Chapter 16

FINANCIALLY TROUBLED VENTURES:

TURNAROUND OPPORTUNITIES?

FOCUS

We direct attention in this chapter toward recognizing and managing financial distress.

An inability to pay creditor obligations as they come due typically poses a major financial

threat and certainly distracts the venture from its primary mission. A successful

entrepreneur copes with such financial distress and finds a way to turn the situation

around. The alternative to a successful turnaround is venture liquidation.

LEARNING OBJECTIVES

LO 16.1: Identify possible options available to struggling or troubled ventures.

LO 16.2: Define financial distress and explain how balance sheet insolvency and cash

flow insolvency differ.

CHAPTER OUTLINE

16.1VENTURE OPERATING AND FINANCING OVERVIEW

16.2 THE TROUBLED VENTURE AND FINANCIAL DISTRESS

16.3 RESOLVING FINANCIAL DISTRESS SITUATIONS

A. Operations Restructuring

16.4 PRIVATE WORKOUTS AND LIQUIDATIONS

A. Private Workouts

16.5 FEDERAL BANKRUPTCY LAW

SUMMARY

DISCUSSION QUESTIONS AND ANSWERS

1. What are the three types or methods of restructuring available when trying to turn

around financially troubled ventures?

The three basic types/methods are: (a) operations restructuring, (b) asset restructuring,

2. Identify major factors that cause ventures to get into financial trouble.

Ventures get into trouble by mishandling strategic issues, failing to unite management

on key initiatives, and having poor finance and accounting practices and controls.

3. What is meant by financial distress?

Financial distress refers to when cash flow is insufficient to meet current debt

obligations.

4. What is meant by loan default? Also, describe (a) an acceleration provision and (b) a

cross-default provision.

A loan default is when there is a failure to meet interest or principal payments when

5. What is foreclosure?

Foreclosure is a legal process used by creditors to try to collect amounts owed on

loans in default.

6. What do we mean when we say a venture is insolvent?

An insolvent venture is one where equity is negative and/or the cash flow of the firm

is unable to meet debt obligations.

7. Compare and contrast (a) balance sheet insolvency and (b) cash flow insolvency.

Balance sheet insolvency is when the firm has negative equity (or the debt is greater

8. Use the concept of cash flow insolvency over time and describe what would happen if

the problem is temporary rather than permanent.

Continued cash flow insolvency over time relates to a sustained inability for cash

9. What are some of the basic requirements of a successful turnaround plan?

A successful turnaround plan should provide immediate remedial actions (once

10. Define operations restructuring and describe how it can be implemented to escape

financial distress.

Operations restructuring is either growing the firm’s revenues relative to cost or

11. Define asset restructuring and describe how it can be implemented to escape from

financial distress.

Asset restructuring involves either selling off assets and/or improving the firm’s

working capital. See Figure 16.2 for this and other ways to address financial distress.

12. Define financial restructuring and describe what is meant by debt payments extension

and debt composition change.

Financial restructuring involves changing the contractual terms or composition of the

13. What is a private workout? Also, describe some of the characteristics of ventures

that are likely to engage in private workouts.

A private workout is a voluntary restructuring of the firm in lieu of declaring

14. What is a private liquidation? What does the process of assignment mean?

A private liquidation is selling the pieces of a venture. The process of assignment is

15. What is Chapter 11 bankruptcy and how is it used by ventures?

Chapter 11 bankruptcy is an attempt by the firm to receive protection from creditors

as it tries to reorganize itself.

16. Describe a venture bankruptcy. Also, indicate the difference between (a) a voluntary

bankruptcy petition and (b) an involuntary bankruptcy petition.

A venture is bankrupt when a petition for bankruptcy is filed with a federal court.

17. Briefly describe the common pool and holdout problems that often make it necessary

for a venture to enter into a court-supervised reorganization.

A common pool problem exists because individual creditors have an incentive to

foreclose on the venture even though it is worth more as a going concern. The

18. Briefly define the following terms: cram down procedure, debtor-in-possession

financing, and prepackaged bankruptcy.

A cram down procedure is when a bankruptcy court accepts a reorganization plan

19. Describe the absolute priority rule.

The absolute priority rule is a hierarchal chain of priority when a firm files for

20. What is the purpose of Chapter 7 of the U.S. Bankruptcy Code? What are some of the

characteristics of ventures that use Chapter 7 instead of private liquidation?

The purpose of Chapter 7 is quickly to shut down the operations of a venture and start

21. From the Headlines – Necton: Describe the business model turnaround Necton

undertook. Comment on what you think would have been the challenges and your

perceptions about the likelihood the new business model will succeed.

Answers will vary: While the market for Necton’s products appears promising, the

INERNET ACTIVITIES

1. Go to the Web site for Wall Street Journal or some other financial publication such

as Inc. magazine and identify a venture that has recently filed for reorganization or

liquidation with the U.S. bankruptcy courts. Then, access the Securities and

EXERCISES/PROBLEMS AND ANSWERS

1. [Balance Sheet Restructuring Concepts] It was shown earlier in the chapter that

Northland Industries was suffering from balance sheet insolvency. Two scenarios are

possible for Northland in year 3. In scenario 1, year 3 for Northland is expected to

result in an additional $150,000 operating loss. On the other hand, scenario 2 is

A. Show Northland’s basic balance sheets under both scenarios.

B. Based on your analysis, will Northland Industries still be balance sheet insolvent

in year 3 under scenario 1? If this trend continues, would you describe

Northland’s financial distress as a temporary or permanent problem?

Northland is balance sheet insolvent in Scenario 1. If this continues, it would be a

C. Based on your analysis, will Northland Industries still be balance sheet insolvent

in year 3 under scenario 2? If this trend continues, would you describe

Northland’s financial distress as a temporary or permanent problem?

Year 0 Year 1 Year 2 Scenario 1 Scenario 2

Current Assets 100,000 100,000 100,000 100,000 100,000

Fixed Assets 100,000 100,000 100,000 100,000 100,000

Total Assets 200,000 200,000 200,000 200,000 200,000

Total Debt $0 $100,000 $250,000 $400,000 $0

YEAR 3

2. [Cash Flow Restructuring Concepts] It was shown earlier in the chapter that

Westland Industries was suffering from cash flow insolvency in terms of its earnings

before interest, taxes, and depreciation (EBITDA). Two scenarios are possible for

If scenario 1 occurs, the cash flow insolvency will continue. Under scenario 2, the

venture moves into substantial cash flow solvency position.

3. [Cash Flow Restructuring Concepts] It was shown earlier in the chapter that

Eastland Industries was suffering from cash flow insolvency. Let’s assume that

scenario 1 projects that year 3 and following years will be like the results incurred

for year 2 where profitability is low and continued large investments in net working

Year 0 Year 1 Year 2 Scenario 1 Scenario 2

YEAR 3

Year 0 Year 1 Year 2 Scenario 1 Scenario 2

Net Income 0 -70,000 20,000 20,000 100,000

+Depreciation 0 20,000 20,000 20,000 20,000

YEAR 3

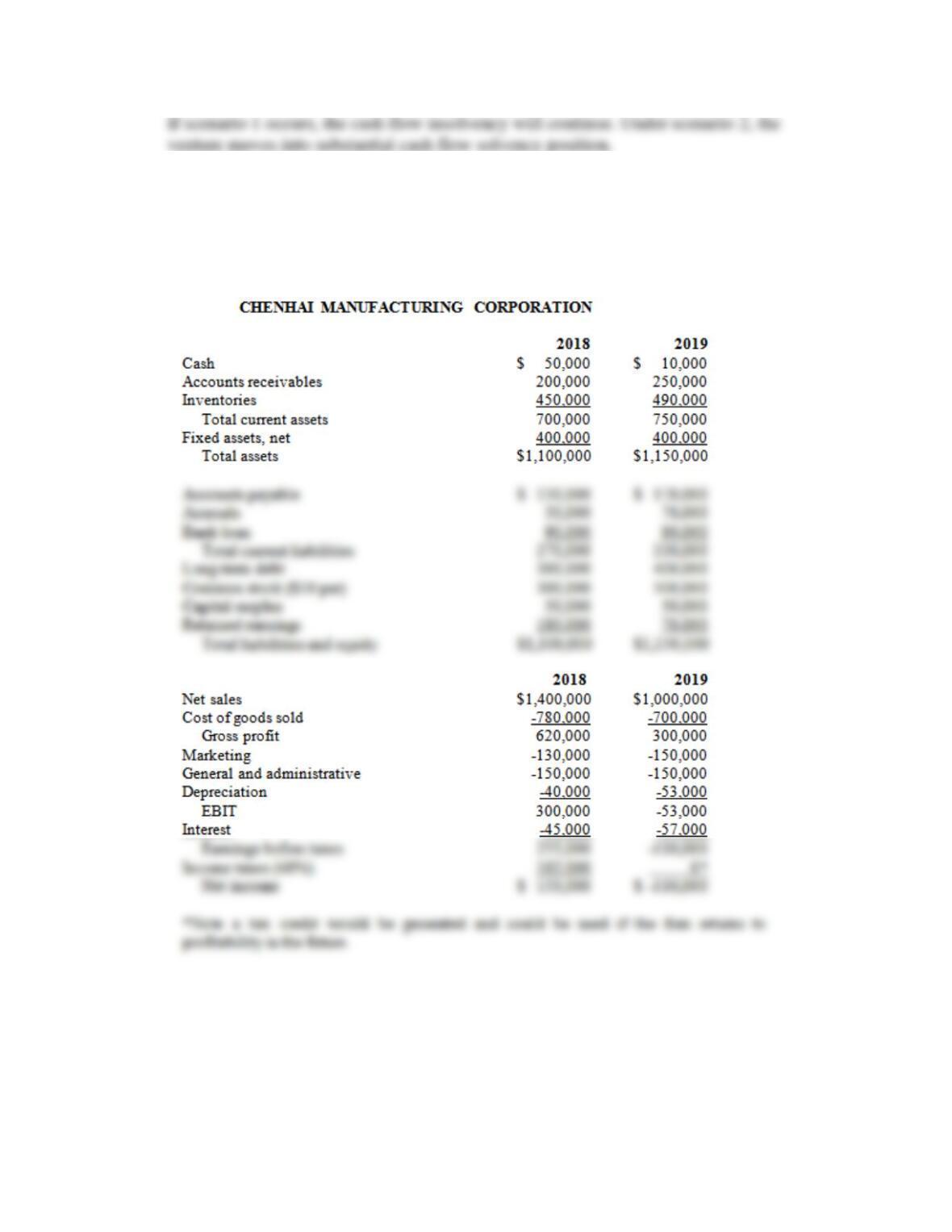

4. [Turnaround Opportunity: Restructuring Issues] Following are the financial

statements for the Chenhai Manufacturing Corporation for 2018 and 2019. The

venture is in financial distress and hopes to turn around its financial performance in

the near future.

A. Calculate the sale-to-cash conversion period for Chenhai in both 2018 and 2019.

Refer to Chapter 6 for calculating the cash conversion cycle and its three

components. Note: use “yearend” balance sheet data instead of averages so that

2018 and 2019 can be compared. Note: the sale-to–cash conversion period also is

2019.

Note: the inventory-to-sale conversion period also is referred to as the inventory

and 2019. Also determine the length of the cash conversion cycle for both 2018

and 2019.

The purchase-to-payment conversion period is the third component in the cash

conversion cycle.

D. What type of working capital restructuring might Chenhai undertake to turn

around its financial performance? What other type of asset restructuring might

Chenhai consider undertaking?

The CCC has increased from 178.49 days to 221.61 days. An effort should be

made to reduce the inventory-to-sale conversion period as well as the sale-to-cash

E. What type(s) of operations restructuring might Chenhai attempt during 2020?

Cost of goods sold increased from 55.7% ($780,000/$1,400,000) in 2018 to

70.0% in 2019 ($700,000/$1,000,000). Better control of the cost of production is

F. What type(s) of financial restructuring might Chenhai attempt during 2020?

Chenhai might attempt to reduce the amount of long-term debt that is outstanding

G. What prevailing conditions (economic, competitive, etc.) might cause you to

believe that Chenhai’s situation may be a turnaround opportunity versus a

permanent problem?

Of major concern is the decline in sales from $1,400,000 to $1,000,000. If the

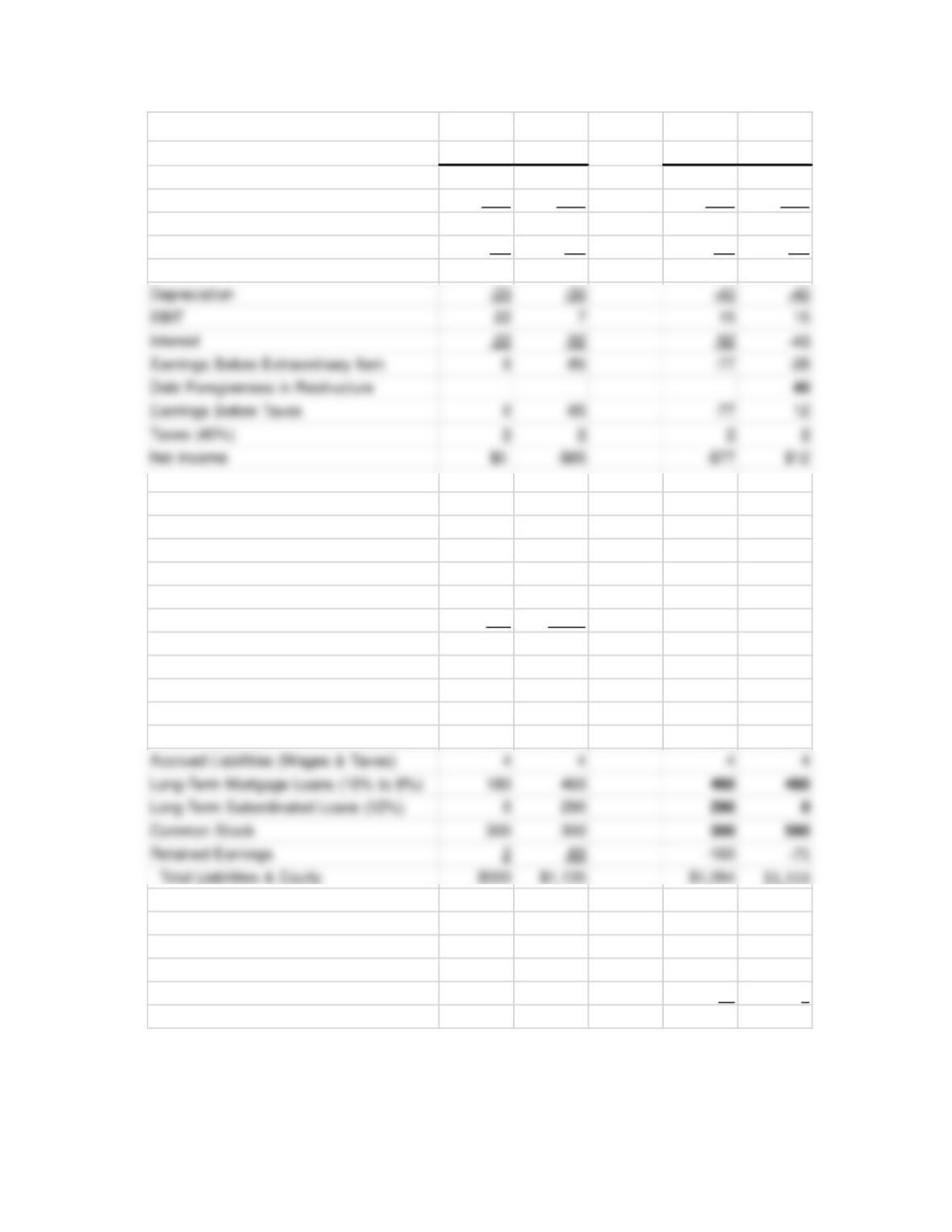

5. [Financial Restructuring Issues] EnCal is a small West Coast-based power company

specializing in power generation methods that use clean burning fuels and renewable

natural resources. However, due to complex and confusing power pricing structure,

EnCal is reeling from the aftereffects of the state government’s attempt at power

deregulation. EnCal has been unable to pass its operating costs on to its consumers.

to replace all of its subordinated loan balance with a 50% equity stake in the

company.

Income Statement ($ Millions)

2018

2019

2020

Revenue

$240

$360

?

COGS (70% – 2018, 80% – 2019/2020)

–168

–288

?

Gross Profit

72

72

?

SG&A

EBITDA

42

37

?

Depreciation

EBIT

22

?

Interest

?

Earnings Before Taxes

?

Taxes (40%)

?

Net Income

$0

–$85

?

Balance Sheet ($ Millions)

Assets

Cash

$10

$10

Accounts Receivable

20

30

Inventories

10

15

Fixed Assets, Net

510

1,080

Total Assets

$550

$1,135

Liabilities and Equity

Accounts Payable

$14

$24

Notes Payable (8% Bank Loan)

50

140

Accrued Liabilities (Wages & Taxes)

180

460

290

Common Stock

300

300

Retained Earnings

Total Liabilities & Equity

$550

$1,135

A. Assuming a 25% increase in revenue with no additional capital investment, what

will EnCal’s new income statement and balance sheet look like in the business as

usual and financial restructuring scenarios?

EnCal Corporation 2020 2020 Re-

Income Statement ($ Millions) 2018 2019 BAU structure

Revenue $240 $360 $450 $450

COGS (70% – 2015, 80% – 2016 & 2017) –168 –288 –360 –360

Gross Profit 72 72 90 90

SG&A –30 –35 –35 –35

EBITDA 42 37 55 55

Balance Sheet ($ Millions)

Assets

Cash $10 $10 –$32 $17

Accounts Receivable 20 30 38 38

Inventories 10 15 19 19

Fixed Assets, Net 510 1,080 1,040 1,040

Total Assets $550 $1,135 $1,064 $1,113

Liabilities

Accounts Payable $14 $24 $30 $30

Notes Payable (8% to 6% Bank Loan) 50 140 140 100

Note: Interest Calculations

Notes Payable (Bank Loan) 8% to 6% 11 6

Long-Term Mortgage Loans (10% to 8%) 46 37

Long-Term Subordinated Loans (12%) 35 0

Total Interest (subtraction in Inc. Stmt.) 92 43

B. Will EnCal be able to service its debt under either scenario?

Under the restructured 2020 projection they can service the debt. Under the

C. Would EnCal be a likely candidate for Chapter 7 bankruptcy?

EnCal would probably avoid liquidation under Chapter 7 if these projections are

D. Suppose the governor has called an emergency legislative session on the utility’s

behalf to prevent its eventual bankruptcy. If the governor is able to get a bill

($450M)/[(800,000kW)*(50%)*(365days)*(24hrs/day)] = $.128 per kWh

MINI CASE: ENDCO, INC.

Endco is a wireless solutions provider that facilitates wireless Internet access through

small remote devices that connect to portable computers. During the past several years,

Endco was lavished with an abundance of equity financial capital from a variety of

venture investors. Although initial adoption rates for this new service were far below

expectations, most were confident that expanding the service area and thus increasing the

Balance Sheet ($ Millions)

Assets

Liquidation

Receipts

Cash

$2.4

$2.4

Inventory

16.0

5.0

Accounts Receivable

5.6

3.0

Net Plant

200.0

Net Equipment

100.0

57.0

Total Assets

$324.0

$232.4

Liabilities & Equity

Accounts Payable

$3.5

Notes Payable (12% Bank Loan)

29.0

Accrued Liabilities (Wages & Taxes)

1.5

Long-Term Mortgage Loans (12%, 10

years)

140.0

(14%, 15 years)

80.0

Payable)

20.0

Preferred Stock

300.0

Common Stock

100.0

Retained Earnings

Total Liabilities

$324.0

A. Who are considered to be the priority claimants in this liquidation?

The priority claimants are the government, employees and mortgage holders.

B. Who are considered to be general creditors?

C. Create a table indicating the cash distribution to each creditor and the percentage of

the original liability that is satisfied.

Claimant

Priority

Payments

Remaining

Claims

Payments on

Remaining Claims

Total

% Liability

Satisfied

Administrative and Legal

0.37 0.37

Wages & Taxes 1.50 1.50 100.00%

Long-Term Mortgage Loan 140.00 140.00 100.00%