56

Chapter 4

PREPARING AND USING FINANCIAL STATEMENTS

FOCUS

In this chapter, we introduce basic accounting and financial statements designed to help ventures

monitor their progress. We stress the need to understand how cash is built and burned both in

terms of financial statements and through operating breakeven analyses.

LEARNING OBJECTIVES

LO 4.1: Describe the process for obtaining and recording resources needed for an early-stage

venture.

LO 4.2: Describe and prepare a basic balance sheet.

LO 4.3: Describe and prepare a basic income statement.

CHAPTER OUTLINE

4.1 OBTAINING AND RECORDING THE RESOURCES NECESSARY TO START AND

BUILD A NEW VENTURE

4.2 BUSINESS ASSETS, LIABILITIES, AND OWNERS’ EQUITY

4.3 SALES, EXPENSES, AND PROFITS

4.4 INTERNAL OPERATING SCHEDULES

4.5 STATEMENT OF CASH FLOWS

4.6 OPERATING BREAKEVEN ANALYSES

A. Survival Breakeven

DISCUSSION QUESTIONS AND ANSWERS

Chapter 4: Preparing and Using Financial Statements

57

1. Describe the types of resources (assets) needed for a new product venture during its

development and startup stages. Comment on the likely revenues and expenses during these

early life cycle stages.

Refer to: Figure 4.1 Obtaining and Recording the Resources Necessary to Start and Build a

New Venture

2. What is accrual accounting? What are generally accepted accounting principles (GAAP)?

Accrual accounting is the practice of recording economic activity when it is recognized

rather than waiting until it is realized.

3. What is meant by the statement that a balance sheet provides a “snapshot” of a venture’s

financial position as of a point in time? Why must a balance sheet be in “balance?”

4. Briefly describe the typical types of accounts that are found in the current assets of a new

venture.

5. What is meant by the terms “depreciation” and “accumulated depreciation”?

Chapter 4: Preparing and Using Financial Statements

58

6. What types of liabilities might show up on a venture’s balance sheet?

Liabilities might include: payables, accrued wages, bank loan, other current liabilities, long–

7. What does an income statement measure or track over time?

The income statement is a performance measure of a firm’s operations over a period of time.

8. Define the term “EBIT.” How does EBIT differ from a firm’s net income or net profit?

EBIT is defined as the earnings of a company before accounting for any interest

9. What are the three internal operating schedules that most firms must prepare?

10. Briefly describe what is meant by a statement of cash flows.

A statement of cash flows shows how cash, as reflected in accrual accounting, flowed into

11. What is meant by net cash build and net cash burn?

Net Cash Build: exists when the sum of cash flows from operations and investing is positive

12. Describe the differences between variable expenses and fixed expenses.

Variable expenses depend upon the level of production while fixed expenses are items that

13. Define the term EBITDA.

The acronym EBITDA stands for earnings before interest, taxes, depreciation, and

amortization.

14. What is a venture’s contribution profit margin?

Chapter 4: Preparing and Using Financial Statements

59

15. Define the term EBDAT.

EBDAT is a firm’s earnings before taxes, depreciation and amortization.

16. Describe the meaning of EBDAT breakeven and survival revenues.

17. Describe and illustrate how an EBDAT (survival) breakeven chart is constructed.

Refer to Figure 4.2. Costs and revenues are plotted on the vertical axis and revenues (in

18. What is meant by breakeven drivers? Identify two important drivers affecting the amount of

revenues needed for ventures to break even.

Breakeven drivers are key elements of the firm’s financial statements that affect breakeven.

19. From the Headlines — “Competing to Let the Light Shine”: Describe three financial

performance measures that d.light’s venture investors might use to examine whether d.light

is measuring up financially as it achieves its “lives touched” goals.

Answers will vary widely: Margins (revenues vs. costs) will be critical in providing the

INTERNET ACTIVITIES

1. A number of Web sites are available to help young ventures to measure their financial

performance and to help them when they are growing and “ramping up” revenues. Access

Chapter 4: Preparing and Using Financial Statements

60

SBA provided information can be compared and integrated with the materials presented in

this chapter.

Web-researched results vary due to constant updating of the related web sites.

EXERCISES/PROBLEMS

1. [Stockholders’ equity] The owners of a new venture have decided to organize as a

corporation. The initial equity investment is valued at $100,000 reflecting contributions of

the entrepreneur and her family and friends. One hundred thousand shares of stock were

initially issued.

A. What dollar amount would initially be recorded in the common stock account?

Common stock (initial investment) $100,000

C. Now assume that 20,000 additional shares of stock are sold to an angel investor at $5 per

share six months after the initial incorporation. Show how your answer in Part A would

change if the common stock did not have a par value. Also show how your answer in

Part B would change given a par value of $.01 per share.

Chapter 4: Preparing and Using Financial Statements

61

D. At the end of the first year of operation, the venture recorded an operating loss of

$80,000. Show the dollar amounts in the common stock account, the additional paid–in–

capital account, and the retained earnings account at the end of one year. Also indicate

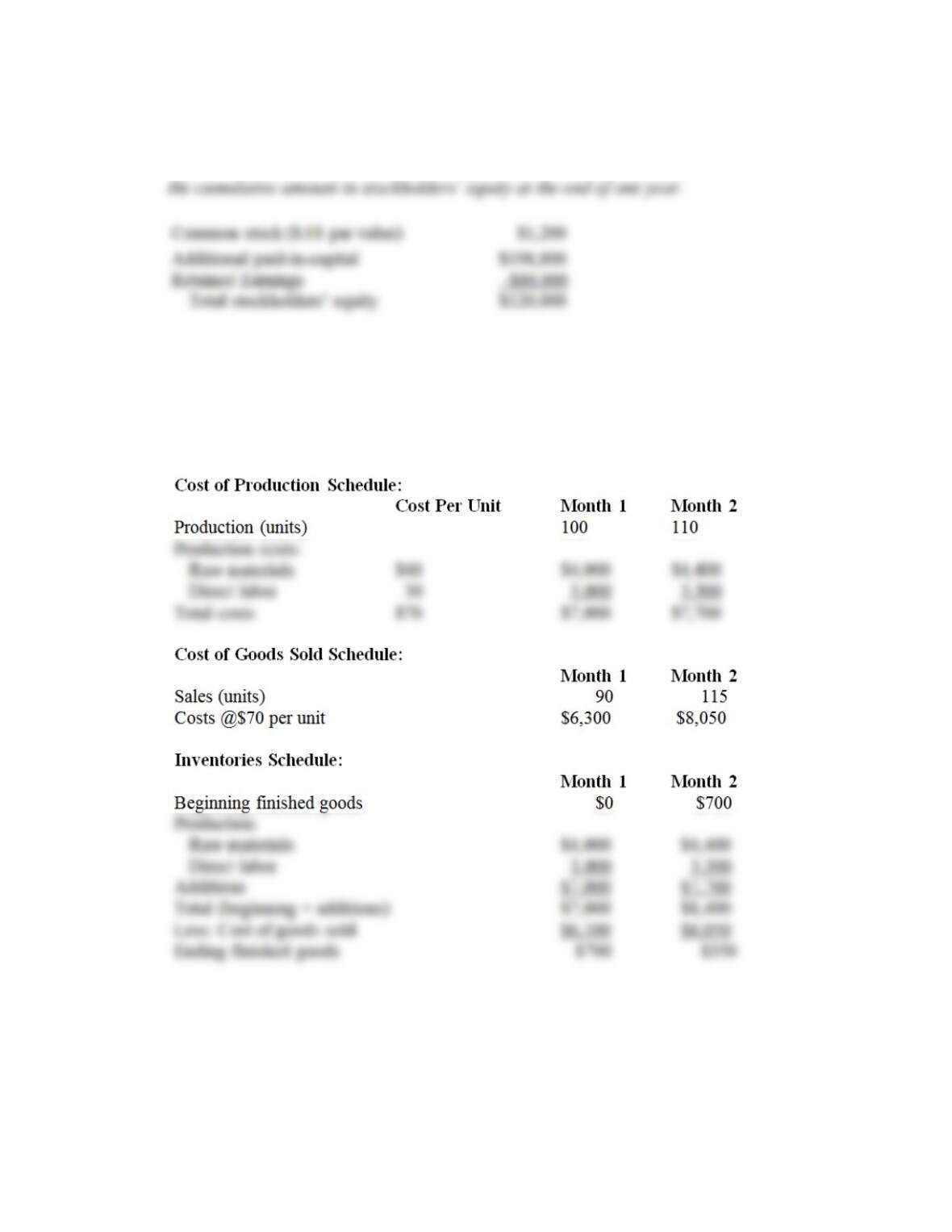

2. [Internal Operating Schedules] Assume you are starting a new business involving the

manufacture and sale of a new product. Raw materials costs are $40 per product. Direct

labor costs are expected to be $30 per product. You expect to sell each product for $110.

You plan to produce 100 products next month and expect to sell 90 products.

A. Prepare cost of production, cost of goods sold, and inventories schedules for next (the

first) month.

B. During the second month, you plan to produce 110 products but expect sales in the month

to be 115 products. Prepare cost of production, cost of goods sold, and inventories

schedules for the second month.

Note: the solutions for Part B are shown in Part A for Month 2.

Chapter 4: Preparing and Using Financial Statements

62

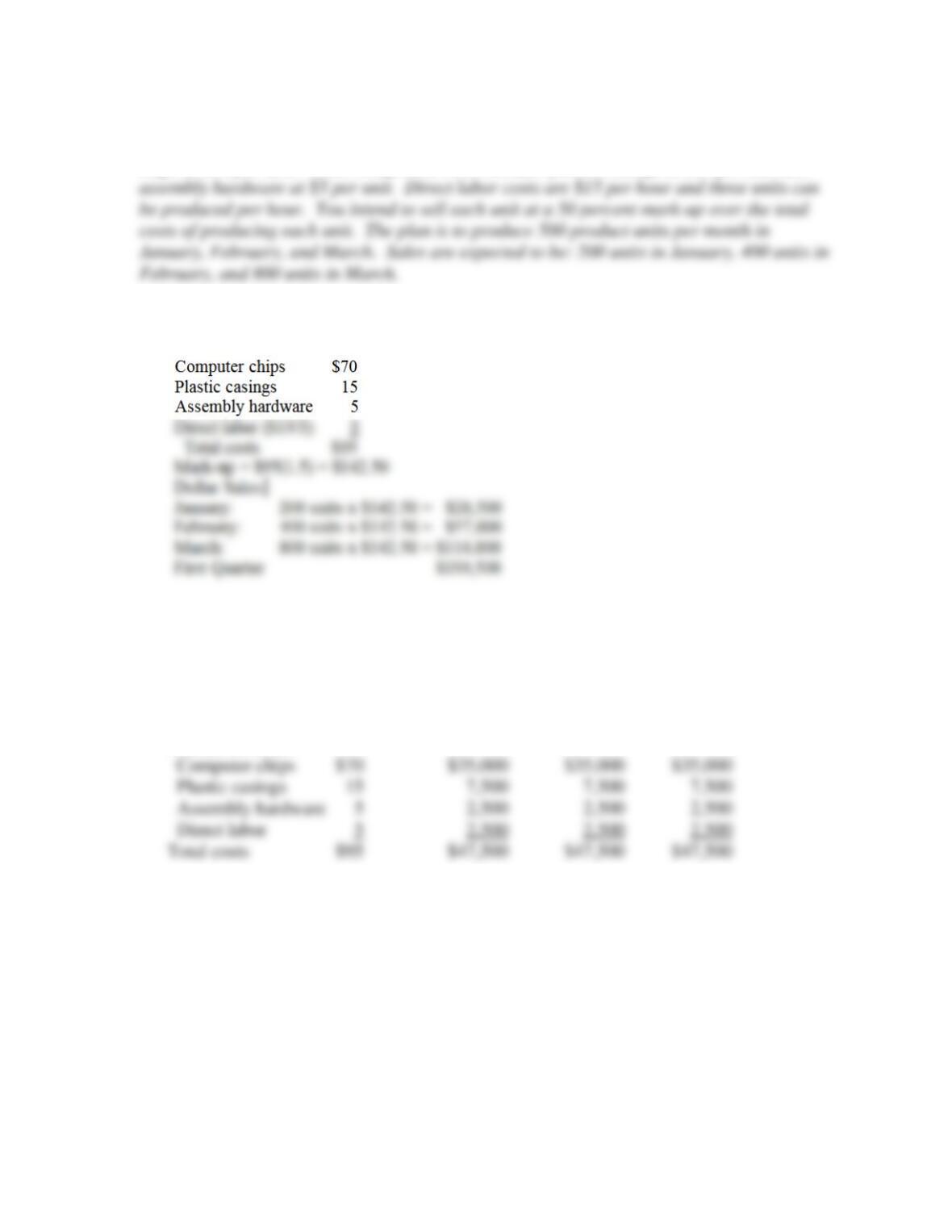

3. [Internal Operating Schedules] Assume you have developed and tested a prototype electronic

product and are about to start your new business. You purchase pre-programmed computer

chips at $70 per unit. Other component costs include: plastic casings at $15 per unit and

A. Calculate the dollar amount of sales revenue expected in each month (i.e., January,

February, and March) and for the first quarter of the year.

B. Prepare a cost of production schedule for January, February, and March.

Cost of Production Schedule:

Cost

Per Unit January February March

Production (units) 500 500 500

Production costs

C. Prepare a cost of goods sold schedule for each of the three months and for the first quarter

of the year. Using your cost of goods sold estimates and the sales revenues expected in Part

A, calculate the gross earnings for January, February, and March, as well as for the first

quarter of the year.

Cost of Goods Sold Schedule:

January February March Total

Sales (units) 200 400 800 1,400

Costs @ $95/unit $19,000 $38,000 $76,000 $133,000

Chapter 4: Preparing and Using Financial Statements

63

Gross Earnings Estimate:

D. Prepare an inventories schedule for January, February, and March.

Inventories Schedule:

January February March

Beginning finished goods $0 $28,500 $38,000

Production

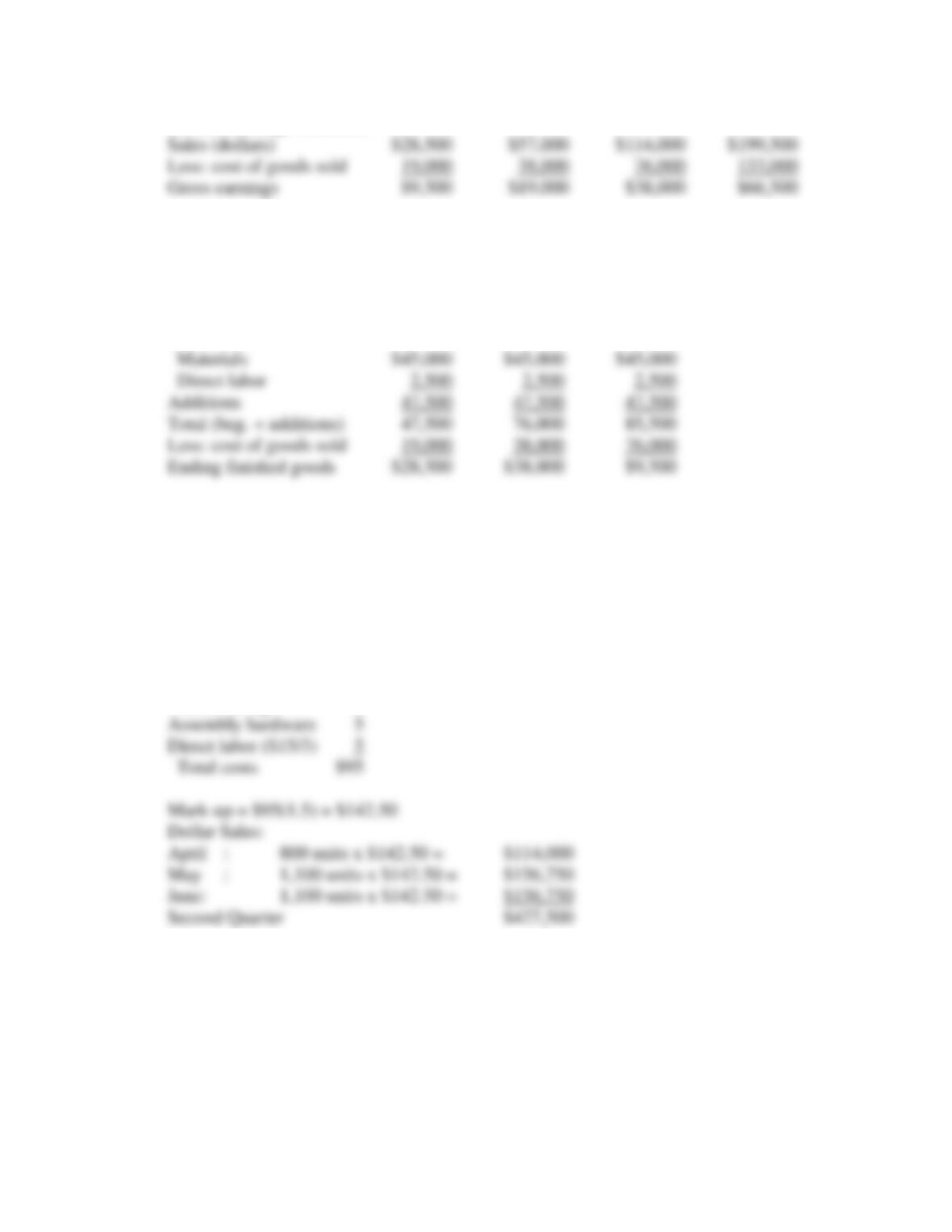

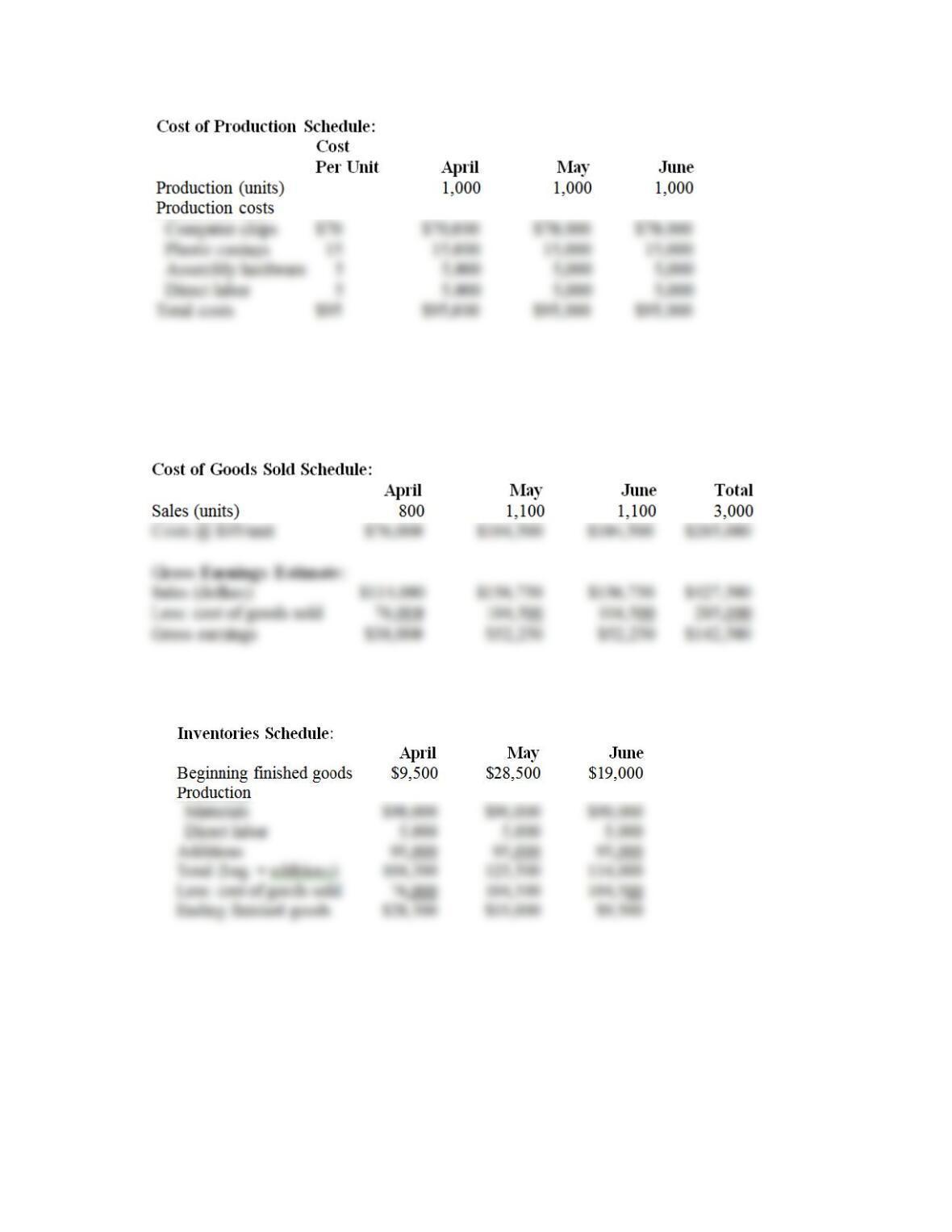

4. [Internal Operating Schedules] This problem is a continuation of Problem 3. Assume you

ramp up production to 1,000 units per month in April, May, and June. Sales are expected

to be 800 units in April and 1,100 units in each of May and June. Repeat the calculations

requested in Problem 3 for the second quarter of the year (April, May, and June).

A. Calculate the dollar amount of sales revenue expected in each month (i.e., April, May, and

June) and for the second quarter of the year.

Computer chips $70

Plastic casings 15

B. Prepare a cost of production schedule for April, May, and June.

Chapter 4: Preparing and Using Financial Statements

64

C. Prepare a cost of goods sold schedule for each of the three months and for the second

quarter of the year. Using your cost of goods sold estimates and the sales revenues

expected in Part A, calculate the gross earnings for April, May, and June, as well as for the

second quarter of the year.

D. Prepare an inventories schedule for April, May, and June.

Chapter 4: Preparing and Using Financial Statements

65

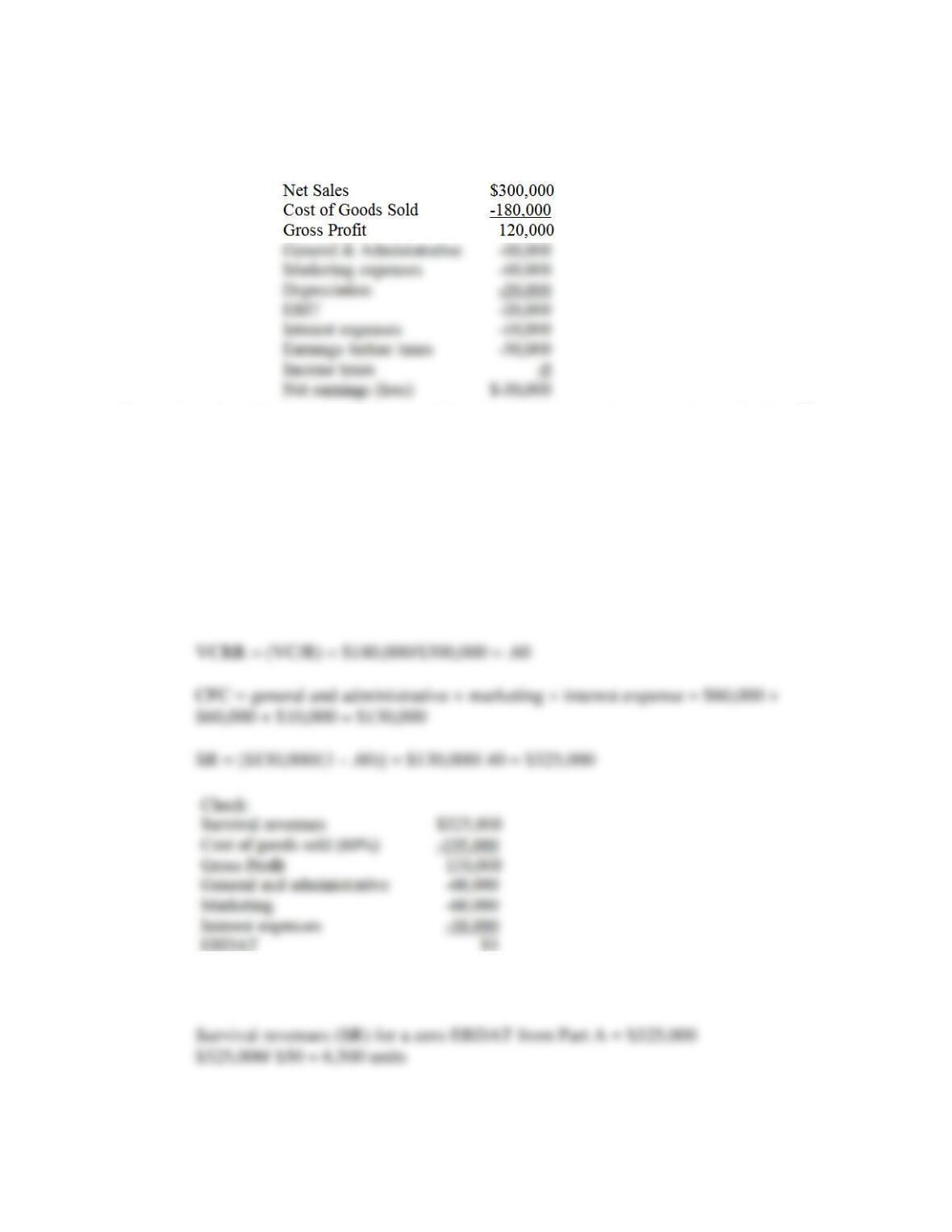

5. [Survival Revenues Breakeven] During its first year of operations, the SubRay Corporation

produced the following income statement results:

Costs of goods sold are expected to vary with sales and be a constant percentage of sales. The

general and administrative employees have been hired and are expected to remain a fixed cost.

Marketing expenses are also expected to remain fixed since the current sales staff members are

expected to remain on fixed salaries and no new hires are planned. The effective tax rate is

expected to be 30 percent for a profitable firm.

A. Estimate the survival or EBDAT breakeven amount in terms of survival revenues necessary

for the SubRay Corporation to breakeven next year.

Survival revenues (SR), when EBDAT = 0, are calculated as:

B. Assume that the product selling price is $50 per unit. Calculate the EBDAT breakeven

point in terms of the number of units that will have to be sold next year.

Chapter 4: Preparing and Using Financial Statements

66

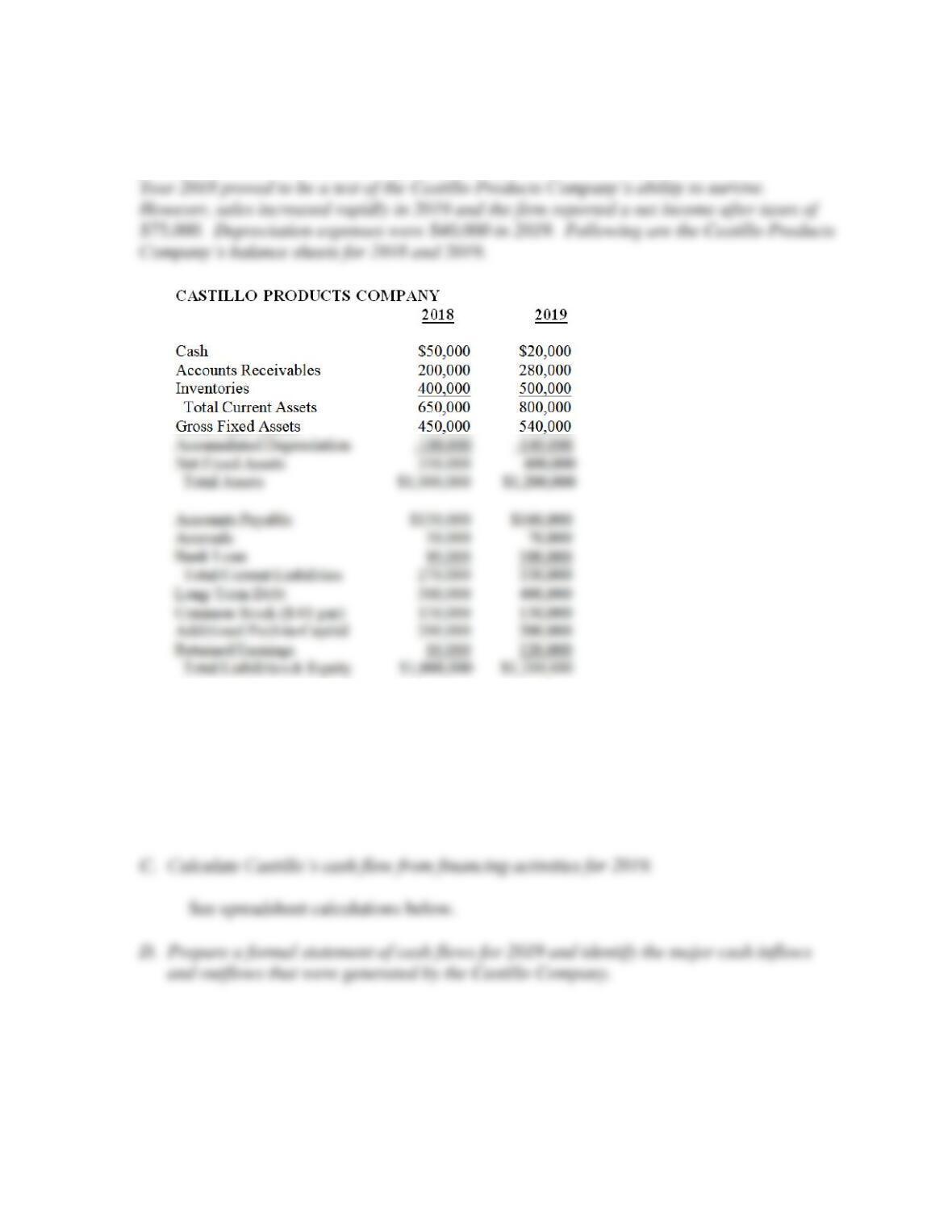

6. [Statement of Cash Flows and Cash Burn or Build] Cindy and Robert (Rob) Castillo founded

the Castillo Products Company in 2018. The company manufactures components for

personal decision assistant (PDA) products and for other hand-held electronic products.

A. Calculate Castillo’s cash flow from operating activities for 2019.

See spreadsheet calculations below.

B. Calculate Castillo’s cash flow from investing activities for 2019.

See spreadsheet calculations below.

See spreadsheet calculations below.

E. Use your calculation results from Parts A and B above to determine whether Castillo was

building or burning cash during 2019 and indicate the dollar amount of the cash build or

burn.