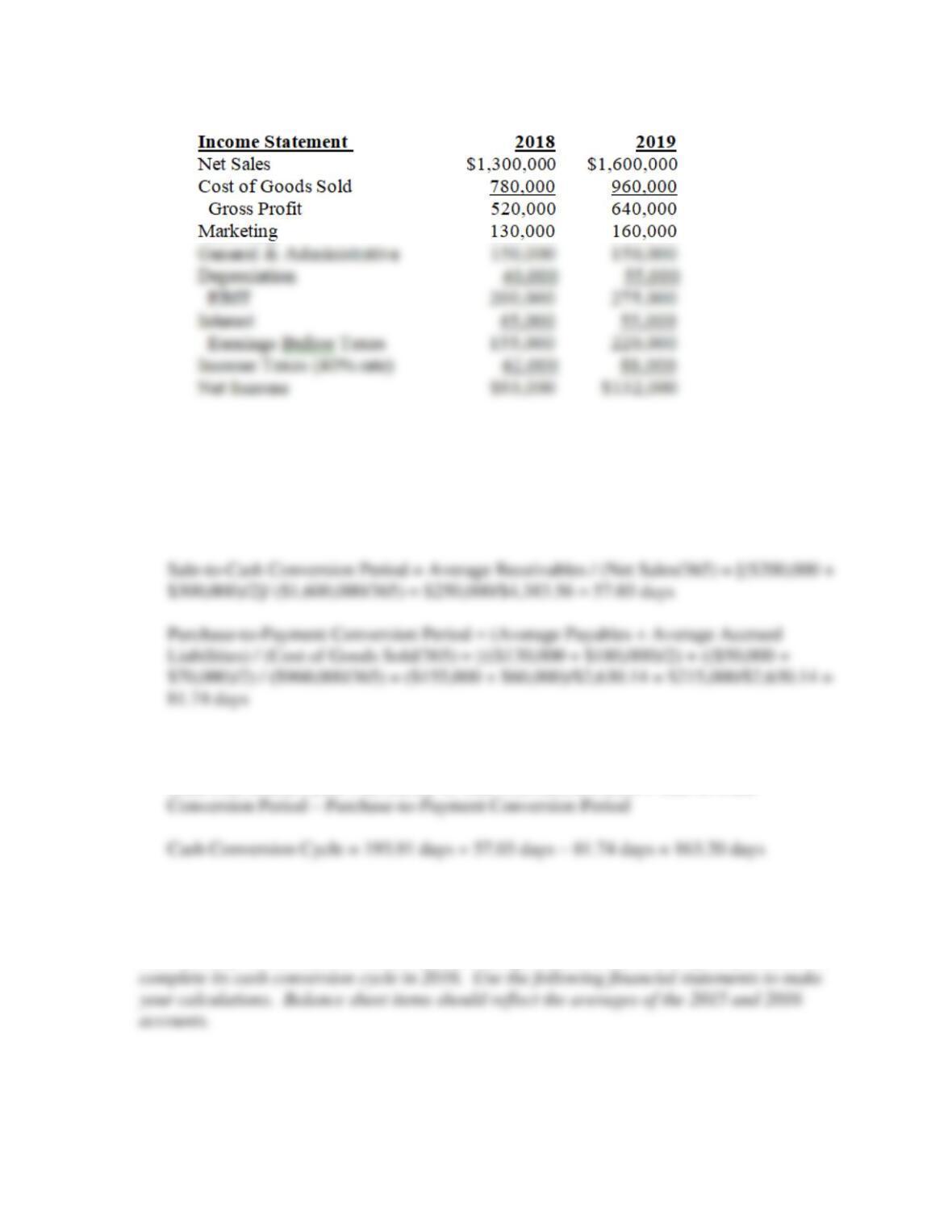

CASTILLO PRODUCTS COMPANY

INCOME STATEMENT

2018

2019

Net sales

$900,000

$1,500,000

Cost of goods sold

540,000

900,000

Gross profit

360,000

600,000

Marketing

90,000

150,000

General and administrative

250,000

250,000

Depreciation

40,000

EBIT

160,000

Interest

45,000

Earnings before taxes

100,000

Income taxes

Net income (loss)

BALANCE SHEET

2018

2019

Cash

$ 50,000

$ 20,000

Accounts receivable

200,000

280,000

Inventories

400,000

500,000

Total current assets

650,000

800,000

Gross fixed assets

450,000

540,000

Accumulated depreciation

–100,000

–140,000

Net fixed assets

350,000

400,000

Total assets

$1,000,000

$1,200,000

Accounts payable

$ 130,000

Accruals

Bank loan

100,000

Total current liabilities

270,000

330,000

Long-term debt

300,000

400,000

Common stock (0.05 par)

150,000

150,000

Additional paid-in-capital

200,000

200,000

Retained earnings

120,000

Total liabilities and equity

$1,000,000

$1,200,000

A. Calculate the inventory-to-sale conversion period for 2019.

Inventory-to-Sale Conversion Period = Avg. Inventory/Avg. Daily COGS

= (($400,000 + $500,000)/2)/($900,000/365) = 182.50 days

Chapter 6: Managing Cash Flow

104

C. Calculate the purchase-to-payment conversion period for 2019.

Purchase-to-Payment Conversion Period

= (Avg. Payables + Avg. Accruals)/Avg. Daily CGS

= (($130,000 + $160,000)/2 + ($50,000 + $70,000)/2)/($900,000/365) = 83.14 days

10. [Cash Conversion Cycle] Safety-First, Inc. makes portable ladders that can be used to exit

second floor levels of homes in the event of fire. Each ladder consists of fire resistant rope

and high strength plastic steps. A lightweight fire resistant cape with a smoke filter is

SAFETY-FIRST, INC.

Income Statements (in $ Thousands)

2018

2019

Net sales

3,750

4,500

Cost of goods sold

2,250

2,700

Gross profit

1,500

1,800

Operating expenses

670

860

Interest

Income before taxes

800

900

Income taxes

250

300

Net income

550

600

Balance Sheets (in $ Thousands)

2018

2019

Cash

400

150

Accounts receivable

500

800

Inventories

1,450

2,000

Total current assets

2,350

2,950

Gross fixed assets

2,000

2,800

Less accumulated depreciation

Net fixed assets

1,050

1,550