Chapter 10

VALUING EARLY-STAGE VENTURES

FOCUS

In this chapter, we introduce basic concepts of valuation, the process of estimating

values. We consider the owner of a growing business who is beginning negotiations with

a potential investor. We introduce the mechanics of valuation and some mathematical

simplification that can be used to value the venture. By dividing the venture’s future into

LEARNING OBJECTIVES

LO 10.1: Explain why it is important to look to the future when determining a venture’s

value.

LO 10.1: Describe the need to consider both forecast period and terminal value cash

flows when determining a venture’s value.

CHAPTER OUTLINE

10.1 WHAT IS A VENTURE WORTH?

A. Does the Past Matter?

B. Looking to the Future

C. Vested Interests in Value: Investor and Entrepreneur

10.2 BASIC MECHANICS OF VALUATION: MIXING VISION AND REALITY

10.3 REQUIRED VERSUS SURPLUS CASH

10.4 DEVELOPING THE PROJECTED FINANCIAL STATEMENTS FOR A DCF

VALUATION

10.6 ACCOUNTING VERSUS EQUITY VALUATION CASH FLOW

SUMMARY

LEARNING SUPPLEMENT 10A:

DISCUSSION QUESTIONS AND ANSWERS

1. What is meant by sweat equity?

2. What is a venture’s present value? Does the past matter?

A venture’s present value is the value today of all future cash flows discounted to the

3. Describe what is meant by the statement “If you’re not using estimates, it’s not a

valuation.”

It is important to recognize that projected financial statements needed to calibrate

4. Define the terms (a) explicit forecast period and (b) terminal or horizon value as they

relate to a venture’s discounted cash flow valuation.

Explicit forecast period: two- to ten-year period in which the venture’s financial

forecast period

5. What is meant by a capitalization (or cap) rate in reference to calculating a terminal

value? What other types of terminal values might be appropriate (i.e., other than

smooth growth procedures)?

Dividing by the cap rate (r – g) in the perpetuity formula is the appropriate

6. What is a venture’s reversion value?

Reversion Value: the present value of the terminal value.

7. What is a stepping stone year? Why is it important in determining a venture’s value?

Stepping-stone year: first year after the explicit forecast period

8. Explain the difference between pre-money valuation and post-money valuation.

Pre-Money valuation: present value of a venture prior to a new money investment

9. Describe the equity valuation method.

Equity valuation method (equity method): process of projecting and then

discounting the relevant cash flows available to equity investors

10. Define required cash and surplus cash. Why does it matter how we treat surplus cash

for valuation purposes?

Required cash: amount of cash needed to cover a venture’s day–to-day operations

11. Briefly describe the process for projecting financial statements.

The process begins by projecting top-line sales forecasts annually for a specified

12. What is net operating working capital?

Net operating working capital: current assets less surplus cash less non-interest-

bearing current liabilities

13. Identify and describe the major components that are used to calculate the equity

valuation cash flow.

Equity valuation cash flow = net income + depreciation and amortization expense –

14. Describe how pseudo dividends are used in the equity valuation method.

Pseudo dividend: excess cash not needed for investment in the assets or operations

to carry out the business plan

15. What is the relationship between equity valuation cash flows and dividends?

If you were to project the maximum possible dividend the venture could afford to pay

16. Why do the numerical examples of this chapter involve a large dividend in the last

year of the explicit forecast period?

The large “dividend” (or pseudo dividend in the equity valuation cash flow) derives

17. Why do net income and cash flow in the numerical examples in this chapter both

grow at the same rate (g) in the terminal value period? Why is this important?

18. From the Headlines — Foursquare: What ingredients would you need to conduct a

traditional equity method valuation for Foursquare? If you had the necessary

projections, do you think that they would also suggest the $80 to $100 million

valuations mentioned in the article? Comment on the warnings you would provide to

accompany your projections and valuation if you completed them.

Answers will vary: Ingredients for a traditional equity method valuation include

INTERNET ACTIVITIES

1. Web surfing exercise: Find a fast growth publicly traded firm with financial

statements posted on the firm’s web page. Relate that firm’s financial statements to

those of the examples in this chapter. Formulate the process by which you would

project that firm’s financial statements into the future in order to conduct a valuation.

Web-researched results vary due to constant updating of the related web sites.

EXERCISES/PROBLEMS AND ANSWERS

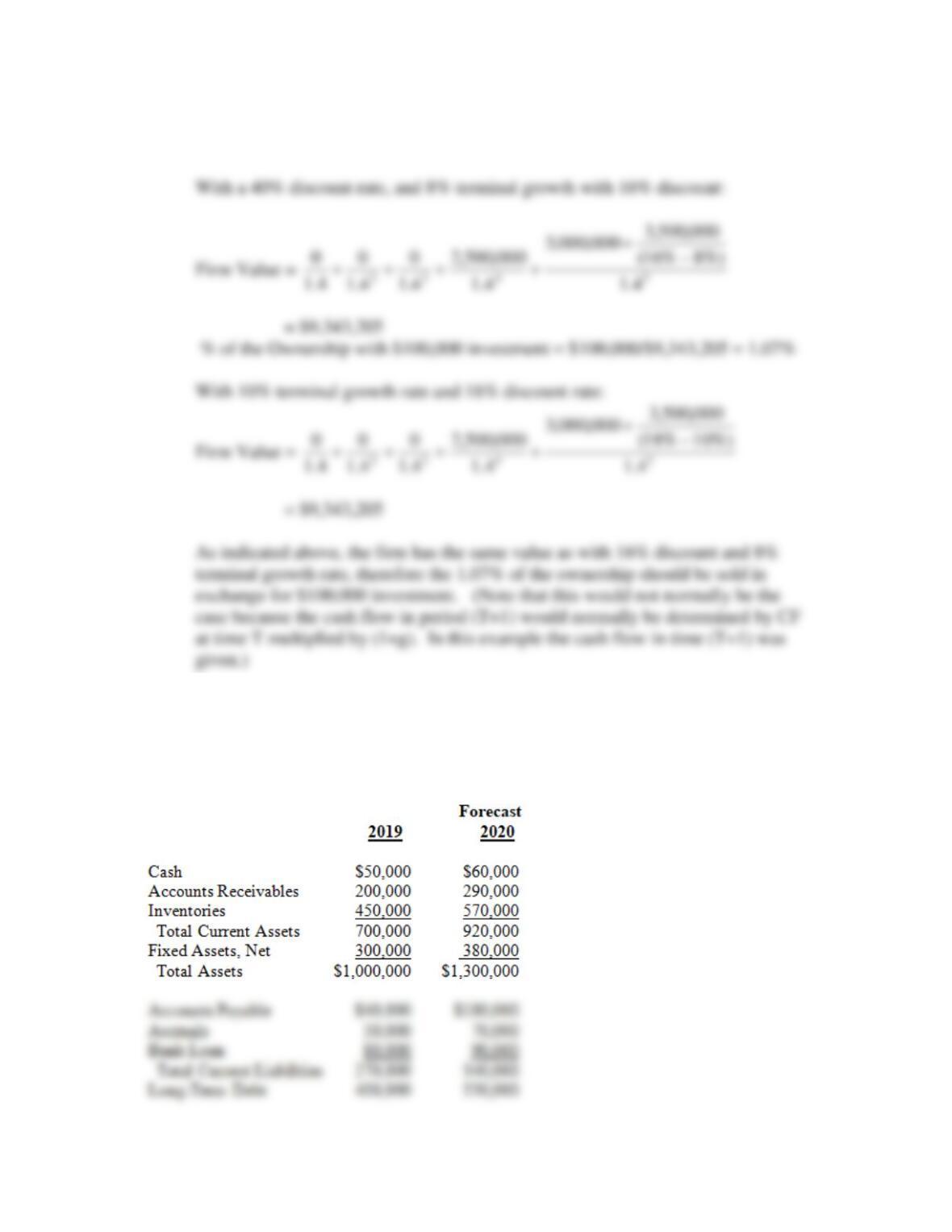

1. [Present Value Valuation Concepts] Assume you sell for $100,000 a 10 percent

ownership stake in a future payment one year from now of $1.5 million.

A. What are you saying about the implied return for the 10 percent owner?

Investment of $100,000 for a dollar return of $150,000 ($1.5 million x .10) one year

Expected venture return = ($1,500,000 – $1,000,000)/$1,000,000 = 50%

B. What is the present value of the entire $1.5 million, using the implied return from Part

A?

PV = $1,500,000/(1.50) = $1,000,000

D. Does it matter whether you grow the $100,000 at 50 percent to $150,000 and note it

is 10 percent of $1.5 million, or discount the $1.5 million at 50 percent to get $1

million and note that $100,000 is 10 percent of this present value?

No. Both approaches provide the same result:

2. [Venture Present Values] The TecOne Corporation is about to begin producing and

selling its prototype product. Annual cash flows for the next five years are forecasted as:

[Note: Following is a spreadsheet solution for Problem 2 (TecOne

Corporation) and Problem 3 (LowTec Corporation).]

TecOne Corporation Solutions

Problem 1

Part A:

Yr 0 Yr 1 Yr 2 Yr 3 Yr 4 Yr 5 Yr 6

Part B:

Yr 0 Yr 1 Yr 2 Yr 3 Yr 4 Yr 5 Yr 6

Annual Cash Flow (50,000) (20,000) 100,000 400,000 800,000 900,000

Part C:

Yr 0 Yr 1 Yr 2 Yr 3 Yr 4 Yr 5 Yr 6

Annual Cash Flow (50,000) (20,000) 100,000 400,000 800,000 900,000

Terminal Value 7,500,000

Total Flow to Discount (50,000) (20,000) 100,000 400,000 8,300,000

Present Value @ 40% $1,637,903.85

LowTec Corporation Solutions

Problem 2

Note: It is assumed that the cash flows in Part C of Problem 1 exist for the LowTec Corporation

Part A:

Yr 0 Yr 1 Yr 2 Yr 3 Yr 4 Yr 5 Yr 6

Annual Cash Flow (50,000) (20,000) 100,000 400,000 800,000 900,000

Terminal Value 8,181,818

A. Assume annual cash flows are expected to remain at the $800,000 level after Year

5 (i.e., Year 6 and thereafter). If TecOne investors want a 40 percent rate of

return on their investment, calculate the venture’s present value.

DCF PV = -$50,000/1.4 + -$20,000/1.42 + $100,000/1.43 + $400,000/1.44 +

[$800,000 + ($800,000/(.4 – .0))]/1.45 = $615,264.47

See TecOne Corporation spreadsheet solution for Part A.

C. Now extend Part B one step further. Assume that the required rate of return on the

investment will drop from 40 percent to 20 percent beginning in Year 6 to reflect

a drop in operating or business risk. Calculate the venture’s present value.

See TecOne Corporation spreadsheet solution for Part C.

3. [Present Value Valuation Concepts] Assume the forecasted cash flows presented in

Problem 2 for the TecOne Corporation venture also hold for the LowTec venture.

However, investors in LowTec have an expected rate of return of 30 percent on their

investment until Year 6 when the rate of return is expected to drop to 18 percent. The

perpetuity growth rate for cash flows after Year 6 is expected to be 7 percent.

4. [Venture Present Values] Ben Toucan, owner of the Aspen Restaurant, wants to

determine the present value of his investment. The Aspen Restaurant is currently in

the development stage but hopes to “begin” operations early next year. After-tax

cash flows during the next five years are expected to be as follows: Year 1 = 0, Year 2

= 0, Year 3 = 0, Year 4 = $2.5 million, and Year 5 = $3 million. Cash inflows are

A. Determine the Aspen BrewPub’s terminal or horizon value at the end of five

years.

Terminal Value =

( )

gr

06.1VCF5

−

+

=

%6%20

000,180,3

−

= 22,714,285.71

B. What is the present value of the Aspen BrewPub?

C. What percent ownership interest should Ben Toucan be willing to give to a

venture investor, Sherri Isitar, for her $1,000,000 investment?

Under the assumption, (consistent with the textbook treatment in Section 9.2) that

the cash flow in years 4 and 5 are fixed and have already incorporated the use of

Some students will assume that the $1,000,000 is not already projected as being

used to generate the $3,880,070.55 “pie.” (This is the type of conjecture that is

5. [Venture Present Value Concepts] Refer to the FrothySlope microbrewery example at

the beginning of this chapter.

A. How does the $500,000 piece of the terminal value relate to the future value of the

$100,000? That is, the brewpub investor was looking for a 40% return. The five-

year-out future value of $100,000 growing at 40% is 100,000*(1.4)5 =$537,824,

slightly more than $500,000. Does this mean the investor is not really expected to

make 40% on the $100,000, even though we used that discount rate to arrive at

the initial $5,856,935 valuation? (Hint: What about explicit forecast period

flows?)

The investor actually does make a 40% return. The $500,000 future value only

B. Returning to the brewpub spreadsheet with all flows included, how much more of

the venture’s ownership of surplus cash flows would have to be sold for the

$100,000 if the investor expected to make 70% (given Jim’s utopian vision of his

future)?

PV of Venture @ 70% discount =

C. What percentage of the brewpub’s present value is contained in the present value

of the terminal value (the venture’s “reversion value”)?

D. How much ownership of the brewpub cash flows would need to be sold to an

investor demanding 40% but agreeing that the mature brewpub venture would

terminally grow at a rate of 8% with a risk profile requiring a discount rate of

16%? What if the terminal growth rate were 10% and the discount rate 18%?

(The spread between the discount rate and the growth rate is sometimes referred

to as the “capitalization rate” for the terminal flows or just the “cap rate.”)

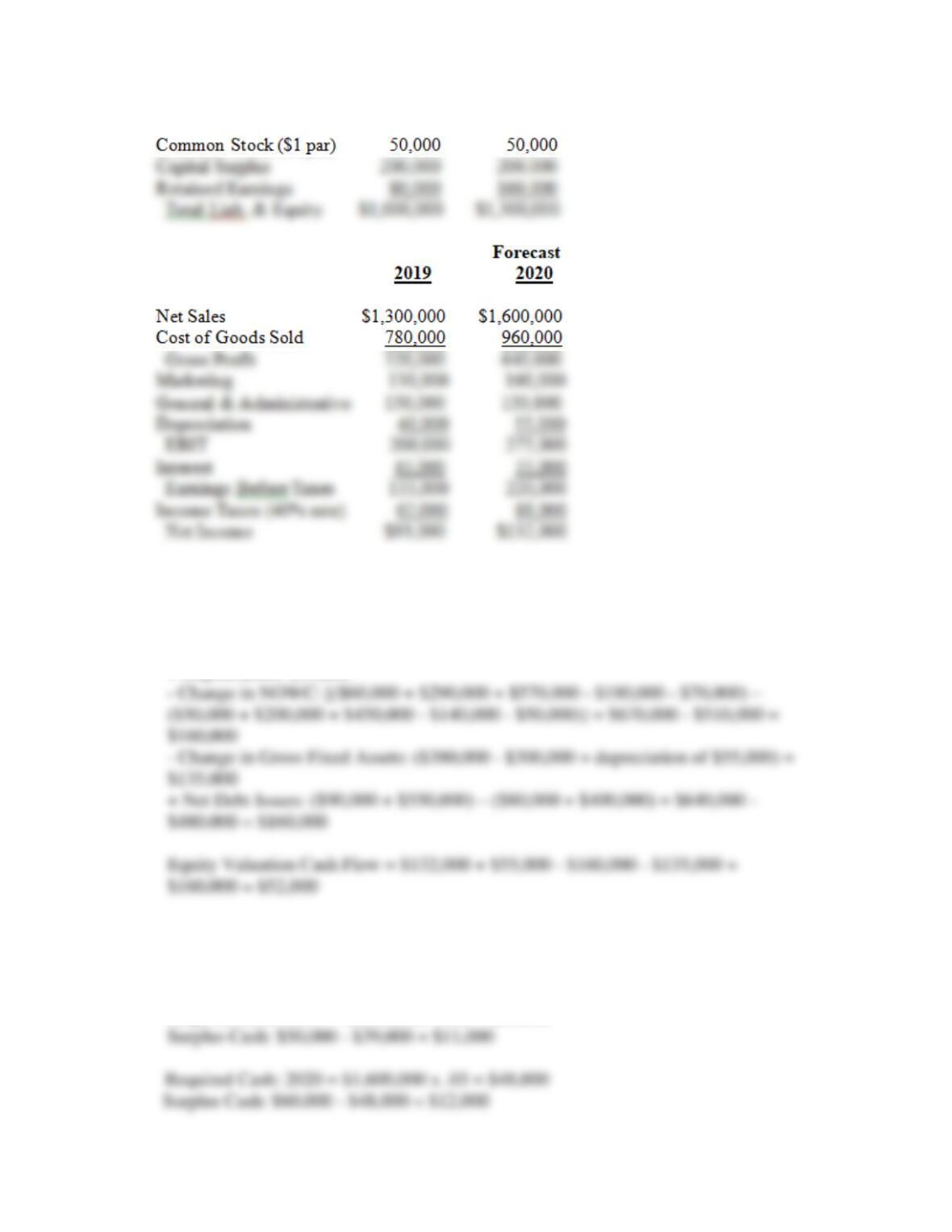

6. [Equity Valuation Cash Flows] Following are financial statements (historical and

forecasted) for the Global Products Corporation.

GLOBAL PRODUCTS CORPORATION

A. Assume that the cash account includes only required cash. Determine the dollar

amount of equity valuation cash flow for 2020.

Equity Valuation Cash Flow =

Net Income: $132,000

B. Now assume that Global Product’s required cash is set at 3 percent of sales. Any

additional cash would be surplus cash. Re-estimate the dollar amount of equity

valuation cash flow for 2020.

Required Cash: 2019 = $1,300,000 x .03 = $39,000

C. Let’s assume that investors in Global Products want to estimate the venture’s present

value at the end of 2019. Forecasted financial statements reflect the stepping stone

year. Cash flows are expected to grow at a perpetual 8 percent annual rate beginning

in 2021. Assume that all cash is required cash as was done in Part A. What is the

Global Products venture’s present value if investors want an annual rate of return of

25 percent?

D. Work with the assumptions in Part B about Global Products required cash being 3

percent of sales. Calculate the present value of the Global Products venture at the

end of 2019 if investors want an annual rate of return of 25 percent and cash flows

are expected to grow at a perpetual 8 percent annual rate beginning in 2021.

Present Value @ 25% = $53,000/(.25 – .08) = $311,764.71

7. Return to the discussion of the FrothySlope venture at the beginning of the chapter.

Formulate an answer for each of the five questions that are posed under the heading

“What Is a Venture Worth?

(1) What are the benefits and disadvantages of his approach to determining the

investor’s percent ownership?

The benefit of Jim’s approach is that it accounted for his sweat equity (in

reality sunk costs,) and that it was a rather simplistic way of looking at the