71

Chapter 5

EVALUATING OPERATING AND FINANCIAL PERFORMANCE

FOCUS

In this chapter, we focus on identifying and understanding the financial ratios used to evaluate

the venture’s financial performance over time. Venture performance and efficiency is important

to a variety of constituencies including lenders and creditors, equity investors, and the

LEARNING OBJECTIVES

LO 5.1: Understand important financial performance measures and their users by life cycle stage.

LO 5.2: Describe how financial ratios are used to monitor a venture’s performance.

LO 5.3: Identify specific cash burn rate measures and liquidity ratios and explain how they are

CHAPTER OUTLINE

5.1 USERS OF FINANCIAL PERFORMANCE MEASURES BY LIFE CYCLE STAGE

5.2 USING FINANCIAL RATIOS

5.3 CASH BURN RATES AND LIQUIDITY RATIOS

5.4 LEVERAGE RATIOS

A. Measuring Financial Leverage

B. Interpreting Changes in Financial Leverage

5.5 PROFITABILITY AND EFFICIENCY RATIOS

5.6 INDUSTRY COMPARABLE RATIO ANALYSIS

5.7 A HITCHHIKER’S GUIDE TO FINANCIAL ANALYSIS

SUMMARY

DISCUSSION QUESTIONS AND ANSWERS

Chapter 5: Evaluating Operating and Financial Performance

72

1. Identify the types of financing typically used during each life cycle stage of the successful

entrepreneurial venture.

Refer to Figure 5.1.

2. Describe the types of financial ratios and other financial performance measures that are

used during a venture’s successful life cycle. Who are the users of financial performance

measures?

Refer to Figure 5.1.

Development and Startup Stages:

Financial Ratios and Measures:

Chapter 5: Evaluating Operating and Financial Performance

73

3. What are financial ratios and why are they useful?

4. What are the three types of comparisons that can be made when conducting ratio analyses?

The three types of comparison that can be made with ratio analysis are trend analysis, cross-

sectional analysis, and industry comparables (benchmark) analysis.

5. What are the meanings of the terms “cash build” and “cash burn”? How do we calculate

net cash burn rates?

Cash build is the amount the firm receives on its sales calculated by net sales less the change

6. How is the current ratio calculated and what does it measure? How does the quick ratio

differ from the current ratio?

7. Describe how a firm’s net working capital (NWC) is measured and how the NWC–to-total-

assets ratio is calculated. What does this ratio measure?

8. What is the meaning of leverage ratios? What are typical ratios used for relating total debt

to a venture’s assets and/or its equity?

Leverage ratios indicate the extent to which the venture is in debt and its ability to repay its

9. What is the importance of the relationship between a venture’s current liabilities and its total

debt?

The portion of total debt that is “current” represents those liabilities that will come due

Chapter 5: Evaluating Operating and Financial Performance

74

10. Describe the two types of “coverage” ratios that are typically calculated when trying to

assess a venture’s ability to meet its interest payments and other financing-related

obligations?

The two types of coverage ratios used are the interest coverage ratio and the fixed charges

11. What are four measures used to indicate how efficiently the venture is in generating profits

on its sales? Describe how each measure is calculated.

The four ratios used are gross profit margin, operating profit margin, net profit margin, and

12. Identify and describe four efficiency/return ratios that combine data from both the income

statement and the balance sheet.

The four ratios are sales-to-total-assets, operating return on assets, return on assets, and

13. Identify and describe the two components of the ROA model both in terms of what financial

dimensions they measure and how they are calculated.

The two components of the ROA model are the net profit margin and the sales-to-total-assets

14. What are the three ratio components of the ROE model? How is each calculated and what

financial dimensions do they measure?

Chapter 5: Evaluating Operating and Financial Performance

75

The three ratio components of the ROE model are the net profit margin (net profit/sales),

15. Indicate some of the concerns or cautions that need to be considered when conducting ratio

analysis.

When conducting ratio analysis, it is important to compare “apples to apples” by consistent

use of the same inputs to the ratios (e.g. annual sales or quarterly sales). It is also important

16. From the Headlines – bext360: Discuss the variable and fixed costs in a single installation

and continuing operation of a “bextmachine.” What are the critical factors in getting to

“breakeven?”

Answers will vary: “For a given installation, the main fixed costs are the bextmachine’s cost

and its related installation costs. Additionally, there are fixed and variable costs of

INTERNET ACTIVITIES

A. Obtain the most recent three years of income statements and balance sheets. Analyze the

changes in operating and financial performance, if any, by applying the ratio analyses

covered in the chapter.

Web-researched results vary due to constant updating of the related web sites.

Chapter 5: Evaluating Operating and Financial Performance

76

B. Identify the industry that the firm being studied resides in and the major competitors.

EXERCISES/PROBLEMS AND ANSWERS

Note: for readers who were introduced to financial statements for the first time in Chapter 4, you

may want to first work the “Supplemental Exercises/Problems” presented at the end of Chapters

1, 2, and 3 which were intended for readers who had a previous understanding of financial

statements.

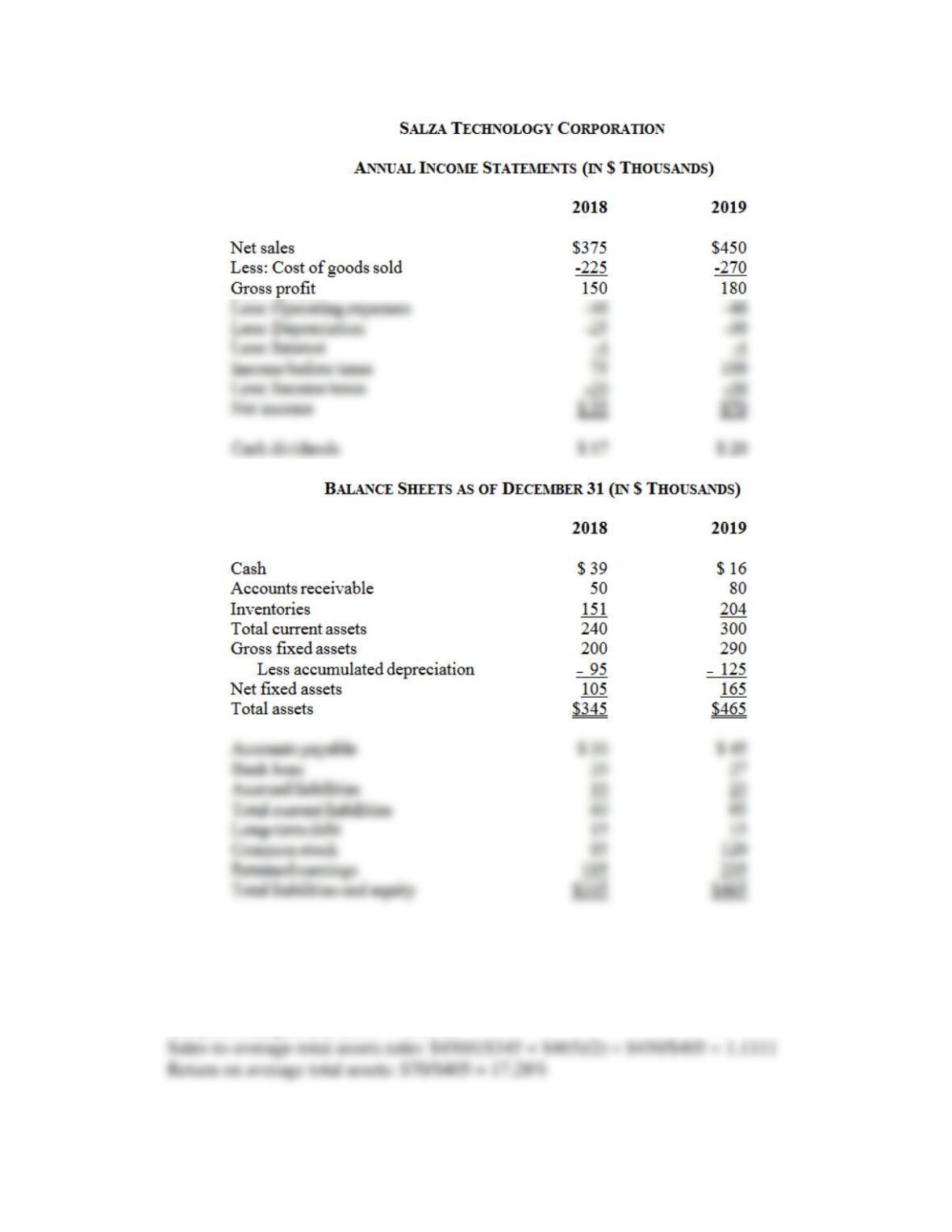

1. [ROA and ROE models and Ratio Components] The Salza Technology Corporation

Chapter 5: Evaluating Operating and Financial Performance

77

A. Calculate the net profit margin and the sales-to-total assets ratio for Salza for 2019 using

average total assets. Also calculate the return on total assets in 2019 using average total

assets.

Net profit margin: $70/$450 = 15.56%

Chapter 5: Evaluating Operating and Financial Performance

78

B. Calculate the ratios in the ROA model for both 2018 and 2019 using year-end total assets.

Comment on any financial ratio differences.

ROA model = Net income/Net sales x Net sales/Total assets = Net income/Total assets

2018: $55/$375 x $375/$345 = 14.67% x 1.0870 = 15.94%

C. Expand the 2019 ROA model discussed in Part A into an ROE model that includes

financial leverage as measured by the equity multiplier. Use average owners’ or

stockholders’ equity in your calculation.

ROE model = Net income/Net sales x Net sales/Average total assets x Average total

assets/Average stockholders’ equity = Net income/Average stockholders’ equity

Where: Average equity multiplier = Average total assets/Average stockholders’ equity

D. Expand the 2018 and 2019 ROA model calculations in Part B into ROE models based on

year-end owners’ or stockholders’ equity amounts.

ROA model from Part B:

2018: $55/$375 x $375/$345 = 14.67% x 1.0870 = 15.94%

2019: $70/$450 x $450/$465 = 15.56% x 0.9677 = 15.05%

2. [Liquidity and Financial Leverage Ratios] Refer to the Salza Technology Corporation in

Problem 1.

Chapter 5: Evaluating Operating and Financial Performance

79

A. Using average balance sheet account data, calculate the (a) current ratio, (b) quick ratio,

(c) total-debt-to-total-assets ratio, and (d) the interest coverage ratio for 2019.

Using average account balances:

(a) Current ratio: Average current assets/Average current liabilities

= (($240 + $300)/2) + (($60 + $95)/2) = $270/$77.50 = 3.48 times

(d) Interest coverage ratio: Average EBITDA/Average interest

EBITDA = Net sales – Cost of goods sold – Operating expenses

2018: $375 – $225 – $46 = $104

2019: $450 – $270 – $46 = $134

B. Repeat the ratio calculations requested in Part A separately for 2018 and 2019 using

year-end balance sheet account data. What changes, if any, have occurred in terms of

liquidity and financial leverage?

(a) Current ratio:

2018: $240/$60 = 4.00 times

2019: $300/$95 = 3.16 times

The current ratio declined but still exceeded 3.0 times in 2019.

Chapter 5: Evaluating Operating and Financial Performance

80

(d) Interest coverage ratio:

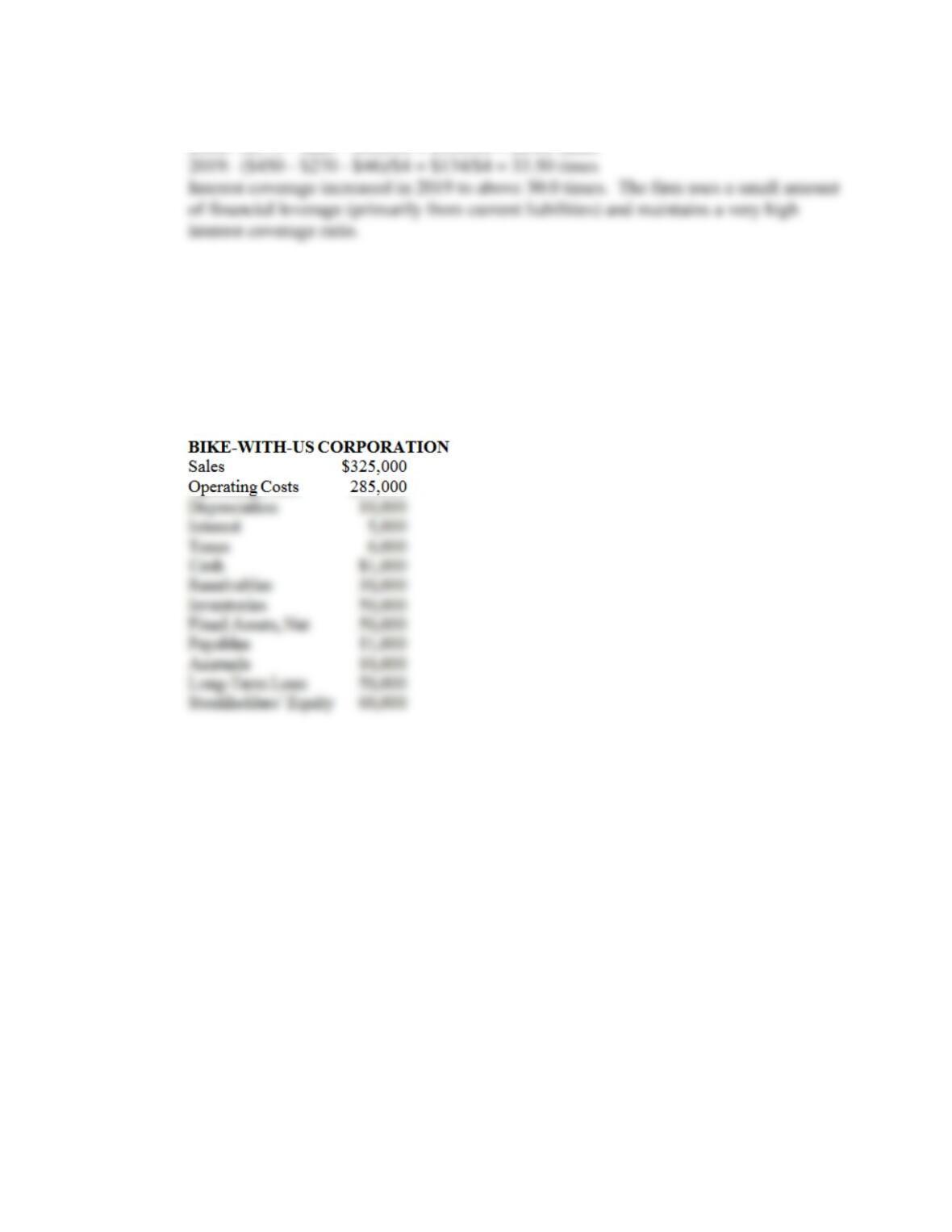

3. [Financial Statements and Ratios] Bike-With-Us Corporation, a specialty bicycle parts

replacement venture, was started last year by two former professional bicycle riders who had

substantial competitive racing experience including competing in the Tour de France. The

two entrepreneurs borrowed $50,000 from members of their families and each put up

$30,000 in equity capital. Retail space was rented and $60,000 was spent for fixtures and

store equipment. Following are the abbreviated income statement and balance sheet

information for the Bike-With-Us Corporation after one complete year of operation.

Chapter 5: Evaluating Operating and Financial Performance

81

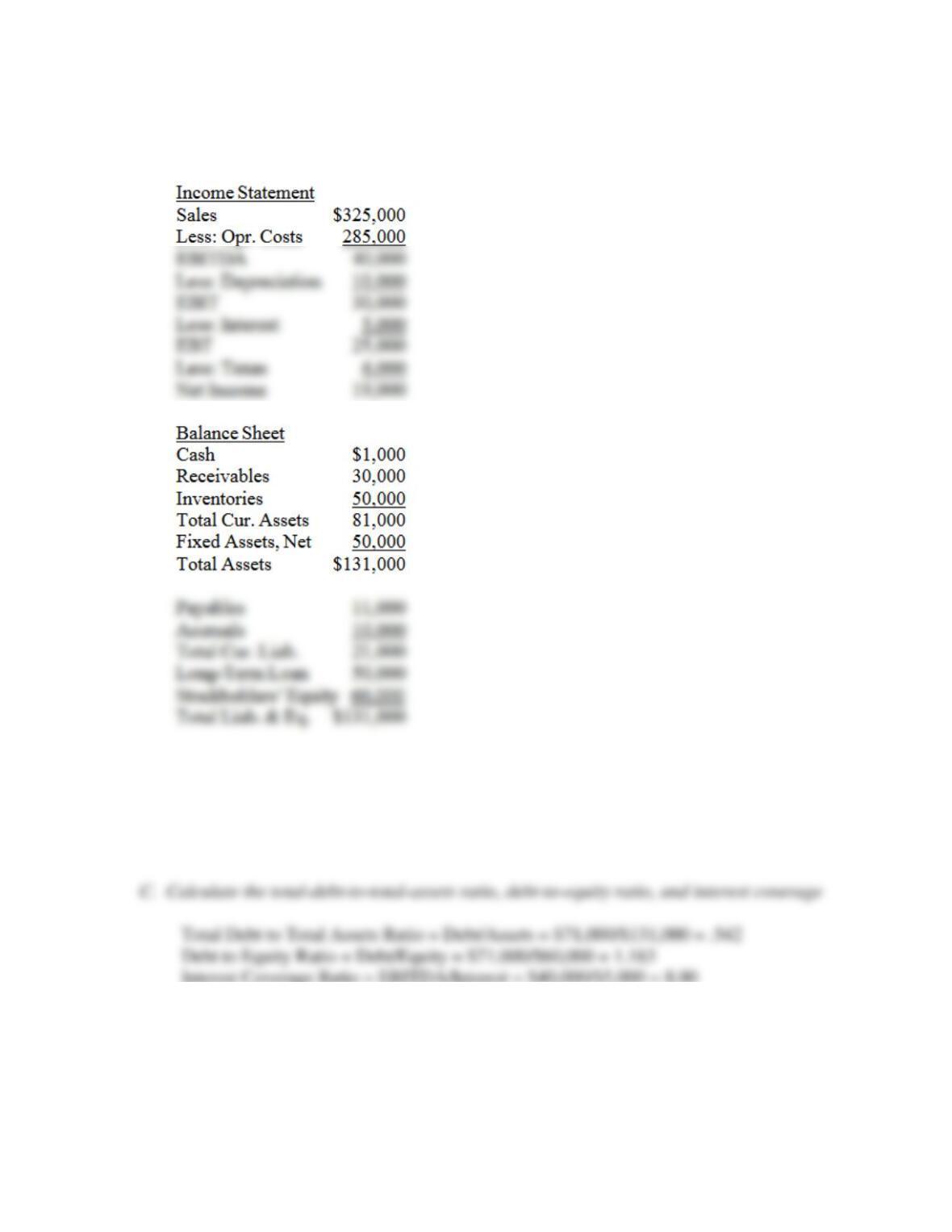

A. Prepare an income statement and a balance sheet for the Bike-With-Us Corporation

using only the information provided above.

B. Calculate the current ratio, quick ratio, and NWC-to-total-assets ratio.

Current Ratio = Current Assets/Current Liabilities = $81,000/$21,000 = 3.86

Quick Ratio = (CA – Inventories)/CL = ($81,000 – $50,000)/$21,000 = 1.48

NWC to Total Assets Ratio = (CA – CL)/Assets = ($81,000 – $21,000)/$131,000 = .458

Interest Coverage Ratio = EBITDA/Interest = $40,000/$5,000 = 8.00

D. Calculate the net profit margin, sales-to-total-assets ratio, and the return on total assets.

Net Profit Margin = Net Profit/Revenues = $19,000/$325,000 = 5.85%

Sales to Total Assets Ratio = Sales/Assets = $325,000/$131,000 = 2.48

Return on Total Assets = Net Profit/Assets = $19,000/$131,000 = 14.50%

Chapter 5: Evaluating Operating and Financial Performance

82

4. [Financial Ratios] Use the financial statements data for the Bike-With-Us Corporation

provided in Problem 3 to make the following calculations.

B. Determine the effective interest rate paid on the long-term debt.

Effective interest rate = Interest/Long-term debt = $5,000/$50,000 = 10.00%

C. Calculate the NOPAT margin. How does this compare with the results for the net profit

margin? Did the owners benefit from the use of interest-bearing long-term debt?

Tax Rate = Taxes/EBT = $6,000/$25,000 = 24.00%

Chapter 5: Evaluating Operating and Financial Performance

83

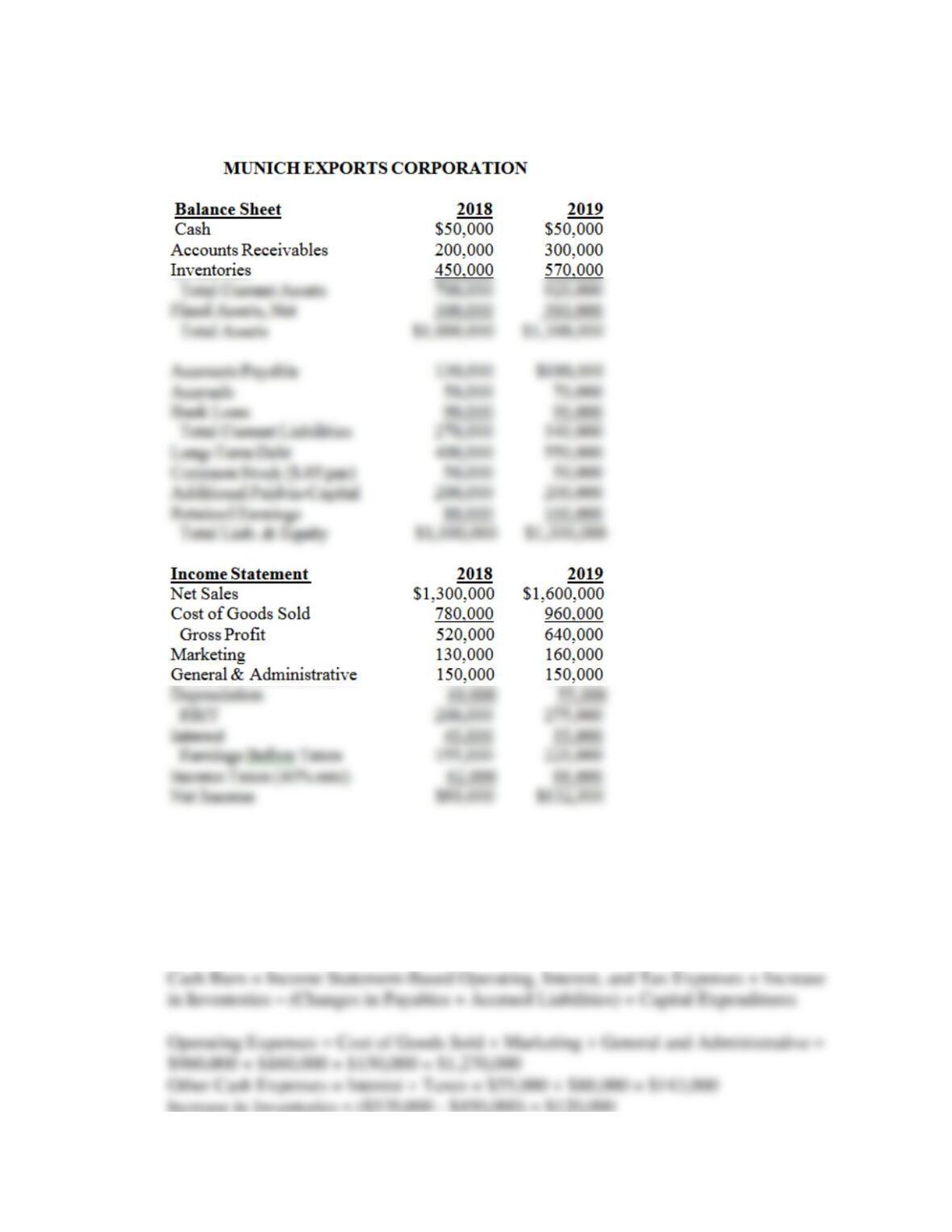

5. [Cash Burn and Build] Following are two years of income statements and balance sheets for

the Munich Exports Corporation.

A. Calculate the cash build, cash burn, and net cash burn or build for Munich Exports in

2019.

Cash Build = Net Sales – Increase in Receivables = $1,600,000 – ($300,000 – $200,000)

= $1,500,000