223

Chapter 15

HARVESTING THE BUSINESS VENTURE INVESTMENT

FOCUS

This chapter in our entrepreneurial finance text focuses on how a successful entrepreneur

can harvest or exit the venture.

LEARNING OBJECTIVES

LO 15.1: Discuss financial decisions faced by ventures during their rapid-growth and

early-maturity stages.

CHAPTER OUTLINE

15.1 VENTURE OPERATING AND FINANCIAL DECISIONS REVISITED

15.2 PLANNING AN EXIT STRATEGY

15.3 VALUING THE EQUITY OR VALUING THE ENTERPRISE

15.4 SYSTEMATIC LIQUIDATION

15.5 OUTRIGHT SALE

A. Family Members

15.6 GOING PUBLIC

A. Investment Banking

DISCUSSION QUESTIONS AND ANSWERS

1. What is the meaning of harvesting a venture?

Harvesting a venture refers to the process of exiting a privately-held business venture

2. What evidence exists as to whether entrepreneurs think about and/or develop exit

strategies?

Holmberg documented that over ½ of entrepreneurs have developed, or at least

3. What are unicorns? How might their exit values be impacted when they go public?

Unicorns are high-expected-growth companies with valuations in excess of $1

billion.

4. Describe how the relative value method is used to value a firm’s equity.

The relative value method estimates a firm’s value by examining how comparable

firms are valued based on value-related multiples.

Comparable firms are firms with lines of business, size, and growth characteristics

5. What is a systematic liquidation of a venture? What are some of the advantages and

disadvantages of a systematic liquidation?

A systematic liquidation of a venture is the process of liquidating the firm by

distributing the cash flows of the firm to the owners. This usually happens when the

Potential disadvantages include: (1) the treatment and taxation of liquidation proceeds

6. Describe an outright sale of a venture. What are the four categories of possible

buyers?

An outright sale of a venture occurs when it is sold to others. The four categories of

7. Describe what is meant by (a) a leveraged buyout (LBO), and (b) a management

buyout (MBO).

An LBO occurs when a firm is bought out by investors who finance the majority of it

8. What is an employee stock option plan (ESOP)? How is an ESOP used to buy out a

venture?

An ESOP is typically a benefit plan where employer and employee contributions are

9. Describe the terms (a) “control premium” and (b) “illiquidity discount” when

discussing possible external or outside buyers of a venture.

10. Describe an initial public offering (IPO). What are the differences between a

primary offering and a secondary offering?

An IPO is the first public sale of a venture’s equity ownership. The primary offering

refers to the sale of new shares to their first owners. A secondary offering is the sale

11. What is investment banking? What is an underwriting spread?

Investment banking facilitates the issue of new securities by creating markets for a

firm’s security.

12. Describe the terms “tombstone ad” and “red herring disclaimer.”

A tombstone ad is an SEC requirement and an advertisement used to notify the public

of an upcoming offering,

A red herring disclaimer is a required statement on the tombstone ad (or elsewhere)

13. What is meant by due diligence? How does a traditional registration differ from a

shelf registration?

Due diligence is the process whereby an investment bank investigates an issuing

company’s financial condition and investment intent.

14. When an investment banking firm decides whether to underwrite or market a

securities issue, what is meant by a firm commitment and best efforts?

A firm commitment by an investment bank means that the bank will purchase the

security issue and then resell it in the market.

15. Describe the two following terms that may be involved in underwriting a new

securities issue: (a) green shoe and (b) lockup provision.

A green show provision is a contract option for the investment bank to sell more

shares than allotted in the underwriting if the issue is broadly oversubscribed.

16. What is meant by initial public offering (IPO) underpricing?

IPO underpricing is when the offering price by the syndicate is lower than the first

17. Briefly describe how securities are traded on an organized stock exchange such as

the New York Stock Exchange.

Organized exchanges have specialized geographic (or electronic) places where

18. Indicate some of the differences between the NASDAQ’s National Market System and

SmallCap listing requirements.

NYSE Initial Listing Requirements are presented in Table 15.1. Another listing

19. Describe some of the preparations that a venture can undertake that may increase

the possibility of IPO success.

Typical preparations for an IPO include, but are not limited to: (i) cleaning up

20. What are the steps or stages in a “typical” execution and time line schedule used in

planning and executing an IPO?

The execution and time line include:

21. From the Headlines – Boom Supersonic: Comment on Boom Supersonic’s

potential to eventual provide liquidity to its investors through an IPO or a sale.

Which one seems more likely to you? Why?

EXERCISES/PROBLEMS AND ANSWERS

1. [DCF Valuation and Ownership Concepts] The venture investors and founders of the

ACE Products venture, a closely held corporation, are contemplating merging the

successful venture into a much larger diversified firm that operates in the same

addition, the venture also has surplus cash of $4 million. ACE currently has 5

million shares outstanding with 3 million held by venture investors and 2 million held

by founders. The venture investors have an average investment of $2.50 per share

while the founders’ average investment is $.50 per share.

A. Based on the above information, estimate the enterprise value of ACE Products.

What would be the value of the venture’s equity?

B. How much of the value of ACE would belong to the venture investors versus the

founders. How much would the venture be worth on a per share basis?

Percent ownership: Venture investors = 3 million shares/5 million shares = 60%

C. What would be the percentage appreciation on the stock bought by the venture

investors versus the investment appreciation for the founders?

Venture investors percentage appreciation = [($8.856 − $2.50)/$2.50] 100 =

D. If the founders have held their investments for five years, calculate their

compound annual or internal rate of return on their investments. The venture

investors made a first round investment of 1.5 million shares at $2 per share four

years ago. What was the compound annual rate of return on the first round

investment? Venture investors made a second round investment of 1.5 million

shares at $3 per share two years ago. Calculate their compound rate of return on

this investment.

Founders investment (present value): $.50 x 2,000,000 shares = $1,000,000

2. [Acquisition Valuation Concepts] The BETA firm is proposing to acquire the ACE

Products venture described in Problem 1. BETA estimates that ACE’s free cash flow

for next year could be improved to $5.5 million because of synergistic benefits in the

form of operating or distribution economies. The potential acquirer also believes

that ACE’s perpetuity growth rate could be increased to 7 percent annually.

However, the riskiness of the cash flows would be increased causing the appropriate

WACC to increase to 16 percent. Interest-bearing debt owed by ACE is $17.5

million. In addition, the venture also has surplus cash of $4 million. ACE Products

has five million shares of common stock outstanding.

A. Determine ACE’s enterprise value from the perspective of BETA. What is ACE’s

equity worth to BETA in dollar amount and on a per share basis?

Enterprise operating value = $5,500,000/(.16 − .07) = $61,111,111

B. Use the per share value of ACE from Problem 1 and the per share value from this

problem and establish a range of values (i.e., without and with expected

synergistic benefits). If one-half of the synergy derived benefits were allocated to

ACE’s venture investors and founders, what price per share would the merger

take place?

C. BETA has thirty million shares of stock outstanding with a market capitalization

value of $600 million. What is BETA’s stock price? Determine the exchange ratio

between ACE’s stock value and BETA’s stock price at each of ACE’s values

established in Part B. That is, what would ACE’s venture investors and founders

receive in BETA’s shares for each share of common stock they currently hold in ACE

Products?

3. [Relative Value Concepts Using Multiples] The WestTek privately held venture is

considering the sale of the venture to an outside buyer. WestTek has net sales =

$21.2 million, EBITDA = $11.1 million, net income = $2.9 million, and interest-

bearing debt = $12 million. Three publicly-traded comparable firms or competitors

in the industry have the following net sales, EBITDA, net income, equity value or

market capitalization (stock price times number of shares of common stock

outstanding), and interest-bearing debt information:

EastTek SouthTek NorthTek

Net sales $25,000,000 $37,500,000 $80,000,000

No surplus cash is being held by WestTek or by any of the three comparable firms.

A. Calculate the enterprise value to net sales ratios for each of the three competitors

(EastTek, SouthTek, and NorthTek), as well as the average ratio for the

competitors.

Enterprise value = equity value + interest-bearing debt

Equity value = market capitalization (i.e., stock price times shares outstanding)

B. Calculate the enterprise value to EBITDA ratios for each of the three competitors,

as well as the average ratio for the competitors.

EastTek: $60,000,000/$12,500,000 = 4.80

C. Calculate the equity value or market “cap” to net income ratios for each of the

three competitors, as well as the average ratio for the competitors.

D. Estimate the enterprise and equity values for WestTek using the individual net

sales multiples from EastTek, SouthTek, and NorthTek, as well as for the average

of the three competitors or comparable firms. Show the valuation ranges from

high to low.

Enterprise Value Estimates:

Using EastTek sales multiple: $21,200,000 2.40 = $50,880,000

Equity Value Estimates:

Equity value = enterprise value – interest-bearing debt

Since WestTek has interest-bearing debt of $12,000,000, this amount must be

subtracted from the enterprise value estimates calculated above to provide equity

value estimates.

E. Estimate the enterprise and equity values for WestTek using the individual

EBITDA multiples from each comparable firm, as well as the average multiple for

the three competitors. Show the valuation ranges from high to low.

Enterprise Value Estimates:

Using EastTek EBITDA multiple: $11,100,000 4.80 = $53,280,000

Equity Value Estimates:

Since WestTek has interest-bearing debt of $12,000,000, this amount must be

subtracted from the enterprise value estimates calculated above to provide equity

value estimates.

F. Estimate the equity values for WestTek using the individual net income multiples

from each comparable firm, as well as the average multiple for the three firms.

Equity Value Estimates:

G. Establish a range of equity value estimates for WestTek based on the highest and

lowest overall values generated from the multiples analyses in Parts D, E, and F.

Also establish a range of market value estimates for WestTek based on the highest

and lowest average values from the multiples analyses in Parts D, E, and F.

Part D: High = $41,000,000; Low = $33,156,000

H. From the perspective of the selling venture investors and founders, would you

recommend that they negotiate for the final selling price be based on the use of

top-line valuation multiples (i.e., using net sales) or bottom-line valuation

multiples (i.e., using net income)?

4. [Venture Capital (VC) Method Valuation Concepts] Benito Gonzalez, founded and grew

the BioSystems Manufacturing Corporation over a several year period. However, Benito

has decided to exit BioSystems as of the end of 2019 with the intention of starting a new

entrepreneurial venture. The Fuji Electronics Company is considering acquiring

BioSystems which is 60 percent owned by Benito Gonzalez with the other 40 percent of the

BIOSYSTEMS MANUFACTURING CORPORATION

Income Statement for 2019 ($ Thousands)

A. Using the percent-of-sales relationships indicated above, prepare BioSystems’

income statements for 2022.

Note: Income statements are projected annually for 2020 and 2021 in order to provide

the 2022 projections. Data are presented in Thousands of Dollars. See spreadsheet

solution shown below.

B. Fuji Electronics has examined other recent acquisitions in BioSystems’ industry and

believes that a 17 times price-earnings multiple would be appropriate for determining

BioSystems value in the future. Calculate the value of BioSystems as of the end of

2022.

P/E Multiple for 2022: 17

C. How much should Fuji Electronics be willing to pay for BioSystems Manufacturing

at the end of 2019 if Fuji’s management believes the appropriate discount rate is 25

percent?

D. What is Gonzalez’s portion of the exit proceeds? What is the venture investors’

portion of the exit proceeds?

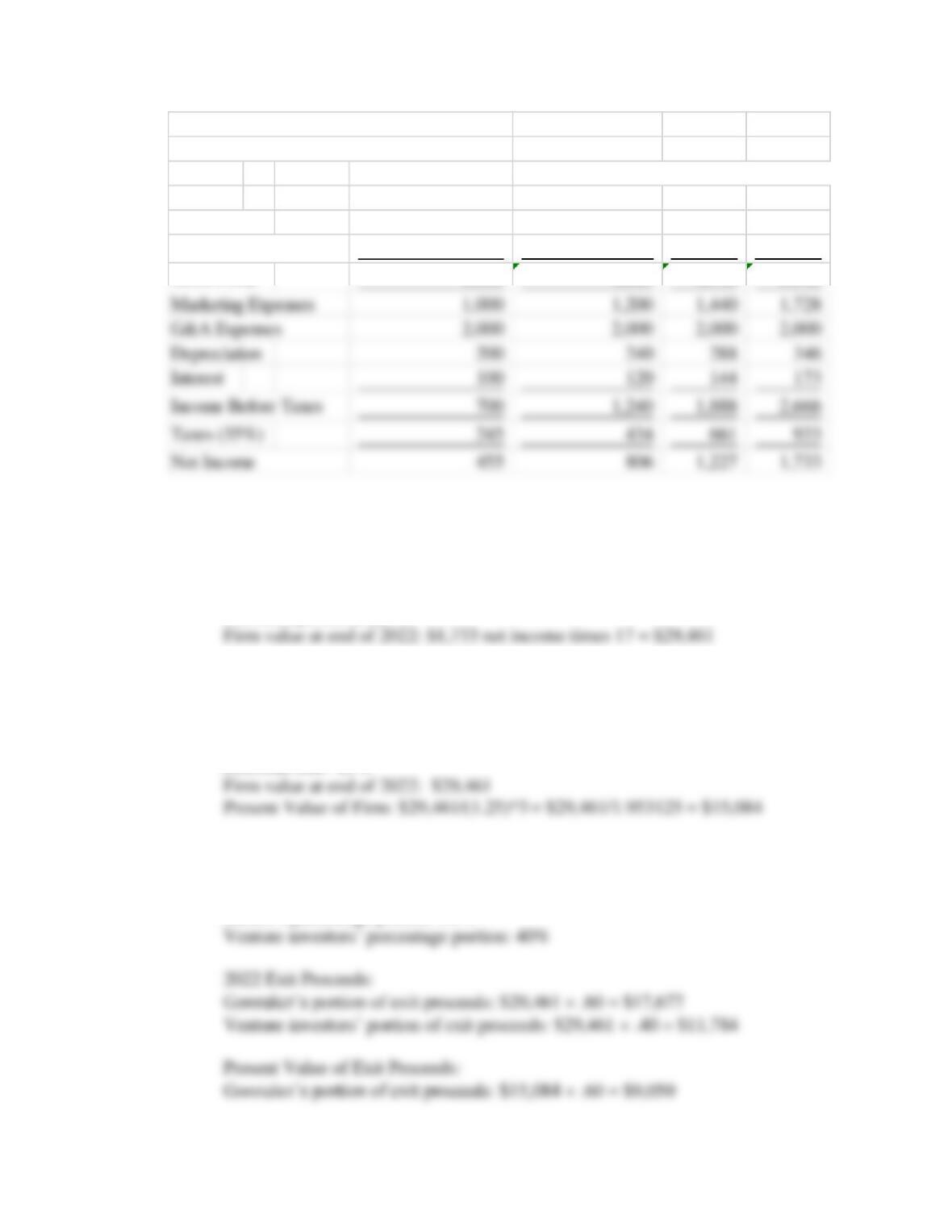

Biosystems Manufacturing Corporation

Income Statement for 2019 ($ Thousands)

Actual Projected –—-—-—-—-—-—–—

2019 2020 2021 2022

Net Sales 10,000 12,000 14,400 17,280

Cost of Goods Sold 6,000 7,200 8,640 10,368

Venture investors’ portion of exit proceeds: $15,084 .40 = $6,034

E. Benito Gonzalez invested $50,000 of his own funds in BioSystems at the end of

2014. What would be the compound rate of return on his investment when the exit

(sale to Fuji Electronics) from BioSystems occurs at the end of 2019?

Initial investment at end of 2014: $50,000

F. The venture investors contributed $500,000 at the end of 2015. What would be

their compound rate of return on their investment if BioSystems is sold at the end of

2019?

Initial investment at end of 2015: $500,000

5. [Terminal or Horizon Period Valuation Concepts] The Gamma Systems Manufacturing

Corporation has reached its maturity stage and its net sales are expected to grow at a 6

percent compound rate for the foreseeable future. Management believes that as a mature

venture the appropriate equity discount rate for Gamma Systems is 18 percent.