Capstone Case 1: Eco-Products, Inc.

2008 forecast of $45 million was associated with a decline in economic activity

(recession), increased competition, and a supply chain problem that made it difficult to

first avoid stocking out of inventory and then accumulating excess inventory. By the end

of 2008, inventory had increased to more than $12 million compared to $2.4 million at

the end of 2007.

J. Explain Eco-Products’ supply chain model that existed in early 2008. Describe the

strengths and weaknesses of such a model from an operations viewpoint. What are the

implications of this supply chain model on Eco-Products working capital financing needs

and its cash conversion cycle?

The supply chain model used by Eco-Products resulted in a long inventory cycle (for a

relatively simple production process). Raw materials were often purchased in the U.S. or

from suppliers in other countries, shipped to manufacturers in Asia, with the final

products being shipped back for sale in the U.S. This long inventory cycle tied up cash

and made it difficult to stock adequate inventory in some time periods, or produce excess

inventory at other times. A long supply chain cycle involves larger asset financing

requirements, particularly in the form of inventory.

Actual 2008 Results:

2008 Total Assets/Sales = 18,903,838/34,378,138 = .5499 = 55.0%

2008 Inventory/Sales = 12,222,801/34,378,138 = .3555 = 35.6%

CCC Calculations:

Capstone Case 1: Eco-Products, Inc.

Purchase-to-Payment Conversion Period (Pmt. CP):

2005 Pmt. CP = 123,429/(2,584,326/365) = 123,429/7,080.4 = 17.4 days

2006 Pmt. CP = 526,555/(3,684,492/365) = 526,555/10,094.5 = 52.2 days

2007 Pmt. CP = 568,131/(7,726,455/365) = 568,131/21,168.4 = 26.8 days

For reference, the actual CCC calculations for 2008 were as follows:

2008 Inv. CP = 12,222,801/(26,041,166/365) = 12,222,801/71,345.7 = 171.3 days

2008 Rec. CP = 3,109,920/(34,378,138/365) = 3,109,920/94,186.7 = 33.0 days

This further increase in the CCC meant that even more financing was required to support

the actual 2008 sales.

An accompanying Excel spreadsheet provides the following ratio calculations for

2007 and 2008 (data not available until 2009).

Cash Conversion Cycle (in Days): 2007 2008

Inventory-to-Sale Conversion Period 114.1 171.3

Capstone Case 1: Eco-Products, Inc.

K. In mid-2008, Eco-Products management sought to quickly (hopefully) raise an additional

$2 million in external financing through a single private equity investment. The term

sheet prepared by Greenmont Capital is presented in Appendix B.

1. After considering a number of possible private equity investors, Greenmont Capital

was selected by Eco-Products’ management. Discuss the pros and cons of selecting a

small locally-based private equity firm relative to a larger private equity investor?

Large private equity firms have large amounts of funds to invest and will have a

portfolio of several projects being simultaneously financed. Large private equity firms

also usually can move quickly in providing funds to specific ventures and are likely to

2. Review the investment terms presented in Appendix B and comment on any factors in

the term sheet that might be “deal breakers.” If you were representing Eco-Products

top management, which terms might you want deleted or modified from the term

sheet? Now, if you were representing Greenmont Capital, which terms would be

important in protecting its investment capital?

It might be helpful to first review Chapter 11, Figure 11.6 which provides a list of

“Typical Issues Addressed in a Term Sheet.’

A term sheet should summarize the proposed principal terms with respect to a specific

Capstone Case 1: Eco-Products, Inc.

A possible “deal breaker” would be the number of warrants being offered to

Greenmont Partners in the term sheet proposal. The July 18, 2008 term sheet

proposal provides for Greenmont to receive 1.5 million shares of Series A

Convertible Preferred Stock initially convertible on a 1:1 basis into shares of Eco–

Products common stock. The term sheet proposal also provides for a 25% warrant

coverage (i.e., warrants to purchase additional Series A Preferred Shares at an

3. Some analysts employ a relative value method that uses multiples from comparable

firms to estimate the value of a target venture. Exhibit 9 contains enterprise value-to–

sales information for a number of possible comparable firms for the purpose of

valuing Eco-Products. Estimate the enterprise value of Eco-Products. What portion

of equity ownership should Eco- Products be willing to give up for the $2 million

Greenmont Capital investment?

Although Eco-Products had been in business since 1990, its business model changed

between 2005 and 2007. Eco-Products became a manufacturer and wholesaler of

eco-friendly products at a time when oil prices were at record highs and concern

Capstone Case 1: Eco-Products, Inc.

As discussed in the text, ventures may be valued using a discounted cash flow (DCF)

method (see Chapters 9 and 13), a venture capitalist (VC) short-cut method (see

Chapter 10), or a relative valuation method (see Chapter 14). Analysts often attempt

to value a firm on the basis of its top line (sales), its rough cash flow (as reflected in

EBITDA), and/or its bottom line (net income).

Unfortunately, no information was available for EBITDA (except for the dated

Newspring transaction) or net income multiples.

As noted in the case, sales estimates changed rapidly in the case. Eco-Products

management in mid-2007 had forecasted 2008 sales to be $22 million. By early 2008,

A range of possible values for Eco-Products using an enterprise value to sales

multiple of 1.55 might be:

Sales or Rev. x Multiple = Value

12-Month Trailing Sales $19.7 million 1.55 $30.535 million

Management’s Forecast $45.0 million 1.55 $69.750 million

Actual 2008 Results $34.4 million 1.55 $53.320 million

Capstone Case 1: Eco-Products, Inc.

Note: As can be seen from the actual 2008 results, the lines of credit at the end of

2008 amounted to slightly more than $8 million, long-term debt (including the

current portion) was nearly $.5 million, and long-term capital leases (including the

current portion) was nearly $.3 million. Thus, the total interest-bearing debt plus

long-term capital leases amounted to approximately $8.8 million.

Or, using pre-money and post-money shares the calculations would be:

Pre-money shares (fully diluted to account for the employee option pool) =

$29,587,500/$1.50 = 19,725,000 shares

Shares issued to Greenmont = $2,000,000/$1.50 = 1,333,333

Post-money shares = 19,725,000 + 1,333,333 = 21,058,333

As noted in the following epilogue, Greenmont Partners negotiated a larger

percentage ownership as Eco-Products struggled to meet its revenue targets due to

inventory-related problems and the rapidly slowing economy during the last-half of

2008. According to the 2008 balance sheet, 1,366,666 shares of preferred stock were

actually issued to Greenmont, instead of the previously negotiated 1,333,333 shares

Capstone Case 1: Eco-Products, Inc.

EPILOGUE: What Happened

Finance deal. Steve Savage and Greenmont Capital Partners signed a $2 million Series A

investment round on July 1, 2008. Greenmont’s valuation was not the highest of those

Savage received, but it was close. Savage chose Greenmont over others because the

valuation was fair and provided the intangible benefits of a strategic partnership, and the

Greenmont team was beset with industry veterans. Greenmont’s terms sheet contained

Recession. Following the investment, Eco-Products struggled to meet revenue targets.

Prior to the Greenmont deal, Eco-Products had never been accountable to outside

investors for its performance and, at that time, introducing new products impeded

Recovery. Eco-Products overcame the decline in spending that most consumer good

companies and manufacturers experienced beginning in the fall of 2008. The 2008

financial statements are given in Exhibits 1 and 2.One year later Eco-Products’

“GreenStripe” product line was being sold through than 450 distributors and the company

planned to conduct another round of private equity financing, this time for $5 million to

operations. He stated:

This $5 million in financial capital is more than enough unless the core business

really takes off, or the new products lines really take off, or an attractive merger

Capstone Case 1: Eco-Products, Inc.

In August 2009, the company reported revenues had more than doubled over the last

three years and more than 54 new jobs had been created since 2006. As for its founder

and former president, Steve Savage remained interested in leading early stage ventures.

He became the majority owner of Ellie’s Eco Home Store, the former building division of

Following are the Eco-Products 2007 and 2008 financial statements that are

available in the accompanying Excel spreadsheet.

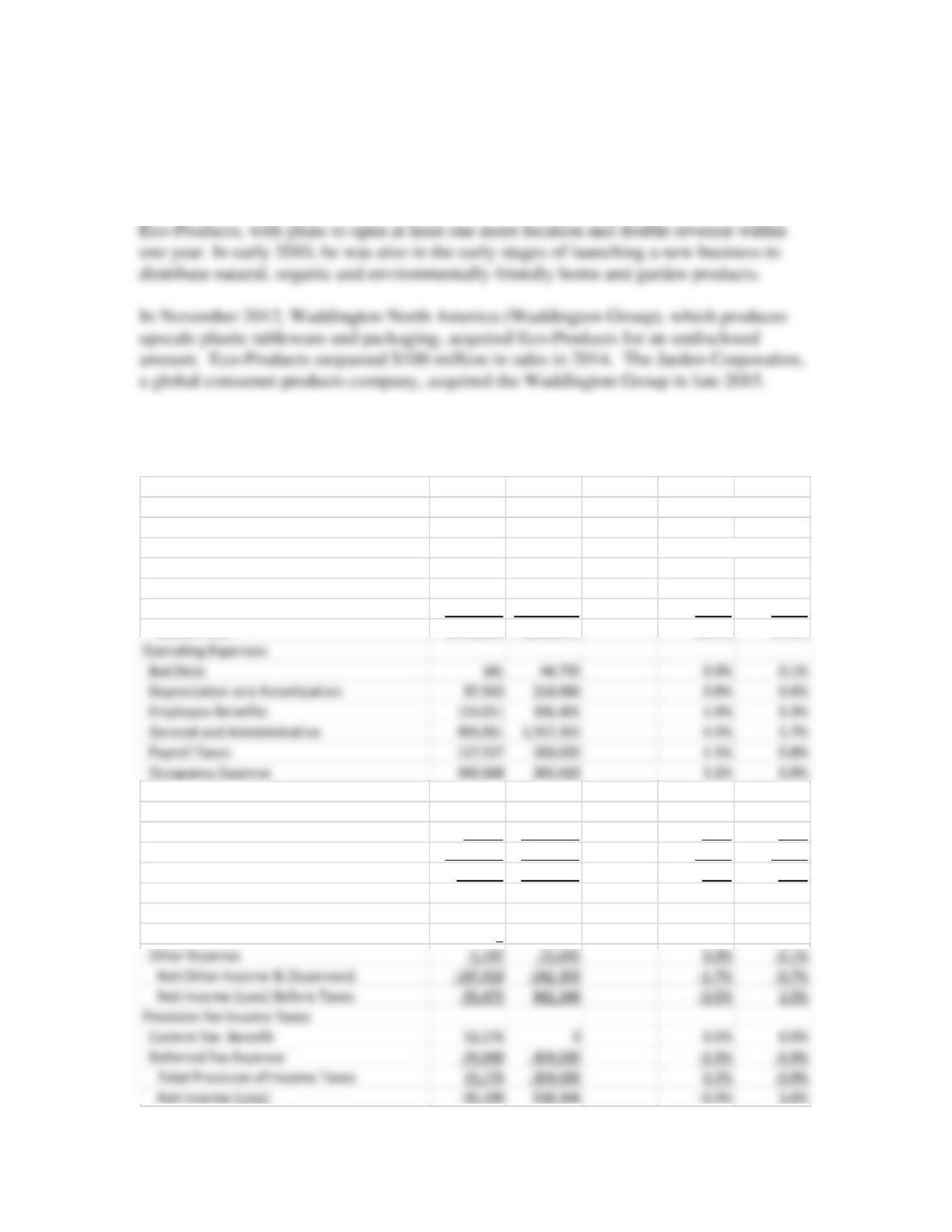

Eco-Products, Inc.

Financial Statements and Projections Common–Size

[In Dollars] Actual Actual Financial Statements

Yearend Yearend [Percent of Revenues]

Income Statements 2007 2008 2007 2008

Net Revenues 10,867,104 34,378,138 100.0% 100.0%

Cost of Goods Sold 7,726,455 26,041,166 71.1% 75.7%

Repairs and Maintenance 27,140 45,447 0.2% 0.1%

Salaries and Wages 1,778,282 3,216,385 16.4% 9.4%

Selling and Marketing Expenses 43,783 1,133,334 0.4% 3.3%

Total Operating Expenses 3,012,206 7,252,325 27.7% 21.1%

Operating Profit 128,443 1,084,647 1.2% 3.2%

Other Income and (Expenses)

Interest Expense –186,726 –253,242 –1.7% –0.7%

Other Income 0 35,984 0.0% 0.1%

Capstone Case 1: Eco-Products, Inc.

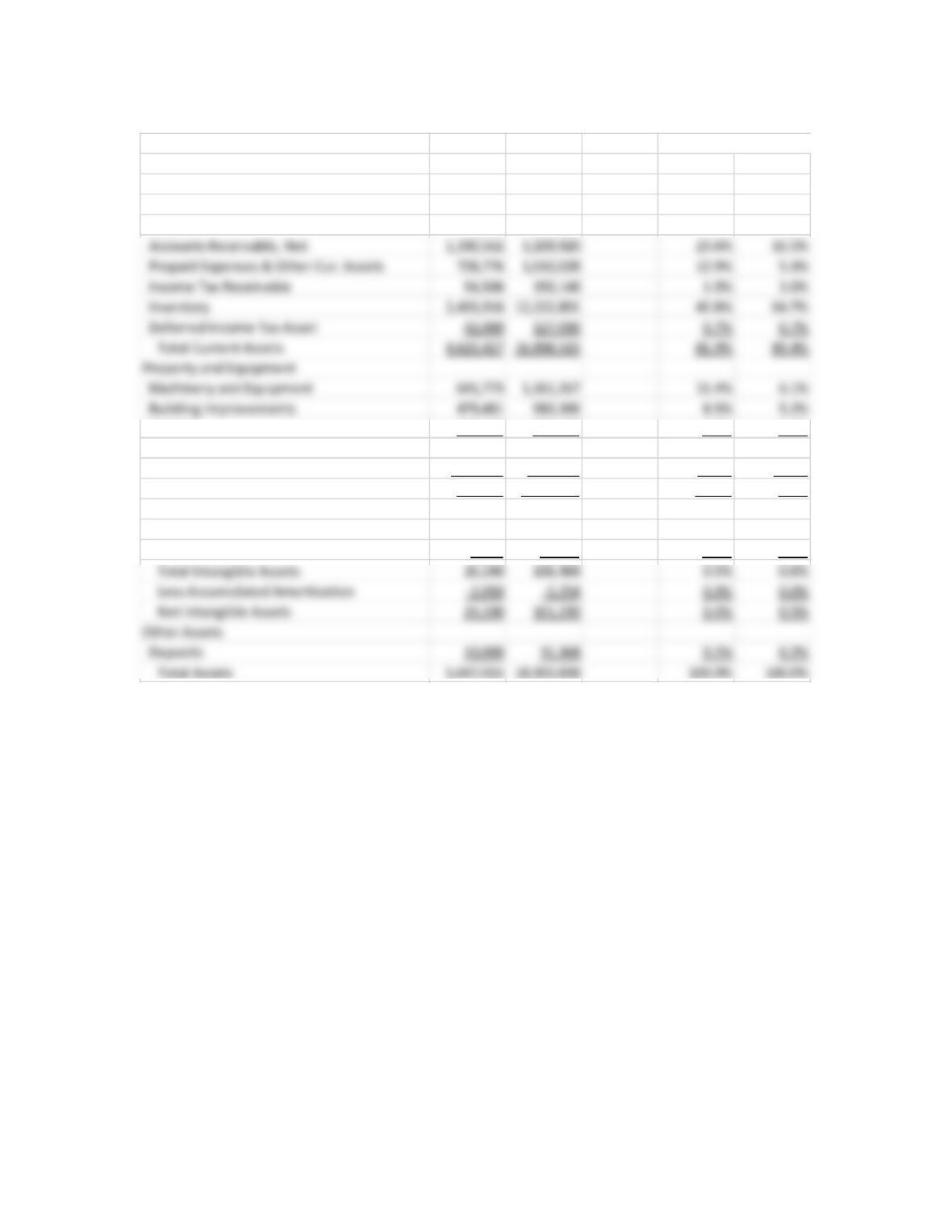

[Percent of Total Assets]

Balance Sheets 2007 2008 2007 2008

Assets

Current Assets

Cash 51,667 235,618 0.9% 1.2%

Vehicles 228,448 299,178 4.0% 1.6%

Total Property and Equipment 1,349,702 2,443,891 23.9% 12.9%

Less Accumulated Depreciation –360,304 –571,166 -6.4% –3.0%

Net Property and Equipment 989,398 1,872,725 17.5% 9.9%

Intangible Assets

Trademarks 20,800 21,564 0.4% 0.1%

Other Intangible Assets 5,440 84,920 0.1% 0.4%

Capstone Case 1: Eco-Products, Inc.

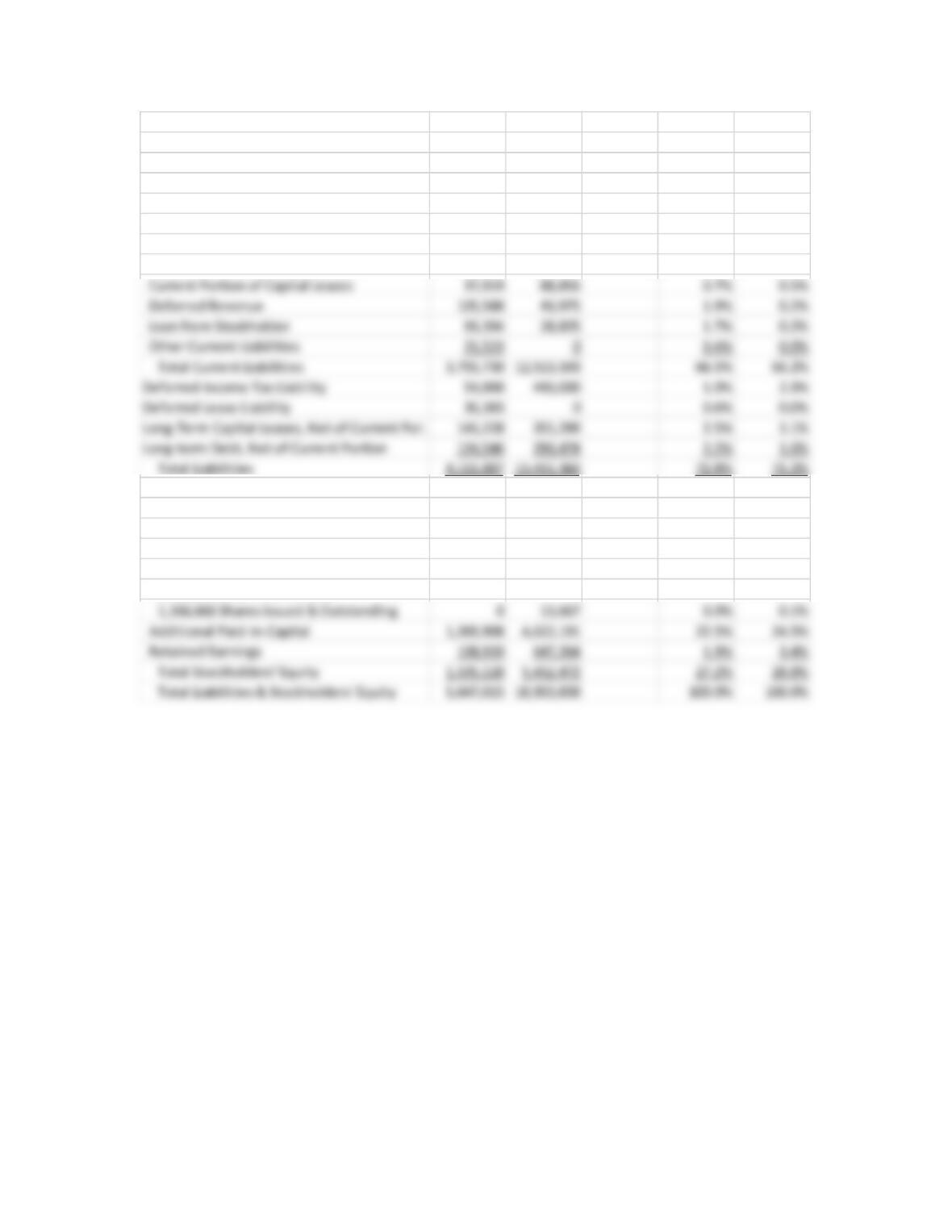

2007 2008 2007 2008

Liabilities and Equity

Current Liabilities

Accounts Payable & Accrued Expenses 568,131 3,804,210 10.1% 20.1%

Accrued Payroll & Payroll Taxes 6,712 253,094 0.1% 1.3%

Accrued Vacation 39,356 84,755 0.7% 0.4%

Lines of Credit 2,843,242 8,043,568 50.3% 42.5%

Current Portion of Long-Term Debt 39,865 166,310 0.7% 0.9%

Stockholders’ Equity

Common Stock, $.001 Par Value

50,000,000 Shares Authorized

16,935,000 Shares Issued & Outstanding 156,300 169,350 2.8% 0.9%

Preferred Stock, $.001 Par Value

1,750,000 Shares Authorized