A. Estimate the free cash flows available to the equity investors for 2020.

The following spreadsheet assumes that most accounts are a constant percent

of sales (starting in 2020). We have balanced the balance sheets by raising the

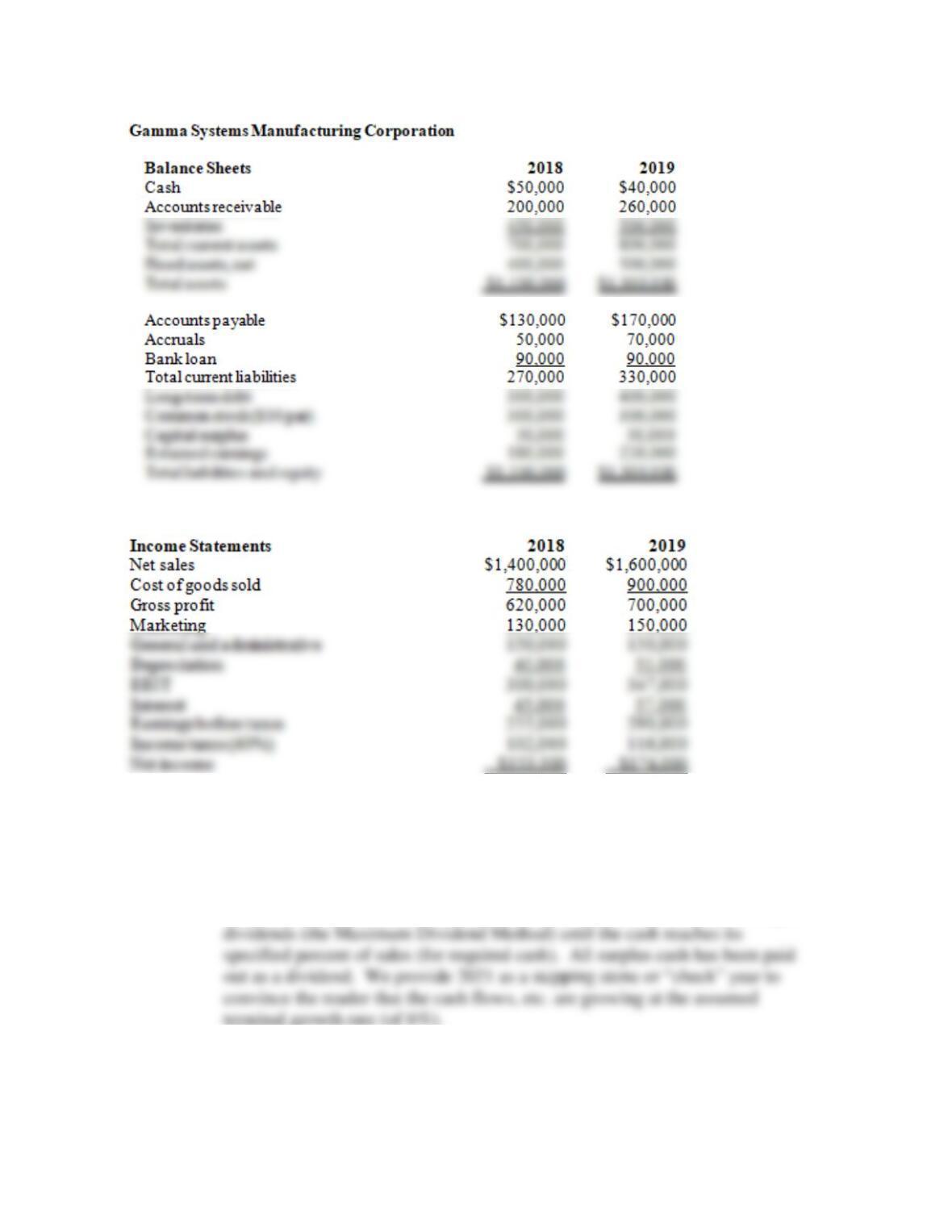

GAMMA SYSTEMS MANUFACTURING CORPORATION

[Chapter 15, Problems 5-7]

Problem 5:

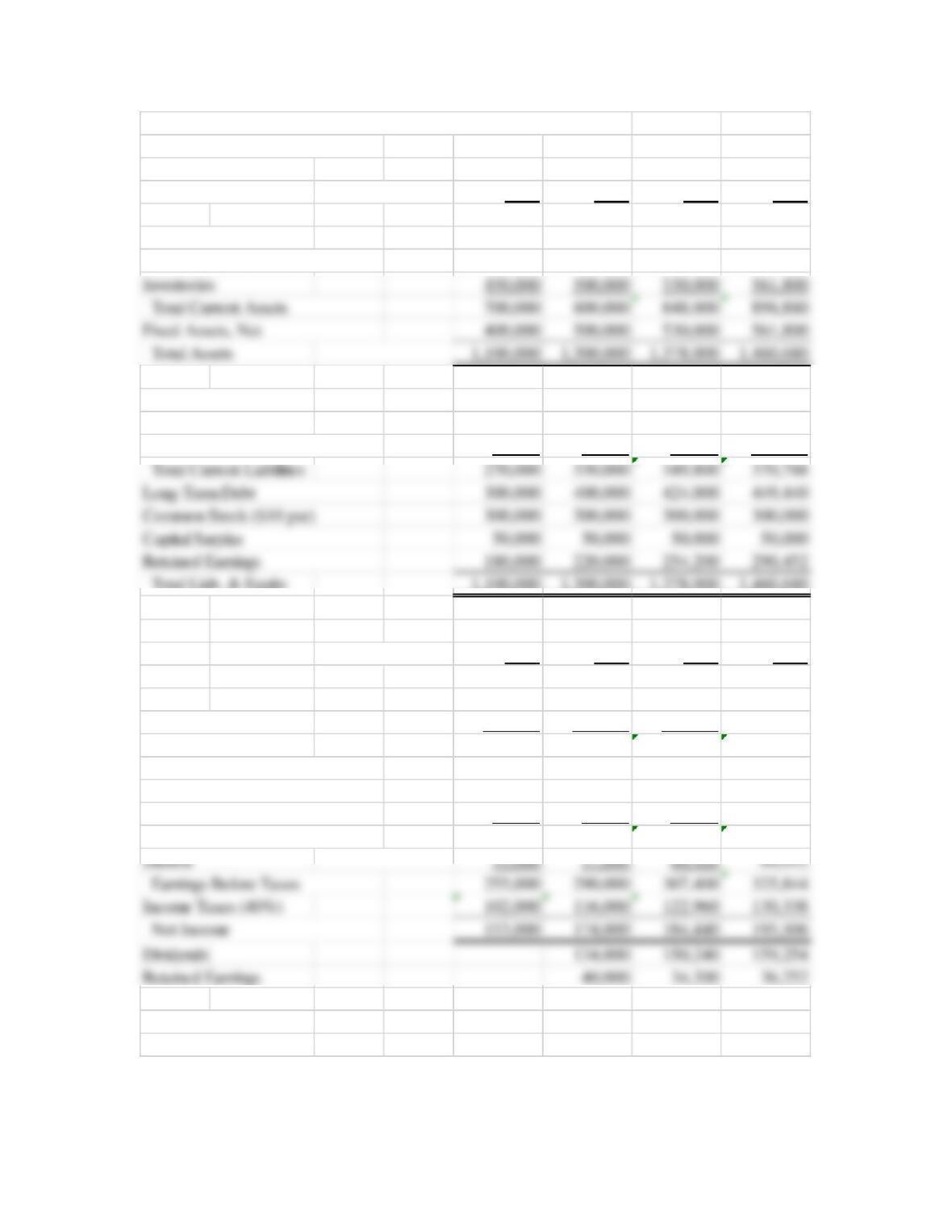

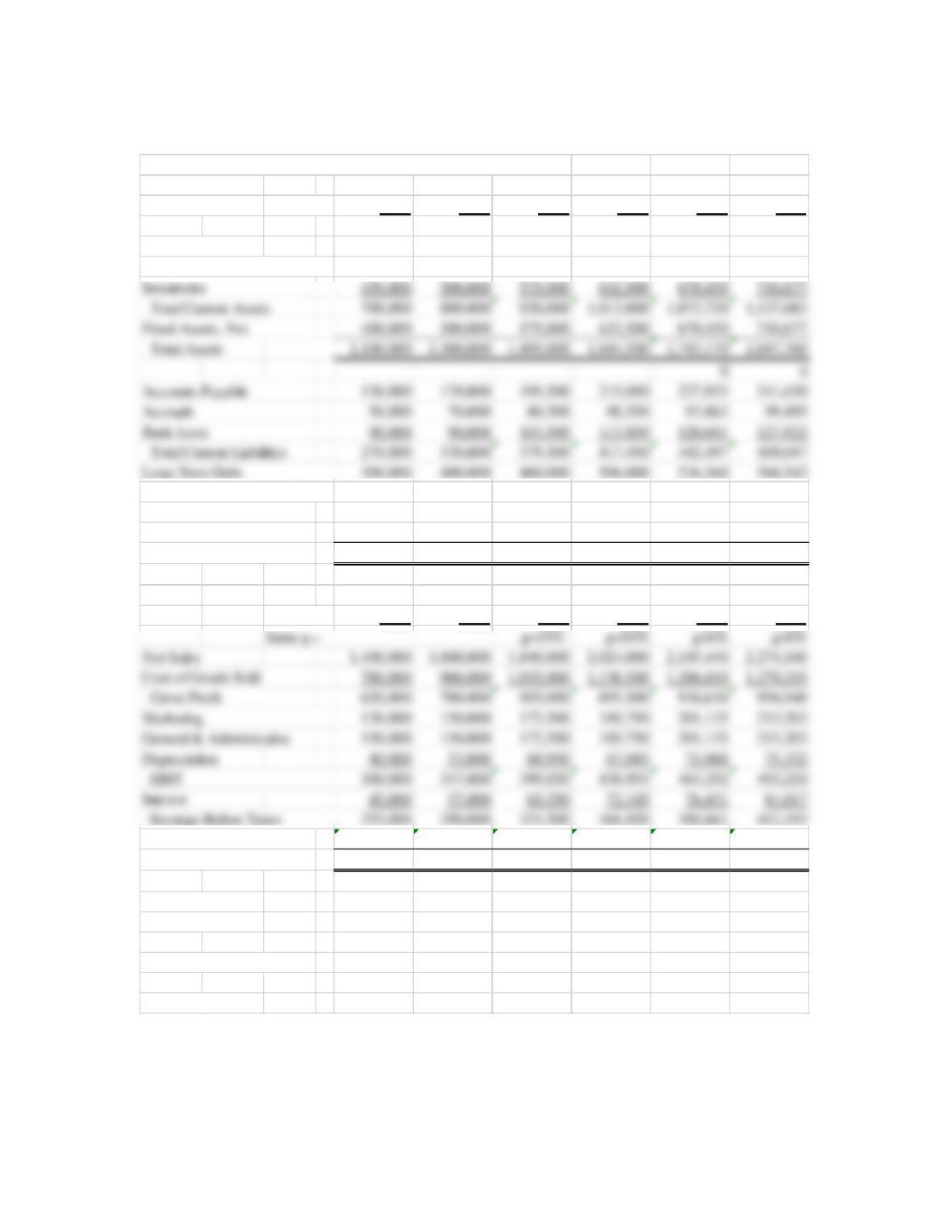

Balance Sheets

2018 2019 2020 2021

Check Year

Cash 50,000 40,000 42,400 44,944

Accounts Receivables 200,000 260,000 275,600 292,136

Accounts Payable 130,000 170,000 180,200 191,012

Accruals

50,000 70,000 74,200 78,652

Bank Loan 90,000 90,000 95,400 101,124

Total Liab. & Equity 1,100,000 1,300,000 1,378,000 1,460,680

2018 2019 2020 2021

Net Sales 1,400,000 1,600,000 1,696,000 1,797,760

Cost of Goods Sold 780,000 900,000 954,000 1,011,240

Gross Profit 620,000 700,000 742,000 786,520

Marketing 130,000 150,000 159,000 168,540

General & Administrative 150,000 150,000 159,000 168,540

Depreciation

040,000 53,000 56,180 59,551

EBIT

300,000 347,000 367,820 389,889

Sales g = 6.00% 6.00%

Growth Rate 6%

Discount Rate 18%

B. Estimate the value of Gamma Systems equity at the end of 2019 by applying

the terminal value perpetuity equation that was presented in Chapter 10.

A) Statement of Cash Flows Approach 2020

Operating:

Net Income 184,440

+Depreciation 56,180

–Inc. in Accts. Receivable

–15,600

Financing:

+Increase in Bank Loans 5,400

+Increase in Long–Term Debt 24,000

FCF (from Statement of Cash Flows) 150,240

(Same as Dividends here)

Shortcut Method:

NI 184,440

+Depr 56,180

Value (End of 2019)

1,252,000$

That the VCF will growth smoothly at 6% for the remainder of eternity and

that the required return will remain constant at 18%.

6. [Valuation Sensitivities to Changes in Growth Rates and Discount Rates] Assume

that some of the information relating to the Gamma Systems Manufacturing

Corporation has changed. Using the financial statement data in Problem 5, answer

the following questions.

A. How would your valuation estimate change if the sales growth rate had been 6

percent but the discount rate had been 20 percent?

B. How would your valuation estimate change if the sales growth rate had been 5

percent and the discount rate 18 percent?

To use a 5% terminal growth rate, we must construct a new stepping stone

or “check” year. The remainder is analogous to the solution to Problem 5

above.

C. How would your valuation estimate change if the perpetuity growth rate had

been 7 percent and the discount rate 20 percent?

Value = 146,280/(.20 − .07) = $1,125,231.

GAMMA SYSTEMS MANUFACTURING CORPORATION

Problem 6:

A) 1,073,143$

[Based on growth rate = 6.00% and discount rate = 20%]

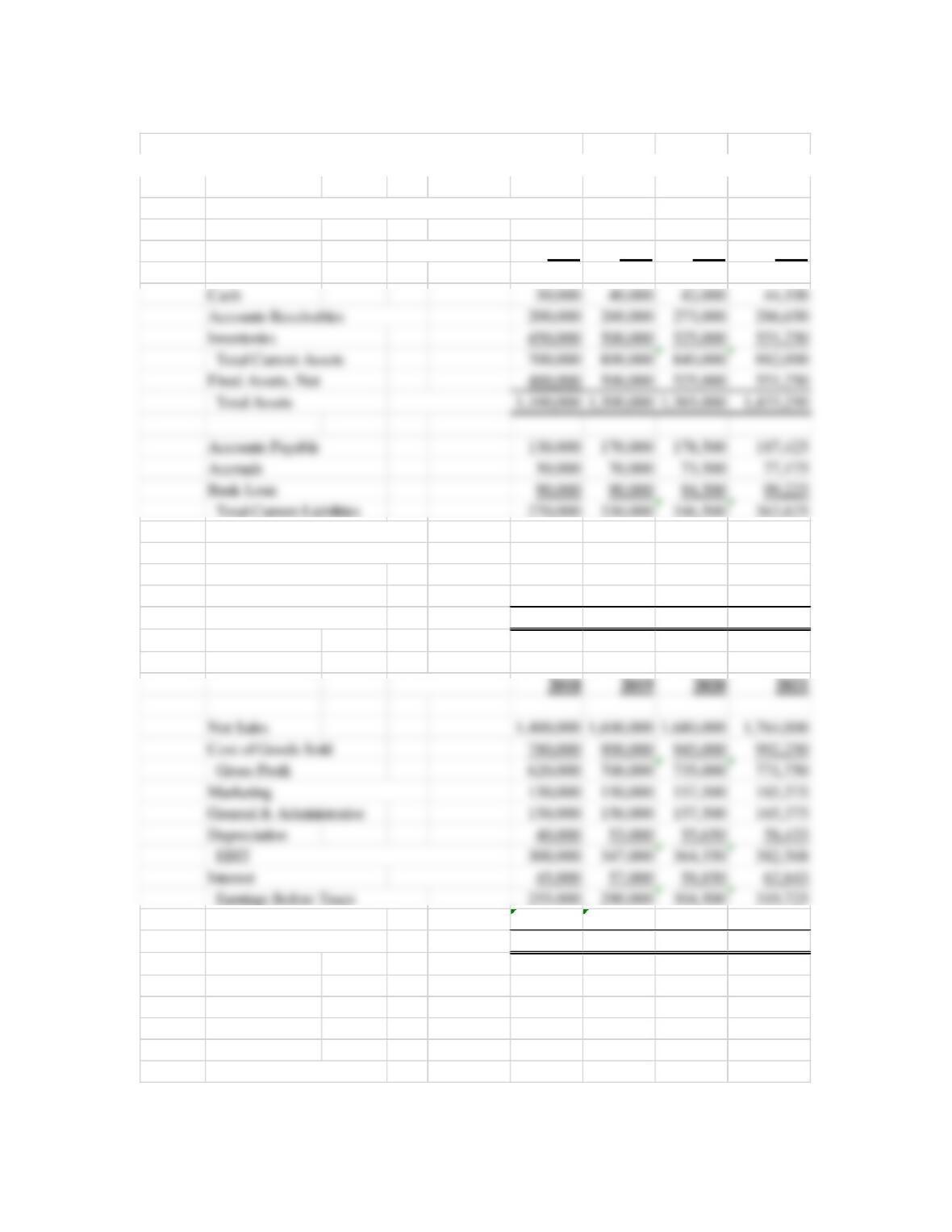

B) Balance Sheets

2018 2019 2020 2021

Check Year

Long–Term Debt 300,000 400,000 420,000 441,000

Common Stock ($10 par) 300,000 300,000 300,000 300,000

Capital Surplus 50,000 50,000 50,000 50,000

Retained Earnings 180,000 220,000 248,500 278,425

Total Liab. & Equity 1,100,000 1,300,000 1,365,000 1,433,250

Income Taxes (40%) 102,000 116,000 121,800 127,890

Net Income 153,000 174,000 182,700 191,835

Dividends 134,000 154,200 161,910

Retained Earnings 40,000 28,500 29,925

Sales g = 5.00% 5.00%

Growth Rate 5%

Discount Rate 18%

Value (End of 2019) 1,186,154

GAMMA SYSTEMS MANUFACTURING CORPORATION

C) Balance Sheets

2018 2019 2020 2021

Check Year

Cash 50,000 40,000 42,800 45,796

Accounts Receivables 200,000 260,000 278,200 297,674

Inventories 450,000 500,000 535,000 572,450

Total Current Assets 700,000 800,000 856,000 915,920

Fixed Assets, Net 400,000 500,000 535,000 572,450

Total Assets

1,100,000 1,300,000 1,391,000 1,488,370

0

Accounts Payable 130,000 170,000 181,900 194,633

Accruals 50,000 70,000 74,900 80,143

Gross Profit 620,000 700,000 749,000 801,430

Marketing 130,000 150,000 160,500 171,735

General & Administrative 150,000 150,000 160,500 171,735

Depreciation 40,000 53,000 56,710 60,680

EBIT 300,000 347,000 371,290 397,280

g = 7.00% 7.00%

Growth Rate 7%

Discount Rate 20%

Value 1,125,231

7. [Valuation Impact of Changes in Forecast Period Growth Rates] New information

for the Gamma Systems Manufacturing Corporation has been brought to the

management’s attention. Use the financial statement information in Problem 5 and

take into consideration that sales will grow at a 15 percent rate in 2020 and a 10

percent rate in 2021 before settling down to a 6 percent perpetuity growth rate.

A. Estimate the free cash flows available to equity investors for 2020, 2021, and

2022.

Free cash flow is the same as “dividends” in the MDM used in the spreadsheet

below.

GAMMA SYSTEMS MANUFACTURING CORPORATION

Problem 7:

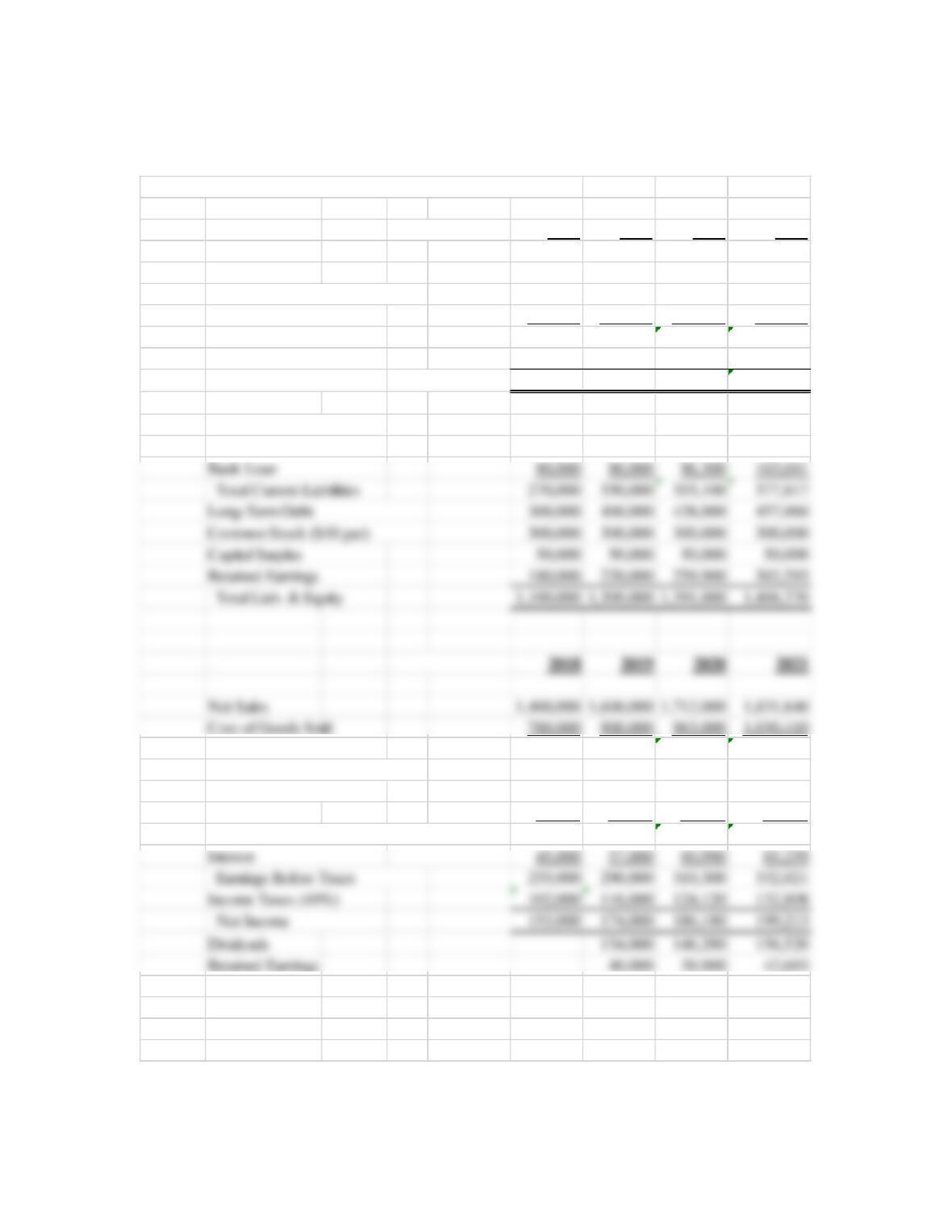

Balance Sheets 2018 2019 2020 2021 2022 2023

Check Year

Cash 50,000 40,000 46,000 50,600 53,636 56,854

Accounts Receivables 200,000 260,000 299,000 328,900 348,634 369,552

Common Stock ($10 par) 300,000 300,000 300,000 300,000 300,000 300,000

Capital Surplus 50,000 50,000 50,000 50,000 50,000 50,000

Retained Earnings 180,000 220,000 305,500 371,050 414,313 460,172

Total Liab. & Equity 1,100,000 1,300,000 1,495,000 1,644,500 1,743,170 1,847,760

2018 2019 2020 2021 2022 2023

Income Taxes (40%) 102,000 116,000 133,400 146,740 155,544 164,877

Net Income 153,000 174,000 200,100 220,110 233,317 247,316

Dividends 134,000 114,600 154,560 190,054 201,457

Retained Earnings 40,000 85,500 65,550 43,263 45,859

Dividend growth g = 34.87% 22.96% 6.00%

2021 Terminal Value 1,583,780

VCF 114,600 1,738,340

2019 NPV 1,345,567

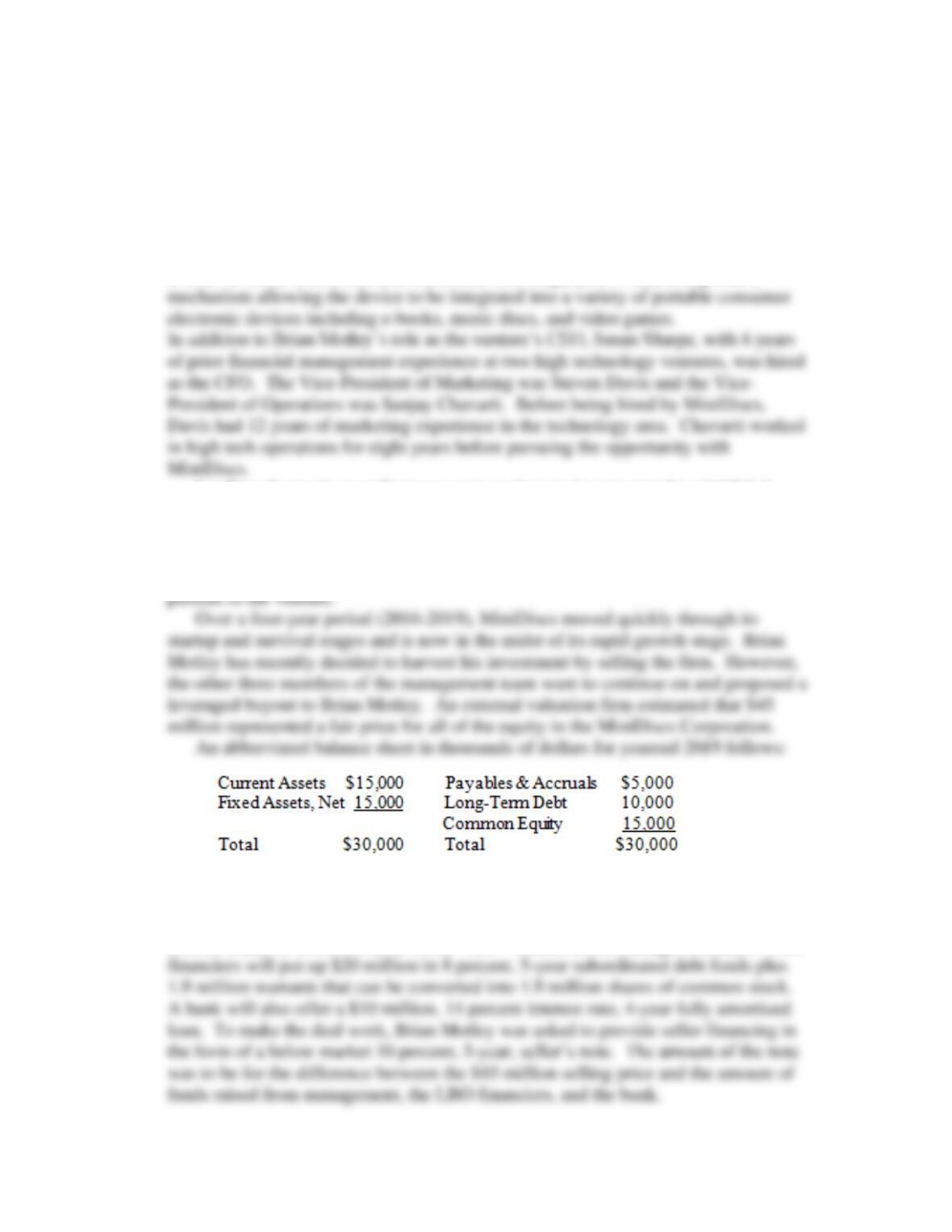

MINI CASE: MINIDISCS CORPORATION

Brian Motley founded the MiniDiscs Corporation at the end of 2014. After nearly

one year of development, the venture produced an optical storage disk about the size

of a silver dollar that could store more than 500 megabytes of data along with a

Leading electronic manufacturers were anxious to incorporate the minidisk in

their products. Brian Motley obtained $7 million financing at the end of 2015 from

venture investors in exchange for 43 percent of the stock in the venture. After this

round of venture financing, Brian retained 50 percent ownership in MiniDiscs and the

other three members of the management team (Sharpe, Davis, and Chavarti) owned 7

It is the beginning of 2020, and the management team has $5 million of their own

capital, including their share of the sales price, available to purchase all of the

venture’s existing equity capital. The intent is to retire all of the old stock and issue 2

million shares of common stock in the “new” venture to the management team. LBO

In exchange for the seller financing by Brian Motley, the existing venture

capitalists agreed to reduce their ownership rights from 43 percent to 40 percent. The

currently at 16 percent.

A. What will be the dollar amount of seller financing that Brian Motley will need to

provide to complete the financing of the $45 million selling price?

Management team = $5 million

B. How much cash will be available to distribute to the existing owners of the

MiniDiscs Corporation? What will be the dollar breakdown for Brian Motley, the

management team, and the venture capitalists?

Original Percent Exit Percent

Equity Owners Ownership Ownership

Brian Motley 50% 55%

Management Team 7 5

Venture Investors 43 40

100% 100%

C. What compound rate of return did Motley earn on his $1 million end of 2014

investment?

The $1million original investment bought only 50% of the 2019 equity value. The

additional $10 million below-market loan (negative NPV loan) was the

D. What compound rate of return did the venture capitalists earn on their $7 million

investment at the end of 2015?

E. After five years of operating as a private venture owing to the LBO, assume that

the common equity in the MiniDiscs Corporation could be sold for $60 million at

the end of 2024. What compound rate of return would the management team earn

on its $5 million investment?

The VCs were given warrants to purchase 1.9 million shares of stock. Thus, at

exit there would be 3.9 million total shares of common stock outstanding.

F. Assume that when MiniDiscs is sold at the end of 2024 for $60 million that the

LBO financiers will have their debt retired and will sell their share of interest in

the venture. What compound rate of return would the LBO financiers receive?

As the exercise price of the warrants is not specified, we will provide two possible

scenarios:

1) The warrants are exercised by surrendering the VC’s claim to the principal

on the subordinated debt it holds. This structure is like assuming the bond

2) The warrants have some trivial (close to zero) exercise price that is negligible

for the purpose of the analysis (as was the assumption in the example solution

presented in Section 15.5 of the textbook) and the $20,000,000 in bond