Linear Programming 269

Alternatively, an addition to secretarial staff would make production possible at point

E. Using the rules for forming the dual linear program, the dual can be written using the

equality form of the constraint conditions as:

Here VA, VB, and VS represent the marginal values of accountant, bookkeeper, and

secretarial time, in dollars. LI and LC represent the excess of input value over output

Taking (4) minus (5),

From (4),

270 Chapter 9

And from the objective function:

The dual solution can be interpreted as follows:

F. Yes, holding all else equal, the firm would be willing to employ additional

P9.9 Revenue Maximization. Designed for Sales (DFS), Inc., an Evanston, Illinois-based

designer of single-family and multifamily housing units for real estate developers,

seeks to determine an optimal mix of output during the current planning period. DFS

offers custom designs for single-family units, Q1, for $3,000 and custom designs for

multifamily units (duplexes, fourplexes, etc.), Q2, for $2,000 each. Both types of

output make use of scarce drafting, artwork, and architectural resources. Each

A. Using the equality form of the constraint conditions, set up the primal linear

program that Benes would use to determine the sales revenue-maximizing

product mix. Also set up the dual.

B. Solve for and interpret all solution values.

C. Would DFS’s optimal product mix be different with a profit-maximization goal

rather than a sales revenue-maximization goal? Why or why not?

P9.9 SOLUTION

A. In determining an optimal weekly product mix, DFS will seek to maximize sales

Creative Accountants, Ltd., LP Graph

160

180

200

Individual

Returns (I)

Accountant

constraint (1)

Bookkeeper

constraint (2)

272 Chapter 9

subject to

Here Q1 and Q2 represent custom designs for single family and multifamily units,

subject to

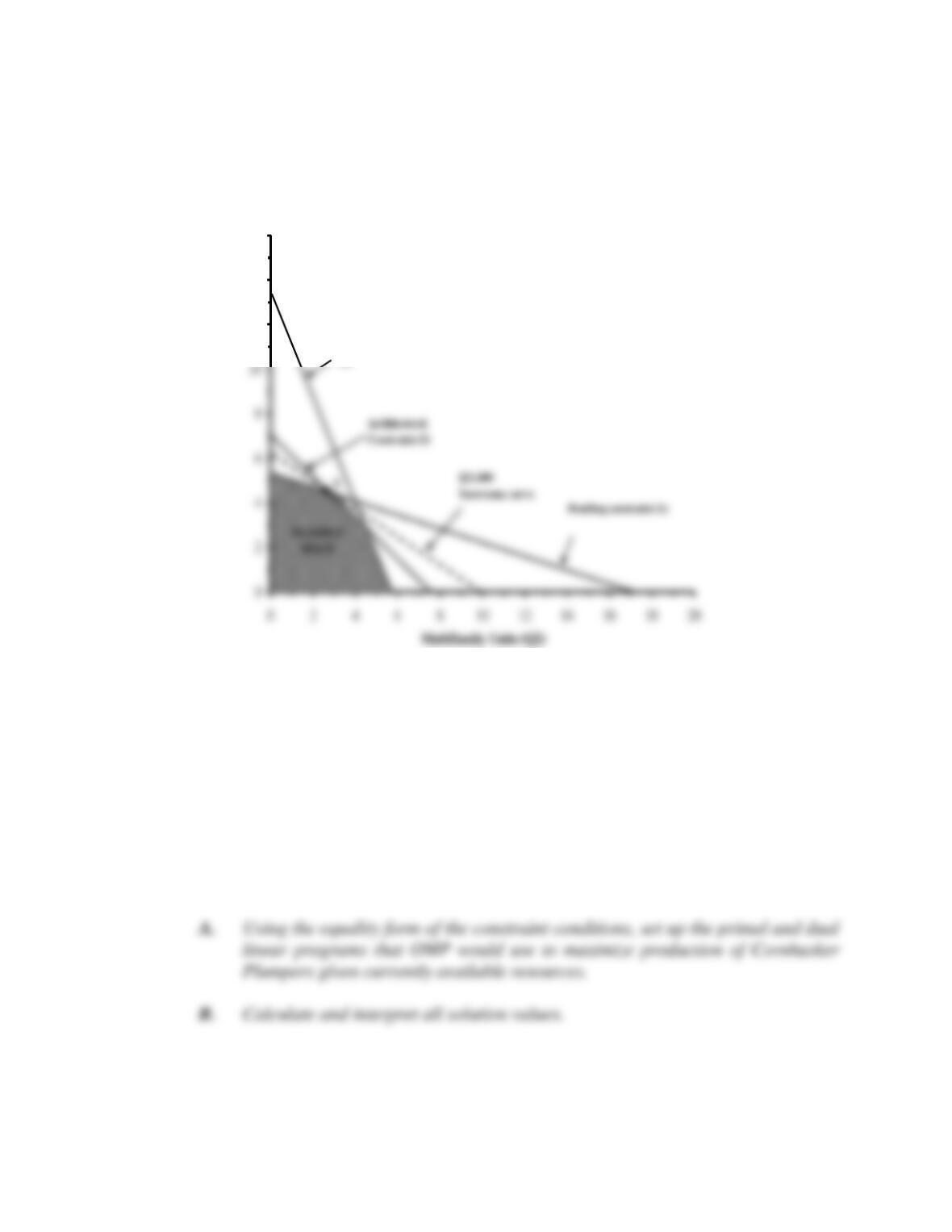

B. By graphing the primal constraints and the highest possible isorevenue line, we find

at the optimal point X that SD = SAR = 0.

Thus,

Linear Programming 273

Taking (1) minus two times (3),

From (1),

From (2),

And finally, from the primal objective function:

The dual can be solved directly, given these solutions to the primal problem.

Because Q1, Q2 and SA are all nonzero-valued in the solution to the primal problem,

274 Chapter 9

From (4),

And finally, from the dual objective function:

Summarizing from above, the solution to the primal linear programming problem and

an interpretation of these values is:

Dual solution values can be interpreted as follows:

Linear Programming 275

C. Whether or not this optimal product mix would change with a goal of profit rather

than sales maximization depends upon the nature of variable costs. The optimal

P9.10 Optimal Output. Omaha Meat Products (OMP) produces and markets Cornhusker

Plumpers, an extra-large frankfurter product being introduced on a test market basis

into the St. Louis, Missouri, area. This product is similar to several others offered

by OMP, and it can be produced with currently available equipment and personnel

using any of three alternative production methods. Method A requires 1 hour of

labor and 4 processing-facility hours to produce 100 packages of plumpers, one unit

of QA. method B requires 2 labor hours and 2 processing-facility hours for each unit

of QB, and Method C requires 5 labor hours and 1 processing-facility hour for each

unit of QC. Because of slack demand for other products, OMP currently has 14 labor

hours and 6 processing-facility hours available per week for producing Cornhusker

Plumpers. Cornhusker Plumpers are currently being marketed to grocery retailers

at a wholesale price of $1.50 per package, and demand exceeds current supply.

C. Should OMP expand its processing-facility capacity if it can do so at a cost of

$40 per hour?

Designed For Sales, Inc.

12

14

16

Single Family

Units (Q1)

Artwork Constraint

(2)

Linear Programming 277

D. Discuss the implications of a new union scale calling for a wage rate of $20

per hour.

P9.10 SOLUTION

A. In determining an optimal use of its resources, Omaha will seek to maximize output,

subject to limitations on scarce labor and production facilities. Thus, the relevant

primal linear programming problem can be written, in equality form, as:

Here QA, QB and QC are the amounts produced using each alternative production

technique. SL and SP are the amounts of excess capacity in labor and production

Here VL and VP are the marginal values of labor and production facility time

278 Chapter 9

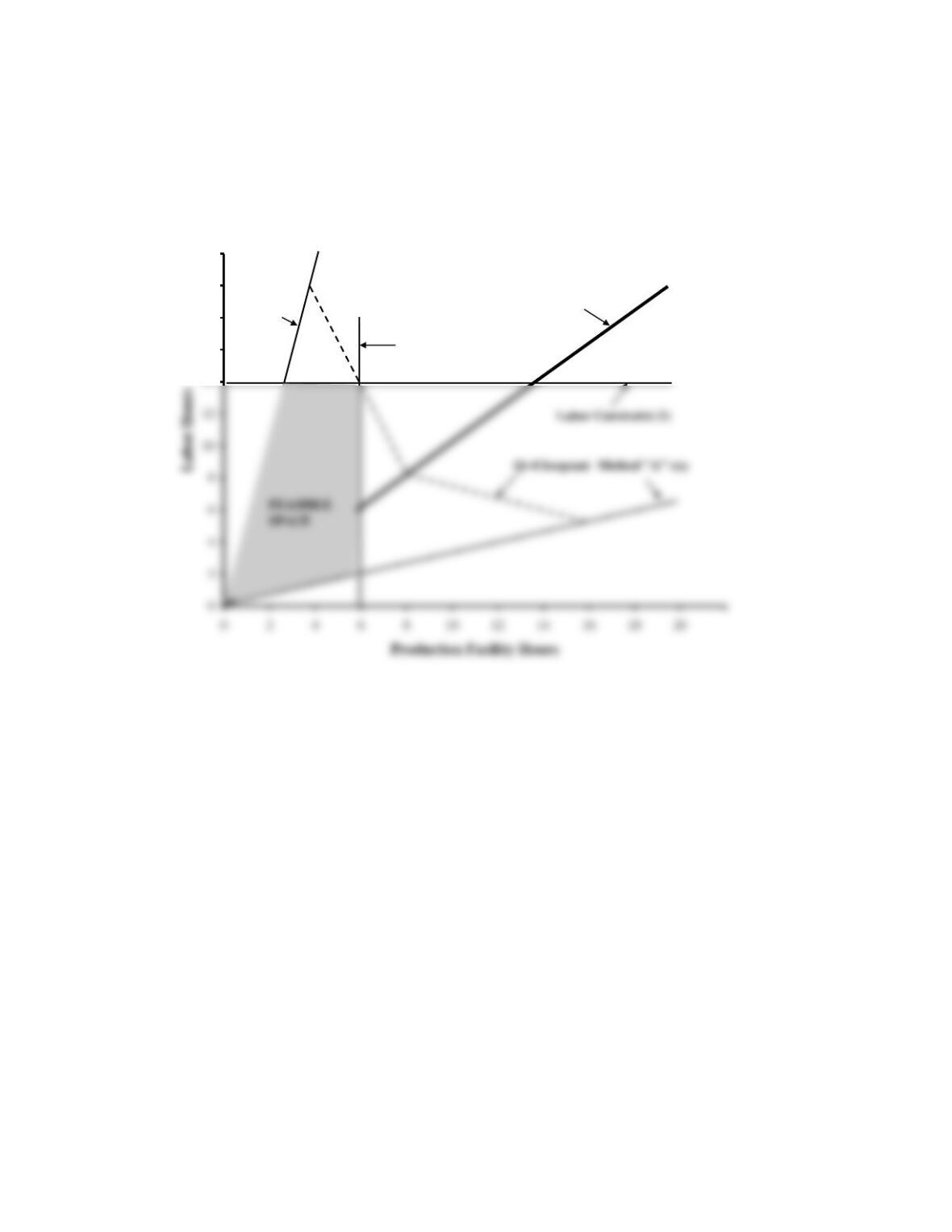

B. From the primal graph, we see that the maximum output level will be reached on the

Take (1) minus (2),

From (1),

Then, from the objective function:

From the primal solution values, we know that VL > 0 and VP > 0 because SL = SP =

Take (4) minus two times (5),

Linear Programming 279

From (3),

Then, from the dual objective function:

Summarizing from above, primal solutions and an interpretation of these values are

as follows:

Dual solution values can be interpreted as follows:

280 Chapter 9

D. The marginal value of labor in dollars can be calculated as illustrated above:

282 Chapter 9

Omaha Meat Products, Inc.

16

18

20

22

Method

“C” ray

Processing facility

constraint (2)

Method “B” ray

Q*

Linear Programming 283

CASE STUDY FOR CHAPTER 9

LP Pension Funding Model

Several companies have learned that a well-funded and comprehensive employee benefits

package constitutes an important part of the compensation plan needed to attract and retain key

personnel. An employee stock ownership plan, profit-sharing arrangements, and deferred

compensation to fund employee retirement are all used to allow productive employees to share in

the firm’s growth and development. Among the fringe benefits offered under the cafeteria-style

promised benefits.

Over time, numerous firms have found it increasingly difficult to forecast the future rate

of return on invested assets, the future rate of inflation, and the morbidity (death rate) of young,

healthy, active retirees. As a result, several organizations have discontinued traditional defined

benefit pension plans and instead have begun to offer new “defined contribution” plans. A

record as a liability any earned but not funded pension obligations. Unfunded pension liabilities

caused gigantic one-time charges against operating income during the early 1990s for AT&T,

General Motors, IBM, and a host of other large corporations. Faced with enormous one-time

charges during an initial catch-up phase, plus the prospect of massive and rapidly growing

retirement expenses over time, many large and small firms have simply elected to discontinue

284 Chapter 9

benefit of defined contribution compensation plans is that individual workers can allocate

pension investments according to individual risk preferences. Older workers who are extremely

risk averse can focus their investments on short-term government securities; younger and more

venturesome employees can devote a larger share of their retirement investment portfolio to

common stocks.

Workers appreciate companies that offer flexible defined contribution pension plans and

closely related profit-sharing and deferred compensation arrangements. To maximize plan

benefits, firms must make modest efforts to educate and inform employees about retirement

income needs and objectives. Until recently, compensation consultants suggested that employees

could retire comfortably on a retirement income that totaled 80 percent of their final salary.

6.4 percent per year; the real return on bonds is only 0.5 percent per year. Indeed, over every

30-year investment horizon during that time interval, stocks have beat short-term bonds (money

market instruments) and long-term bonds. The added return from common stocks is the

predictable reward for assuming the greater risks of stock-market investing. However, to be

sure of earning the market risk premium on stocks, one must invest in several different

companies (at least 30) for several years. For most pension plans, investments in no-load low-

expense common stock index funds work best in the long run. However, bond market funds have

a place in some pension portfolios, especially for those at or near the retirement age.

To illustrate the type of retirement income funding model that a company might make

available to employees, consider the following scenario. Suppose that an individual employee

has accumulated a pension portfolio worth $250,000 and hopes to receive initial post-retirement

income of $500 per month, or $6,000 per year. To provide a total return from current income

Linear Programming 285

percent plus 1.5 percent, 4 percent plus 1 percent for medium-term tax-exempt bonds, and 4.5

percent plus 0 percent for money market instruments. Also assume that the effective marginal

tax rate is 30 percent.

A. Set up the linear programming problem that a benefits officer might use to determine the

total-return maximizing allocation of the employee’s pension portfolio. Use the

inequality forms of the constraint conditions.

CASE STUDY SOLUTION

A. The linear programming problem that a benefits officer might use to determine the total–

return maximizing allocation of the employee’s pension portfolio appears as follows:

(1) CS – LG = 25% (Growth constraint)

A LP Pension Plan Funding Model

Asset

Before-tax

yield

After-tax

yield

Capital

Appreciation

Amount

invested

Percent

invested

Before-tax

income

After-tax

income

Common Stocks

3.50%

2.45%

6.50%

$125,000

50.00%

$4,375

$3,063

Linear Programming 287

C. The amount of unrealized capital gain earned per year on this investment portfolio can be

D. The amount of after-tax income generated at the optimal solution shown in part A is